Top Global Macro Event Risk This Week: A Focus on FOMC; BOJ, BOE and PBOC; December PMIs; China November Health Check

Talking Points:

- We are heading into the final high-profile week of event risk for the calendar year, can the Fed and other top listing generate some late-stage volatility?

- A possible BOJ rate hike along with an important BOE and PBOC rate decision will market the last run of major central bank decisions for the year

- We are due a range of major developed economy PMIs this week which will be complemented by the run of China’s November data

Though there are certainly a number of high-profile events scheduled for release over the coming week, there is no question as to which release will be top billing. The FOMC rate decision on Wednesday has a basic level of awareness that is usually well above most other global macro listings even in the slowest of times. And, the circumstances with which we are dealing from the questions around the relative standings of monetary policy globally, the trajectory of the US central bank’s medium-term path and the backdrop of fragile market liquidity will set the stage for some serious fundamental interpretation. While the traders among us will be monitoring the short-term market reactions to this event, don’t forget what is decided here will very much carry into 2025.

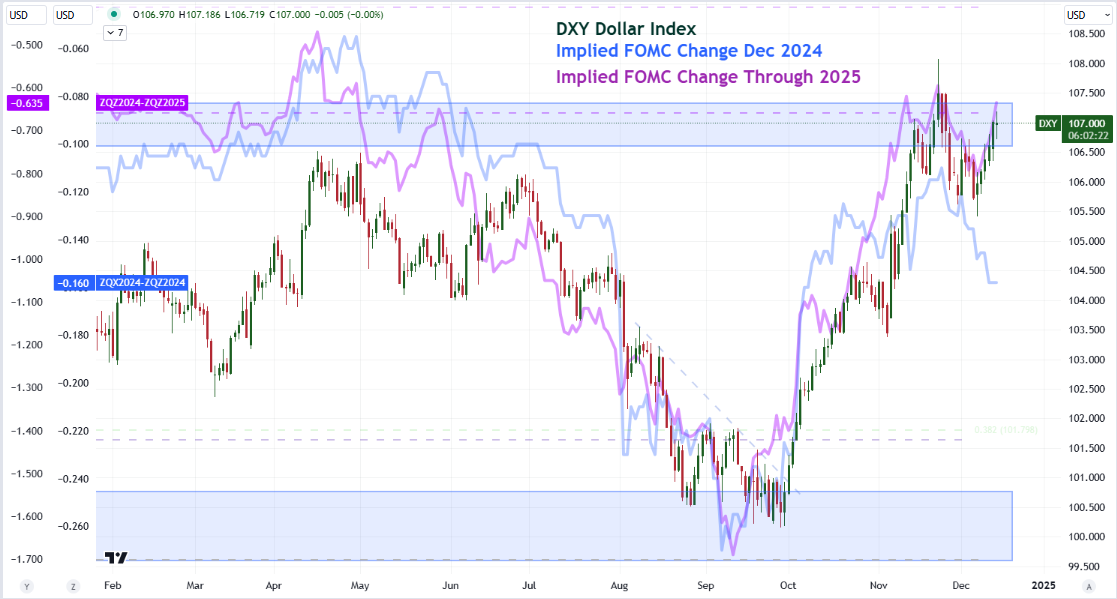

Chart of the DXY Dollar Index Overlaid with Implied December 2024 and 2025 Forecast

Source: TradingView, John Kicklighter

That said, let’s consider what at stake starting from the short-term and work our way out through time frames. While there are notable global macro listings after the Fed’s rate decision (eg BOJ rate decision, US PCE deflator, China industrial profits, etc), this monetary policy event will effectively be the turning point for liquidity through the end of the year. That can translate into greater short-term volatility response from the likes of the US dollar, indices and yields among other assets should there be a material surprise. Otherwise, we should register the developments and interpret what they may mean for trends through the medium term (aka in January and beyond).

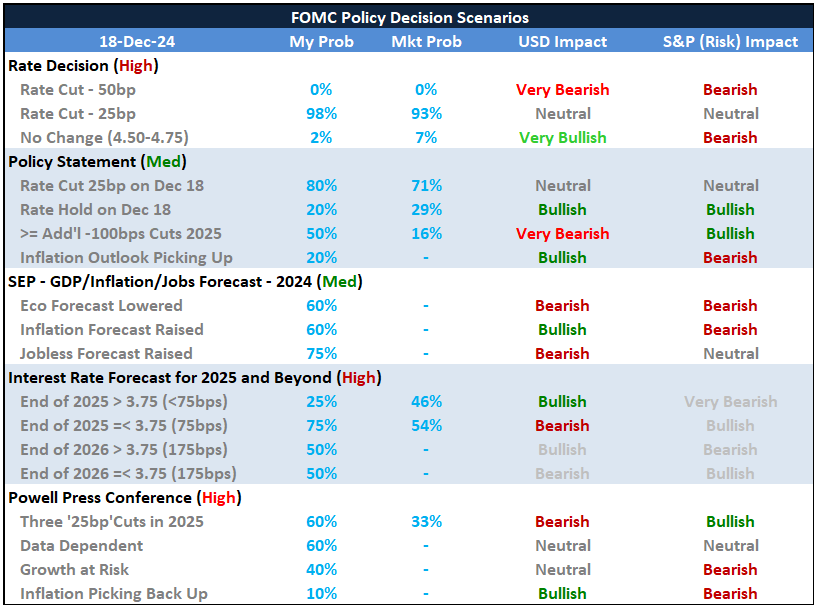

From this policy update in particular, we are dealing with considerable changes in backdrop forecasts. Looking to measures of ‘market expectations’ – like the consensus forecast from economists or Fed Fund futures – a -25 basis point (bp) cut to a range of 4.25–4.50 percent is the discounted outcome. That seems a reasonably-set assumption with the language from Fed officials and key dual mandate readings as of late. Purely falling in-line with that outcome would mean benchmark assets like the Greenback and S&P 500 are theoretically discounted and at ‘fair value’ heading into the event.

If that were the case, we would be looking a slow drift into the close of the year. If that were the only consideration for this event, the equation would be fairly simple. That said, we have an open-ended and more sensitive gauge to weigh in on: the updated Summary of Economic Projects (SEP). These are the FOMC’s official forecasts for interest rates, growth, inflation and employment. While these projects were meant to curb volatility; in this case, they are more likely to boost it.

Table of FOMC Policy Decision Scenario Table

Source: John Kicklighter

In the September forecasts from the Federal Reserve, the group’s average projection was for -100 basis points of easing through 2025 from the an anticipated average rate of 4..375 (in other words a 4.25-4.50 range) percent. For short-term impact, there seems a contrast in outcome potency depending on the asset we focus on. If the Fed is materially more hawkish than is afforded for by the market – particularly in action but also in forecast – the near-record high of the risk-oriented benchmark of the S&P 500 is the most exposed skew to be rebalanced.

The Dollar, on the other hand, is near the top of a two-year range; so ‘hawkish’ traction will contend with illiquidity. Alternatively, the stretch on the Greenback could see a dovish turn urge a short-term pull back while the already ebullient equity/risk view will be difficult to extend. Just remember, the course of monetary policy from the world’s largest central bank will continue to steer markets into first quarter 2025’ and the lull in liquidity over the holiday is only a temporary affliction.

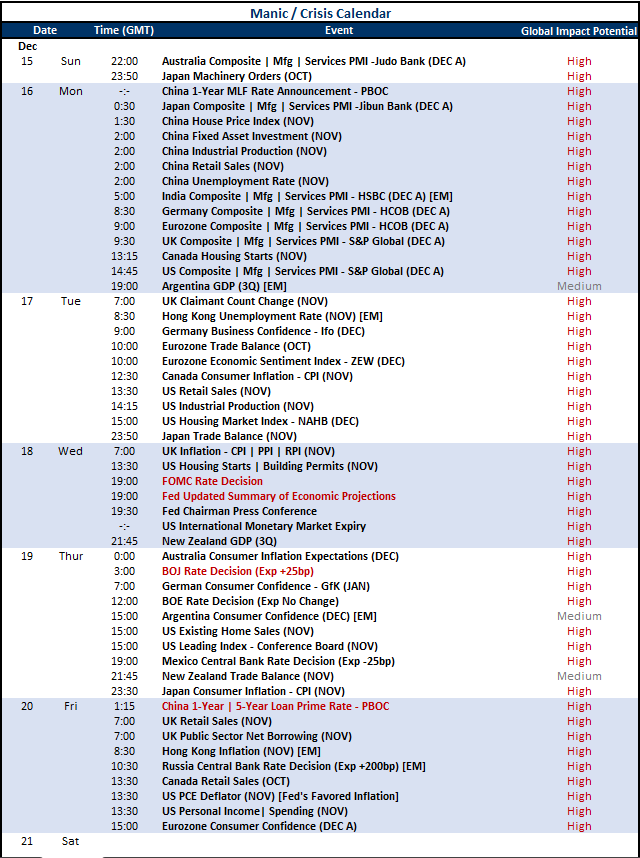

The last full week of trade for the calendar year has a lot of fundamental event risk to work with for the industrious market participants willing to indulge. It is worth noting that key events over the past few weeks – some with meaningful surprises – have rendered tangibly underwhelming market response whether reading in historical or implied volatility metrics. As such, it’s important to ingest what’s on tap with both an awareness as to what the markets can do in the short term but also considering what trends may pick up on heading into 2025.

Table of Major Global Macro Events Scheduled for Week

Source: John Kicklighter, StoneX

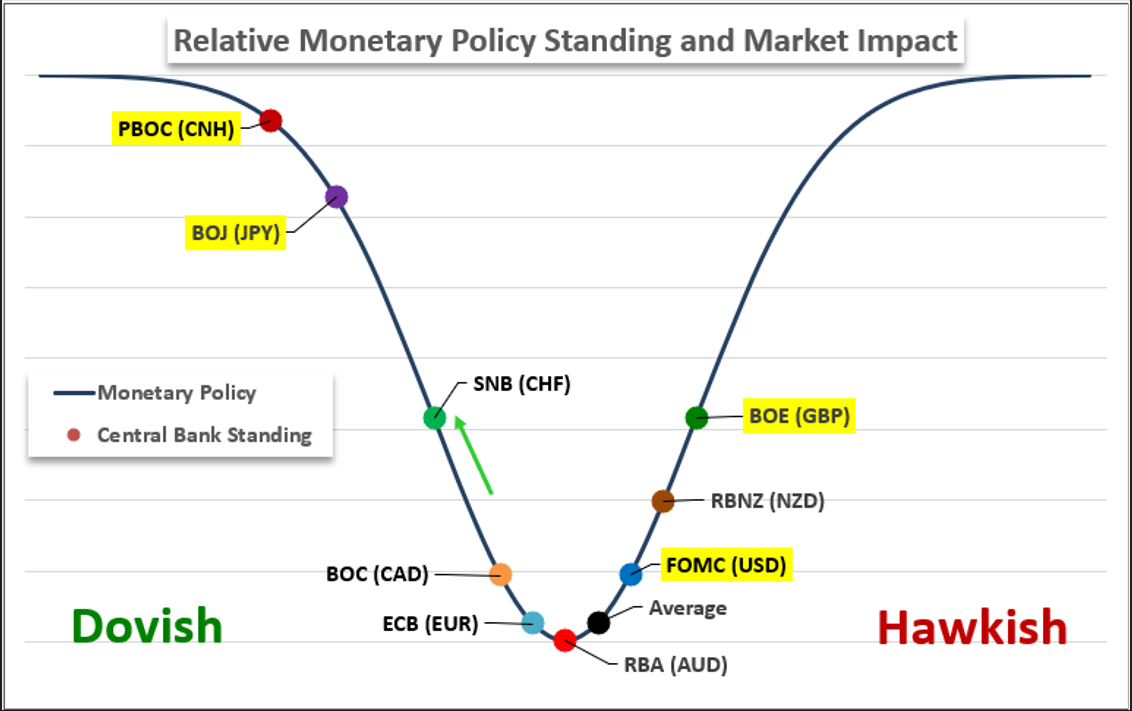

For sheer fundamental power, monetary policy carries the greatest scheduled potential ahead. The Federal Reserve’s policy decision and forecast carry singular market-moving potential for the global system. That said, it isn’t the only group weighing its settings – nor the only authority that can sway conditions outside its own jurisdiction. While I will be watching central banks in Russian, Mexico, Taiwan and Indonesia; their global weight will only stretch so far, particularly in our present liquidity conditions. In turn, the Bank of Japan (BOJ) is actively counteracting the general flow of the broader developed central bank setting as it weighs rate hikes. The Bank of England (BOE) is expected to hold rates even as its Euro-area counterpart cut and its US peer is seen easing itself the same week. The Chinese authority (PBOC) will recalibrate on Friday, so its short-term volatility impact is likely to be truncated. That said, the unflattering economic outlook for the world’s second largest economy makes this turning exceptionally important heading into 2025.

Chart of Relative Monetary Policy Standing of Major Central Banks

Source: John Kicklighter

If we are focusing in on China, there is perhaps more runway for fundamental adjustment through the week when it comes to the run of November data that is scheduled for release Monday morning. The monthly run of domestic data from the government itself doesn’t always generate the scale of event risk we see in readings like US NFPs, Japanese CPI or the like; but this collection of data reflects a comprehensive and significant update to the country’s health. Housing inflation figures for the past month is the first of the monthly figures to hit (at 1:30 GMT), but the fixation on a troubled property market – though not resolved – seems to have faded in interest. The combination of fixed asset investment, industrial production and retail sales half an hour later though represents a spread that more thoroughly covers the economy. The question is how willing the markets are to take the government’s stats at their word.

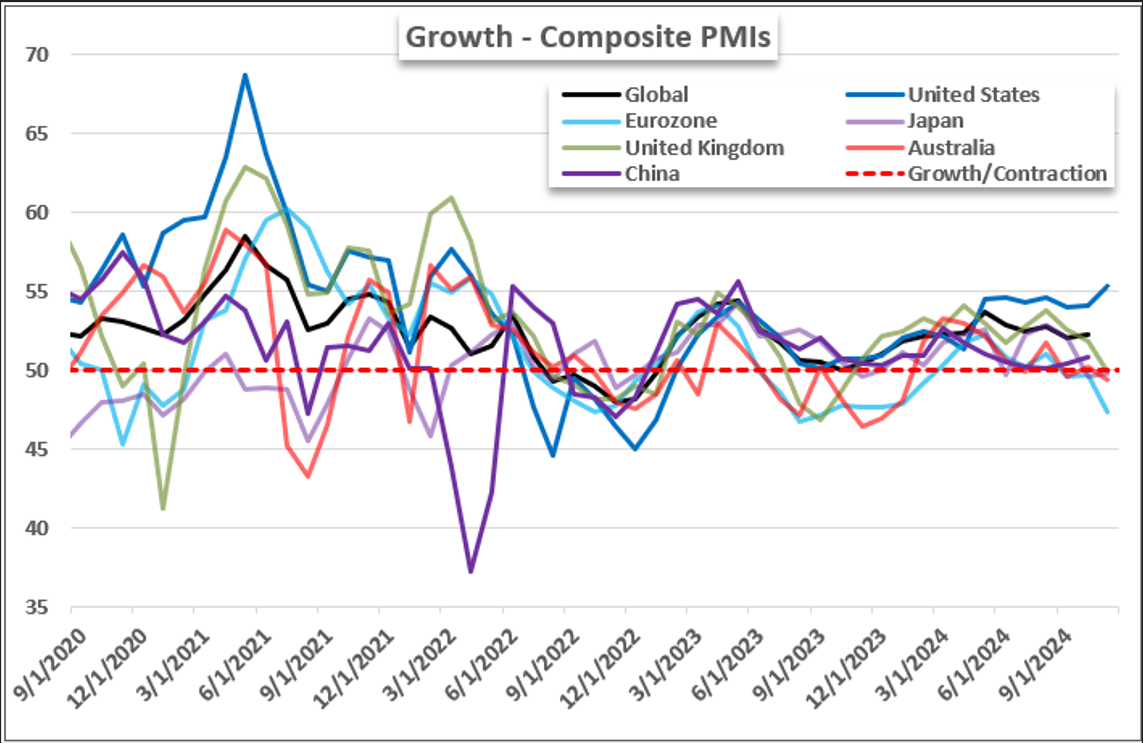

Finally, if we are really going to pay heed to the health of the global economy, a more reliable update will come from the developed world leaders thanks to the updated, advanced December PMI readings. I consider these ‘timely proxies to GDP’ but the market-moving potentially of this series seems to depend on how counter-prevailing trend the outcome proves. The US economy has enjoyed a solid, outpacing trend in its series up through the past month, while most others have flagged or even contracted. In particular, the Eurozone has tipped heartily into contraction as of November’s read. If these bearings were to inverse, it would find a pair like EURUSD fundamentally stretched. Extended its bullish move on the other hand would be hard to do given the liquidity environment.

Chart of Developed Economy Composite PMIs (Monthly)

Source: Standard & Poor’s, John Kicklighter

-- Written by John Kicklighter, Global Head of Content