The first time the Grain Initiative was signed, at the end of July 2022, marked the resumption of the cargo flow, still with little expression, starting to gain more relevance only from September 2022.

Despite the initial slow pace, the resumption of Ukrainian shipments through the Black Sea has brought an optimistic effect to the market as it promotes more predictability for the trade flow in the region and opens space for relief in global supply since, until then, volumes were well below the levels recorded before the conflict for the wheat, corn and sunflower oil markets.

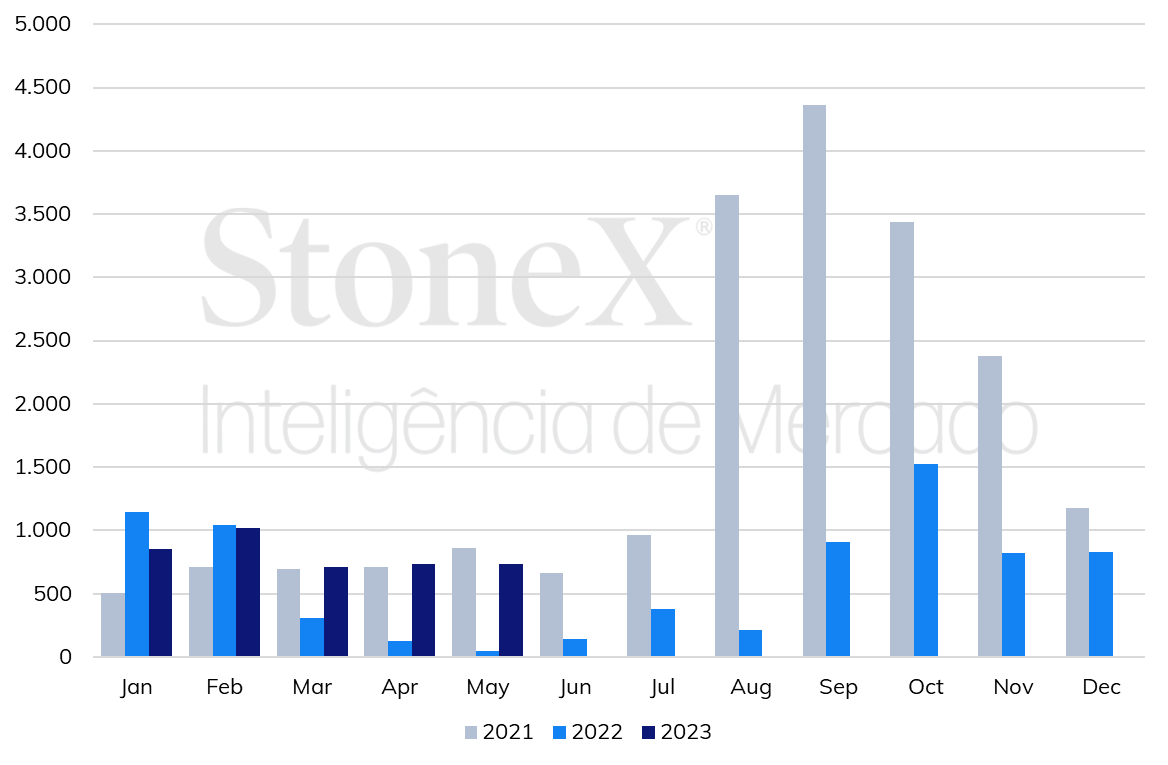

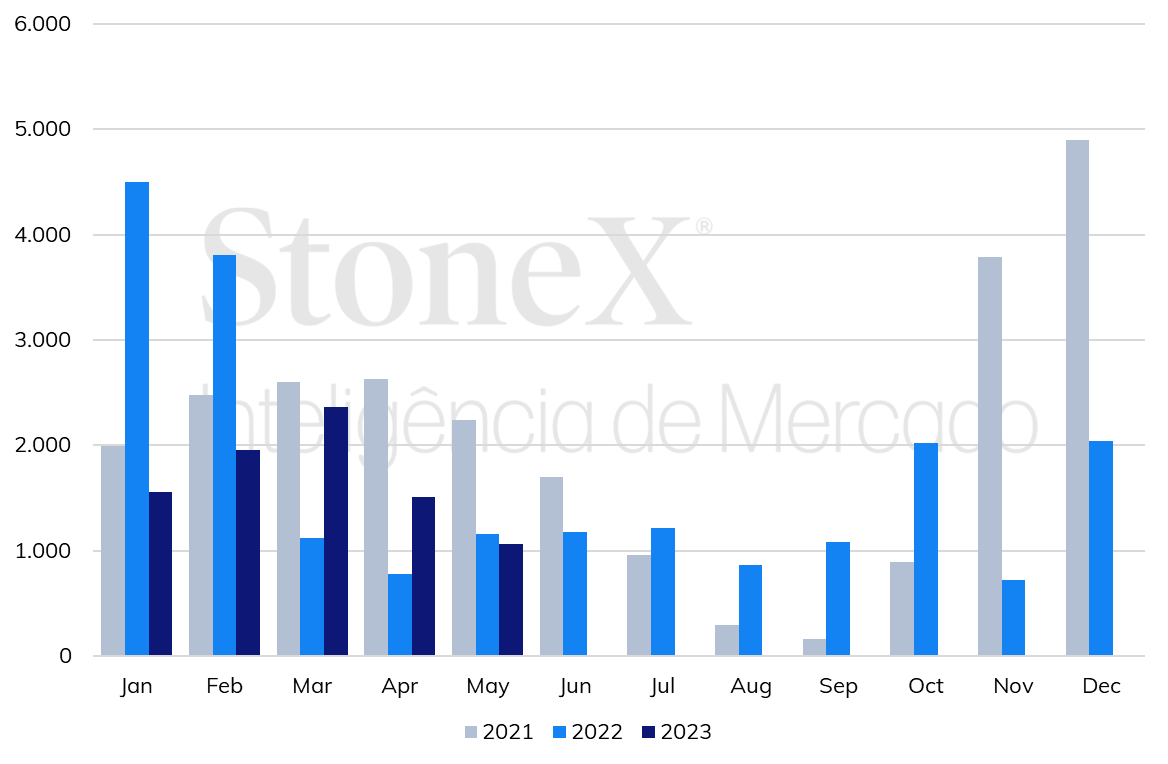

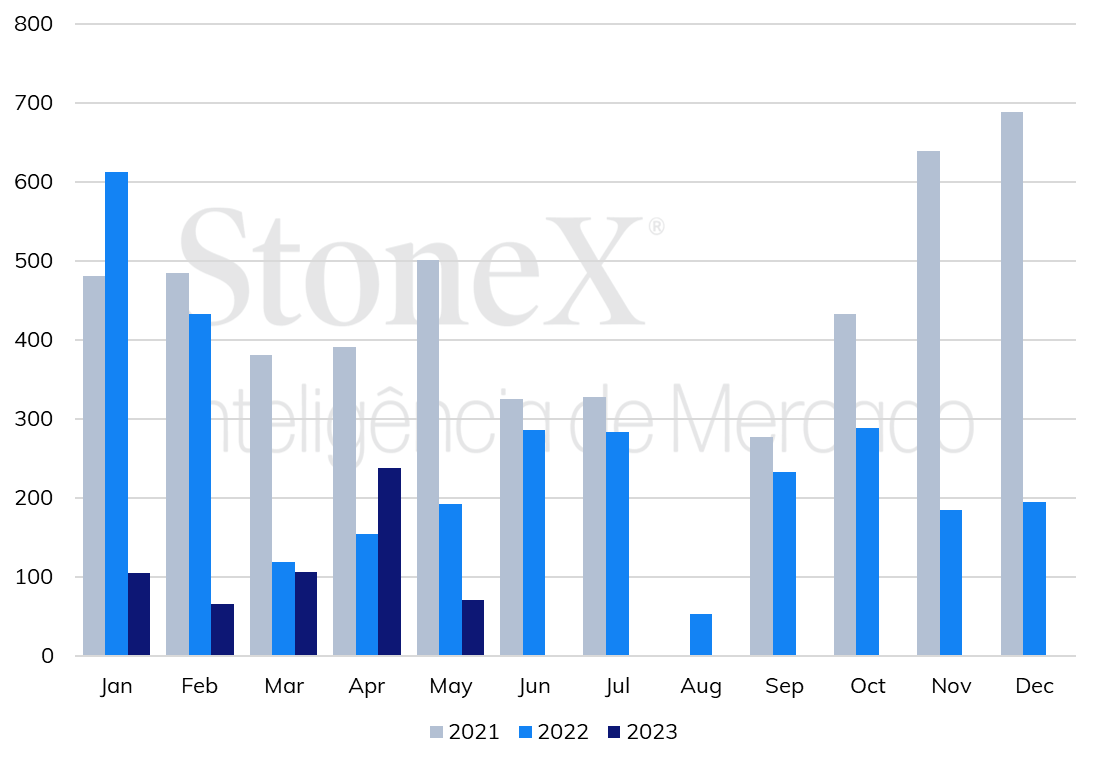

As seen in the following graphs, the agreement was essential to resuming the outflow of Ukrainian shipments overall. However, 2022 recorded significantly lower volumes than those reported in 2021.

On the other hand, 2023 can be seen as a recovery period for the outflow of Ukrainian wheat exports, given the good pace of shipments that resembles the period before the conflict. It is worth noting that, historically, there is a peak in grain exports between August and November. Before this period, the agreement will be negotiated again to determine its continuation, which could directly impact wheat prices.

In the case of corn, there was a relative increase compared to last year, but still below the pre-conflict level. For sunflower oil, only April 2023 recorded a higher volume than last year after the start of the conflict. As with corn, lower export volumes usually mark the next few months.

The question with the extension of the agreement is whether the pace of cargo inspections in Ukrainian ports will stabilize, with greater security for cargo transportation and predictability for the Ukrainian supply, despite the continuing war on its territory. Accordingly, the market continues to pay attention to the events in the Black Sea and the pace of exports.