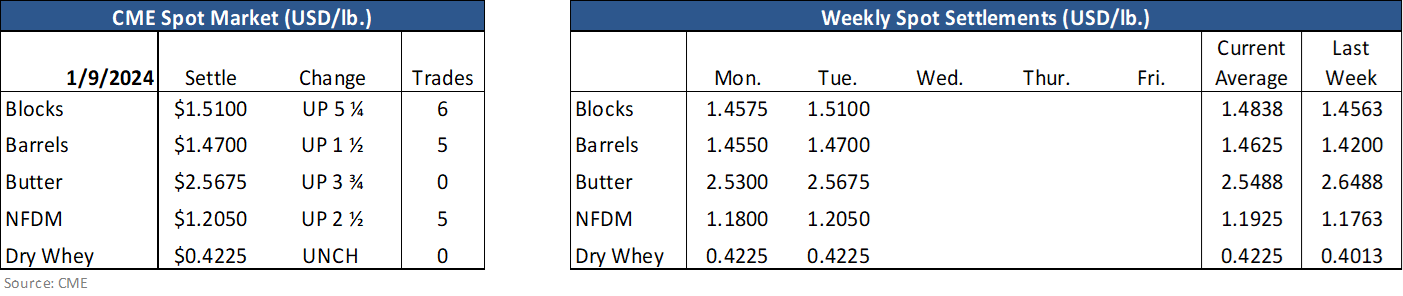

Class III, Cheese and Dry Whey futures all pushed higher Tuesday on what appears to be new buying interest. Spot cheese continued to firm pushing higher for most of the 10-minute session without trading. It was only near the end of the trade that sellers plunked bids resulting in 6 block and 5 barrel trades before the close. Fresh cheese is reportedly still readily available in the country. The question we will sort out in the coming weeks given that the spot price appears to be changing direction and becoming more well-supported is: will there be a desire by end-users (both domestic and potentially for export) to become more aggressive buyers (to perhaps refill their pipelines) if fear of missing out sets in?

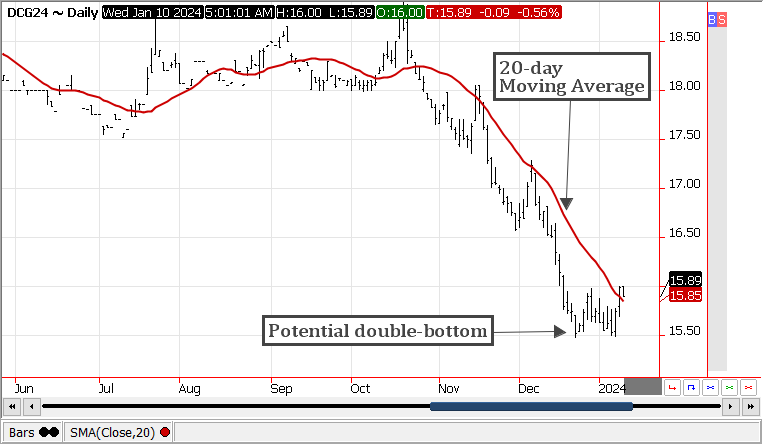

The late session spot selling did stunt some of the nearby Class III and Cheese strength, but only briefly. Buyers appear ready to buy any dips. At least that was the case yesterday. For now, however, the nearby Class III/Cheese contracts more broadly appear to be reverting to the 20-day moving average – an area markets like to chop around once in play.

To get a better look, the chart below is of lead Class III futures month of February 2024. The overall trend remains down. That said, despite the premium to spot and still rather bearish overall market sentiment there remains solid underpinning support for the February contract (as well as other contracts in 1H). In fact, of the 1,915 Class III contracts that traded yesterday, 1,004 changed hands in February alone.

Spot Butter also pushed higher yesterday – up 3.75 cents to $2.5675 on zero trades, 5 bids left unfilled. As we mentioned in yesterday’s report, the market remains ranged-bound between $246.000 and $267.000 for now. Butter futures erased much if not all of the prior day’s losses on 240 contracts of trade volume and open interest up by 43 contracts. There continues to be a rather steady supply of buy side interest on 2024 futures with burgeoning concerns from a still somewhat tight AA salted market to future milk and cream supply. Despite retail sales projected to have been slow in December, the butter market continues to defy expectations of more sustainable price weakness.

Speaking of price weakness, NFDM futures was the only dairy product to close mostly lower Tuesday. Even spot NFDM moved higher (up 2.5 cents to $120.500 on 5 trades. NFDM futures still has a rather healthy forward curve premium to spot and there remains to be little in the way of excitingly bullish news at the moment, which cleared the way for a lighter 111 contracts of trade volume yesterday (OI up 53). Market conditions for NFDM futures remains sideways at the moment.

The USDA will release a slew of reports on Friday at 11 AM Central including the USDA WASDE, Crop Production, Quarterly Grain Stocks, and Winter Wheat Seedings. The Reuters survey of analysts estimates 2023/24 World soybean carryout at 111.58 MMT—close to 3 MMT lower than the December WASDE report. The trade expected World corn carryout to land at 313.03 on the January WASDE—down from 315.22 on the December report.

The USDA will also release its final production estimates of the 2023 fall harvest. The trade expects the USDA to keep corn and soybean yields the same while slightly lowering acreage leading to a small expected decline in production. The average trade guess for U.S. soybean production is 4.127 billion bushels. Corn is expected to be pegged at 15.226 billion bushels for the 2023/24 marketing year.

The StoneX Group Inc. group of companies provides financial services worldwide through its subsidiaries, including physical commodities, securities, exchange-traded and over-the-counter derivatives, risk management, global payments and foreign exchange products in accordance with applicable law in the jurisdictions where services are provided. References to over-the-counter (“OTC”) products or swaps are made on behalf of StoneX Markets LLC (“SXM”), a member of the National Futures Association (“NFA”) and provisionally registered with the U.S. Commodity Futures Trading Commission (“CFTC”) as a swap dealer. SXM’s products are designed only for individuals or firms who qualify under CFTC rules as an ‘Eligible Contract Participant’ (“ECP”) and who have been accepted as customers of SXM. StoneX Financial Inc. (“SFI”) is a member of FINRA/NFA/SIPC and registered with the MSRB. SFI is registered with the U.S. Securities and Exchange Commission (“SEC”) as a Broker-Dealer and with the CFTC as a Futures Commission Merchant and Commodity Trading Adviser. References to securities trading are made on behalf of the BD Division of SFI and are intended only for an audience of institutional clients as defined by FINRA Rule 4512(c). References to exchange-traded futures and options are made on behalf of the FCM Division of SFI . StoneX is a trading name of StoneX Financial Ltd (“SFL”). SFL is registered in England and Wales, Company No. 5616586. SFL is authorized and regulated by the Financial Conduct Authority [FRN 446717] to provide to professional and eligible customers including: arrangement, execution and, where required, clearing derivative transactions in exchange traded futures and options. SFL is also authorised to engage in the arrangement and execution of transactions in certain OTC products, certain securities trading, precious metals trading and payment services to eligible customers. SFL is authorised & regulated by the Financial Conduct Authority under the Payment Services Regulations 2017 for the provision of payment services. SFL is a category 1 ring-dealing member of the London Metal Exchange. In addition SFL also engages in other physically delivered commodities business and other general business activities which are unregulated and not required to be authorised by the Financial Conduct Authority. StoneX Group Inc. acts as agent for SFL in New York with respect to its payments services business. StoneX APAC Pte. Ltd. acts as agent for SFL in Singapore with respect to its payments services business. ‘StoneX’ is the trade name used by StoneX Group Inc. and all its associated entities and subsidiaries.

Trading swaps and over-the-counter derivatives, exchange-traded derivatives and options and securities involves substantial risk and is not suitable for all investors. Past performance of any futures or option is not indicative of future success. Indicators are not a trading system and are not published as a specific trade recommendation. The information herein is not a recommendation to trade nor investment research or an offer to buy or sell any derivative or security. It does not take into account your particular investment objectives, financial situation or needs and does not create a binding obligation on any of the StoneX group of companies to enter into any transaction with you. You are advised to perform an independent investigation of any transaction to determine whether any transaction is suitable for you. No part of this material may be copied, photocopied or duplicated in any form by any means or redistributed without the prior written consent of StoneX Group Inc.

© 2024 StoneX Group Inc. All Rights Reserved.

Discover more insights