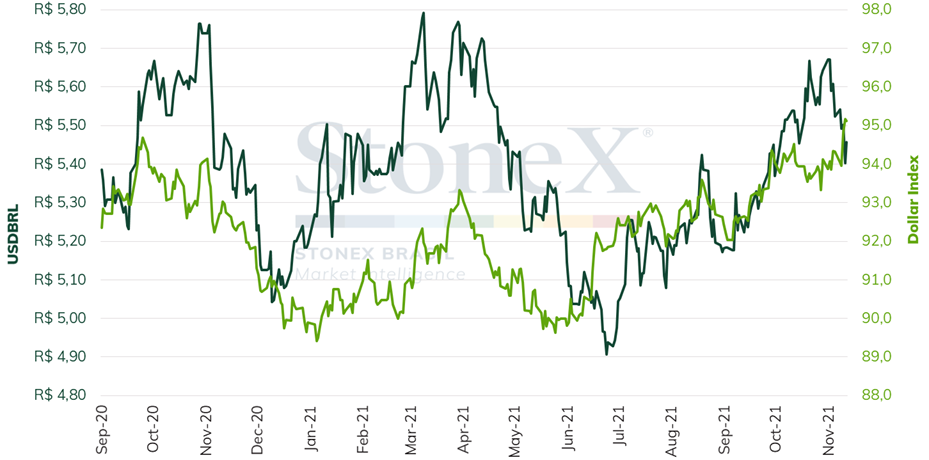

Foreign scenario

Following the stronger-than-expected Consumer Price Index (CPI) reading for October, particularly for housing-related components, attention will turn to the Federal Reserve's members (Fed) who have public statements scheduled for next week to gauge whether any of them will change their discourse on the key features of the current inflationary acceleration or projections for interest rate increases in the economy. Thomas Barkin, Raphael Bostic, Mary Daly, John Williams, Michelle Bowman, Christopher Waller, Charles Evans, and Richard Clarida are scheduled to speak. In addition, at the next meeting of the Federal Open Market Committee (FOMC) on December 15, its members will release their projections for key macroeconomic variables, such as forecasts of appropriate interest rates ("dot plot"), real GDP growth and inflation for the coming years.

Democratic members of Congress seek to pass legislative measures from US President Joe Biden's economic plan this week. Last week, the House of Representatives approved a bipartisan package of USD 1.2 trillion in infrastructure investments over ten years, a package that had already passed the Senate. However, Democrats remain at odds over another bill for investments in education, health care, immigration, climate, and taxation, worth approximately USD 2 trillion. With a unified Republican opposition and amid accelerating price levels, it is resistance within the Democratic party itself that has prevented this important victory for President Biden on one of his key election promises.

It is also worth noting that reports indicate that President Biden is close to announcing his choice for Fed Chairman. The current president's term, Jerome Powell, ends in February, but Biden's nomination will need to be confirmed by the US Senate. According to these reports, it is most likely that the president will again nominate Powell for the post, even though Donald Trump chose him for his first term. A second possibility would be Federal Reserve Governor Lael Brainard, who was reportedly interviewed for the position last week.

Domestic scenario

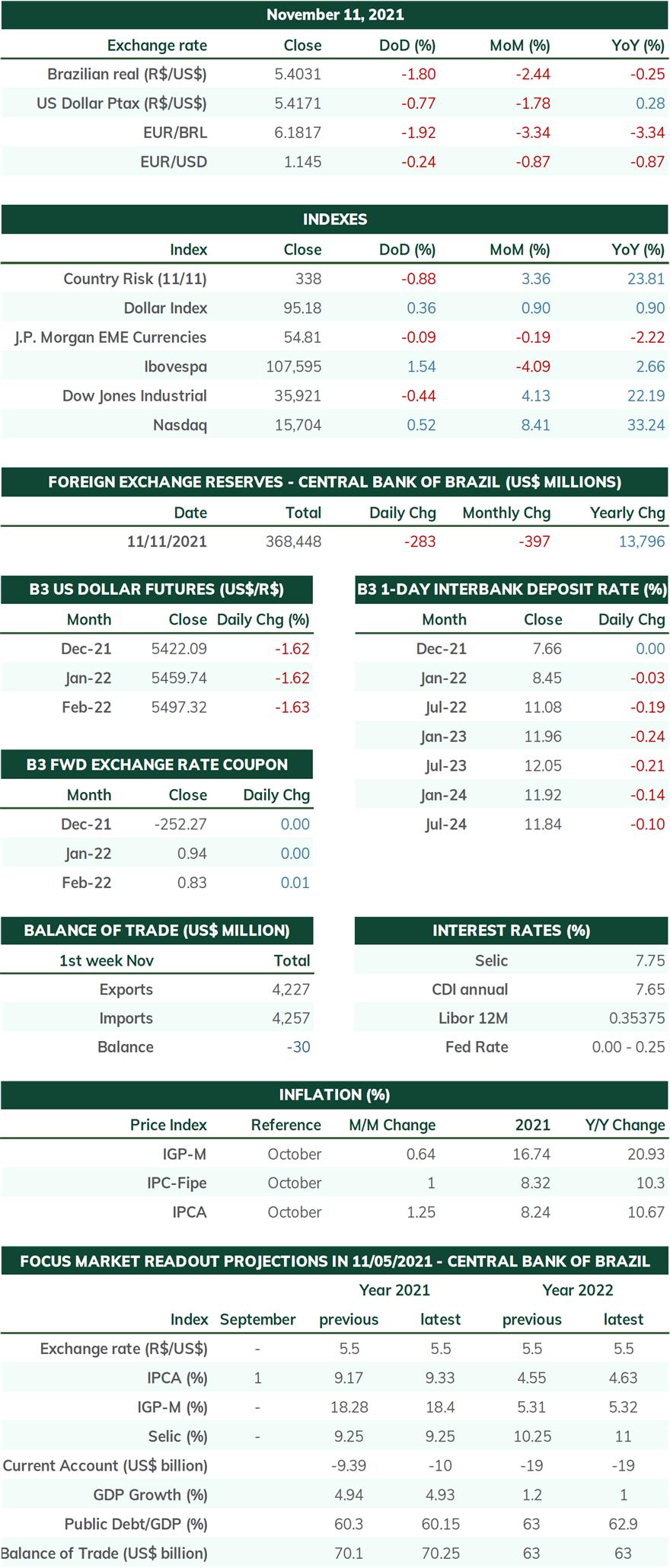

Next week's schedule will be empty of domestic indicators. The highlight is the Central Bank's Economic Activity Index (IBC-Br) for September, which should register a slight drop after the Brazilian Institute of Geography and Statistics released this week below-expected performances for industrial production, retail sales volume, and services volume for the month. Industrial production contracted by 0.4% in October, 2.2% in the third quarter and 6.3% year-to-date. The volume of retail sales shrank by 1.3% in October, 2.6% in the July-September quarter, and 0.6% in 2021. The volume of services, in turn, shrank by 0.6% in October but accumulated 0.9% in the third quarter and 7.1% in 2021. These performances reinforce the perspective that the GDP for the third quarter should remain close to stability or even register a slight reduction.

The outlook for the second half of the year is more challenging, with a drop in the population's average income, rising interest rates, which make credit more expensive, and increased inflationary pressure. This week, the Brazilian Institute of Geography and Statistics (IBGE) released that the National Broad Consumer Price Index (IPCA) increased by 1.25% in October, above the median of analysts' expectations, which pointed to a growth of 1.0%. It is the highest increase for the month since 2002. The indicator has accumulated 8.24% for the year and 10.67% for the last 12 months. All of the nine subgroups surveyed showed price hikes, especially Transportation (+2.62%), Clothing (+1.80%), Household items (+1.27%), Food and beverages (1.17%), and Housing (1.04%). Thus, the inflationary pressure seems to be becoming more comprehensive. In this sense, several institutions this week raised their expectations for 12-month accumulated inflation in 2021, with part of the projections starting to signal an IPCA of around 10.0% by the end of December. Thus, bets are also growing that the Monetary Policy Committee (Copom) will adopt a more contractionary stance at its December meeting to try and combat the inflationary process. Although the committee has signaled that it foresees a 1.5 p.p. readjustment in the basic interest rate (Selic) in its next meeting in December, some analysts believe in an even higher increase, of 1.75 p.p. or even 2 p.p.

Finally, it is worth pointing out that the markets are showing greater optimism after the Chamber of Deputies approved the second round of the basic text of the PEC of judiciary bonds (PEC 23/21), which, in a nutshell, allows the government to expand its spending capacity by extending the payment of a substantial part of the judicial debts with definitive sentences and by altering the period for calculating the correction of the constitutional spending limit. Furthermore, despite weakening the fiscal precepts of the public sector, the fact that the government will define its funding source for its election measures in 2022 has reduced uncertainties for the coming year. According to estimates released by the Ministry of Economy, PEC 23/21 adds BRL 91.6 billion in additional space to the 2022 Budget, of which BRL 47 billion comes from the change in the calculation of the spending cap and BRL 44.6 billion from the postponement of the commitment to honor the government's judicial commitments. Also, according to the Ministry, of these BRL 91.6 billion, the Executive intends to allocate BRL 50 billion to temporarily increase the average benefit of the Auxílio Brasil income transfer program (which will replace Bolsa Família) from BRL 191 to BRL 400/month, effective until December 2022, an election year. In addition, at least BRL 10 billion will be earmarked for "mandatory expenses and society's demands," according to "Congress' decision."