The USDA's supply and demand report brought the South American grain crop adjustments. For wheat, the highlight was the increase in imports from some countries. On the other hand, there was a decrease in the expectation of exports from Indonesia in the case of vegetable oils. As for cotton, the report continued to indicate increased consumption.

Soybean

For soybean, there were great expectations for the updated figures for South America, given the scenario of crop losses and with private consultants making significant cuts.

The USDA cut Brazil's 2021/22 crop to 134 million tonnes and Argentina's to 45 million tonnes. Even so, compared to the figures that have been released, these cuts were moderate. StoneX, for example, estimates Brazil’s crop at 126.5 million tonnes.

Conab released its monthly survey one day after the USDA, reducing the Brazilian crop from 140.5 to 125.5 million tonnes.

Even if the USDA cuts are less than what has been reported by other institutions, these losses will result in a rearrangement of soybean flows worldwide. For example, the Department cut Brazilian exports for the 2021/22 cycle from 94 million to 90.5 million tonnes. However, compared to StoneX, the USDA is still betting on very high exports. StoneX estimates 80 million tonnes but remembering that the period of the crop year is different.

Amid this scenario, the USDA maintained the estimate of US exports for the 2021/22 crop at 55.8 million tonnes, even with sales and shipments much lower than last year. However, with the lower availability of soybeans in Brazil, US exports should get a boost in unusual periods. It is also noteworthy that the US crushing was raised to 60.3 million tonnes, given the heated processing of soybeans in the country and the possibility of exporting more meal, amid losses in Argentina.

Another important point in the report was the cut in Chinese imports to 97 million tonnes, highlighting that the country's imports are weaker in the 2021/22 cycle.

Considering these changes, the gap between world consumption and production grew, with global stocks falling to 92.8 million tonnes.

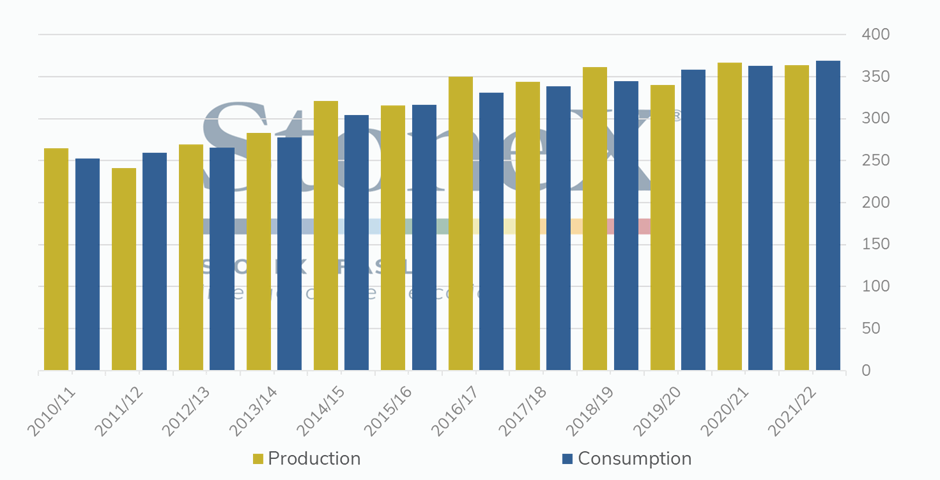

World soybean production and consumption (MMT)

Source: USDA. Design: StoneX.

Corn

Regarding corn, the Department did not bring any big surprises in its supply and demand figures, and there were no changes in the US 2021/22 corn crop balance.

For South America, which was quite expected due to the recent climatic adversities experienced by the region, the revisions were modest. The USDA reduced its production estimate for Brazil's 2021/22 crop from 115 million to 114 million tonnes, slightly above the average of market estimates, at 113.6 million tonnes.

Argentina's crop was kept at 54 million tonnes, while the average market estimates pointed to 52.2 million tonnes.

The figures for the South American crop in the next USDA S&D report will still be very important for the market since the Department may have adopted a more conservative position and will only promote more significant changes in the next reports.

By way of comparison, the Buenos Aires Grains Exchange reduced its estimate for the 2021/22 corn crop to 51 million tonnes, 6 million tonnes less than previously estimated.

The world balance showed a slight decrease in production and consumption, to 1,205.4 million and 1,195.17 million tonnes. As a result, 2021/22 ending stocks fell to 302.2 million tonnes, almost 2 million tonnes above-average market estimates.

Besides the South American crop, another point of attention for the next report will be the Ukrainian crop. Last week, the White House warned that a Russian invasion could be initiated. However, in this last report, the USDA did not promote any changes in the country's 2021/22 balance, and its export is still estimated at 33.5 million tonnes. So far, the outflow channels in the Black Sea region have not been affected. Still, the beginning of a military operation could harm the logistics of the product and impact Ukrainian shipments.

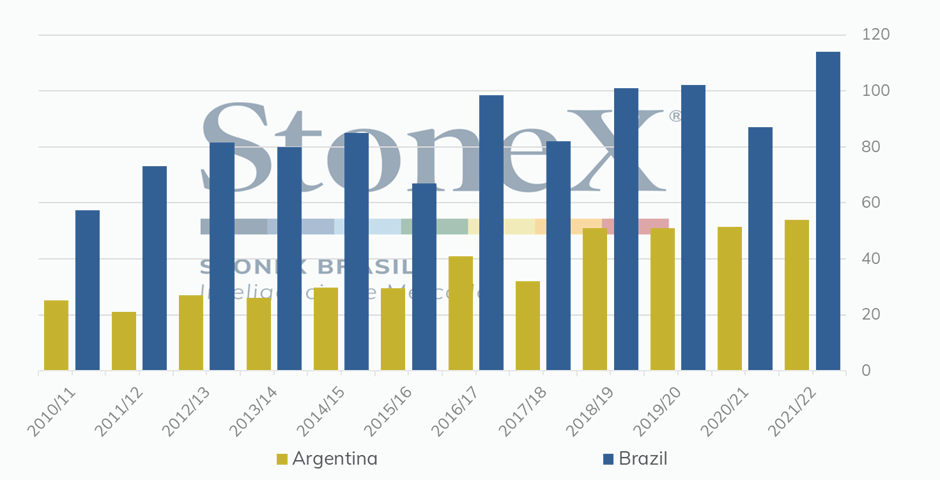

Soybean production trend (MMT)

Source: USDA. Design: StoneX.

Wheat

For wheat, in the US domestic scenario, the USDA maintained its supply-side estimates (carryin, production and imports) and cut domestic consumption and export estimates, which led to a positive adjustment on its ending stocks estimate.

According to the data released last Wednesday (9), the US is expected to produce 44.8 million tonnes of wheat from a harvested area of 15.05 million hectares, which would result in an average yield of 2,979.15 kg/ha - of this total produced, 45.5% is estimated to be Hard Red Winter (HRW); 21.9% Soft Red Winter (SRW); 18.0% Hard Red Spring (HRS); 12.2% White; and 2.2% Durum.

The main revisions were made on the demand side, with a cut of 130,000 tonnes on total domestic consumption (30.84 million) and 410,000 tonnes on exports (22.04 million). However, it is worth noting that the pace of US exports has been below that recorded last year, accumulating an annual deficit of more than 3.0 million tonnes as of the week ended February 3.

On the international front, as commented in our weekly wheat summary, the February/22 update brought some revisions to global estimates, with emphasis on the cut of 2.18 million tonnes on world production, which is estimated at 776.4 million, and also the reduction of 1.72 million on ending stocks, estimated at 278.2 million. As the USDA has not reviewed the production of major exporting countries, the new number should little affect the exportable surplus and the level of grain supply in the international market. The cut on world production stems from reducing small crop numbers, such as those of the UK, Brazil, Kazakhstan, Syria and Iraq.

About the international trade, the USDA raised its estimates for imports from some countries, such as the UK (+300,000 tonnes) and Brazil and Kazakhstan (+200,000 tonnes each). On the export side, the main revisions were to the US (-400,000), Ukraine (-200,000), Kazakhstan (+100,000), Brazil and Canada (+200,000 each), and Argentina (+500,000). Finally, the most significant corrections occurred in the estimates for ending stocks, with a highlight to the increases in the US (+540,000) and Ukraine (+400,000), and reductions in Canada (2.0 million) and Argentina (630,000).

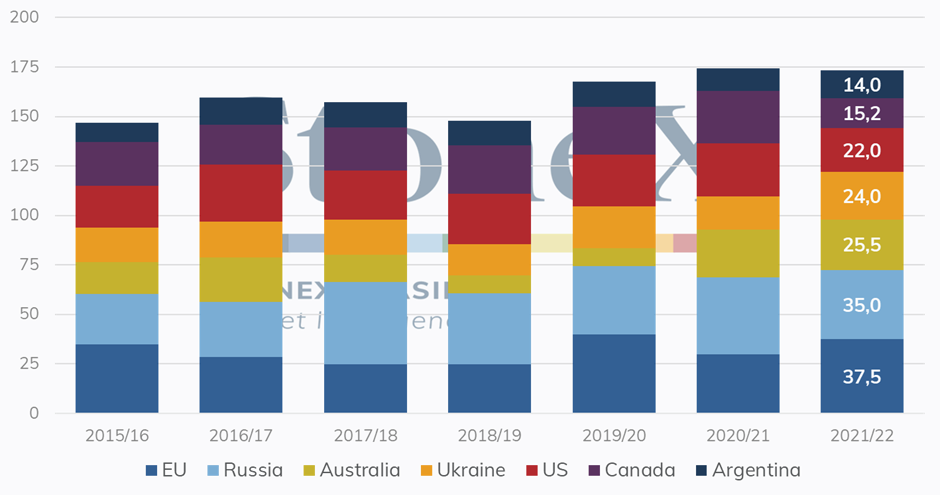

Main wheat exporting countries (MMT)

Source: USDA. Design: StoneX.

The WASDE report had neutral repercussions for cotton, although it supported the loss of strength in the short-term upward trend in future prices. The USDA did not promote major changes in the supply and demand balance and, where it did change, it was in variables already expected by the agents.

First of all, Indian production was cut by 110,000 tonnes in the 2021/22 cycle, reaching 5.88 million tonnes. In May 2021, when the USDA brought the first figures of the current crop, it had expected Indian production at 6.31 million tonnes. Over time, the country suffered from irregular rainfall, and its crop faced natural pests - the main drivers for this 7.3% decrease in the size of the Indian crop by the months. As a result, the domestic market has faced tight availability, and textile industries are having difficulties receiving cotton from processors. The slow pace of cotton deliveries to mills can come in two ways: producers are holding onto their bales for processing in expectation of even higher prices, or the production itself is lower than expected. The first case is limited since domestic physical cotton prices in India are at nominal record highs, and it is more likely that, at the very least, the situation is a combination of the two scenarios.

Second, the USDA also cut US exports for the second month in a row, now at 3.21 million tonnes (60 thousand tonnes lower than the January forecast). As of February 3, the country exported 998 thousand tonnes of cotton, increasing the pace of weekly shipments, it is worth noting. With six months to go until the end of the 2021/22 crop, this number is unlikely to be met, even though it is more consistent with the current scenario due to various logistics problems around the world. However, even if this drop in exports indicates a relief in the final stocks in the United States, this volume not exported in 2021/22 is not "free," that is, according to the sales at a faster pace of the North American cotton, these stocks are still committed for shipment sometime after July 2022, thus being not so bearish news as it seems.

Finally, the highlight remains the tight number in the cotton S&D balance. Consumption projections continue to rise to record highs globally, particularly driven by recovering economies. The declining stocks point to this inability of production to keep up with demand. As shown by the evolution of USDA estimates, the physical market has been supporting the escalations in New York, in which future prices continue at 11-year highs.

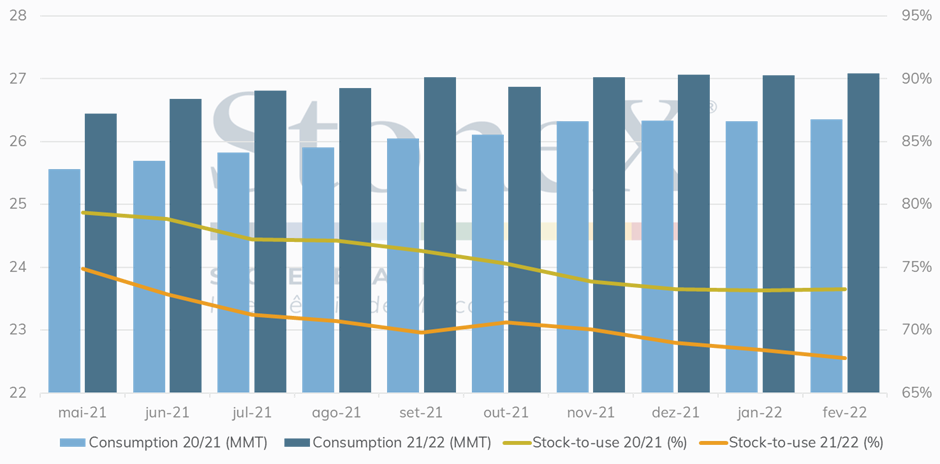

Global supply and demand estimates trend (MMT)

Source: USDA. Design: StoneX.

For the vegetable oil complex, the main highlight of the February WASDE was the 5.4% reduction in the expectation of palm oil exports by Indonesia for the 2021/22 season compared to the January figure, totaling 28 million tons. The market already expected a decrease in exports in the world's largest palm oil producer since January. The local government established that exporting companies should direct 20% of the volume previously reserved for export to the domestic market. Furthermore, when palm oil prices are advancing over the historical high, the government has defined a ceiling for the prices, which will be subsidized. With this, WASDE/USDA also raised expectations for domestic consumption of palm oil in Indonesia to 15.98 million tonnes, high by 3.3%.

It is also worth noting that WASDE did not change the export projections for Malaysia, a direct substitute for Indonesian exports.

The numbers for soybean oil production in 2021/22 followed the changes observed for soybeans, with a reduction in crushing and production of soybean oil, in Brazil and Argentina by -0.6% and -3.2%, compared to January. As a result, Brazilian soybean oil exports were reduced by 1.6%, compared to what was expected in January, but continue to show record volumes. The escalating concerns about the lack of rainfall in the southern part of the continent are the main limiting factor for the South American supply of soybean oil.

It is also worth mentioning that despite the increasing tensions between Russia and Ukraine in recent weeks, the WASDE/USDA has not changed the expectations for sunflower oil production and stocks in these countries, which are the two main players in the market.