Dollar expected to reflect inflation data in the US and Brazil, geopolitical tensions in the Middle East, and ECB interest rate decision

- Bullish

- The release of the May CPI and PPI in the US is expected to reinforce the perception of inflationary pressures in the country, favoring US Treasury yields and strengthening the USD globally.

- The persistence of the diplomatic standoff between the US and Iran reduces expectations for a swift reopening of the Strait of Hormuz, potentially increasing global risk aversion and further strengthening the dollar.

- The release of Brazil's IPCA may show a slowdown in inflationary pressures, favoring bets on Selic rate cuts, which could reduce foreign capital attraction and weaken the BRL.

- Bearish

- The ECB is expected to increase its interest rate by 0.25 p.p., which could strengthen the EUR and, consequently, contribute to weakening the USD.

The Week in Review

- The release of robust US indicators reinforced the perception of a more resilient and robust economy and increased expectations for higher interest rates for longer in the country.

- The United States has proposed tariffs on the import of goods from various countries, including Brazil, which could see rates increase by up to 32.5 p.p.

- The resumption of clashes between the US and Iran and the failure of the ceasefire between Israel and Lebanon kept the perception of geopolitical risks in the Persian Gulf elevated.

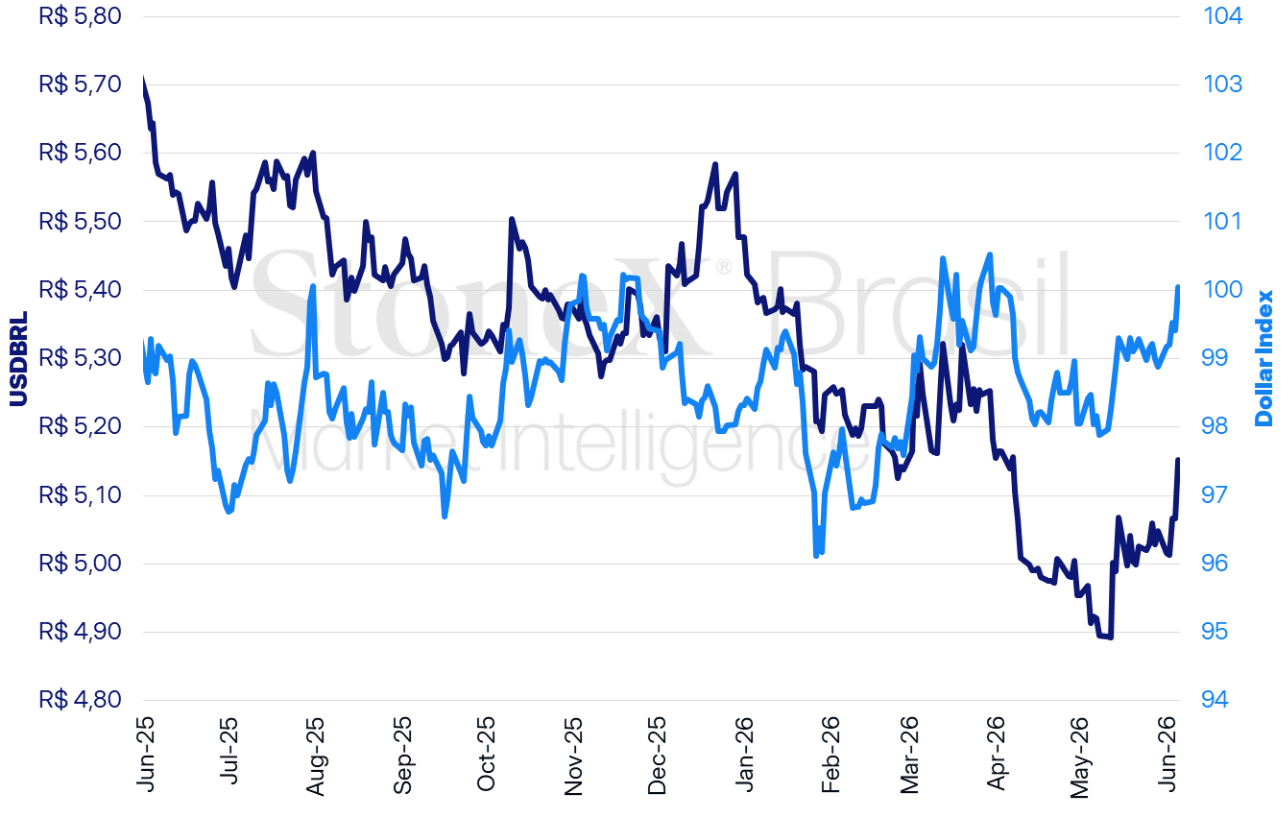

USD/BRL and Dollar Index (points)

Source: StoneX cmdtyView. Design: StoneX.

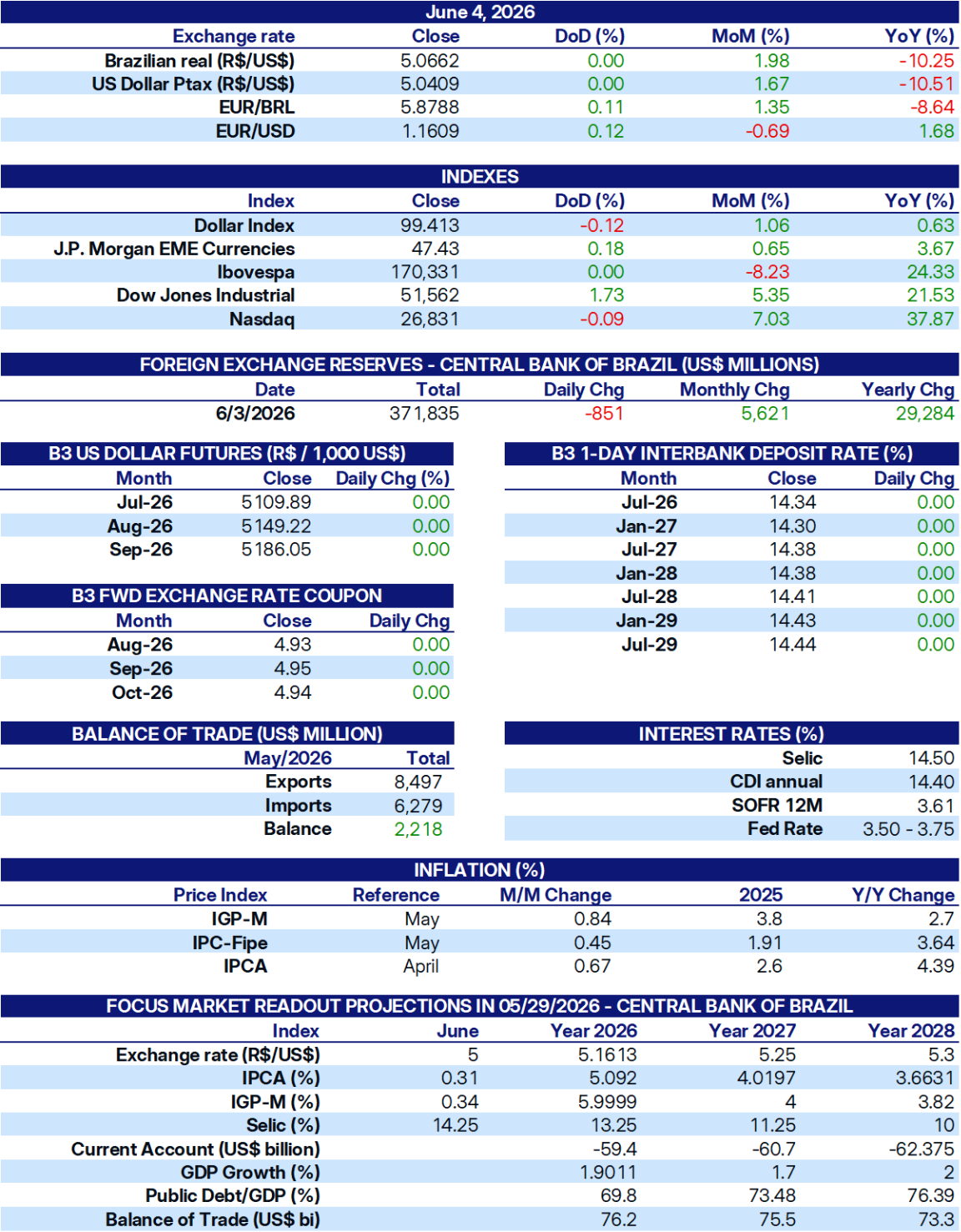

USDBRL Variations | Daily: +1.70% | Weekly: +2.07% | Monthly: +2.07% | Year-to-date: -5.93% | Last 12 months: -7.77%

Dollar index Variations | Daily: +0.64% | Weekly: +1.17% | Monthly: +1.17% | Year-to-date: +1.75% | Last 12 months: +1.28%

KEY EVENT: Inflation Data in the US

Expected impact on the BRL: bullish

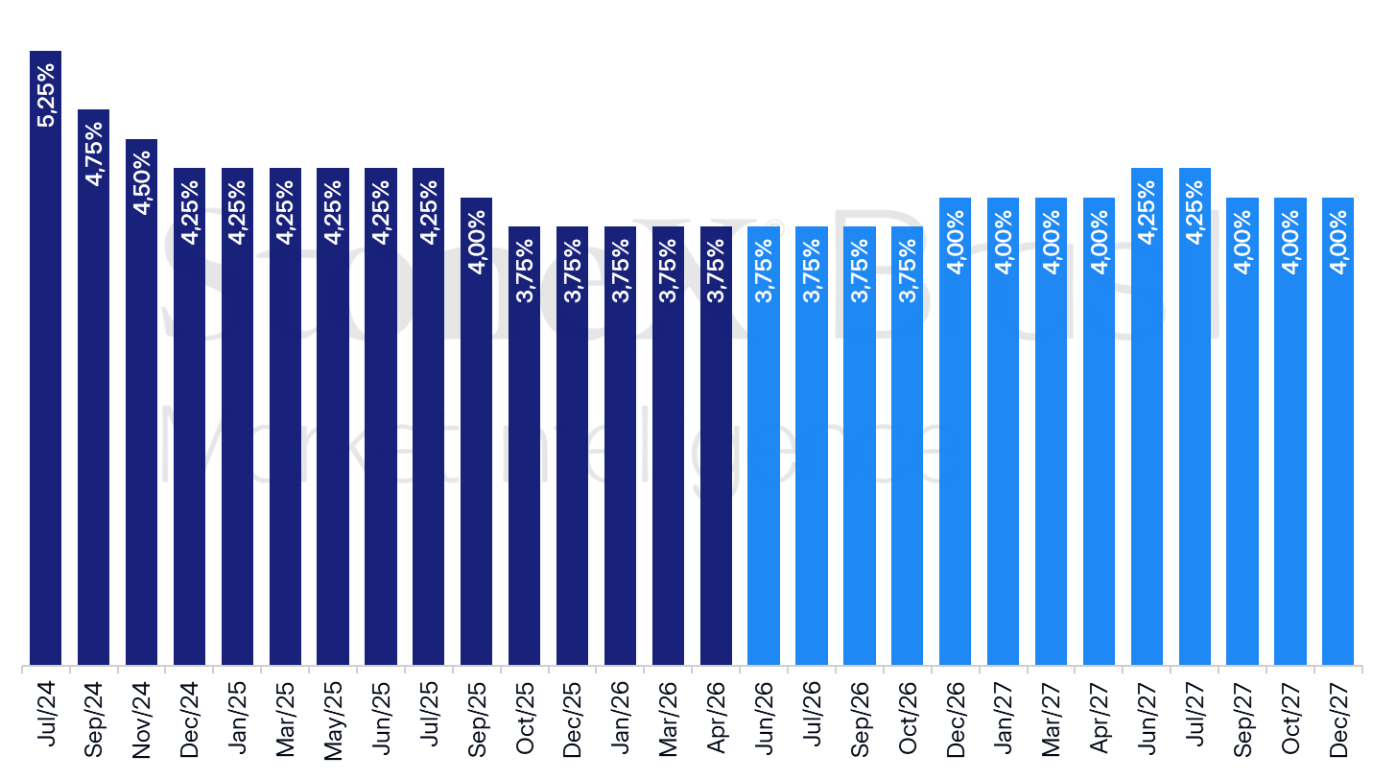

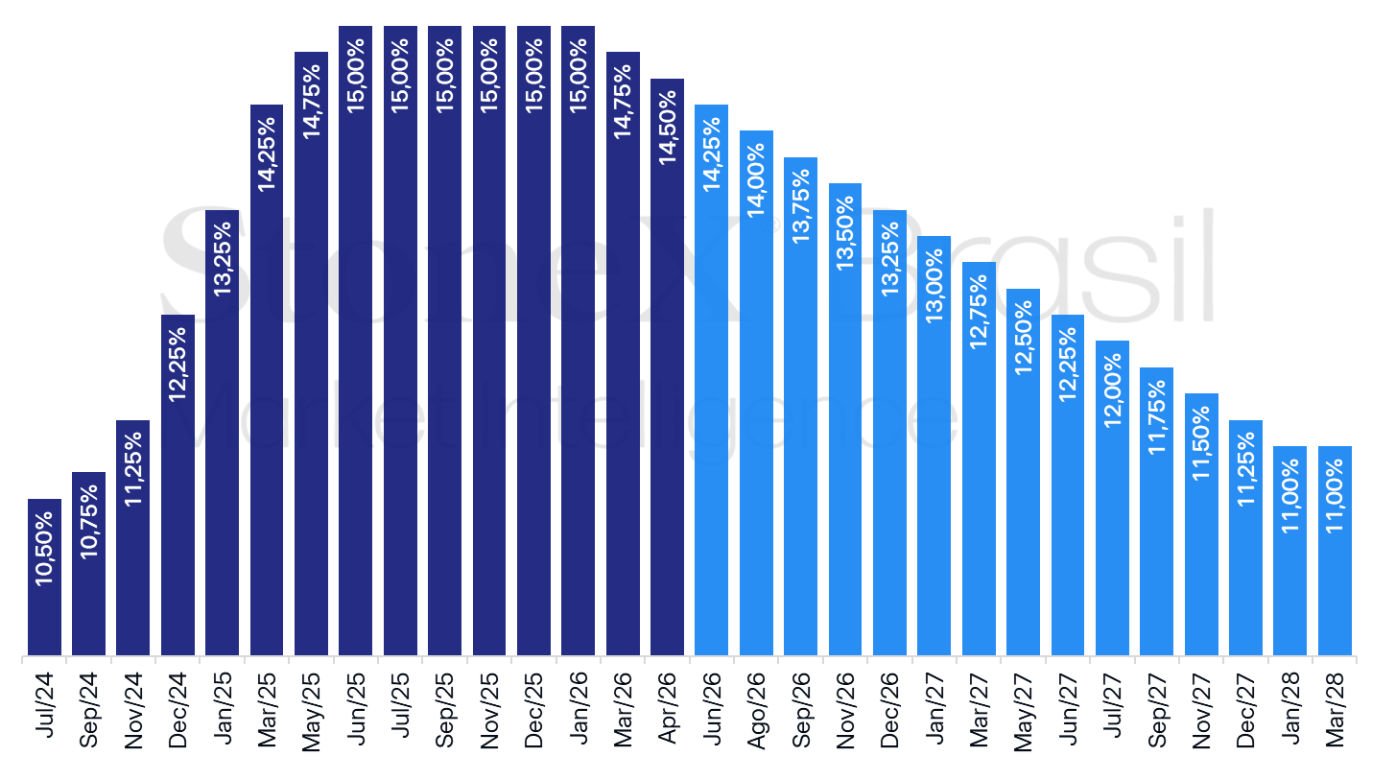

US: Historical and Expected Interest Rate – Updated June 5, 2026

Source: CME FedWatch Tool. Design: StoneX. Refers to the most probable market future interest rate bet on the indicated date.

The foreign exchange market is expected to react to the release of the US Consumer Price Index (CPI) and Producer Price Index (PPI) for May amid a series of robust indicators for the country.

Why This Matters: The data is expected to reinforce the perception of more persistent and widespread inflation in the US, increasing expectations for higher interest rates for longer in the country.

- This, in turn, tends to increase the yields on US Treasury securities (Treasuries) and attract foreign capital, strengthening the USD globally.

Estimates: The median estimates for the CPI indicate a slight decline in consumer inflation between April and May, from a 0.6% increase to 0.5% in the headline index and from 0.4% to 0.3% in its core measure, excluding volatile food and energy components.

- Meanwhile, the median estimates for the PPI foresee a sharper slowdown in producer inflation over the same period, from a 1.4% increase to 0.8% in the headline index and from 1.0% to 0.4% in its core measure.

- If confirmed, these figures point to more persistent and widespread inflation, necessitating higher interest rates to stabilize prices.

- Although much of the inflationary pressure remains tied to the closure of the Strait of Hormuz and fears of global oil supply shortages, there is significant spread beyond energy prices, primarily due to rising freight costs.

- Additionally, indications of inflationary pressures arise from the global shortage of semiconductors, driven by the rapid acceleration of investments in artificial intelligence-related infrastructure.

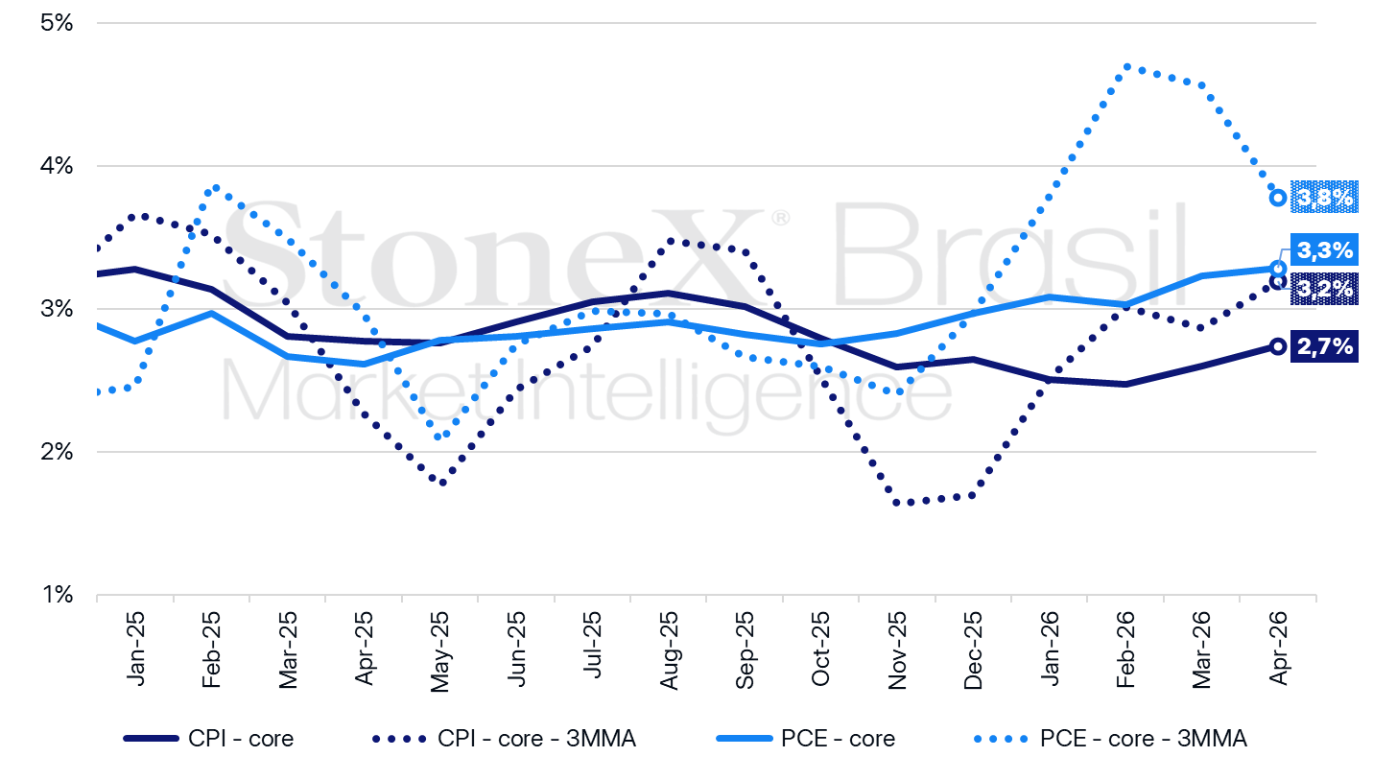

US Inflation Measures (%)

Source: US Bureau of Economic Analysis (BEA), US Bureau of Labor Statistics (BLS), Federal Reserve Bank of St. Louis. Design: StoneX.

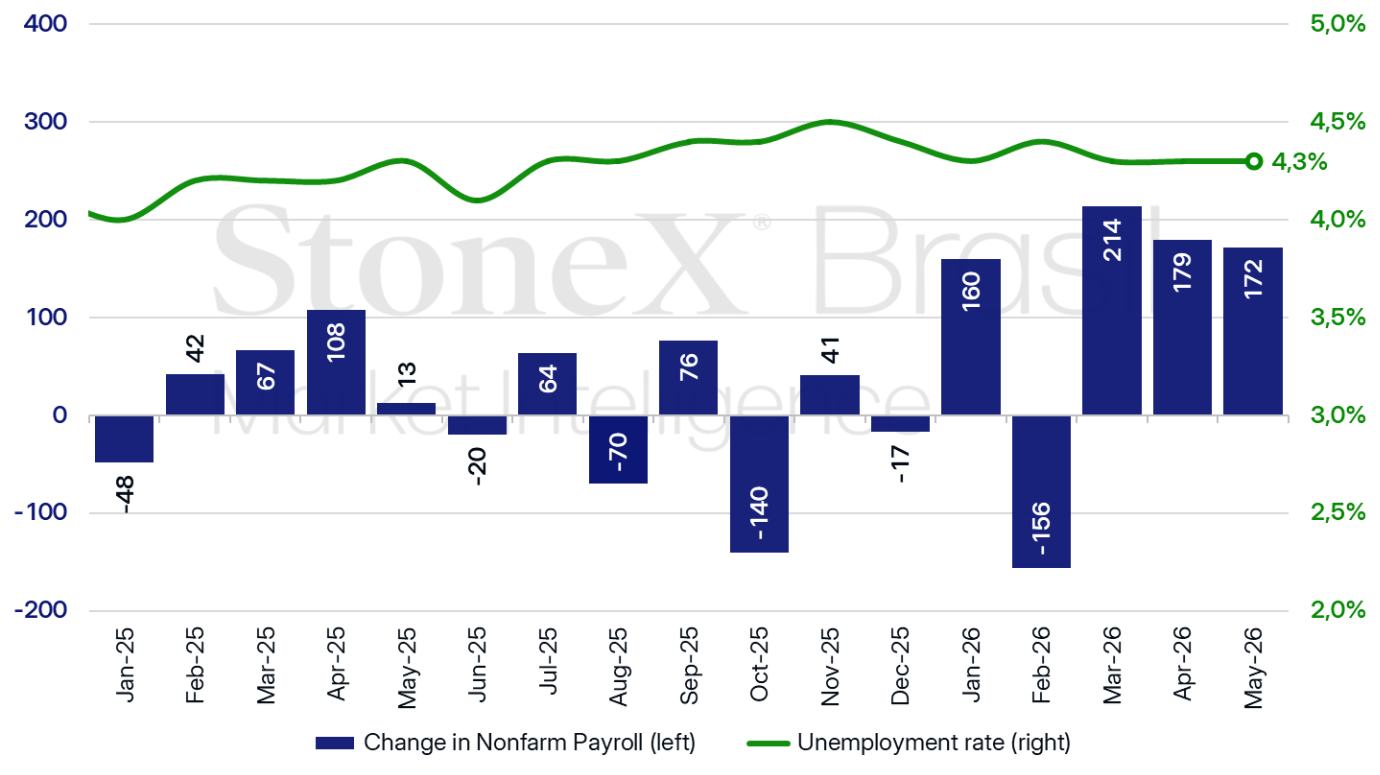

Full Speed Ahead: At the same time, last week's economic data points to a more vigorous US economy than anticipated, particularly concerning its labor market.

- The Employment Situation Report showed net job creation in the US was 172,000 in May, well above the median estimate of 85,000.

- Additionally, net job creation was revised from 115,000 to 179,000 in April and from 185,000 to 214,000 in March, suggesting strong demand for workers by US companies.

- The Job Openings and Labor Turnover Survey (JOLTS) for April surprised with the highest number of job openings since May 2024.

- Meanwhile, the Purchasing Managers' Index (PMI) for manufacturing accelerated its expansion to 54.0 points in May, the highest reading in four years, while the services PMI recorded 54.5 points in May.

Change in Total Urban Employment ('000 People) and Unemployment Rate (%) in the US

Source: US Bureau of Labor Statistics (BLS), Federal Reserve Bank of St. Louis. Design: StoneX.

No Room for Rate Cuts: Robust inflation and labor market data in the US have led investors to solidify bets on further interest rate hikes by the Federal Reserve in the future.

- The June 17 interest rate decision will be crucial for calibrating agents' expectations regarding the country's interest rate trajectory.

- Firstly, as it will be the first decision with Kevin Warsh as Federal Reserve Chair, from whom investors expect greater receptivity to White House demands for lower rates.

- Additionally, due to updates to Fed members' macroeconomic projections for variables like GDP, inflation, unemployment, and interest rates.

- Finally, due to the more cautious stance of various Fed members, who have warned of greater inflation risks compared to labor market risks.

Geopolitical Stalemate in the Middle East

Expected impact on the BRL: bullish

Investors are also expected to react to the prolonged uncertainty regarding a possible end to the Middle East conflict, amid contradictory news about diplomatic negotiations between the US, Iran, Israel, and Lebanon.

Why This Matters: Reduced expectations for a swift peace agreement to reopen the Strait of Hormuz tend to heighten geopolitical risk perceptions among investors, which could negatively affect risky assets like the BRL.

Advances and Setbacks: In the previous week, media reports stated that Washington and Tehran had reached a consensus to sign a Memorandum of Understanding, but no formal agreement was made.

- Last week, Iran announced that diplomatic negotiations were interrupted due to Israeli attacks on Lebanon.

- Additionally, various military clashes were reported in the region involving both the US and Iran.

- On Wednesday, US President Donald Trump announced a ceasefire between Lebanon and Israel, but the Hezbollah militant group rejected the agreement, and Israel stated it would not withdraw its troops or halt its military operations in Lebanon.

Delay in Normalization: It is worth remembering that even if countries quickly resolve the stalemate, there will be delays in normalizing oil flows in the Strait of Hormuz.

- The first obstacle would be the time needed to remove mines in the region to allow ships to navigate safely.

- Additionally, due to export restrictions on crude oil, companies are operating at reduced capacity and would require weeks to restore operations to pre-war levels.

- Finally, there would still be the transit time of the energy commodity from the Middle East to its destination, as tankers move slowly.

- In this context, even with an immediate resolution, the time required to normalize the entire chain should keep oil prices elevated, sustaining global inflationary concerns.

Inflation in Brazil

Expected impact on the BRL: bullish

Brazil: Historical and Expected Interest Rate – Focus Bulletin of May 29, 2026

Source: Central Bank of Brazil. Design: StoneX.

Domestically, investors are expected to follow the May reading of the Broad National Consumer Price Index (IPCA).

- The median estimates from the Focus Bulletin point to inflation of 0.47% for the month, which would represent a slowdown compared to the previous reading of 0.67%.

- With this result, the inflation accumulated over the last 12 months should rise from 4.39% to 4.61%, exceeding the 4.5% ceiling of the Central Bank's target.

Why This Matters: Signs of lower inflationary pressures tend to increase bets for further cuts in the benchmark interest rate (Selic), which could reduce the attractiveness of domestic bonds and weaken the real globally.

- On the other hand, inflationary expectations among investors have been steadily rising due to fears of global oil supply shortages and higher international energy prices.

Recent Data: The latest release of the Broad National Consumer Price Index 15 (IPCA-15) indicated a monthly slowdown, despite the 12-month accumulated index rising to 4.64%.

- Additionally, the indicator's core measure, which excludes volatile food and energy components, showed a solid increase of 0.46%.

- In the most recent edition of the Focus Bulletin, the median projections for the year-end accumulated IPCA rose for the 12th consecutive week.

Less room for rate cuts? Advances in accumulated inflation and projections from the Focus Bulletin reinforce the perception of deteriorating inflation expectations, which could limit the Selic rate cut cycle.

- One factor for this shift is the persistence of the Middle East conflict, which reached the three-month mark last week.

- In addition to higher oil prices—which already have global inflationary potential—other central banks are revising their monetary policies and adopting a more restrictive tone.

- This could limit broader interest rate cuts in Brazil, as potential reductions in the interest rate differential could globally weaken the real and add another element of inflationary pressure.

Eurozone Interest Rate Decision

Expected impact on the BRL: bearish

Next week, there is almost consensus that the European Central Bank (ECB) will raise its benchmark interest rate from 2.00% to 2.25% per year.

- Additionally, investors are betting on another hike later in the year due to inflationary pressures stemming from the Middle East conflict.

Why This Matters: The increase in the benchmark interest rate is expected to strengthen the EUR against the USD.

- This, in turn, could indirectly favor the performance of the BRL due to potential weakening of the USD.

Overview: Until the start of the Middle East conflict, inflation accumulated over the previous 12 months was near the 2% target for about a year.

- However, with the onset of the conflict, the preliminary reading of May's Consumer Price Index (CPI) indicated 12-month accumulated inflation of 3.2%.

- During a conference, ECB board member Isabel Schnabel stated, "We can no longer ignore this shock," indicating a firmer stance by the monetary authority to control prices in the euro area.

INDICATORS

Sources: Central Bank of Brazil; B3; IBGE; Fipe; FGV; MDIC; IPEA and StoneX cmdtyView.