- The monetary policy decision of the Federal Reserve is expected to reinforce the institution's cautious stance as it carries out its interest rate cutting cycle this year, which may foster the American interest rate differential and the USD.

- COPOM is expected to cut the basic interest rate (SELIC) by 0.50 p.p., harming the Brazilian interest rate differential and weakening the BRL.

- Friction between the Executive and the Legislative could hinder the acquisition of new revenues for the government this year. It would increase the perception of fiscal risks of Brazilian assets, weakening the BRL.

- US Economic data may suggest that economic activity in the country is slowly slowing down, increasing bets for interest rate cuts by the Fed and weakening the dollar.

The week in review

The week was marked by the release of the American Gross Domestic Product for the fourth quarter, stronger than anticipated, along with moderate inflation data, reinforcing the perceptions that the country is heading for a soft landing. However, it did not change the bets that the Federal Reserve should not start cutting interest rates before May.

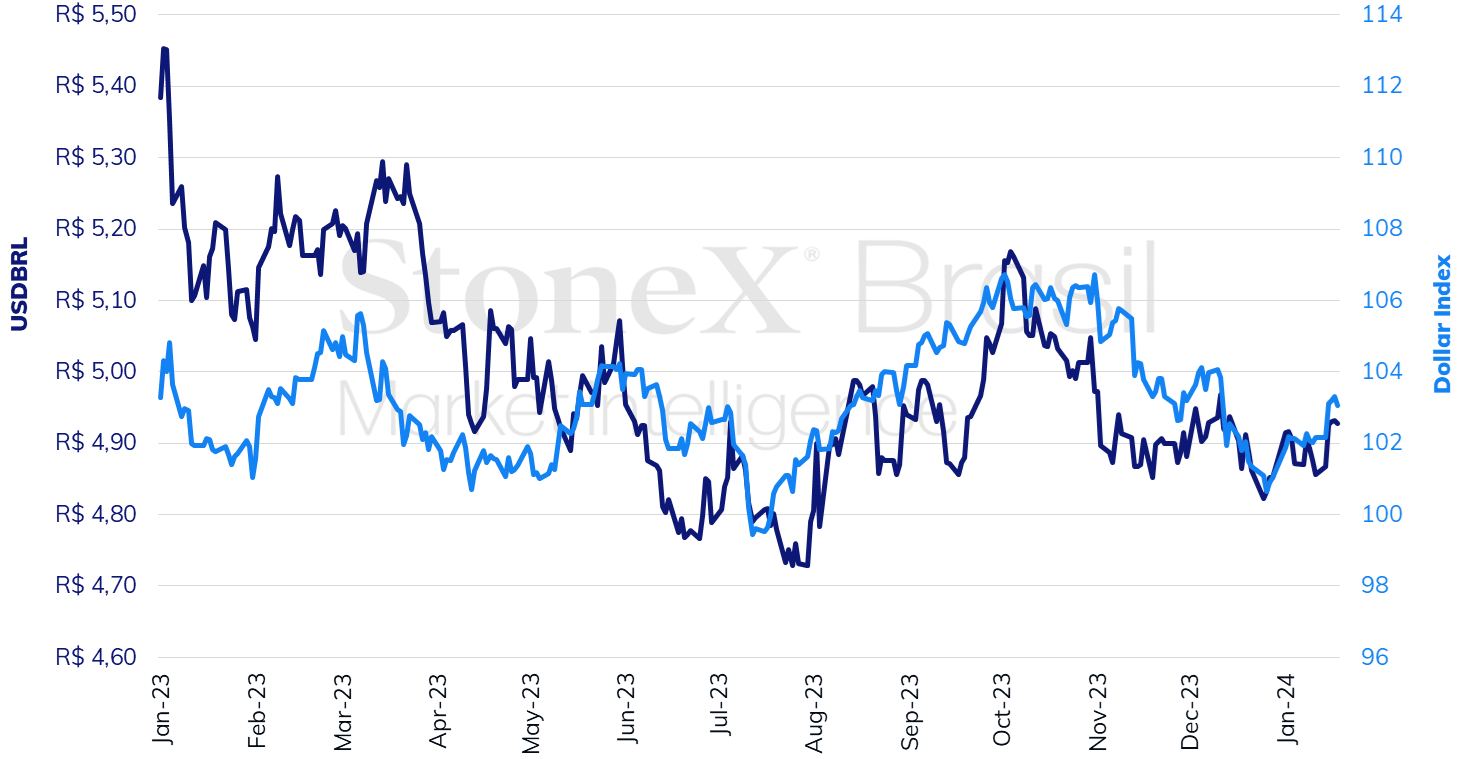

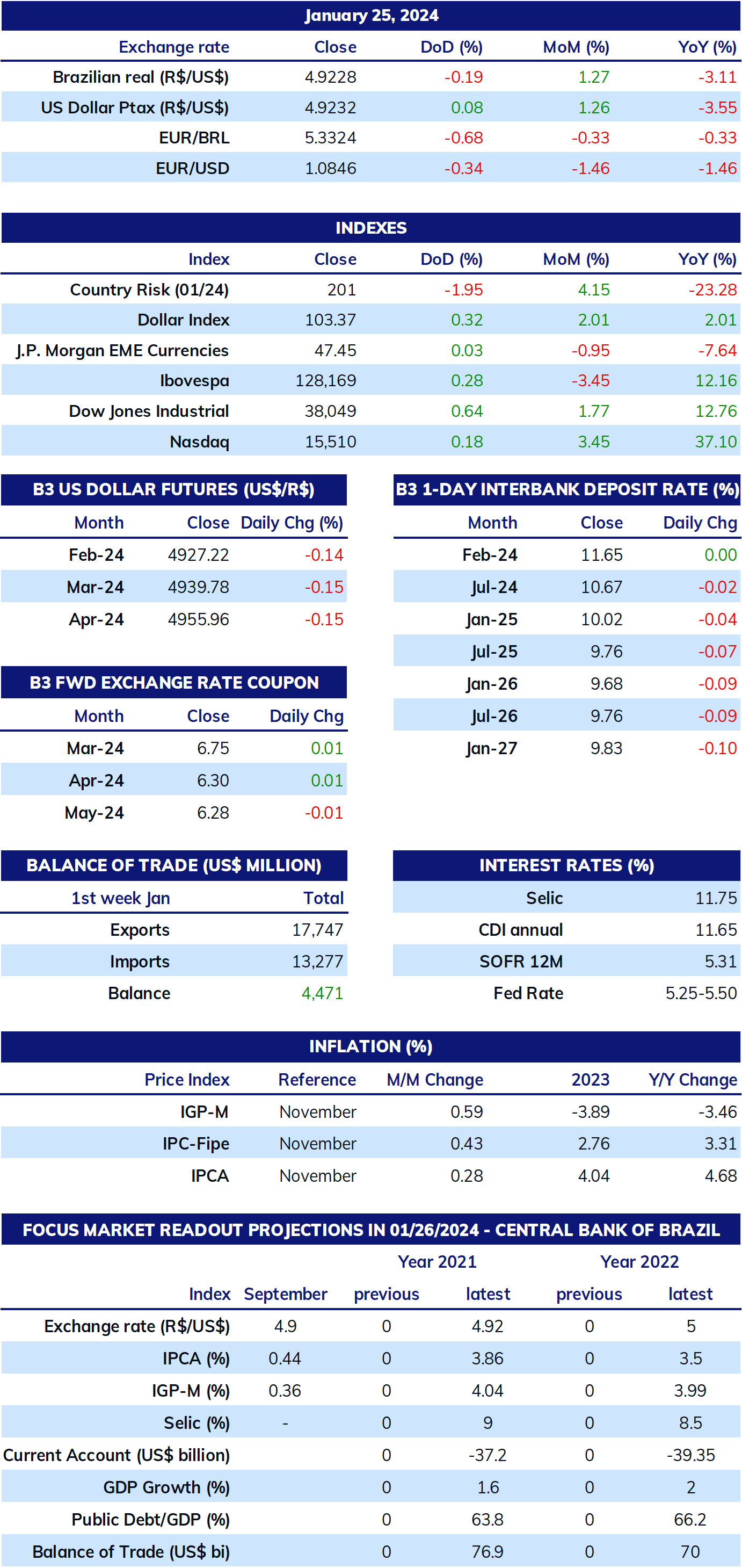

The USDBRL ended the week lower, closing Friday's session (26) at BRL 4.911, a variation of -0.3% for the week, +1.2% for the month, and +1.2% for the year. The dollar index closed Friday's session at 103.2 points, a weekly gain of 0.2%, a monthly gain of 2.2%, and an annual gain of 2.2%.

THE MOST IMPORTANT EVENT: Federal Reserve monetary policy decision

Expected impact on USDBRL: bullish

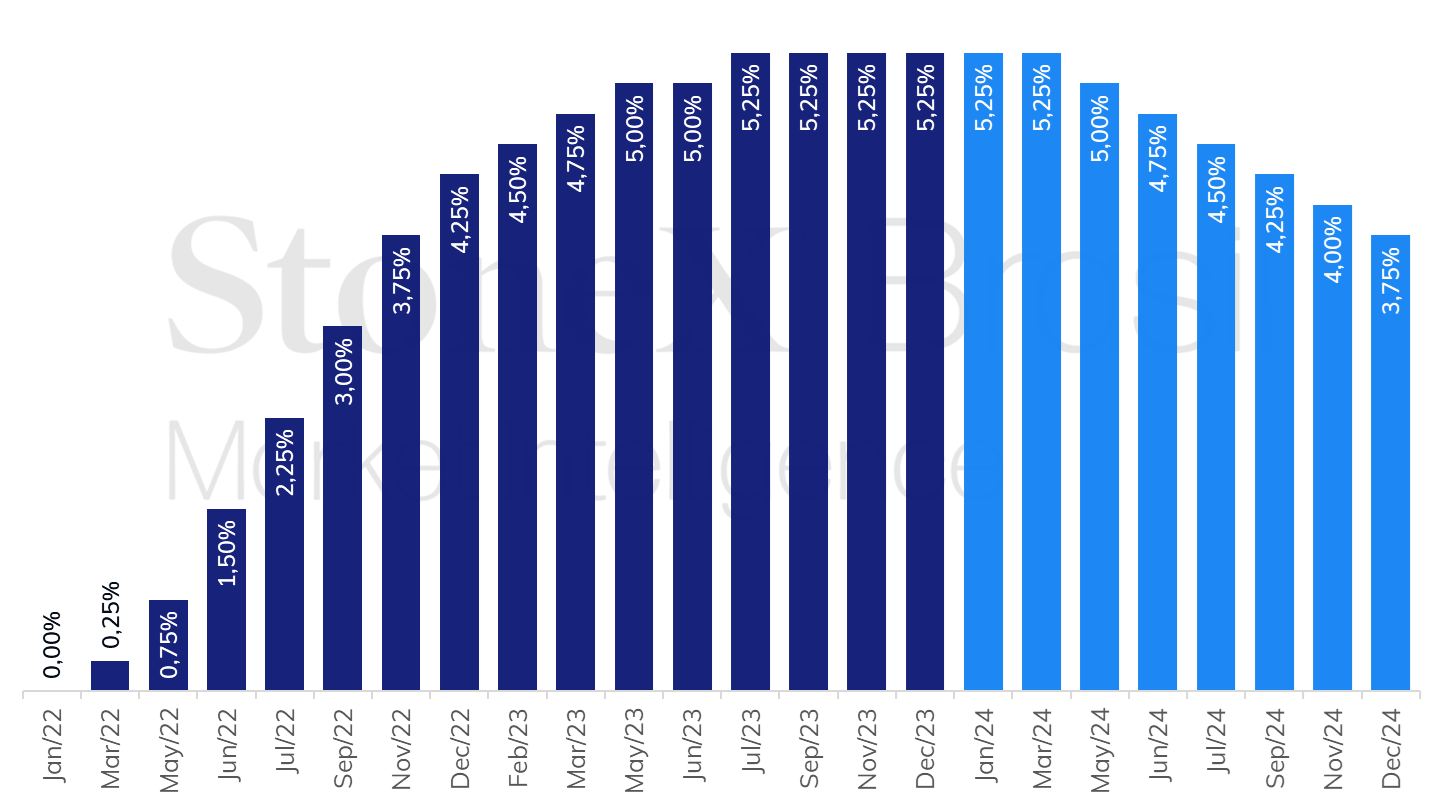

There is virtually consensus that the FOMC should keep the American basic interest rate unchanged, between 5.25% and 5.50% per year. The decision statement should seek to maintain the flexibility of monetary policy options for the future, stating that interest rates still need to be kept stable for longer to ensure monetary stability and that it is still not possible to know when a cycle of interest rate cuts by the Federal Reserve would begin. The Fed should reaffirm the importance of the evolution of economic indicators for decision-making at each meeting, trying to curb the possibility of reducing the basic rate in March without excluding it from the range of options.

After practically all indicators for December presented data more heated than anticipated and coordinated speeches by several Federal Reserve members preaching caution, the bets in the futures market for interest rates finally predict the maintenance of the FOMC decision in March. However, from this point forward, a perception of optimism prevails among traders, with bets on cuts in all decisions until the end of 2024 - something that would only be compatible with a rapid stabilization of American prices or a rapid decline in productive activity.

COPOM monetary policy decision

Expected impact on USDBRL: bullish

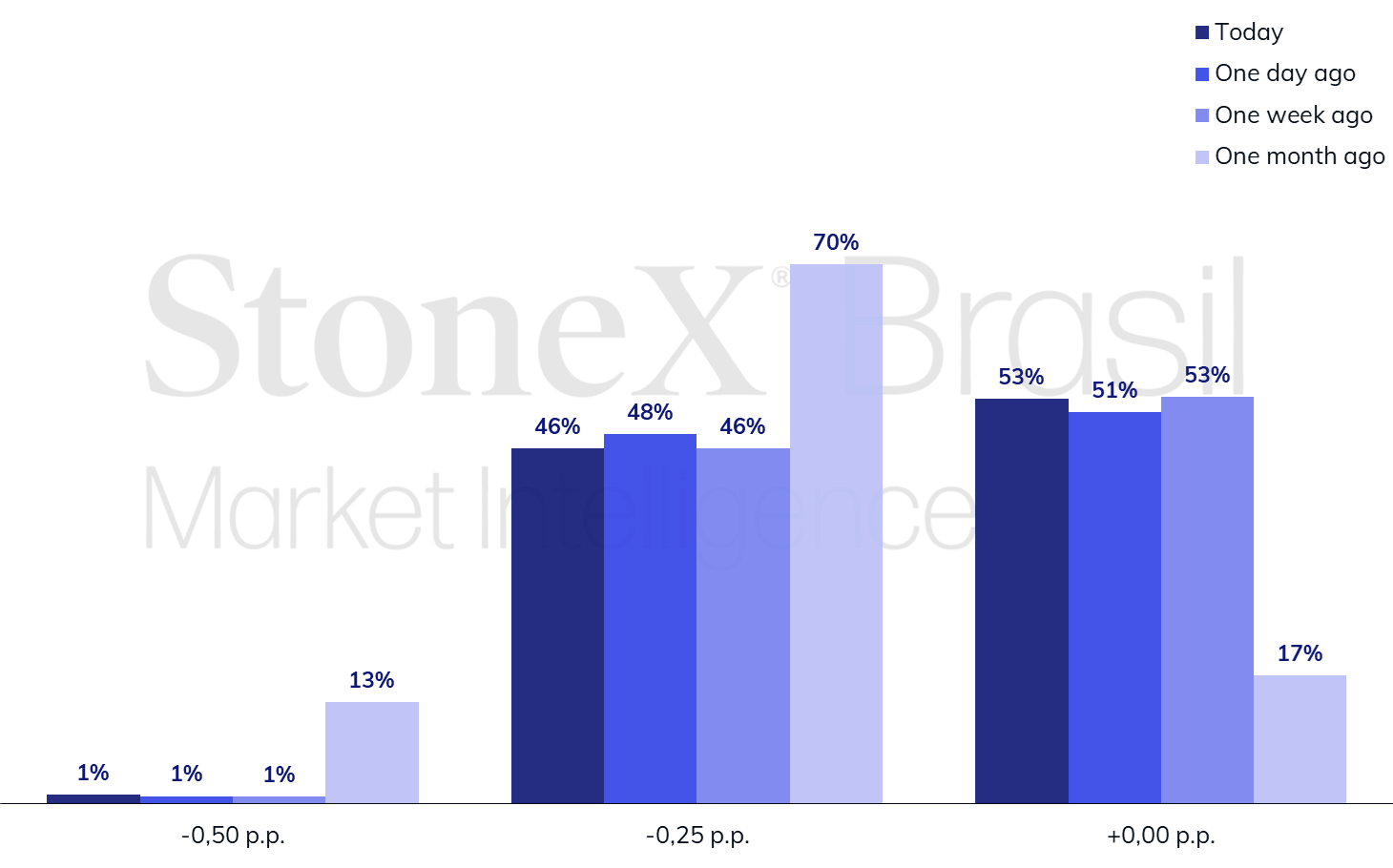

The Central Bank of Brazil's Monetary Policy Committee (COPOM) is expected to reduce the basic interest rate (SELIC) by 0.50 p.p., from 11.75% p.a. to 11.25% p.a. next Wednesday, according to its latest signal that it would repeat cuts of "the same magnitude in the next meetings." In recent months, inflation rates have risen slightly without threatening the longer-term trends of moderation. Still, an important warning about service inflation showed a sharp increase in the IPCA in November and December and the IPCA-15 in January. Therefore, investors should follow the decision statement to assess whether there will be any change in the inflationary risk balance or its guidance on the next steps.

Data on the American economy

Expected impact on USDBRL: bearish

The median of expectations for job creation shows a slight reduction, from a positive balance of 216 thousand in December to 178 thousand in January, with a slight increase in the unemployment rate, from 3.7% to 3.8% in the period. These indicators would be consistent with the interpretation of a "soft landing," in which productive activity and the labor market remain resilient to the monetary tightening carried out by the Federal Reserve while inflation rates show gradual moderation.

Friction between the Executive and the Legislative branches

Expected impact on USDBRL: bullish

The National Congress does not officially return from recess until Friday (05). Still, the work of the legislature members should start earlier this week due to the intense stress caused by the recent initiatives of the Executive. Specifically, during the parliamentary recess, the government issued on December 29 the Provisional Measure (PM) proposing the payroll tax reinstatement after the Legislative branch established the renewal of subsidies for 17 sectors for another four years and vetoed on Monday (22) the committee amendments, totaling R$ 5.6 billion. There is a high and explicit dissatisfaction among the parliamentarians of both Houses, which should impose difficulties on the government's agenda progress at the beginning of this year.

The StoneX Group Inc. group of companies provides financial services worldwide through its subsidiaries, including physical commodities, securities, exchange-traded and over-the-counter derivatives, risk management, global payments and foreign exchange products in accordance with applicable law in the jurisdictions where services are provided. References to over-the-counter (“OTC”) products or swaps are made on behalf of StoneX Markets LLC (“SXM”), a member of the National Futures Association (“NFA”) and provisionally registered with the U.S. Commodity Futures Trading Commission (“CFTC”) as a swap dealer. SXM’s products are designed only for individuals or firms who qualify under CFTC rules as an ‘Eligible Contract Participant’ (“ECP”) and who have been accepted as customers of SXM. StoneX Financial Inc. (“SFI”) is a member of FINRA/NFA/SIPC and registered with the MSRB. SFI is registered with the U.S. Securities and Exchange Commission (“SEC”) as a Broker-Dealer and with the CFTC as a Futures Commission Merchant and Commodity Trading Adviser. References to securities trading are made on behalf of the BD Division of SFI and are intended only for an audience of institutional clients as defined by FINRA Rule 4512(c). References to exchange-traded futures and options are made on behalf of the FCM Division of SFI . StoneX is a trading name of StoneX Financial Ltd (“SFL”). SFL is registered in England and Wales, Company No. 5616586. SFL is authorized and regulated by the Financial Conduct Authority [FRN 446717] to provide to professional and eligible customers including: arrangement, execution and, where required, clearing derivative transactions in exchange traded futures and options. SFL is also authorised to engage in the arrangement and execution of transactions in certain OTC products, certain securities trading, precious metals trading and payment services to eligible customers. SFL is authorised & regulated by the Financial Conduct Authority under the Payment Services Regulations 2017 for the provision of payment services. SFL is a category 1 ring-dealing member of the London Metal Exchange. In addition SFL also engages in other physically delivered commodities business and other general business activities which are unregulated and not required to be authorised by the Financial Conduct Authority. StoneX Group Inc. acts as agent for SFL in New York with respect to its payments services business. StoneX APAC Pte. Ltd. acts as agent for SFL in Singapore with respect to its payments services business. ‘StoneX’ is the trade name used by StoneX Group Inc. and all its associated entities and subsidiaries.

Trading swaps and over-the-counter derivatives, exchange-traded derivatives and options and securities involves substantial risk and is not suitable for all investors. Past performance of any futures or option is not indicative of future success. Indicators are not a trading system and are not published as a specific trade recommendation. The information herein is not a recommendation to trade nor investment research or an offer to buy or sell any derivative or security. It does not take into account your particular investment objectives, financial situation or needs and does not create a binding obligation on any of the StoneX group of companies to enter into any transaction with you. You are advised to perform an independent investigation of any transaction to determine whether any transaction is suitable for you. No part of this material may be copied, photocopied or duplicated in any form by any means or redistributed without the prior written consent of StoneX Group Inc.

© 2024 StoneX Group Inc. All Rights Reserved.

Discover more insights