As Volatility Cools Does Trade Data, Magnificent 7 Earnings and NFPs Pose a Threat to Calm?

Market conditions seem to have settled further this past week, but a busy week of event risk including US GDP and NFPs represents a significant threat of reigniting disruptive themes.

Key Talking Points:

A recent rebound in markets and ease in volatility doesn’t fully offset lingering fears for growth amid trade wars

Trade and manufacturing data will given a tangible connection to the pain accumulating from choked globalization

Mag 7 earnings will pair forecast with market weigh while NFPs will direct monetary policy expectations…and Trump’s criticisms

Market Conditions Show Some Relief but Concern Remains

Market conditions seem to have settled further this past week. Risk-leaning benchmarks like the S&P 500 and high-yield assets extended their recovery, while measures of fear like the VIX index further dropped to lows last seen back on the United States’ ‘liberation day’ and recent favorites for hedging such as gold finally crested. These tide changes reflect conditional adaptations that will likely translate into greater resistance to sudden directional changes and dramatic runs. That said, it will likely take weeks of quiet and policy reversals to return to the resolute confidence – or deep complacency, depending on what perspective you take – that saw the market ride over most fundamental waves through the first two months of the year. Should we expect calm to persist that long without stirring up any of the deeper waters of uncertainty like broader trade wars, tangible evidence of recession or monetary policies that unnerve in one way or another? As the saying goes: an ounce of prevention is a worth a pound of cure. It is worth remaining diligent, and where necessary, lower risk.

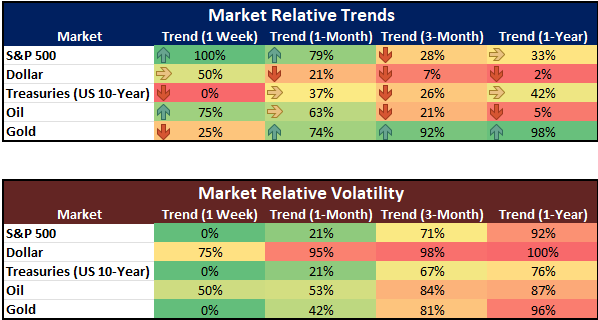

Table of Relative Market Trend and Volatility Over Different Time Frames

Source: John Kicklighter

Looking out over the economic docket of the coming week, we are faced with a situation in where there is such an abundance of high-profile and thematically-relevant event risk that the weight of anticipation for the next release on tap may end up muting the response to day-of fundamental surprises. Overall, there are four general categories of event risk that can generate a significant resonance across the speculative masses should they align to enthusiasm or fear. Economic activity would seem the most prominent run with GDP readings for major economies as well as China’s April PMIs. Earnings will also hit its zenith for the session with the bulk of the ‘Magnificent 7’ reporting after hours on Wednesday and Thursday. Perhaps a little more obtuse from the calendar is the tangible data checking into the effects of the trade war that has built prominence amid key players the past two months. And, coming in a little more under the radar will be monetary policy which seems more target of fundamental developments than the initial mover it can often play through BOJ rate decision and the data on the Federal Reserve’s dual mandates.

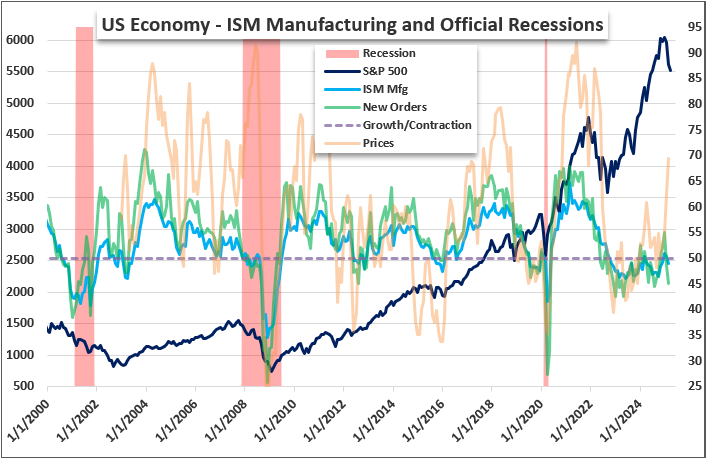

Working chronologically, the first theme to consider for a comprehensive market overview in the week ahead is the update on trade wars. Of course, data that centers on the massive scale of levies between the United States and China would carry the most weight, but the latter’s data is taken with a grain a salt and the heaviest moves were made in recent weeks which means the results of the impact via lagging economic data is probably some weeks away. In the meantime, the more direct measures from the North American neighbors will offer a more objective picture.

The US ISM manufacturing report for April will carry greater weight than the S&P Global figures owing to its more closely watched detail components such as employment, new orders and inflation. For Canada, the April PMI figure is due with an update on factory health with the slow burn of deteriorated trade relationships with its largest trade partner, but the Canadian election is likely to also prove a statement in the future of relations between then two. And then there is Mexico’s update across March trade and April business confidence all against the backdrop of an outlook of possible recession according to the IMF’s recent growth forecast updates.

Chart of S&P 500, ISM Manufacturing Activity, New Orders and Prices (Monthly)

Source: John Kicklighter, ISM Manufacturing

Mag 7 Earnings Carry Forecast Power, Trade Insights and Consequence

As the week continues, there will be a number of high caliber data that will be competing for the financial headlines, our attention and market direction. For the high profile first quarter GDP readings, the limitation is the lagging nature of the data. While trade wars were certainly unfolding in February and March, the full impact would not be expected until into he beginning of the second quarter. The US consumer confidence survey from the Conference Board will offer a more timely gauge of tariff fallout, but the indicator doesn’t have the best track record for generating volatility from the major US indices, dollar or Treasuries.

The best mix of forecasting balance, trade considerations and market consequence are arguably the Mag 7 earnings. Wednesday after the close, we are due Microsoft and Meta numbers. These are major market cap tickers and considered core tech players. However, Thursday’s major names – Amazon and Apple – may carry greater heft. Apple is the largest market cap stock and recent headlines have shown the White House is pressuring its supply chains. From Amazon, we are also looking at the consumer appetite angle which will play a key role in how steadfast the economy will be in the face of headwinds.

Chart Nasdaq 100 Overlaid with Apple, Microsoft, Amazon and Meta (Daily)

Source: John Kicklighter, TradingView

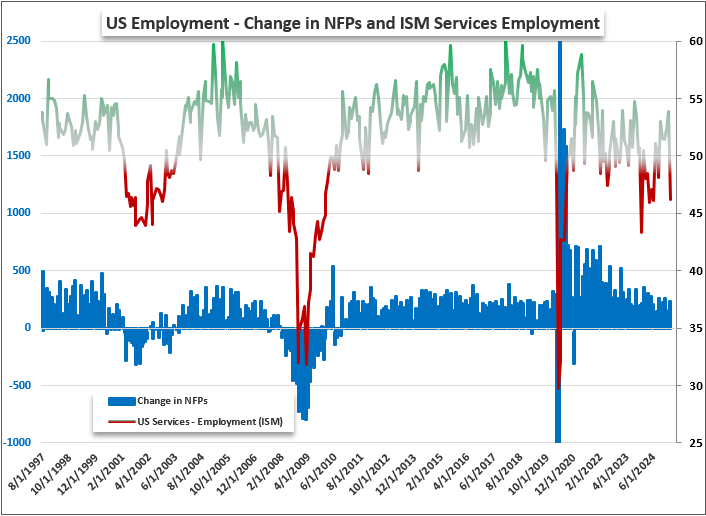

Nonfarm Payrolls Will Raise At Least Some Concern

At the end of the week, the US labor figures for April will no doubt be closely observed by the FOMC, President Trump and concerned Americans. If nonfarm payrolls miss expectations substantially, the headlines will no doubt interpret the data as evidence that the world’s largest economy is straining under the pressure of the trade war. That would in turn encourage the President to urge action from the central bank, but the ‘wait and see’ approach will linger for the group in its pre-FOMC meeting media blackout – and the PCE deflator earlier in the week could tip the scales if inflation pressures are also firming up as consumer expectations have suggested they were this past week. Alternatively, a strong jobs number would keep the Fed’s foot off the policy break and shift the focus back on the state of the economy that will be assessed through opinion polls and slow data accumulation. There is nary a scenario given this backdrop where the jobs report will not draw concern for the path forward.

Chart of Change in Nonfarm Payrolls and Services PMI Employment (Monthly)

Source: US Bureau of Labor Statistics and ISM Non-Manufacturing

Follow the Global Macro Calendar

What are the major events and indicators on tap for the global economy that could charge volatility in markets and reshape deeper fundamental themes? Sign up for the updated Global Macro Calendar updated each week with a two week look ahead of the top events!

The subsidiaries of StoneX Group Inc. provide financial products and services, including, but not limited to, physical commodities, securities, clearing, global payments, risk management, asset management, foreign exchange, and exchange-traded and over-the-counter derivatives. These financial products and services are offered in accordance with the applicable laws in the jurisdictions in which they are provided and are subject to specific terms, conditions, and restrictions contained in the terms of business applicable to each such offering. Not all products and services are available in all countries. The products and services offered by the StoneX Group of companies involve risk of loss and may not be suitable for all investors. Full Disclaimer. This content is not intended for residents of any particular country, and the information herein is not advice nor a recommendation to trade nor does it constitute an offer or solicitation to buy or sell any financial product or service, by any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation. Please refer to the Regulatory Disclosure section for entity-specific disclosures. No part of this material may be copied, photocopied or duplicated in any form by any means or redistributed without the prior written consent of StoneX Group Inc. The information herein is provided for informational purposes only. This information is provided on an ‘as-is’ basis and may contain statements and opinions of the StoneX Group of companies as well as excerpts and/or information from public sources and third parties and no warranty, whether express or implied, is given as to its completeness or accuracy. Each company within the StoneX Group of companies (on its own behalf and on behalf of its directors, employees and agents) disclaims any and all liability as well as any third-party claim that may arise from the accuracy and/or completeness of the information detailed herein, as well as the use of or reliance on this information by the recipient, any member of its group or any third party.

Our market expertise, advanced platforms, global reach, culture of full transparency and commitment to our clients’ success all set us apart in the financial marketplace.

Reach

With access to 40+ derivatives exchanges, 180+ foreign exchange markets, nearly every global securities marketplace and numerous bilateral liquidity venues, StoneX’s digital network and deep relationships can take clients anywhere they want to go.

Transparency

As a publicly traded company meeting the highest standards of regulatory compliance in the markets we serve, our financials and track record are matters of public record. StoneX’s commitment to “doing the right thing over the easy thing” sets us apart in the industry and helps us build respect, client trust and new partnerships.

Expertise

From our proprietary Market Intelligence platform to “boots-on-the-ground” expertise from award-winning traders and professionals, we connect our clients directly to actionable insights they can use to make more informed decisions and achieve their goals in the global markets.