S&P 500 and Bitcoin Different Ends of the Liquidity Scale this Week with a Thinned Macro Economic Calendar

Talking Points:

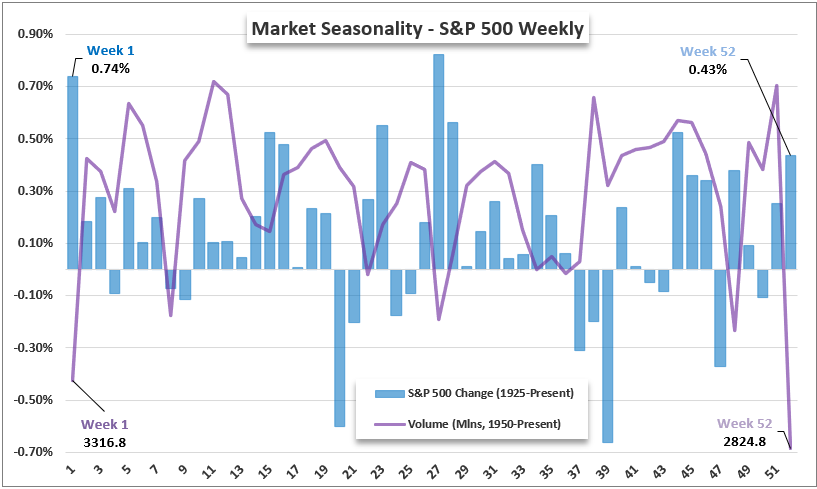

- The first week of the trading year is a known liquidity slump for New Years, but historically the S&P 500 has averaged the best week of the calendar year

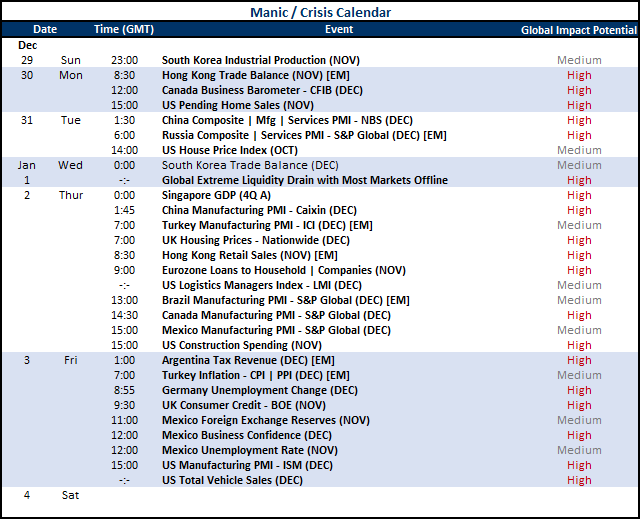

- Top event risk this week includes China’s December PMIs, Singapore’s 4Q GDP release and the United States’ ISM manufacturing report

- Without the commitment to a top fundamental theme, the market may remain sensitive to event risk touching major economies and systemic risks

We have passed through the lowest volume week of the year – on average – and are looking at the transition from the close of one year to the open of the next. There is a lot left unresolved in 2024 and that we will carry forward into the new year, but the restoration of liquidity does not ensure the market will be forced to sort out its unresolved fundamental conflicts. Make no mistake, we are still due for the lowest singular global liquidity day of the calendar year through the coming week. Where Christmas is a broadly recognized exchange holiday for many countries, far more of the world abides by the New Year holiday closure.

S&P 500 Average Performance and Volume By Calendar Week

Source: John Kicklighter, Bloomberg

In fact, if you are looking for a market to reflect on speculative sentiment on the off-chance that something is afoot, you’d be hard pressed to find something that is truly representative. Perhaps the only serious candidate to consider for that role is Bitcoin as a lead cryptocurrency – where it has also taken up the torch through weekend liquidity drains.

Chart of Bitcoin and Implied Bitcoin Volatility (Daily)

Source: John Kicklighter, TradingView

The week ahead of us hosts a thin global macro docket and it is punctuated by a definitive liquidity drain in the New Year holiday which will pull most exchanges offline. That said, we are still looking at event risk that can hold some short-term sway over targeted markets – but will almost certainly weigh on medium to long-term fundamental considerations that will continue beyond the short-term swoon in market participation for the opening session of 2025. It is worth noting that there doesn’t seem a full commitment to any singular, high-profile fundamental theme. Rate forecasts, growth outlooks, political loggerheads and other big picture uncertainties all stand a chance of wrestling our attention heading into the new year. That can certainly keep the market from committing to a clear and systemic trend. Then again, it can also make us prone to developments from all these matters as they could each take the reins.

Calendar of Major Global Macro Events Scheduled for Week

Source: John Kicklighter, StoneX

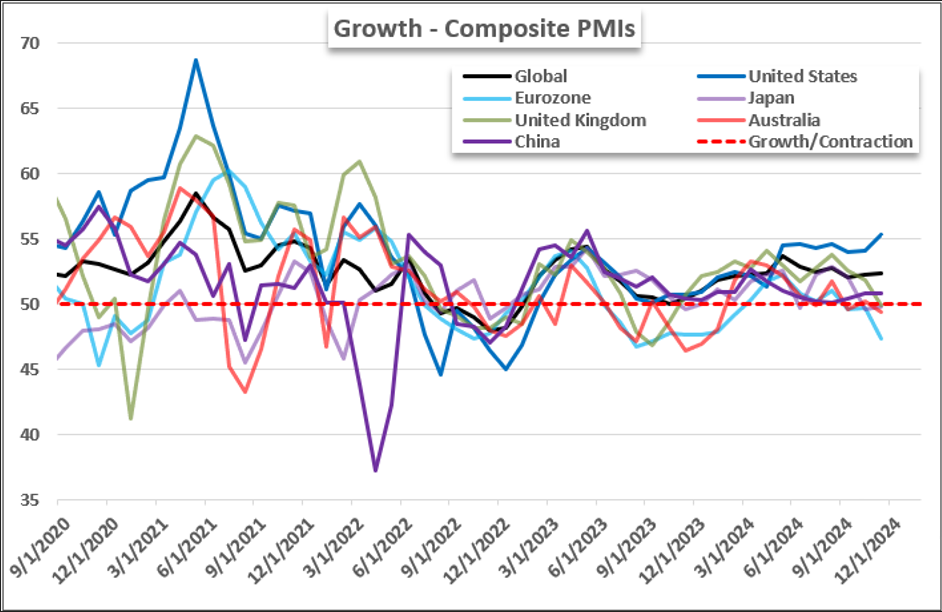

For top event risk to monitor over the coming week, arguably the most impactful and comprehensive listing on my radar is the December PMIs from China’s government (NBS). The Tuesday release is not convenient for a liquid market to absorb the outcome for a full response, but the markets have already grown to be cynical over the accuracy of the data itself. Nevertheless, the general health mile marker for the world’s second largest economy is going to be an important measure to set our signpost. While the Chinese government would like the country to shift to consumer demand and greater services – in a mirroring of the US economy – the reality is that China is still very dependent on manufacturing, trade and lending. As such, watch the manufacturing PMI component more closely.

Chart of Composite PMIs of Major Economies (Monthly)

Source: John Kicklighter, S&P Global

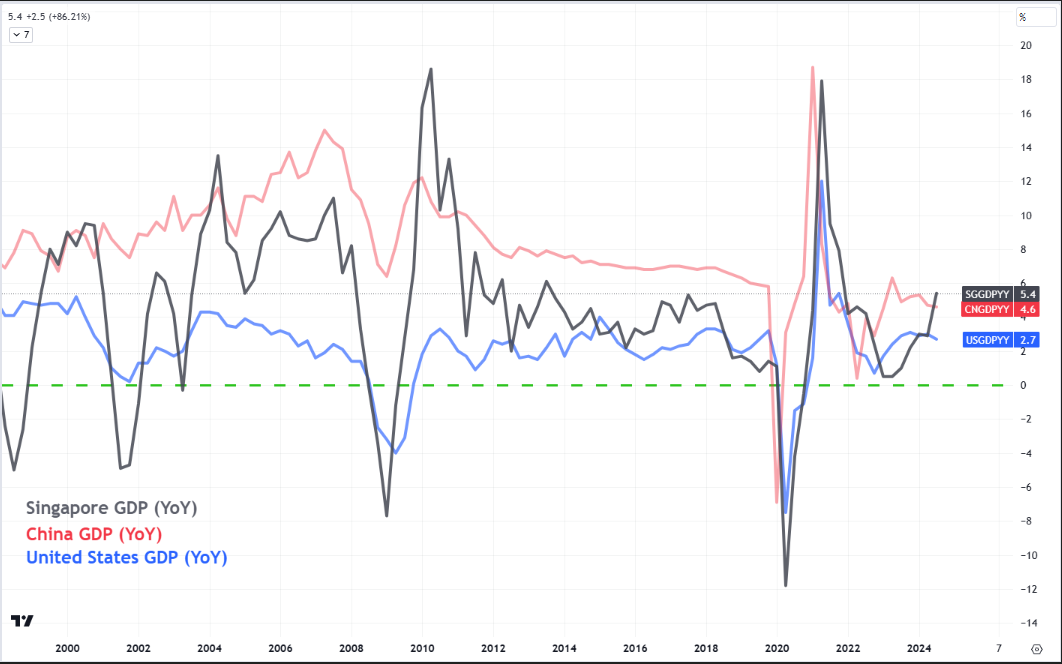

Materially smaller in economic terms, but far more likely to be taken at face value is the January 2nd release of Singapore’s 4Q GDP figure. Singapore is ‘only’ the 26th largest economy in the world, but it is large enough to be indicative of Asia’s general performance and can even extend to the developed world’s global economy. This will be the first of the major economies to report economic activity through the final quarter of 2024. The next major economy to report performance over the same period for this scale will be China some weeks later – and major Western economies weeks after that. The correlations are strong for Singapore to global counterparts, but not so coordinated that the world will extrapolate, say, a US performance from this reading.

Chart of Singapore, China and US GDP Year-Over-Year (Quarterly)

Source: John Kicklighter, TradingView

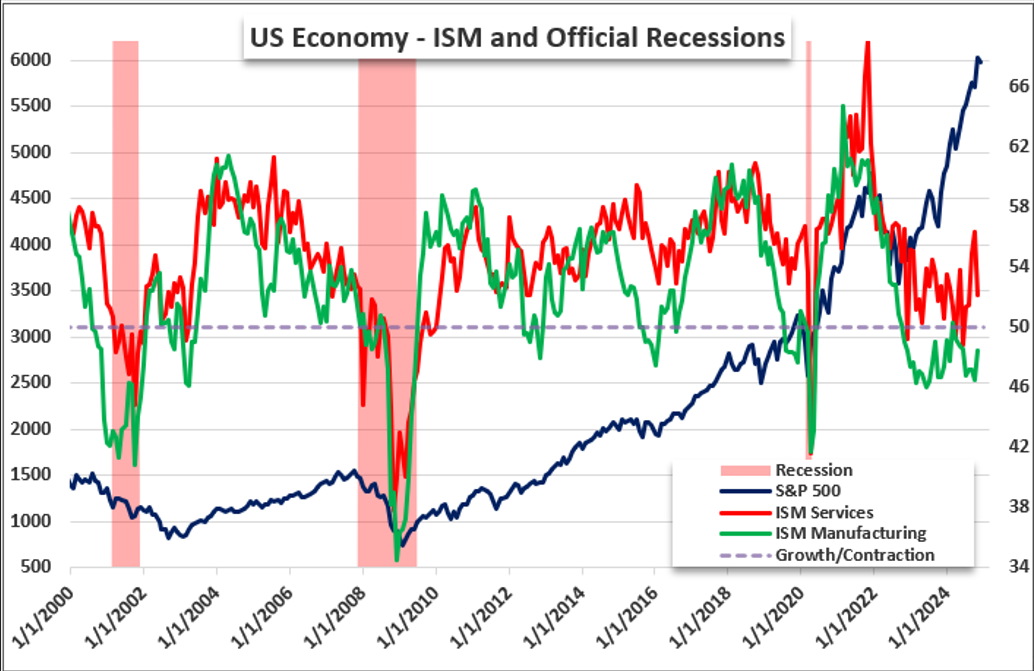

In terms of density of major event risk, Thursday and Friday will pick up materially. There are a number of manufacturing activity figures due for multiple countries due over the week, but Friday’s US ISM manufacturing report for December will carry more systemic weight. If we are looking for a figure truly indicative of the United States broader economy, the following week’s service sector report will be more indicative of output, employment and inflation, Nevertheless, manufacturing is once again the focus of political ire with the Trump administration driving the threat of trade retaliation against unfair partner practices around factory-oriented issues. How strong will his mandate be when he enters the White House in a few weeks? This indicator will be a direct consideration.

Chart of the S&P 500 Overlaid with ISM Manufacturing and Services PMIs (Monthly)

Source: ISM, John Kicklighter

-- Written by John Kicklighter, Global Head of Content