Dollar to Reflect Interest Rate Decisions in Brazil and the US, As Well As Expectations for Middle East Peace Agreement

- Bullish

- The Federal Reserve's interest rate decision is expected to reinforce expectations of higher rates for longer in the US, favoring the yield of US Treasury bonds and strengthening the USD globally.

- The Copom is expected to reduce the benchmark interest rate (Selic) by 0.25 p.p., which tends to decrease the yield of domestic public bonds and harm the attraction of foreign capital, weakening the BRL.

- Bearish

- Expectations for a diplomatic agreement between the US and Iran that allows the reopening of the Strait of Hormuz should increase investors' risk appetite, which tends to depreciate the USD globally.

The Week in Recap

- Contradictory news in the Middle East kept financial markets volatile, alternating between raising and lowering hopes for a peace agreement in the region.

- In Brazil, the accumulated National Consumer Price Index (IPCA) rose to 4.72%, above the target ceiling. Additionally, the core of the index also accelerated, generating concerns about more persistent inflation.

- In the US, the core Consumer Price Index (CPI) rose less than expected in May, with an increase of 0.2%, partially alleviating concerns about the American inflation scenario.

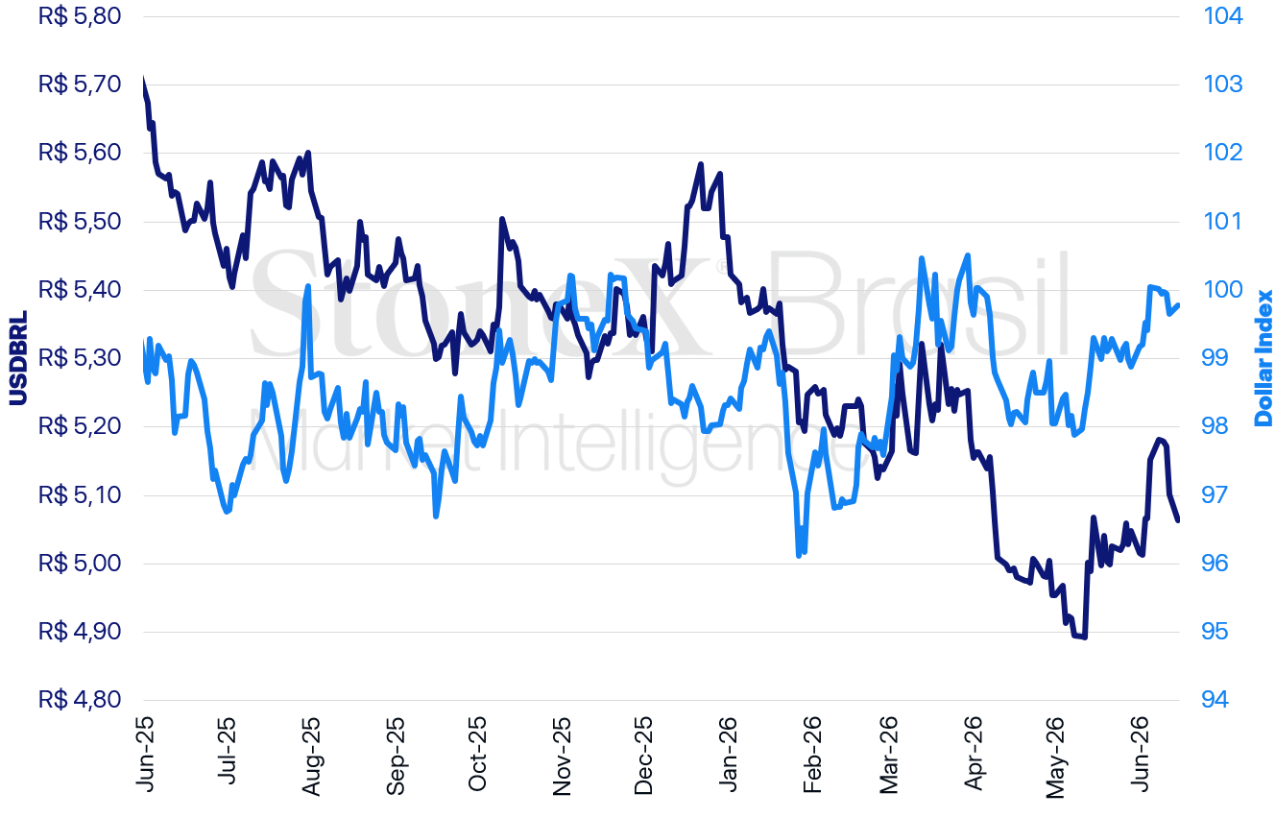

USDBRL and Dollar Index (points)

Source: StoneX cmdtyView. Design: StoneX.

USDBRL Variations | Daily: -2.09% | Weekly: -1.72% | Monthly: +0.31% | Annual: -7.55% | In 12 months: -8.65%

Dollar Index Variations | Daily: -0.17% | Weekly: -0.27% | Monthly: +0.90% | Annual: +1.48% | In 12 months: +1.90%

KEY EVENTS: Federal Reserve interest rate decision

Expected Impact on the BRL Exchange Rate: Bullish

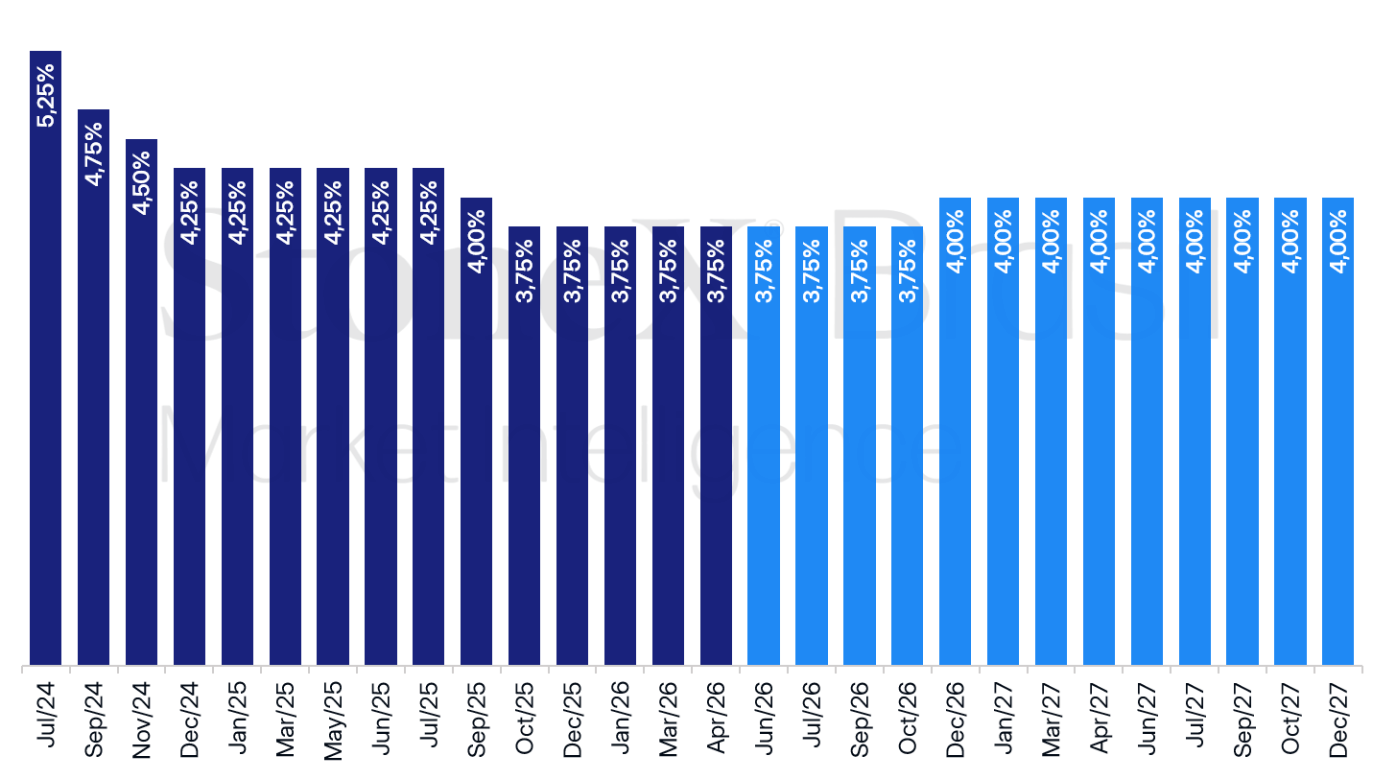

US: History and Expectations for Interest Rates – Updated June 12, 2026

Source: CME FedWatch Tool. Design: StoneX. Refers to the most probable market bet on interest rate futures as of the indicated date.

The Federal Open Market Committee (FOMC) of the Federal Reserve (Fed) is expected to keep its benchmark interest rate unchanged in its decision this Wednesday (17), in the range of 3.50% to 3.75% p.a.

- Since there is virtually a consensus on the decision, investors are likely to focus their attention on changes in the Statement, updates to the Summarized Economic Projections, and the first press conference by Kevin Warsh as president of the institution.

Why This Tatters: The expectation of a more cautious Federal Reserve stance is likely to reinforce bets on higher rates for longer in the country.

- This, in turn, tends to increase the yield of US Treasury bonds (Treasuries) and favor the attraction of foreign capital, strengthening the USD globally.

Heated US Economy: Recent data for the United States points to a stronger-than-anticipated economy, with a reacceleration of the labor market over the last three months.

- On the other hand, inflation indices are accelerating, mainly driven by the rapid rise in energy item prices following the start of the conflict between the United States, Israel, and Iran.

- This inflationary pressure has also spread at a slower pace to other goods and services in the country, as observed in the core indicators, excluding volatile components such as food and energy.

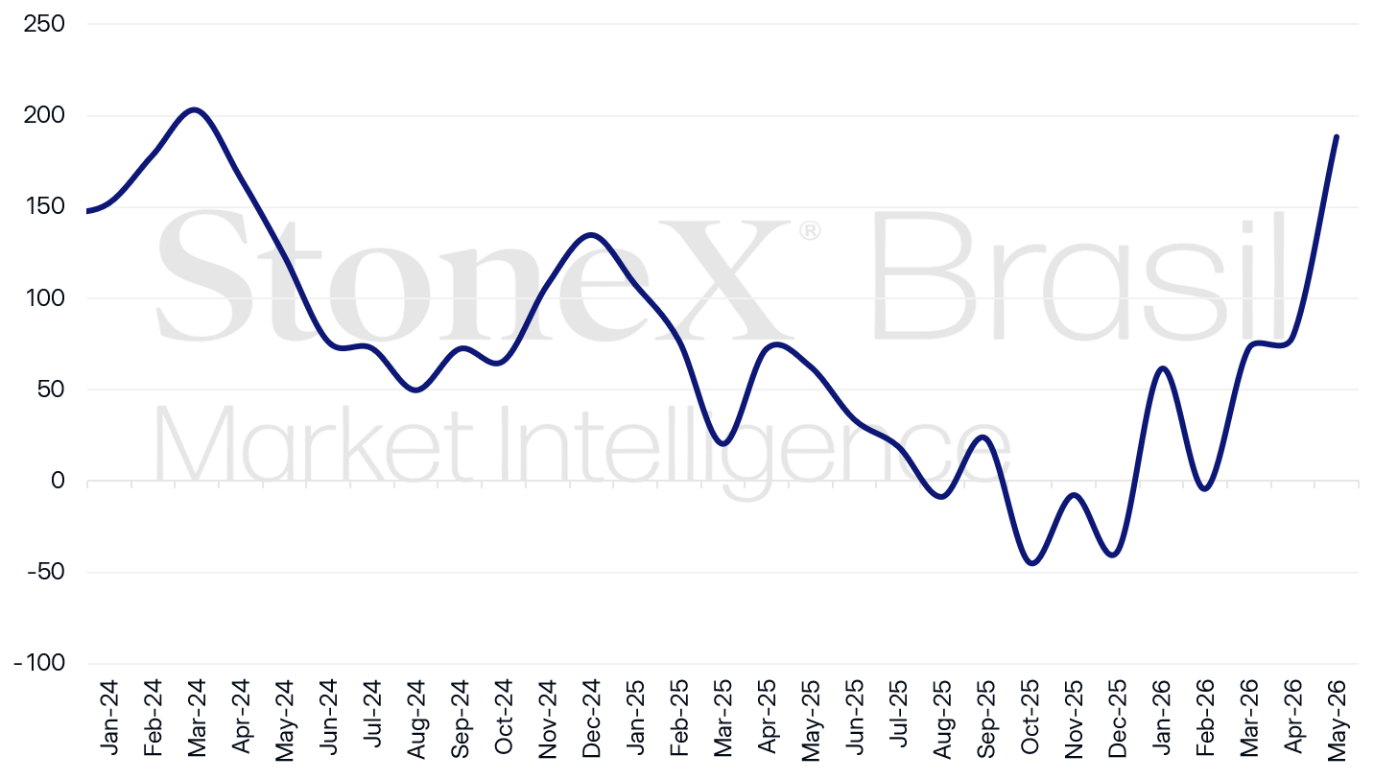

Change in Total Urban Employment in the United States – 3-Month Average (000 People)

Source: U.S. Bureau of Labor Statistics (BLS), Federal Reserve Bank of St. Louis. Design: StoneX.

Some Counterpoints for the Labor Market: Although net urban job creation in the US has intensified over the last three months, other indicators suggest that the labor market does not yet pose a more serious inflationary risk.

- Firstly, despite the strong hiring pace reported by companies, the unemployment rate, calculated through household surveys, remained stable at 4.3% during this period.

- Additionally, labor income also remained stable during the period.

- Therefore, without an acceleration in labor income or a drop in the unemployment rate, it is unlikely that FOMC members will conclude that the labor market is overheating.

What to Expect From the FOMC: Normally, the Federal Reserve moves gradually when deciding to modify its monetary policy, meaning abrupt changes in stance are rare.

- As such, the first step is expected in this Wednesday's (17) decision, with the removal of the dovish bias (i.e., the next step will likely be a rate cut) from the Statement.

- This would signal that the balance of risks for the US economy is neutral, meaning the risks of labor market weakening are approximately equal to the risks of inflation acceleration.

- If the inflationary scenario remains challenging, the next step would be the inclusion of a hawkish bias in the Statement, indicating the need for tighter financial conditions.

- This could occur in the July or September rate decision.

- Finally, a rate hike, if deemed necessary, would be more likely in the October or December decision.

Subtle Adjustments are Uncommon: It is worth noting that when a Central Bank evaluates the need to change its monetary policy, whether with higher or lower rates, it is rare for it to decide that just one increase or decrease of 0.25 p.p. is sufficient to reposition its stance.

- The most common scenario involves a sequence of consecutive increases or decreases over several meetings.

- In other words, if the Federal Reserve at some point concludes that inflation risks outweigh economic activity weakening risks, it is highly unlikely that it will raise rates only once, as current investor bets indicate.

- Such a scenario would likely involve at least two or three consecutive 0.25 p.p. rate hikes.

- Therefore, the most likely scenario at the moment is for US rates to remain stable throughout the year.

- This scenario is reinforced by Kevin Warsh's beginning term as Fed president, from whom investors expect greater receptiveness to White House demands for lower rates.

- Since Warsh would face significant difficulty in seeking a consensus to reduce rates in the current framework, it is more likely that he will aim to consolidate the view that rate hikes are not yet necessary for the US economy.

Interest Rate Decision in Brazil

Expected Impact on the BRL Exchange Rate: Bullish

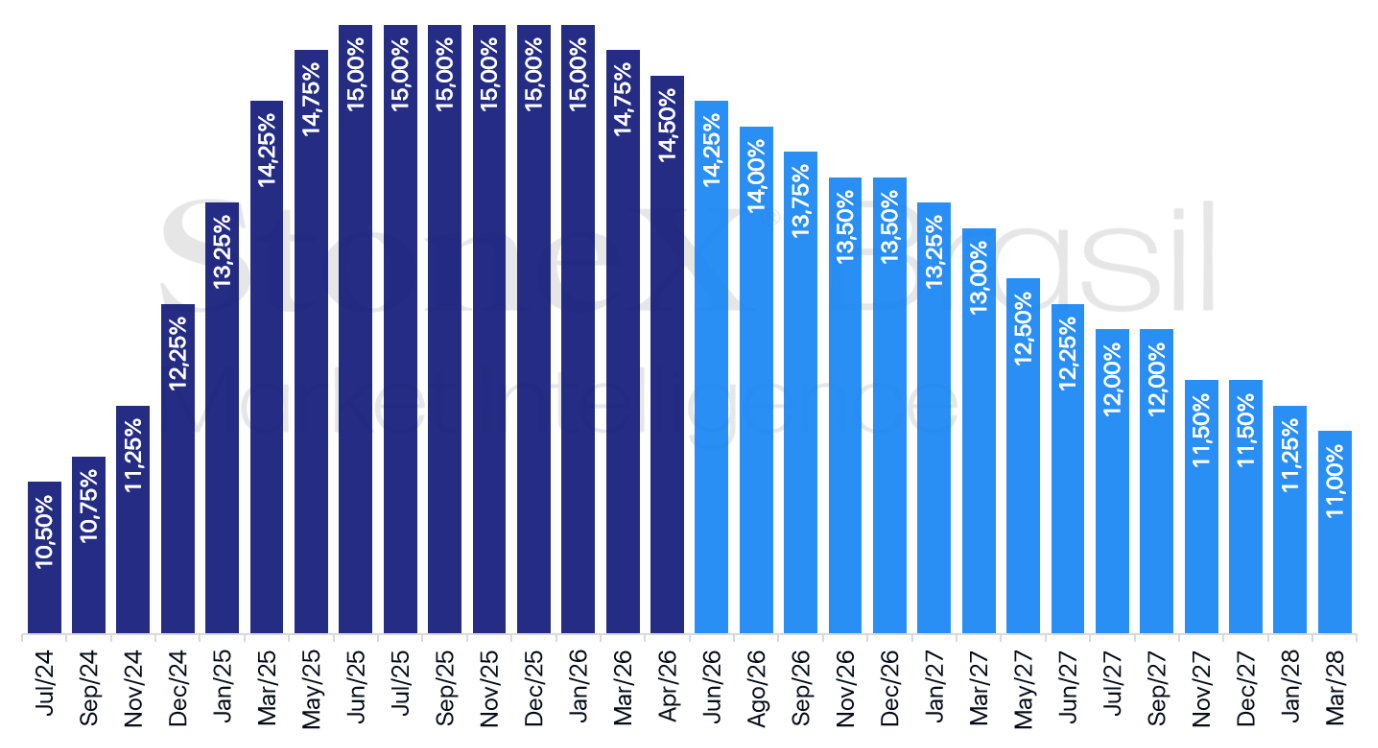

Brazil: History and Expectations for Interest Rates – Focus Bulletin Dated June 5, 2026

Source: Banco Central do Brasil. Design by: StoneX.

On Wednesday (17), the median of estimates points to the Monetary Policy Committee (Copom) of the Central Bank (BC) reducing the benchmark interest rate (Selic) from 14.50% to 14.25% per year.

Why This Matters: The reduction in the Selic rate tends to decrease the yield of domestic public bonds and harm the attraction of foreign capital, weakening the BRL.

Inflationary challenges: Although Copom is in a cycle of Selic cuts, inflationary challenges remain the primary concern, especially with the Middle East conflict extending into its fourth month, which may limit the cycle of cuts.

- Last Friday (12), the May reading of the accumulated National Consumer Price Index (IPCA) rose from 4.39% to 4.72%, above the inflation target ceiling of 4.5%.

- Additionally, the core indicator, excluding volatile items such as food and energy, rose 0.41%, indicating that energy item inflationary pressures are spreading to other goods.

- Until the onset of the Middle East conflict in late February, the accumulated IPCA was at 3.81%, within the target, reinforcing the war's impact on domestic prices.

Rate Trajectory: According to the latest Focus bulletin, the median expectation is for Copom to continue cutting the Selic rate by 0.25 percentage points in the next four meetings while keeping it stable at the last meeting of the year, ending the year at 13.50% per year.

- However, the evolution of the inflation trajectory will be crucial for defining monetary policy. If inflationary pressures persist, Copom may adopt a more restrictive tone.

- Signals of diplomatic progress between the US and Iran and the reopening of the Strait of Hormuz should remain on investors' radar.

- For comparison, since the beginning of the conflict, Focus bulletin projections for the year-end Selic rate have risen from 12.00% to 13.50%.

Diplomatic progress in the Middle East

Expected Impact on the BRL Exchange Rate: Bearish

This week, investors are expected to continue following the back-and-forth news about diplomatic negotiations between the US and Iran.

- Currently, expectations are that the countries may sign a peace agreement as early as this Sunday (14) in Geneva, Switzerland.

Why This Matters: The possibility of ending the Gulf conflict reduces geopolitical risk perceptions among investors, favoring the performance of assets considered risky, like the BRL.

- Additionally, the potential reopening of the Strait of Hormuz alleviates inflationary fears caused by a global oil shortage, reducing the dollar's attractiveness as a safe-haven asset.

Positive signals from both sides: US President Donald Trump stated, "We have made a great deal to end the war with Iran," and that the Strait of Hormuz will officially reopen once the memorandum is signed.

- According to Iran's Ministry of Foreign Affairs spokesperson, Esmail Baghaei, the Persian nation has reached "understandings" on most issues with the US, and the process is in its final stages of "internal conclusions."

Terms and Conditions: Despite positive signals regarding the proximity of a diplomatic resolution, the terms of the agreement remain unclear.

- Reported terms include a ceasefire on all combat fronts, including Lebanon, reopening of the Strait of Hormuz without toll charges, lifting the US naval blockade, easing sanctions against Iran, and the Persian nation's commitment not to develop a nuclear weapon.

- However, media outlets from both countries differ on some points regarding the terms, especially concerning control over the Strait of Hormuz passage and Iran's right to enrich uranium.

- In this context, President Donald Trump accused Iran of acting in bad faith during negotiations and stated that the information provided by the country does not reflect what was agreed upon.

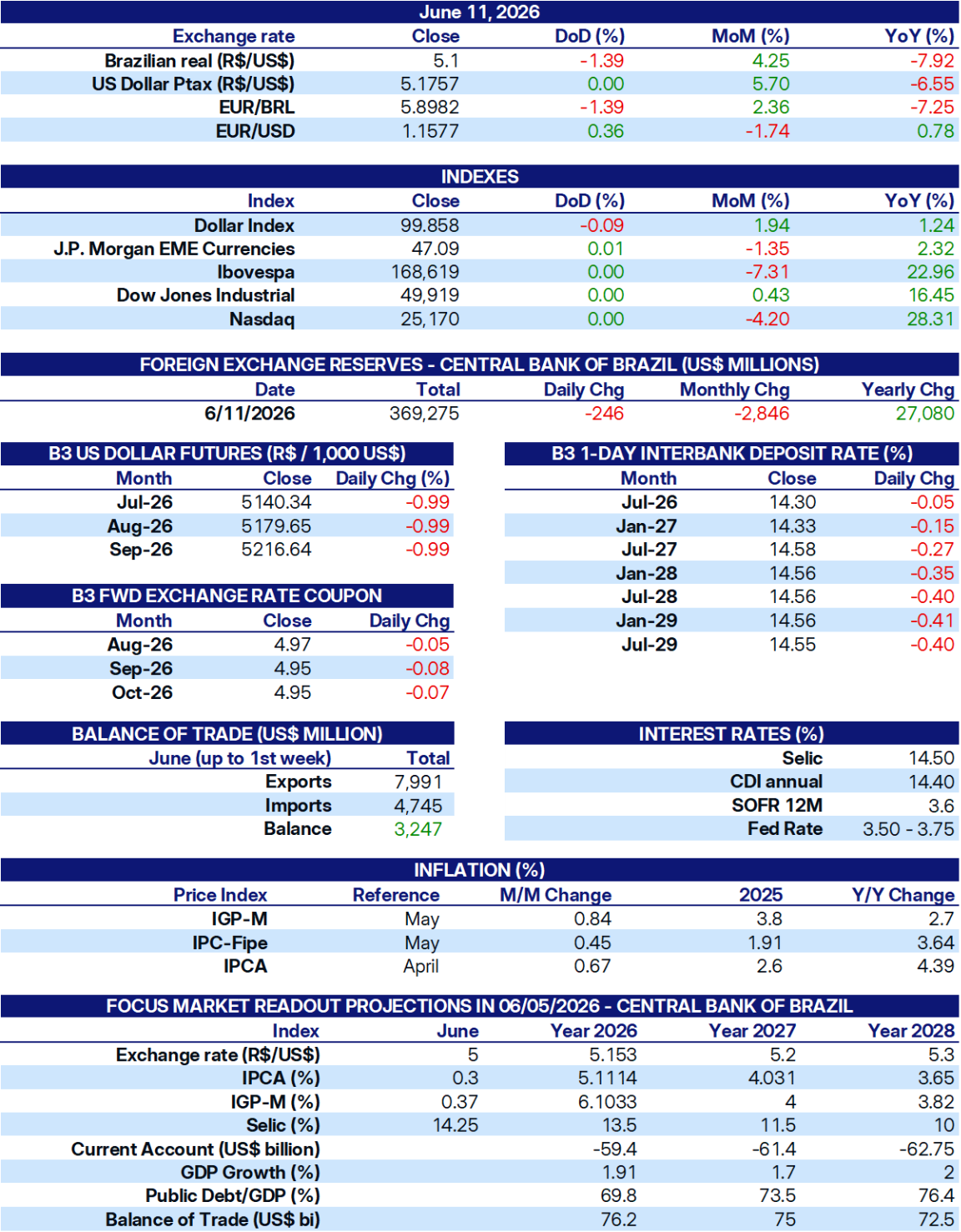

INDICATORS

Sources: Central Bank of Brazil; B3; IBGE; Fipe; FGV; MDIC; IPEA, and StoneX cmdtyView.