Foreign Scenario

The war between Russia and Ukraine is now six weeks old, and there is still little clarity about what its outcome may be. Negotiations for a possible ceasefire have stalled after the heinous scenes uncovered in Bucha, on the outskirts of Kiyv, this week. The United States and other allied nations have harshly condemned what they called a war crime and implemented new rounds of sanctions against Moscow, increasing the country's geopolitical and economic isolation. The European Union banned the import of coal, among other products, and the export of advanced materials and further restricted Russian ships and banks from doing business with the economic bloc. The US Congress ratified the ban on Russian oil, natural gas and coal imports and excluded Russia and Belarus from preferential economic partner status, making the sanction a law. Thus, the United States may apply differentiated economic tariffs on these countries.

This week, investors will await the publication of the Consumer Price Index (CPI) for March, which is expected to rise due to the effects of the conflict in Eastern Europe. After a 0.6% increase in January and 0.8% in February, the median of analysts' estimates points to a 1.1% increase in March, which would bring the accumulated figure in 12 months to 8.4% – its highest value since December 1981. In addition, other productive activity data for the US, such as retail sales and industrial production, should reveal that economic growth remains healthy, while the price index should keep accelerating for a few more months.

The March monetary policy decision minutes were considered firm by market analysts, as they indicated that the Federal Open Market Committee (FOMC) members were open to a 0.50 percentage point interest rate adjustment already at the previous meeting and set an accelerated pace of asset reduction on the US central bank's balance sheet. For this reason, attention should also continue to be focused on public statements from members of the Federal Reserve (Fed) as analysts try to gauge how many interest rate hikes will be seen this year. The public speeches by Raphael Bostic, Michelle Bowman, Charles Evans, Lael Brainard, Thomas Barkin, Loretta Mester, and Patrick Harker are scheduled for this week.

Finally, investors will also follow news about the Covid-19 contagion that China is going through and the containment measures being put in place. This week, the isolation measures in Shanghai were deepened, as the two-phase approach did not have the desired effect. The Asian country is experiencing the worst wave of Covid-19 and the biggest lockdowns since the new disease was discovered in late 2019, as the highly infectious omicron variant exponentially raises the economic, social and political costs of the "zero Covid" strategy and reaps fewer and fewer benefits. Shanghai remains in lockdown with no end date, burdening the logistics chain of the country's industrial hub and site of the world's largest port terminal. Although the port remains in partial operation, businesses and cargo sheds were forced to close during the lockdown, causing delays and hampering port operations. The new coronavirus strains defy the practicality of isolating entire metropolises for weeks, repeatedly, at the enormous political and economic expense.

Domestic Scenario

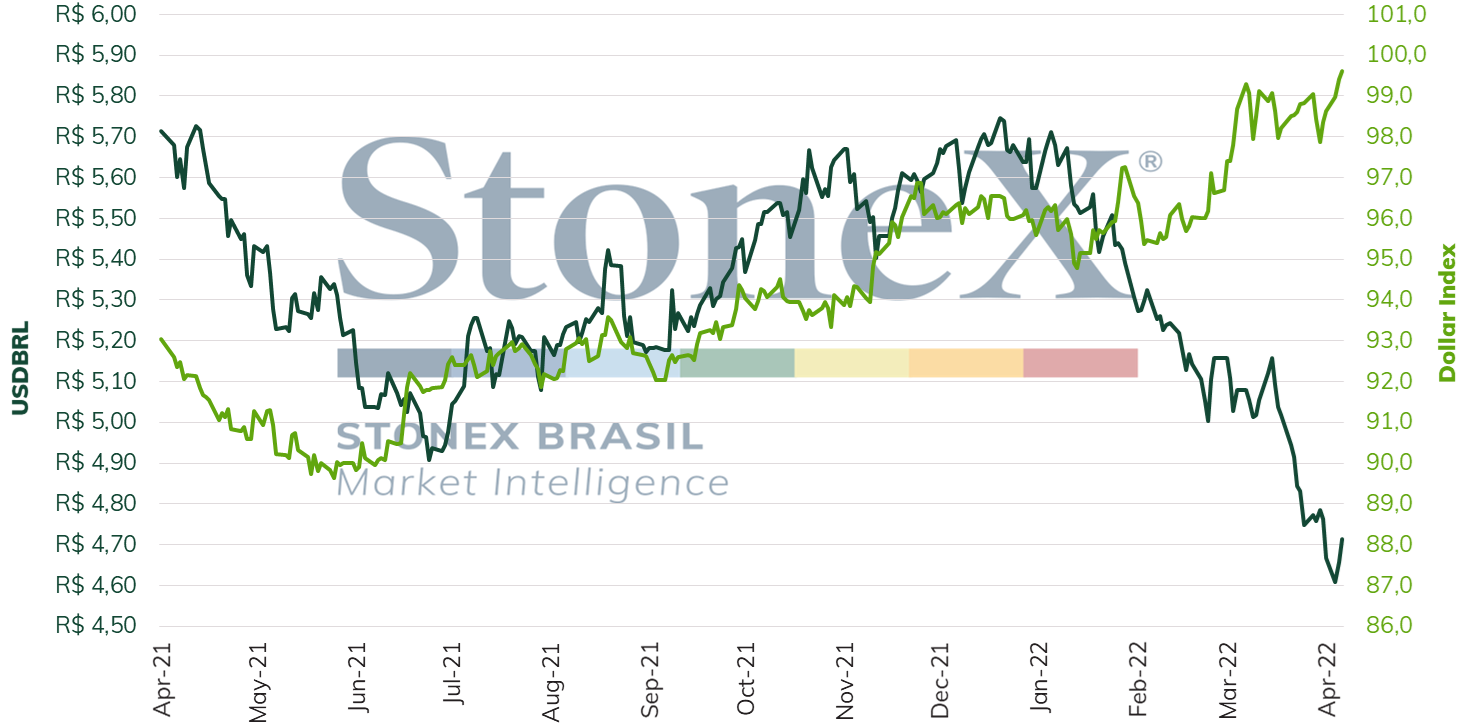

Last week, the consolidation of expectations of a rigorous monetary tightening by the United States in a few months in a scenario of exacerbated uncertainty and volatility – mainly due to the conflict between Russia and Ukraine, but, to a lesser extent, to the possibility of the victory of the extreme right in the French presidential elections -, provoked strong gains in the dollar against other currencies. The dollar index reached 100 points for the first time in almost two years, and the BRL, which had appreciated against the American currency for five consecutive weeks, retreated.

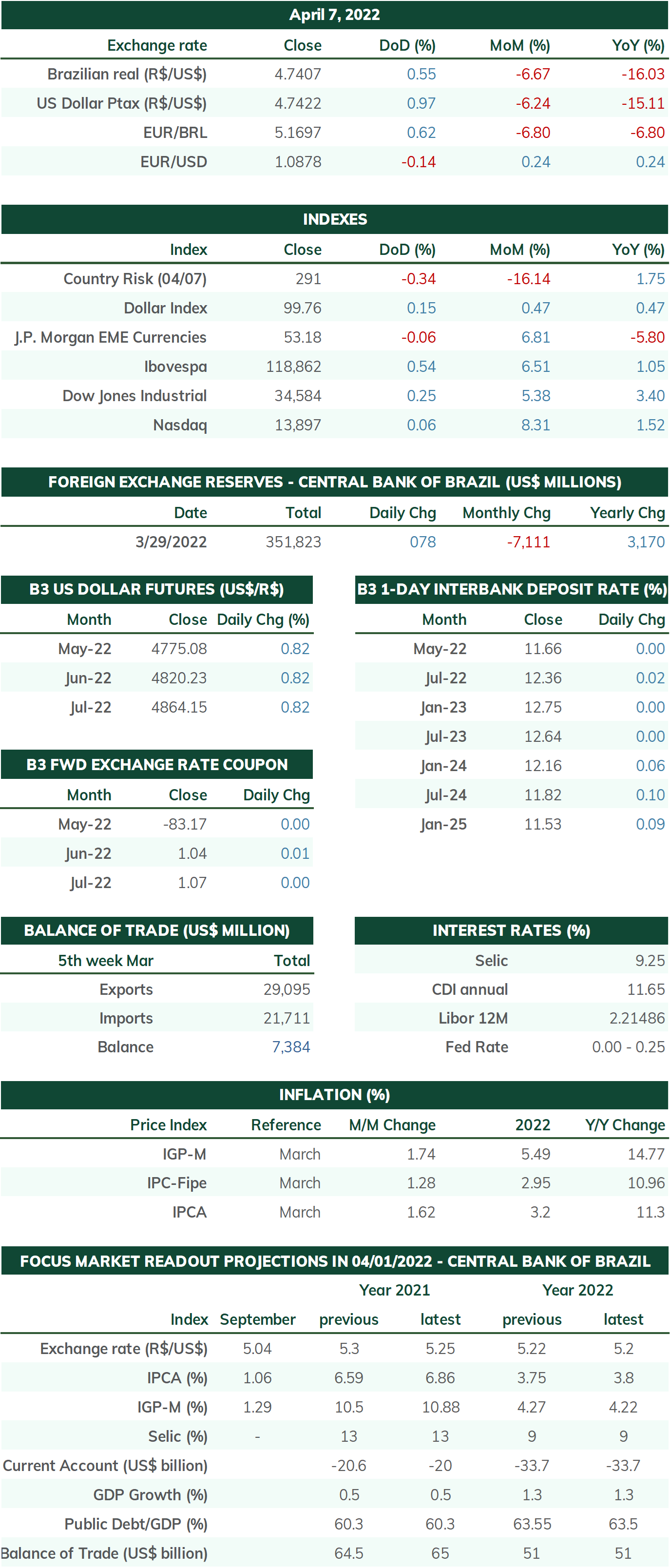

The factors driving the appreciation of the Brazilian currency in recent weeks have not fundamentally changed. The Brazilian interest rate differential from other nations is still quite high. Friday's release of the Higher than estimated National Broad Consumer Price Index (IPCA) for March – 1.62% versus 1.30% –reinforced that the acceleration of prices is still slow to cool down. The Central Bank of Brazil will probably still be quite forceful in its next interest rate readjustments. On Friday, the real interest rate – the difference between the nominal interest rate minus inflation – in Brazil is only lower than that of Russia, a country that faces difficulties in attracting foreign investors. This wide Brazilian interest differential helps attract investors looking for "carry trade" strategies – taking financing in a low-interest country to invest in a high-interest country.

In addition, the continuing war between Russia and Ukraine and the failure of another attempt to end the conflict through diplomatic means keep pressure on the prices of food, metal and energy commodities. The UN Food and Agriculture Organization (FAO) said that the Food Price Index, which tracks changes in international prices for a basket of agricultural commodities, rose to 159.3 points in March, up 12.6% from February. This is the highest level since the indicator was created in 1990 and the highest monthly rise since 2008. Since the end of January, the general upward trend in commodity prices has benefited the value of Brazilian exports and increased foreign exchange inflows through the trading account, thanks to the country's diversified commodity export capacity. In addition, there was a keen foreign appetite for Brazilian assets because of the low exposure, in relative terms, to the risks posed by the Russian-Ukrainian conflict and the low price of Brazilian assets in foreign currency terms. It will be extremely important to observe whether the movement of exchange rate flows next week will favor the factors contributing to the exchange rate's fall or its increase.

Finally, it is important to note that the strike by Central Bank employees significantly hinders the reading of the macroeconomic and exchange rate conjuncture in the country. Staging demonstrations and stoppages since February, these employees have interrupted their work after not receiving any proposals from the government for months. As a result, since the last week of March, the Central Bank has stopped publishing fiscal, monetary and credit statistics, foreign sector statistics, weekly data on foreign exchange flows, commodity indices and even the Focus bulletin. The vacuum of information worsens the ability to interpret economic movements in real-time.