BEARISH FACTORS

-

Creation of food export corridors in Ukraine;

-

Concerns about new Covid-19 cases and lockdown measures in China;

-

Reduction of concerns for US planting.

Bullish factors

-

Advancing vaccination roll out against Covid-19;

-

Expectations of a record grains crop in South America;

-

Conflict between Russia and Ukraine and expectation of lower planting in Ukraine.

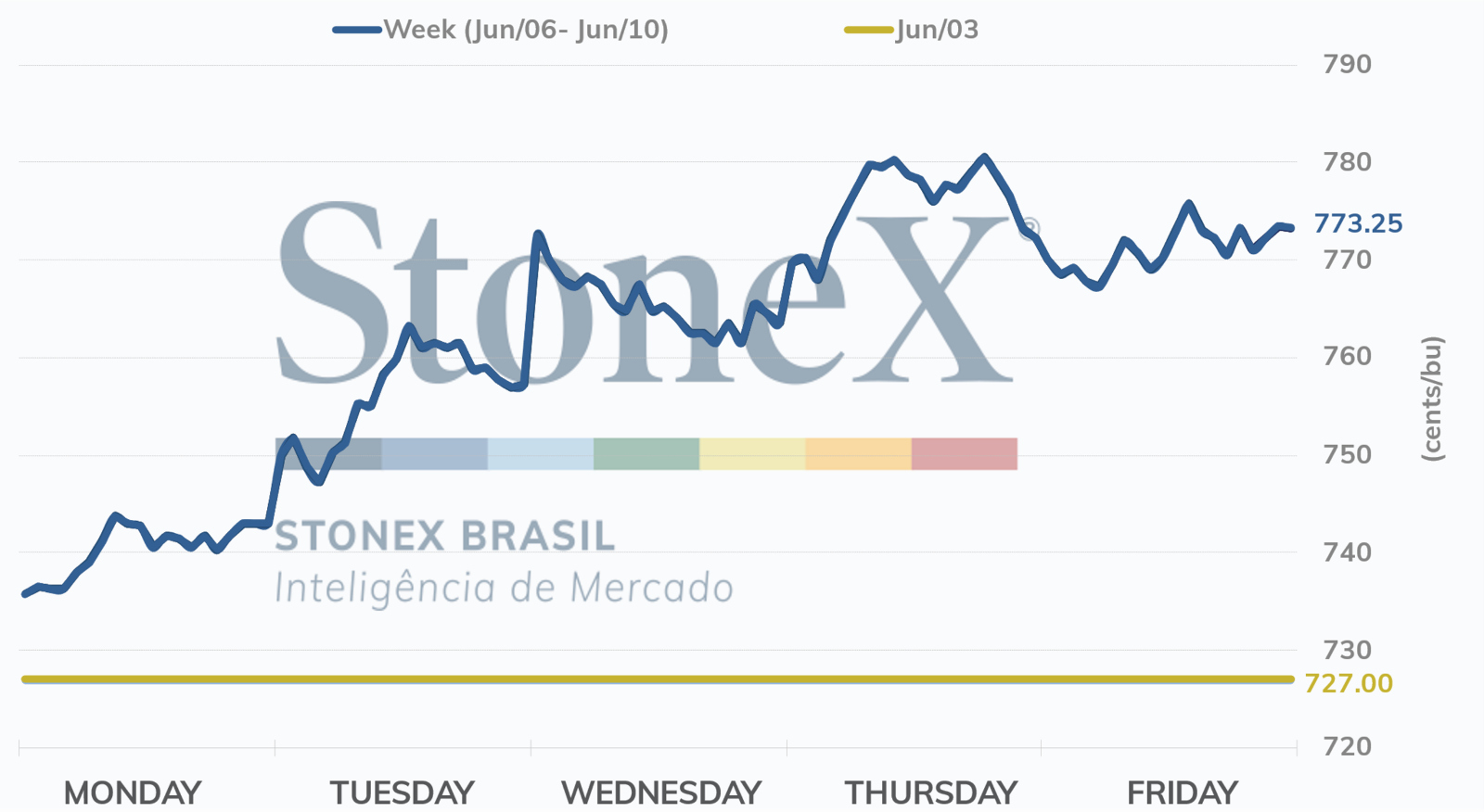

Corn futures started last week significantly higher in Chicago, driven by the rallies seen in the wheat market. July/22 closed Monday with 15.5 cents/bushel worth of gains from the previous session.

Late in the day, the USDA updated its weekly crop progress report. According to data from the Department, sowing reached 94% by June 5, a weekly advance of 8 points. In the same period of 2021, planting had reached 98%, while the five-year average is 92%. With planting practically finished, the market's attention is turned to corn conditions. Until the same date, 73% of the crops were in good or excellent condition, against 72% at the same time last year.

Intraday (15 min) - July/22 (CBOT)

Source: CME. Design: StoneX.

Corn Prices - CBOT (cents/bushel)

Source: CME. Design: StoneX.

On Wednesday, the nearby corn contract ended another session in the positive field, accumulating an increase of 7.5 cents/bu in the intraday. Forecasts of warm and dry weather for the US Midwest contributed to sustaining the grain’s price.

The Energy Information Administration (EIA) reported that US ethanol production dropped to 1,039 million barrels per day in the week ended June 3, a weekly decline of 32,000. Ethanol stocks rose to 23.64 million barrels, up 675,000 compared to the previous week.

Also on Wednesday, Conab released its monthly supply and demand report. The company made small positive adjustments in the three Brazilian crops. The first fell from 24.7 million to 24.8 million, the second from 87.7 million to 88 million and the third from 2.2 million to 2.4 million tonnes. As a result, total production rose from 114.6 million to 115.2 million tonnes, 1.6 million less than estimated by StoneX. There were no adjustments in demand variables, and, with this, the ending stocks increased from 9.9 to 10.6 million tonnes.

On Thursday, the eve of the USDA supply and demand report release, corn futures did not follow a single direction, with the nearby contracts rising higher and back month contracts receding. July/22 accumulated an 8.5 cent/bu increase in the intraday.

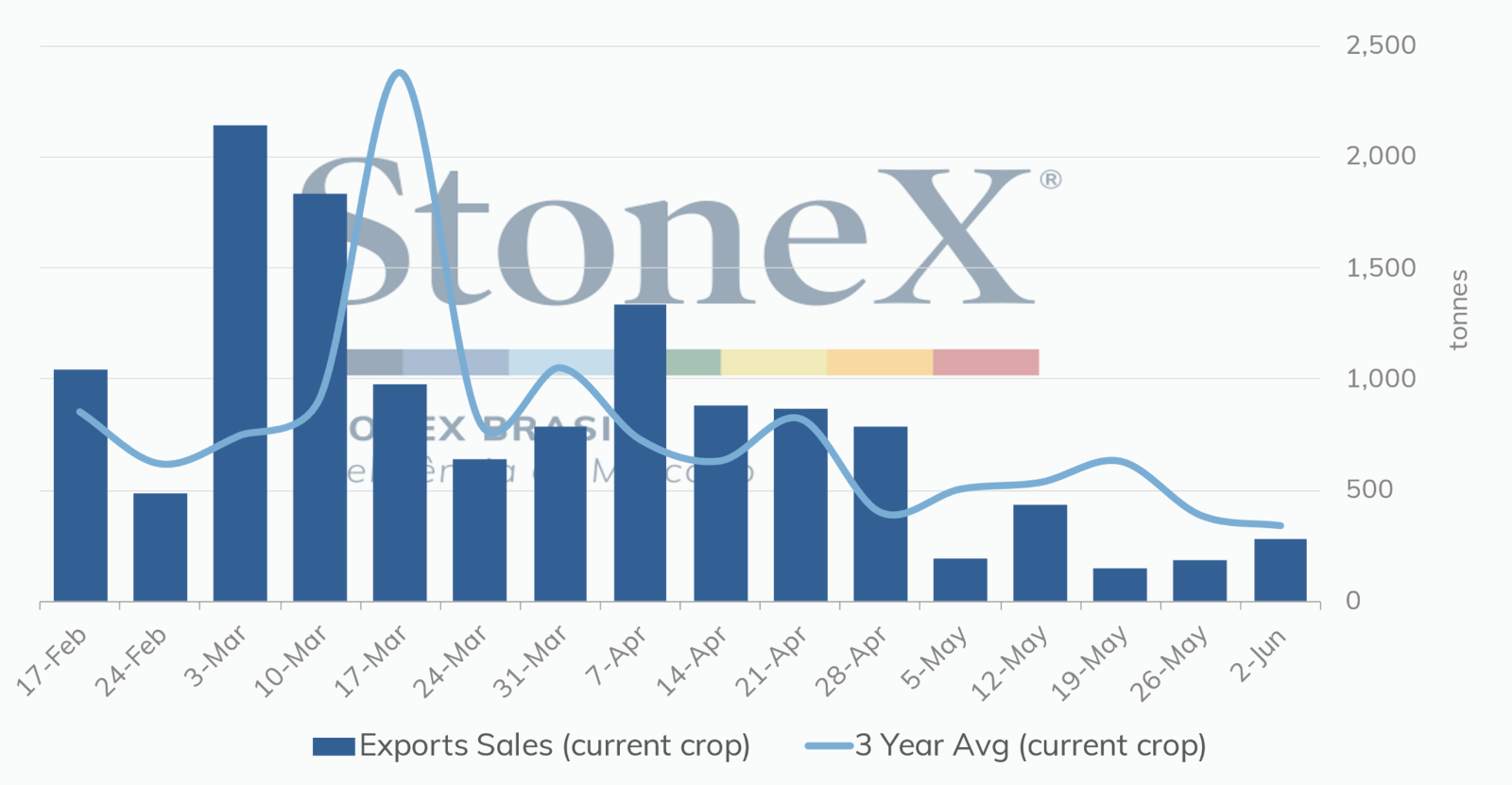

The USDA reported that net sales for the 2021/22 crop totaled 280,400 tonnes in the week ended June 2, which was 94,700 tonnes more than in the previous week, and 90,800 tonnes above the same week of 2021. The volume surpassed the ceiling of market expectations, which ranged from 125,000 to 500,000 tonnes. As such, commitments to all destinations rose to 59.5 million compared with 69.3 million tonnes in the same period last year.

Weekly US export sales - 2021/22

Source: USDA. Design: StoneX.

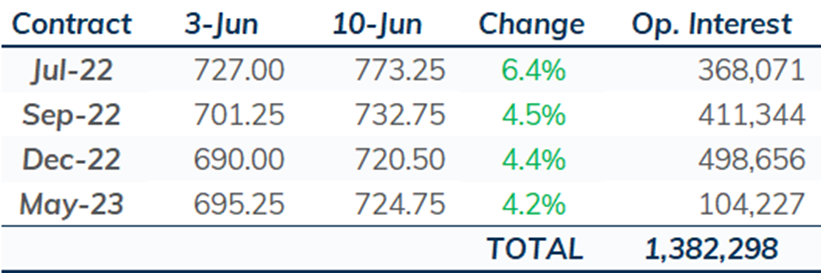

On Friday, corn futures rose higher again in Chicago. July/22 gained 0.25 cents/bushel from the previous day. With this, the contract closed the week quoted at 773.25 cents/bu, accumulating a 46.25 cent/bu appreciation (+6.4%).

Despite the WASDE release on the day, the market had limited fluctuations. This is because the June S&D report, as expected, brought no major surprises, as the Department is waiting for planted area data that will be released on June 30 to make further changes to the US grains supply.

The main highlight in the US balance sheet was the reduction in exports from the country’s 2021/22 crop, from 63.5 to 62.2 million tonnes. On the other hand, the Department partially compensated for the reduction in external demand with a slight increase of 127,000 tonnes in domestic consumption for food, seeds and industrial use to 173.1 million tonnes. With this, the 2021/22 season ending stocks were raised by 1.1 million tonnes, to 37.7 million, resulting in a stocks/use ratio of 10%, compared to 9.6% in the May report.

In the next few days, it will still be important to follow the conflict in the Black Sea, as Russia continues to attack and there is great uncertainty about grain exports through Ukrainian ports. In China, Covid-19 cases are still a cause for great concern. Beijing recently warned about a possible new outbreak and has promoted tighter restrictions, while Shanghai has conducted mass testing to hold the advance of new cases. However low the contamination rate in the country is compared to other locations, China is pursuing its zero-tolerance policy for coronavirus. In the US, the weather and planting conditions will continue to be closely watched, as the coming months will be key to defining corn productivity in the country.

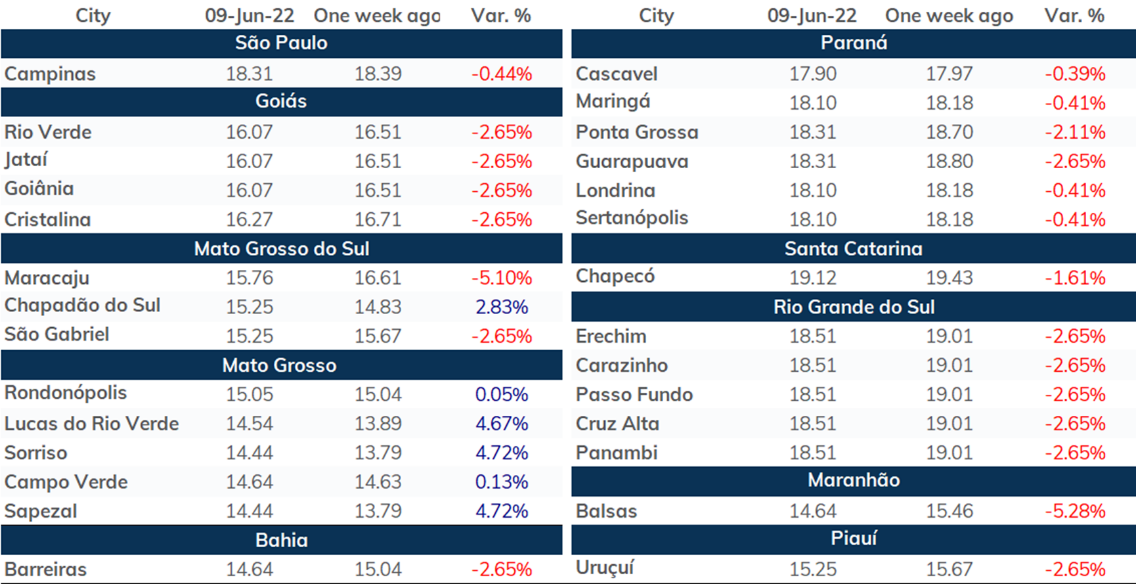

SPOT PRICES (USD/60kg-bag)

Source: StoneX, Agrolink and IMEA. Design: StoneX.