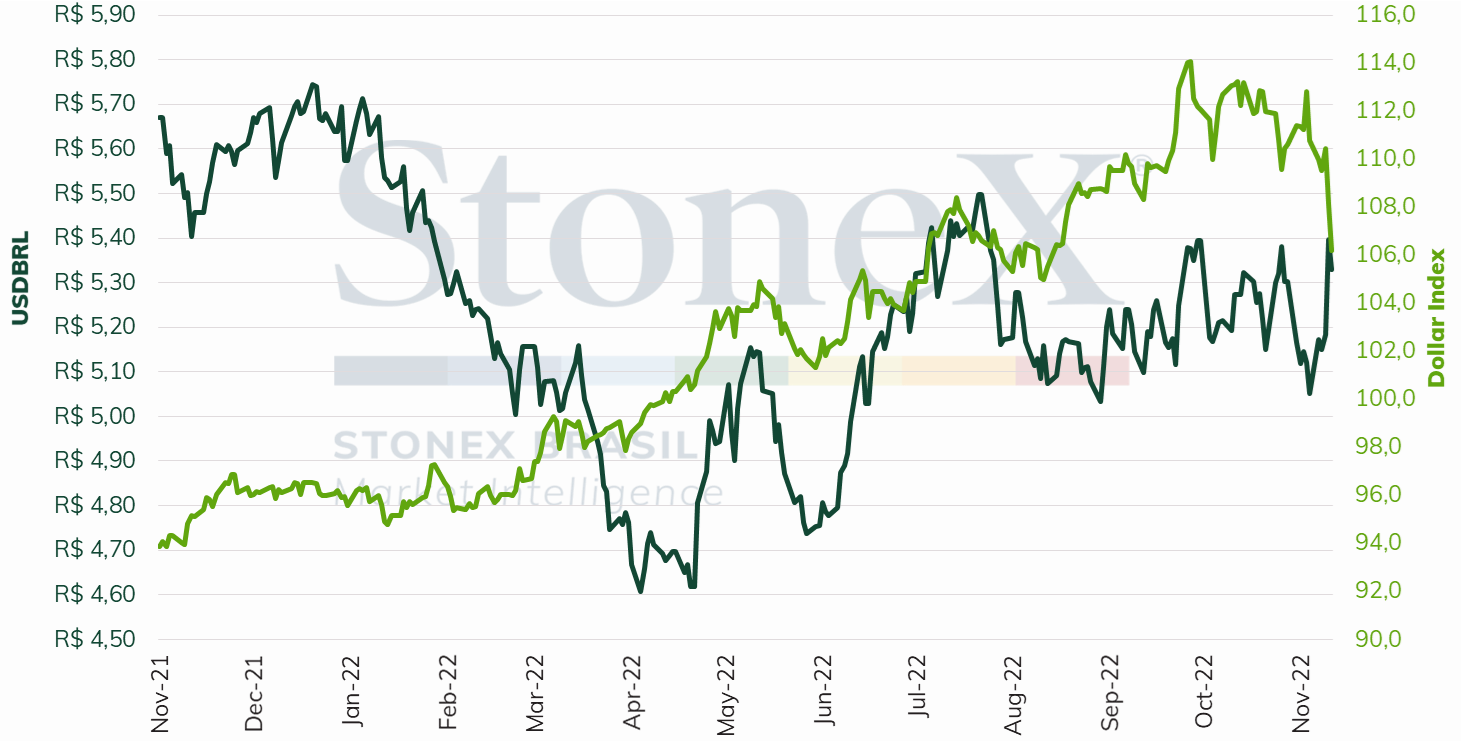

Foreign Scenario

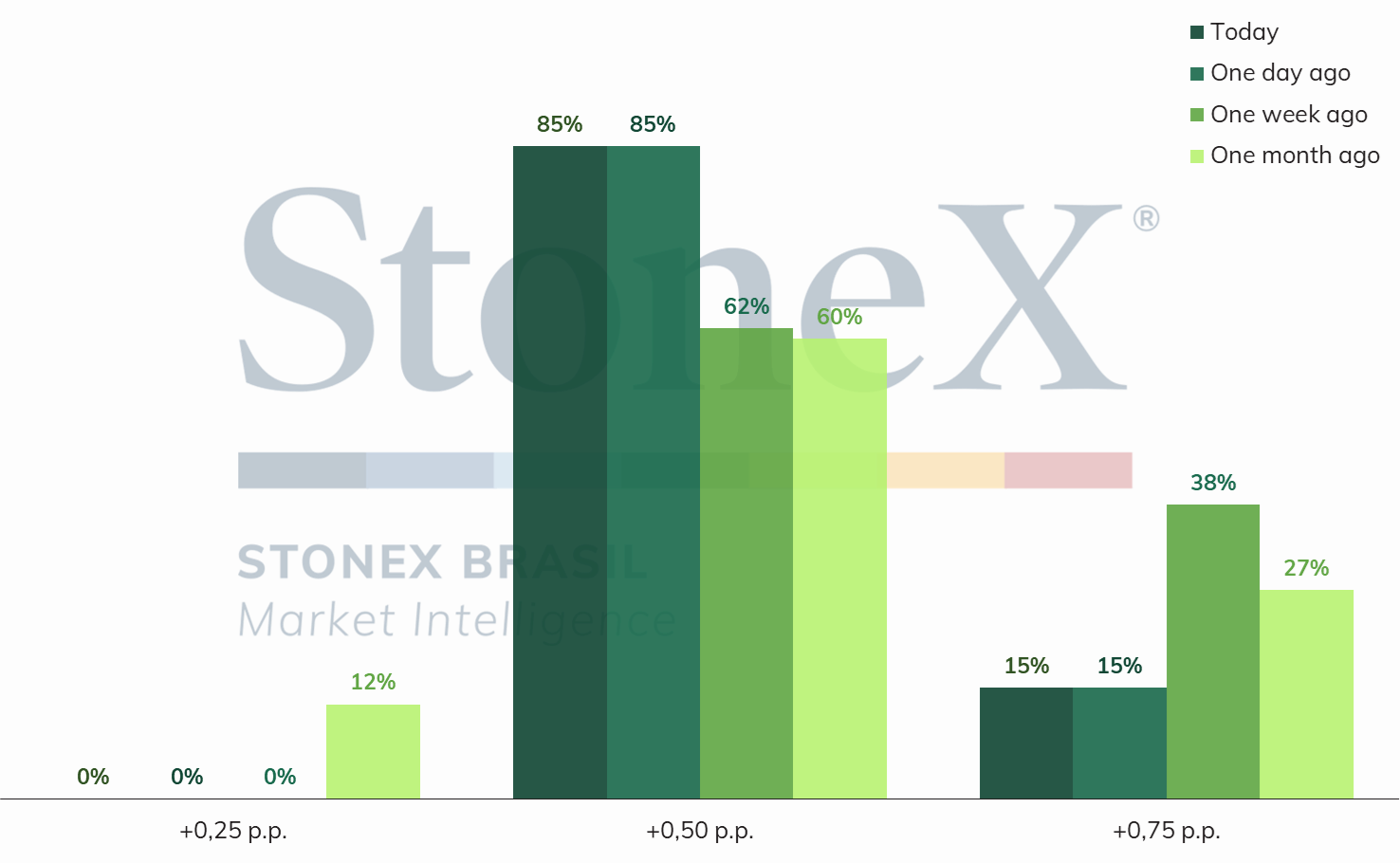

This week, attention should turn to the speech of the Federal Reserve’s (Fed) officials. The expectations of financial market agents changed profoundly last Thursday (10) after the Consumer Price Index (CPI) surprised and increased less than expected, reinforcing the interpretation that the Fed will moderate the pace of interest rate adjustments from this point on, boosting a wave of optimism and broad risk appetite. Furthermore, it consolidated expectations that the Fed will reduce the pace of its interest rate adjustments to 0.50 p.p. already in December's decision.

Bets for the Federal Reserve's interest rate decision on December 14

US interest rate history and higher probability bets on the futures market

Source: CME FedWatch Tool. Design: StoneX. Futures market interest rate probabilities as of November 04, 2022.

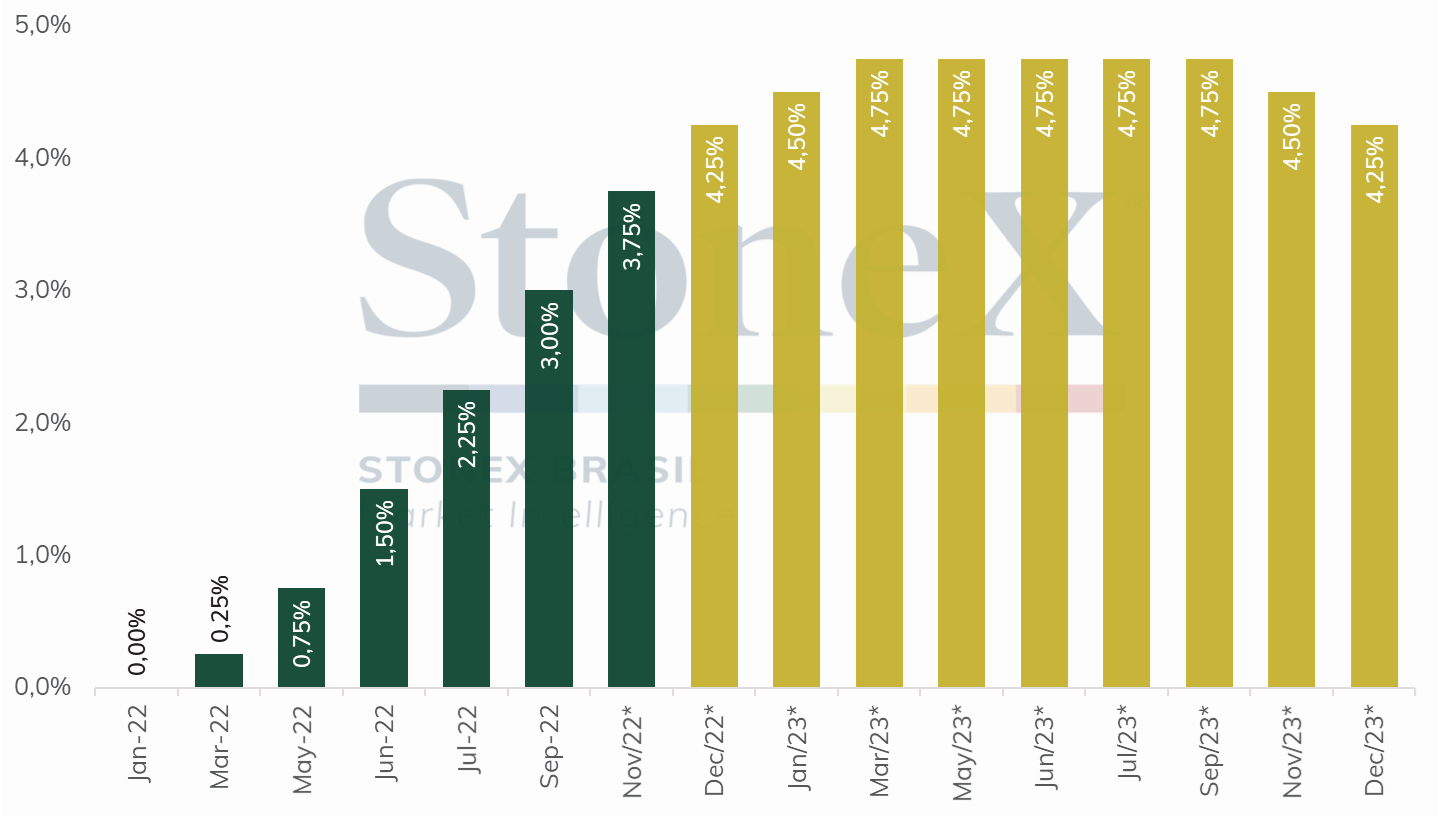

Thus, it will be important to see if the members of the monetary authority will adapt their communication, emphasizing the possibility of easing the pace of monetary tightening, or if they will persist in the original tone that it is important to bring inflation back to the target in a quick and timely manner. In addition, analysts will be looking for more details about the country's possible final level of interest rates, as well as estimates about the time frame for the central bank to start the tightening movement. The Fed Board of Governors member Christopher Waller, Fed Vice Chair Lael Brainard, Board of Governors member Lisa Cook, Board of Governors member Michelle Bowman, New York Fed President John Williams, Philadelphia Fed President Patrick Harker, Board of Governors member Michael Barr, St. Louis Fed President James Bullard, Cleveland Fed President Loretta Mester, and Minneapolis Fed President Neel Kashkowski are scheduled to speak this week.

Another highlight will be the release of data about economic activity in the United States, such as industrial production and retail sales for October. Analysts expect that such readings will reveal a continued slowdown in the activity level but will remain in positive territory. Additionally, the October Producer Price Index (PPI) will be released, which should receive a more refined analysis than usual after the wave of optimism caused by the below estimates CPI reading.

Over the weekend, the counts for the midterm elections in the United States last week should be finalized. At the time of writing, it was impossible to anticipate the division of the Senate, and there were indications that the Republicans (who oppose President Joe Biden) would win a slim majority in the House of Representatives of one or two seats. Nevertheless, the election turned out better than anticipated for the Democrats, who seemed destined to lose both legislative houses by a wide margin. However, such a performance should bring little consolation since, in practice, control of the House is enough for the Republicans to make Joe Biden's final two years in office more difficult and increase the chances that he will not be re-elected in 2024.

Finally, it is worth mentioning that the number of Covid-19 cases in China continues to increase, with a daily average of 3,731 cases, almost double the previous week (1,553), especially in Guangzhou, one of the country's largest regional economies. Still, the Politburo of the Chinese Communist Party surprised analysts on Friday by easing some of the restrictions concerning the control of the spread of the disease, such as reducing to two days the quarantine required of international travelers and people who have had contact with someone infected. In addition, authorities will no longer attempt to identify and require isolation of people with "secondary contact." The announcement was well received by investors and contributed to a greater appetite for Chinese assets, even if the authorities still caution that these decisions are incremental and a reopening is not yet in the plans.

Domestic Scenario

In Brazil, the focus should again be on the direction of fiscal policy under the next Lula administration. This week, discussions about the economic area and the 2023 Budget have alarmed investors, who reacted with strong mistrust and risk aversion. The first point of dissatisfaction is due to the resistance of the newly elected government to nominate the leadership cadres for the ministries of the economic area, prioritizing the definition of priority technical nuclei for the transition instead. Analysts point out that negotiating the 2023 Budget without having the people responsible for its execution can lead to omissions or errors in estimates.

The proposal for amendment to the Constitution (PEC) itself, baptized as the "Transition PEC," negotiated with Congress, is also the target of criticism. Initially, the proposal was to allow the government to exceed the constitutional spending cap in its first year to accommodate the promises made during the campaign to next year's Budget, such as the increase of the Bolsa Família income transfer program to BRL 600/month, the additional payment of BRL 150 per child, and the increase of the minimum wage adjustment to BRL 1320, whose total funding would be around BRL 80 billion. However, as negotiations evolved, the PEC began to incorporate the entire Bolsa Família program outside the spending cap, a figure estimated at BRL billion. This would free up around BRL 95 billion for additional expenses for the 2023 Budget, which would be earmarked for public investments in infrastructure and social welfare spending, such as the Popular Pharmacy or the housing program, Minha Casa Minha Vida. Finally, on Friday (11), the rapporteur of the Annual Budget Bill (PLOA) for 2023, Senator Marcelo Castro (MDB-PI), stated that the future president's intention was "to permanently exempt the entire Bolsa Familia from the spending cap. However, there would be disagreement whether this "exception" would last four years or would be permanent. The final text of the PEC is scheduled to be released next Wednesday (16).

The reaction was contradictory, faced with the devaluation of Brazilian assets and criticism from financial market agents. On the one hand, the president-elect criticized the fiscal balance rules in force in the country since they would limit, in his opinion, the capacity for public investment and social welfare spending. In his words, "why are people made to suffer for the sake of ensuring fiscal stability in this country?” On the other hand, people close to him tried to be more moderate. Senator-elect Wellington Dias (PT-PI), responsible for negotiating the Budget with the members of Congress, stated that "we are doing this [PEC] very responsibly, with control of the public accounts. It is only what is strictly necessary". At the same time, Congressman Marcelo Ramos (PSD-AM) declared that "Lula is no fool to go on a fiscal adventure." Congressman José Guimarães (PT-CE) argued that "everyone knows that Lula has fiscal responsibility."

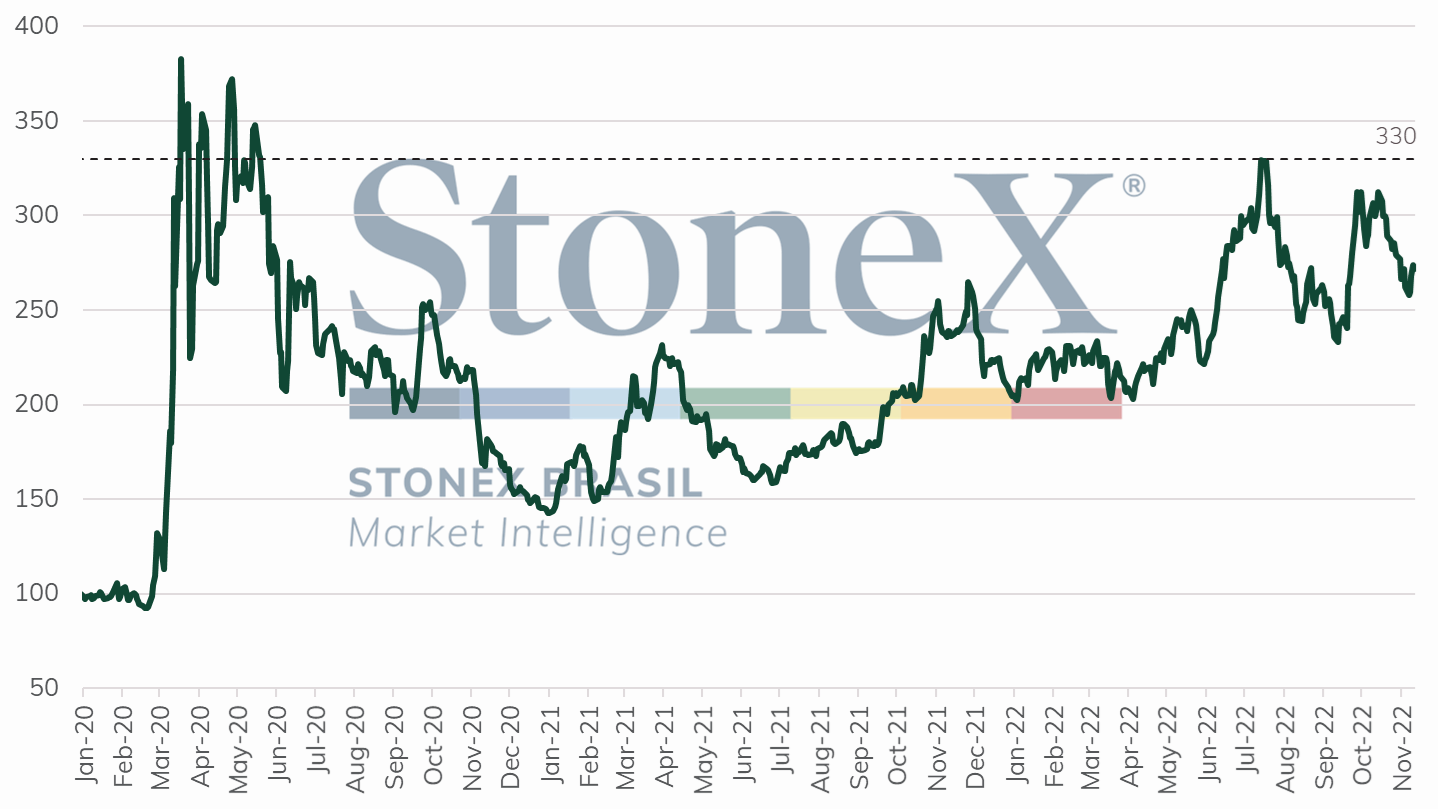

Some political analysts say that, with the PEC - and its resources - Lula would be seeking to establish a base of parliamentary support in Congress and ensure the viability of his legislative agenda from the beginning of his term and that, not necessarily, his government will be marked by lack of control of public accounts. Even if one admits this hypothesis, the fact is that the initial reception by the financial market was negative, and the communication after the fact did not sound convincing enough to calm things down. Consequently, there was a slight increase in the perception of risk of Brazilian assets, according to the spread of five-year CDS contracts, and a considerable increase in interest rates on the country's public debt bonds.

Spread of the Brazilian 5-year Credit Default Swap (CDS) contracts (basis points)

Source: Bloomberg. Design: StoneX.

NTN-B purchase rate due on 05/15/2045 (% p.a.)

Source: Tesouro Direto. Design: StoneX.

Besides the political scenario and the week shortened by a holiday in Brazil, the Central Bank's Economic Activity Index - IBC-Br for September will be released this Monday (14) and whose average estimates point to an increase of 0.20% compared to August and 4.86% compared to the same month last year.