• Futures prices fall amid weak commercial activity

• July contract drops 3.6% in NY; London declines 2.3%

• Brazilian real strengthens, with the USD/BRL falling 0.5%

• Arabica down 0.9% and robusta down 2.8% in Brazil

• Investment funds increase net long positions; appetite improves

• USDA begins releasing reports on key producing countries

• India expected to produce 6 million bags, down 2.4%

• Guatemala shows stability with slight growth in output and exports

• Brazil’s April exports may fall 41%, according to Secex preliminary data

• Inflation weighs on coffee consumption and major company earnings

*Translated by AI

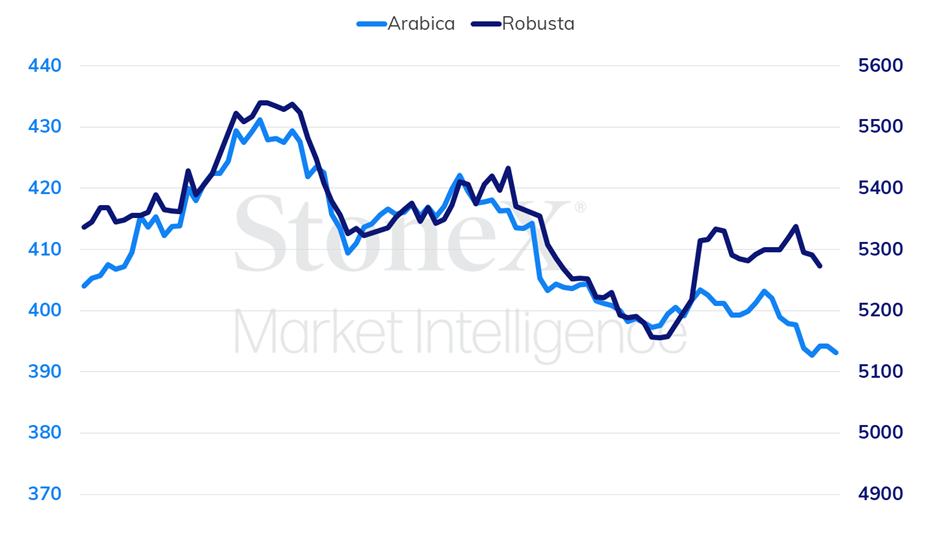

Futures prices for both arabica and robusta coffee ended last week lower. Market activity was considered sluggish, with a notable decline in trading by commercial agents. From a fundamentals perspective, there were no major shifts, with constrained supply and expectations of a smaller 2025/26 crop remaining as bullish factors. However, attention continues to focus on the progress of Brazil’s new harvest.

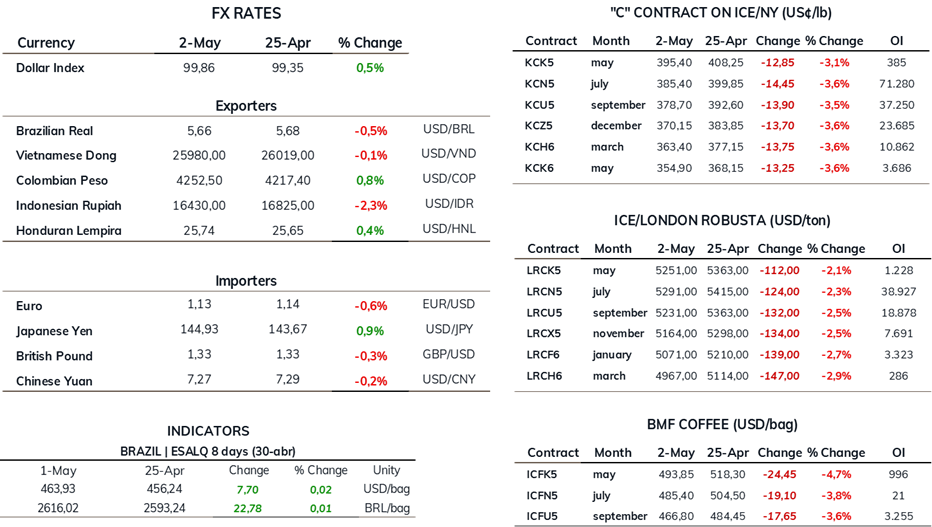

In New York, the most active contract (July) closed Friday, May 2nd, at 385.40 US cents per pound, down 3.6% from the previous Friday. In London, prices fell 2.3%, with the July contract settling at USD 5,291 per metric ton. Over the same period, the US dollar depreciated 0.5% against the Brazilian real, closing at BRL 5.66.

Intraday Chart – Most Active Contract – April 28 to May 2

Prices also fell in Brazil’s domestic market. The Cepea arabica indicator dropped 0.9%, closing at around BRL 2,589 per 60kg bag. The robusta indicator declined 2.8%, reaching approximately BRL 1,668 per bag.

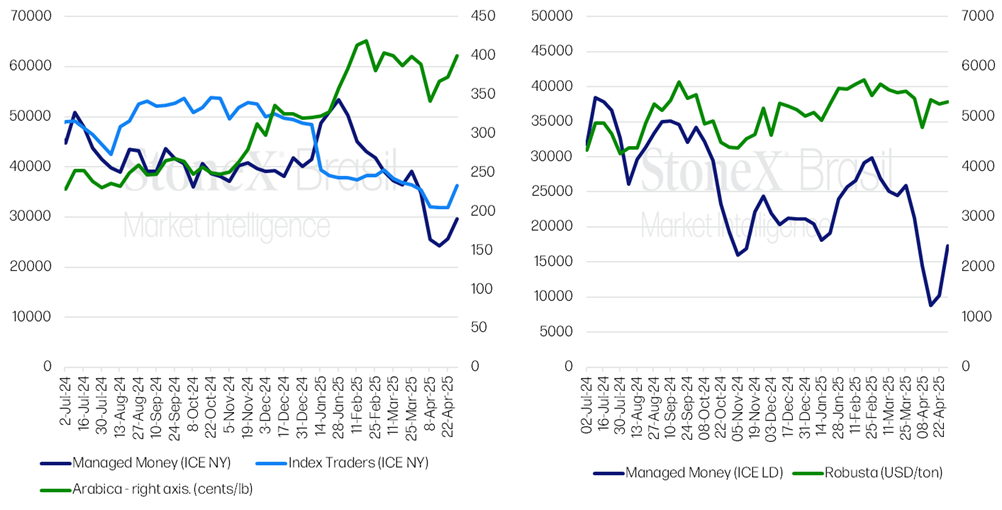

Last week also saw improved investor appetite for the coffee market. According to the COT-CFTC report released Friday (May 2), covering data through April 29, actively managed funds in New York increased their net long positions by 15.4%, reaching 29,618 contracts. Index funds, more aligned with macroeconomic trends, expanded their net long by nearly 14%, to 36,227 contracts. In London, the increase was even stronger, with funds growing their net long position by more than 68%, to 17,296 contracts.

Net Fund Positions in New York (left) and London (right) vs. Futures Prices

Sources: ICE and CFTC. Design: StoneX.

Also last week, the U.S. Department of Agriculture (USDA) began publishing agricultural attaché reports with details on coffee production in major producing countries. Reports for India and Guatemala were released, with additional updates for Brazil, Vietnam, and Colombia expected in the coming weeks. These publications are closely monitored by the market at this stage.

According to the USDA report, India’s 2025/26 coffee production is forecast to decline 2.4% to just over 6 million bags due to adverse weather. Arabica output is expected to fall 3.6% to 1.35 million bags, while robusta may decline 2.1% to 4.7 million bags. Meanwhile, domestic consumption is projected to increase 4.6% to 1.36 million bags, while exports are seen falling 3.6% to 5.99 million bags.

Guatemala’s report suggests production stability. Output for the 2025/26 season is forecast at 3.54 million bags, up just 0.4%. Domestic consumption and exports are also expected to rise 0.4%, reaching 720,000 bags and 3.27 million bags, respectively.

As previously noted in StoneX reports, Brazil’s 2025/26 harvest is underway across all producing regions. However, the pace remains slow. Recent rains, especially in arabica-producing regions, have contributed to the delay. On the other hand, good rainfall in April may help preserve plant health and mitigate post-harvest stress. If scattered rains continue in the coming months, trees may experience less exhaustion during the dry season.

Fruit development has been strong and uniform, which should support harvest efficiency. Early arabica deliveries to the market already show a higher share of beans sized 17 and above compared to the previous crop. Similar improvements are being reported in conilon quality.

Next week, the market will closely watch the release of Brazil’s April coffee export data from Cecafé. Preliminary figures from the Foreign Trade Secretariat (Secex) show that Brazil exported around 2.5 million bags through the fourth week of April, which would represent a 41% drop from the same period in April 2024.

Weather remains a critical factor for the coffee market. Although no frost risk is expected in the short term, forecasts show a drop in temperatures through mid-May. Minimum temperatures in Varginha, Minas Gerais, are expected to reach 6°C on May 18. While this event is not expected to bring frost, the onset of the Brazilian winter and potential cold fronts may contribute to greater price volatility in the coming weeks.

Inflation Pressures Consumption and Earnings in the Coffee Sector

Inflation continues to pressure the global coffee market, particularly at the consumer level. As noted in prior editions, retail coffee prices have risen sharply. In Brazil, the 12-month accumulated inflation for coffee reached nearly 78% by March, according to IBGE. In the U.S., the annual increase was close to 24%.

Recent earnings reports from major industry players help illustrate the impact on demand. Kraft Heinz reported a 6.4% decline in net sales in Q1 2025, totaling USD 6 billion. Organic net sales dropped 4.7%, driven by a 5.6% decline in volume/mix, partly offset by a 0.9% price increase—particularly in categories like coffee. The company revised its annual outlook and now expects a 1.5% to 3.5% decline in organic sales and a 5% to 10% decline in adjusted operating income.

Starbucks also posted weaker results for Q2 of fiscal year 2025. Global same-store sales fell 1%, driven by a 2% drop in transactions, partially offset by a 1% increase in average ticket. In the U.S., comparable sales declined 2%, while international markets saw a 2% increase. The company opened 213 new stores during the quarter, ending the period with 40,789 locations. Net revenue rose 2% to USD 8.8 billion, but GAAP EPS fell 50%, and adjusted EPS declined 40%, reflecting operational pressures, labor costs, and restructuring efforts.

In contrast, China’s Luckin Coffee delivered strong growth. The company’s net revenue rose 41.2% year-over-year, reaching RMB 8,865.4 million (USD 1.22 billion). Monthly transacting customers increased 24% to 74.3 million. Store-level operating profit from self-operated stores jumped 244.8%, with a 17.1% margin. The company added 1,757 new stores during the quarter—1,743 in China—and ended the period with 24,097 stores (15,598 self-operated and 8,499 partnerships). Same-store sales grew 8.1%, reversing losses from prior quarters, indicating a strong rebound for the brand.

INDICATORS