Precious Metals Talking points 060826: StoneX weekly gold, silver round-up; gold MM shorts at lowest since 28th January

Politics, economic, geopolitics and investor sentiment

Rhona O'Connell

- Precious Metals

By: Rhona O'Connell, Head of Market Analysis

We write a brief monthly analysis of the LBMA's daily trading volumes in the spot, forward, lease and options markets for gold, silver, platinum and palladium; the figures, when set against market background and economic and financial forces, can be very revealing.

LBMA Precious Metals market volumes, December and year 2025, and their significance

Rhona O’Connell, StoneX Financial Ltd; 22nd January 2026

Any views expressed here are of the writer and do not reflect a house view from NASDAQ.

A very happy, peaceful and prosperous New Year to our readers.

To make a change as we enter the New Year, this edition will be slightly different from the norm, with these initial charts looking back over the year before we move into text. Every picture tells a story!

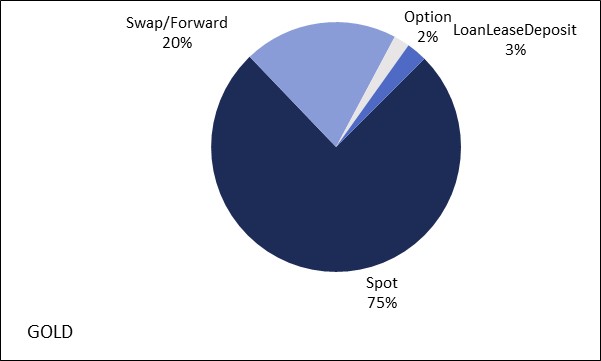

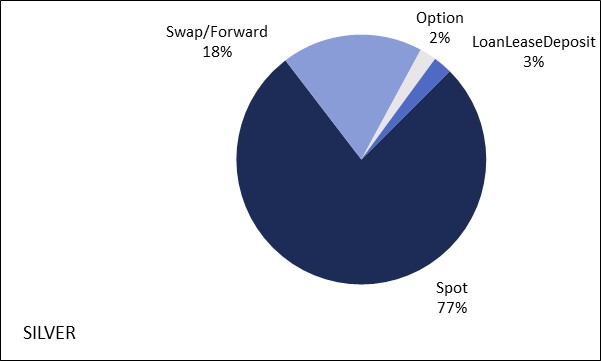

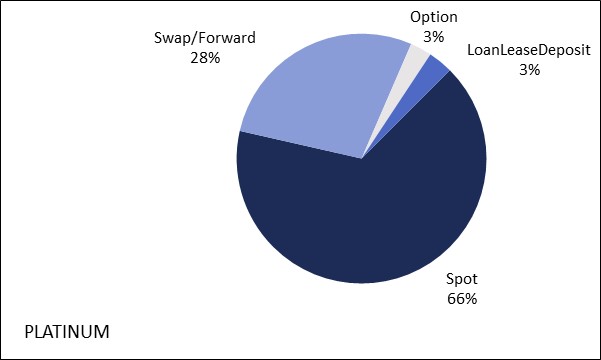

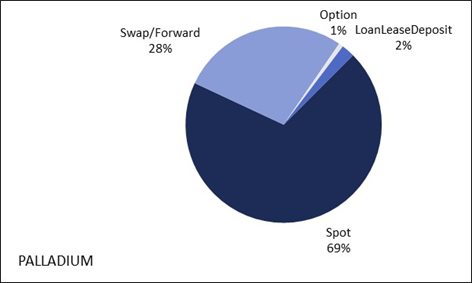

2025 full-year sectoral market shares

GOLD

SILVER

PLATINUM

PALLADIUM

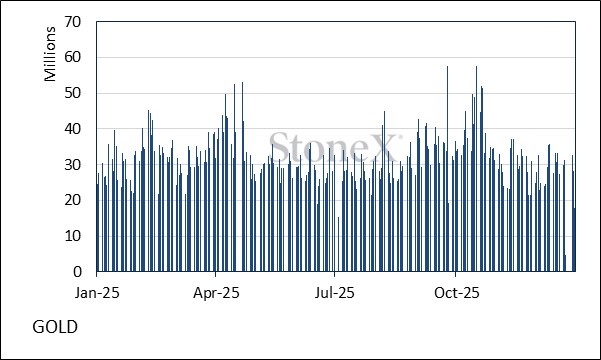

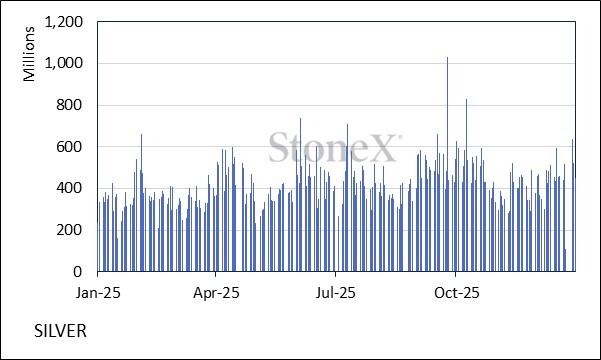

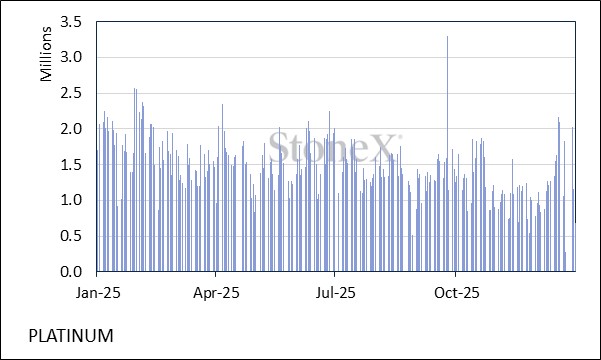

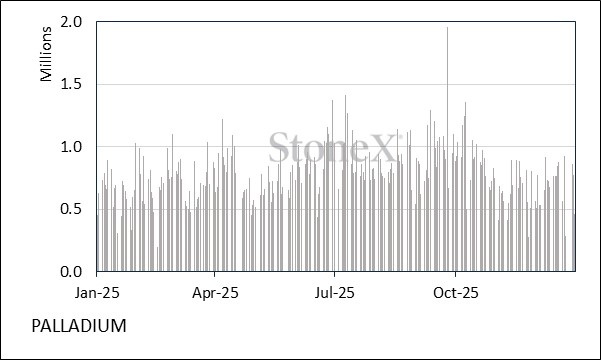

2025 spot volumes, ounces

GOLD

SILVER

PLATINUM

PALLADIUM

Source: for all eight charts above; LBMA, StoneX

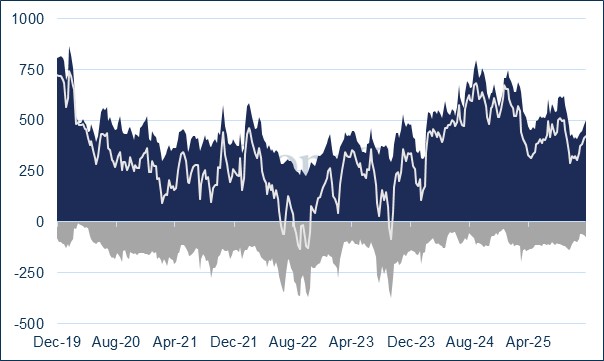

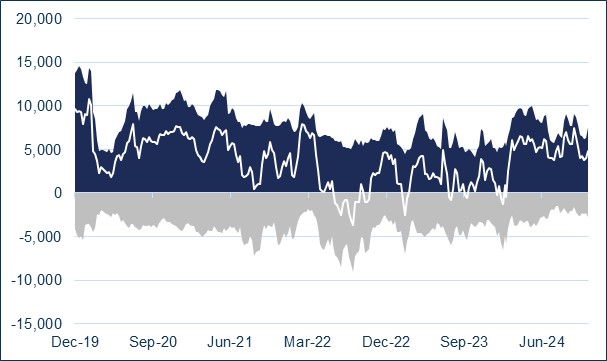

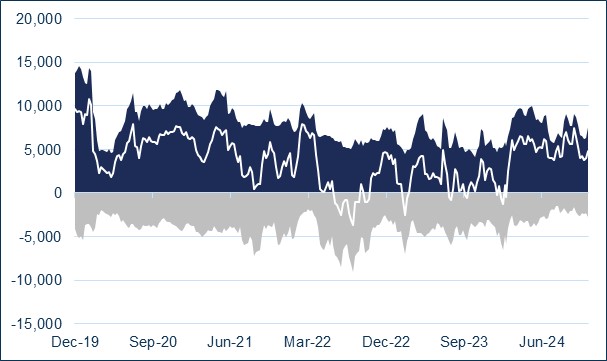

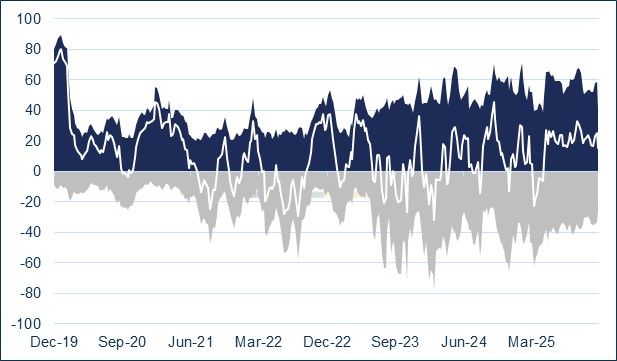

COMEX, NYMEX, positioning

GOLD

SILVER

PLATINUM

PALLADIUM

Source: CFTC, StoneX

December in brief:

Daily December average compared with daily average for the previous twelve months.

Source: LBMA

Source: LBMA

Welcome to our monthly round-up of the LBMA OTC trading volumes in gold, silver, platinum and palladium, as recorded on a daily basis by the Association. These are split into spot, swap/forward, options and LoanLeaseDeposit (LLD) and give a flavour of the markets’ activity and how they were influenced by external forces and news items.

All references to COMEX or NYMEX positioning refer to Managed Money, not commercial positions.

General introduction:

CME raised margins on all four precious metals towards month-end, contributing to sharp price corrections in all four, on 29th December.

Margin changes can be found here

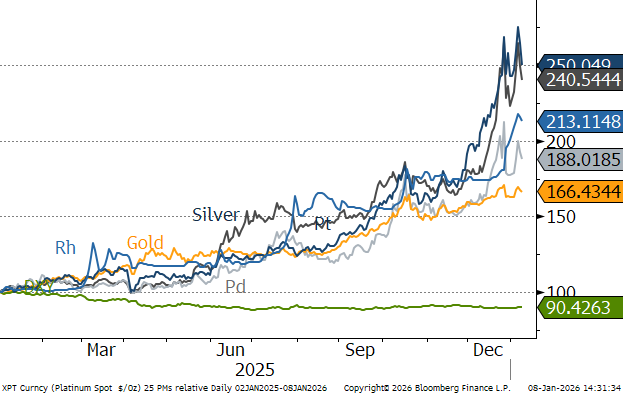

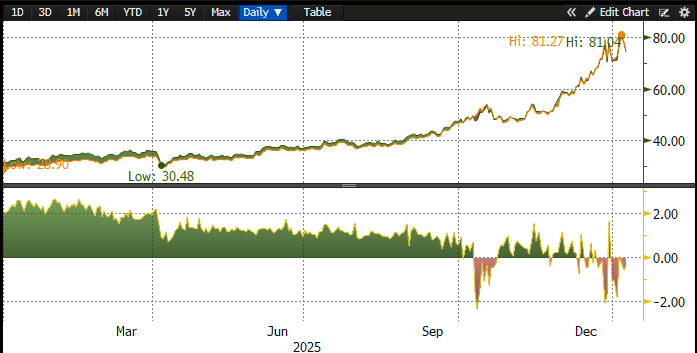

December: silver and platinum in the spotlight where spot and option volumes are concerned. Both metals remained tight with EFPs flying in and out as the US tariff issue continued to inform sentiment. By this stage silver was hurtling higher, trading off its own momentum, to reach a high of $84.0 on the 29th before it took a breather, prompted in part, by the margin changes.

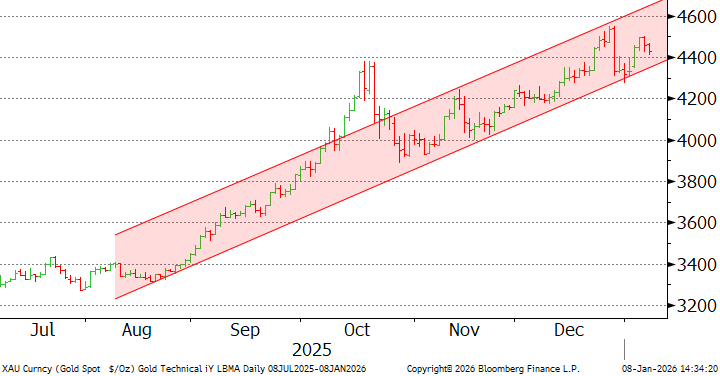

Gold was still going strong, peaking at $4,550 (intraday) on Boxing Day, when London markets were closed but New York was open, before correcting towards $4,270 and settling into a narrow range as we moved into the New Year. Sentiment remained buoyant, although the US’ strike on Venezuelan soil only generated a rally of only $100 (just 2.5%), which was pretty rapidly unwound, reflecting the fact that there is a substantial geopolitical premium already priced in.

Platinum also reached the year’s high on 29th at $2,491 and this metal, too, was speeding higher in a self-fulfilling move as conditions remained tight and both platinum and palladium enjoyed the first month of futures trading on the Guangzhou futures market.

Palladium was pulled up in platinum’s wake, although it is worth noting that palladium ETFs expanded by a full 50% over 2025 as a whole. Palladium also peaked for the year on 29th December, at $1,982 before three days of falls, sliding to $1,490, a fall of 24%, before rebounding towards $1,800.

The long-term outlook remains bleak, however and while platinum’s prosects are brighter, both metals started 2026 overbought, and a correction is likely for both of them.

Gold, silver, platinum and palladium, 2025

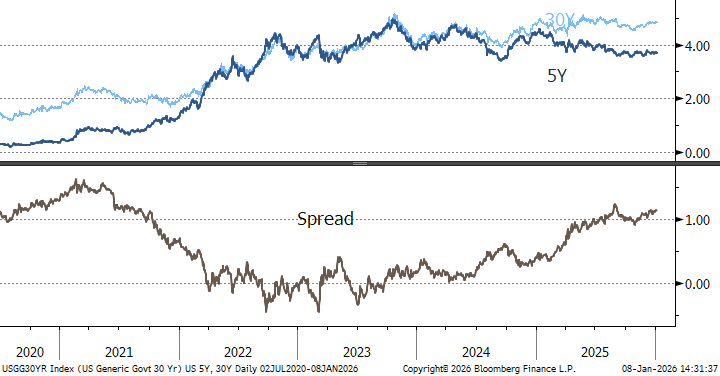

The US yield 5Y-30Y curve; interest re-appears in the longer tenors.

Source: Bloomberg, StoneX

GOLD

Turnver, M ounces

Source: NASDAQ, LBMA

Spot gold in nominal and real terms (deflator; US CPI)

Source: Bloomberg, StoneX

Gold, 2025

Source: Bloomberg, StoneX

SILVER

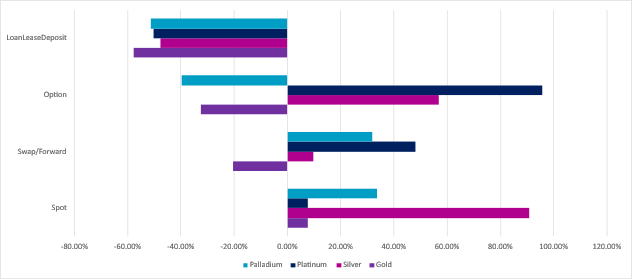

As the market became more frenetic spot volumes almost doubled against the previous 12-month average, with the high volumes concentrated in the final few days. Options were up 57% and swap/forwards, 10%. The LLD sector was off by 48%, suggesting that no-one wanted to sell forward into a whirlwind, for fear of opportunity cost. When this goes into reverse we may well see LLD volumes bounce.

Silver spot and active contract

Source: Bloomberg

Meanwhile retail demand for coins and bars has continued to balloon in Europe and parts of Asai. New York remains at a discount to London.

Turnover

Source: NASDAQ

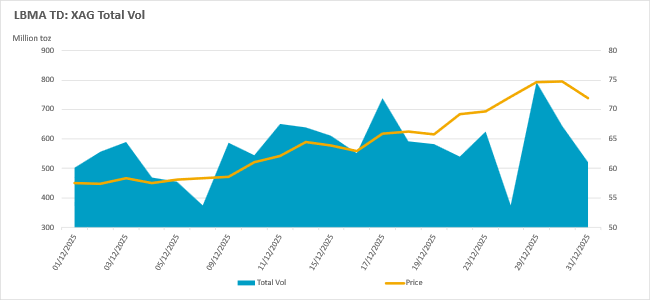

There were four standout days in the spot market. The first two were the 12th and the 17th when, just like gold, silver was pushing into new levels. Unlike gold, however, the 12th was a day of price retreat from just under $65, to $62.and this coincided with heavy options trading so it is possible that put options were in play, likely at the $65 level.

On the 17th prices were forging higher again, pushing through $65 so there may have been some short covering here as silver moved up to $67, providing a springboard for the burst higher. That saw five consecutive bullish days, from $64 to $79, including the heavy day on the $23rd when $70 was breached, culminating in a test of on the 29th, which was extremely heavy volume under what was almost certainly profit taking.

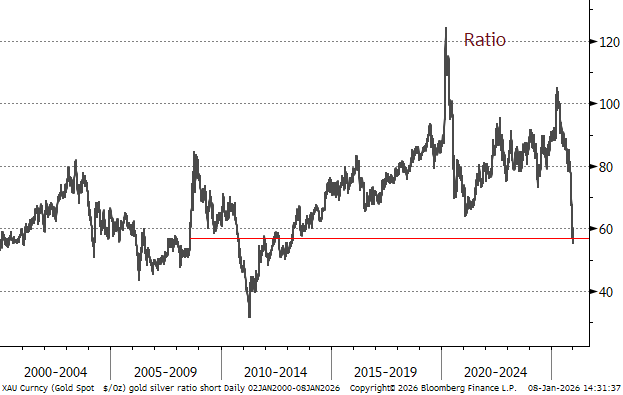

Gold:silver ratio

Source: Bloomberg, StoneX

PLATINUM and PALLADIUM

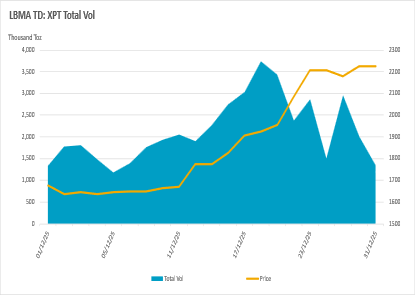

While spot platinum and LLD volumes were down by 18% and 31% respectively, there was massive activity in the options sector in December, up 85% against the previous 12-month average, with the heaviest days clustered in the middle of the month. This coincided with the strong run in prices, from .$1,800 to $2,300, a gain of 28% the strongest days in swap/forwards, more or less coincided with these days, as they did for spot (albeit that volumes were lower than the previous average).

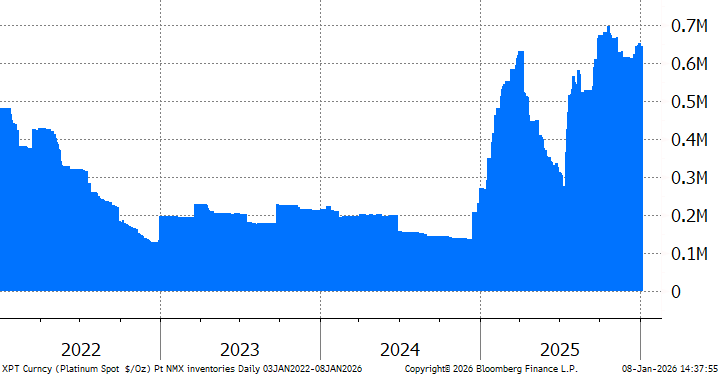

This was on the back of continued tight supply with continued additions to ETF holdings (up 6.4t over the month) and NYMEX inventories rising by 1.2t. That took 7.6t out of the free float in the market and lease rates rose again accordingly.

At end-month the Chicago Mercantile Exchange (CME) margin changes led to a sharp drop in price from the month’s high of $2,491 to $2,075. Volumes were heavy in spot loco London. On the other side of the world the Guangzhou Futures exchange imposed single-day open interest limits on both platinum and palladium as of 23rd December, amid strong demand.

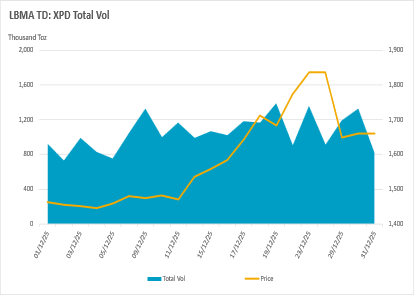

Palladium volumes were down everywhere except swap/forwards, which were up 11%, with quiet conditions early on, but picking up smartly in the final week, suggesting forward selling into the top of the very rapid surge that took spot from $1,500 to $1,962 in the space of ten days, boosted by platinum strength and underpinned by, much like platinum, sustained ETF investment with only three days of redemptions over the month. Just prior to the forwards perking up, spot was comparatively busy as stakeholders were drawn into the rally, feeding the fire. Options were moribund, while the only real action in the LLD was in the first two days of December, temporarily capping the rally in the final week of November, which saw spot briefly clear $1,500 which may have been a psychological target.

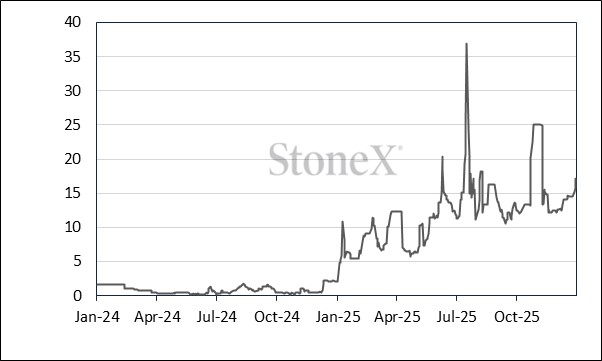

Platinum implied one-month lease rate, January 2024 -to-date.

Source: Bloomberg, StoneX

Turnover

Source: NASDAQ

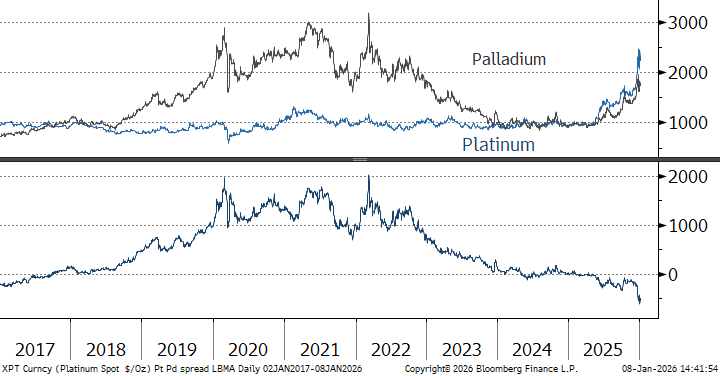

Platinum, palladium and the ratio, January 2022 to date

Source: Bloomberg, StoneX

Platinum; NYMEX inventories, ounces

Source: Bloomberg, StoneX

Spot platinum, palladium and the spread, January 2020 to date

Source: Bloomberg, StoneX

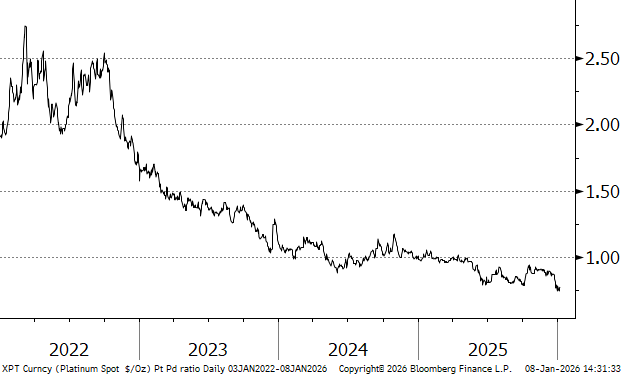

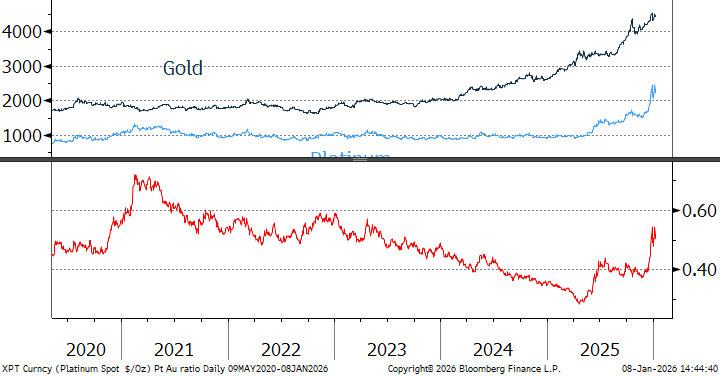

Platinum, gold and the ratio

Source: Bloomberg, StoneX

--------------------------------------------------------

This material should be construed as market commentary and represents the opinions and viewpoints of the author, and does not reflect tailored advice associated with any specific account.

The views are current only through the date stated and are subject to change at any time based upon market or other conditions, and StoneX Group Inc. (“SGI”) disclaims any responsibility to update such views. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources. Past performance does not guarantee future results.

The StoneX Group Inc. group of companies provides financial services worldwide through its subsidiaries, including physical commodities, securities, exchange-traded and over-the-counter derivatives, risk management, global payments and foreign exchange products in accordance with applicable law in the jurisdictions where services are provided.

References to certain OTC products or swaps are made on behalf of StoneX Markets, LLC (SXM), a member of the National Futures Association (NFA) and provisionally registered with the U.S. Commodity Futures Trading Commission (CFTC) as a swap dealer. SXM’s products are designed only for individuals or firms who qualify under CFTC rules as an ‘Eligible Contract Participant’ and who have been accepted as customers of SXM.

StoneX Financial Inc. (SFI) is a member of FINRA/NFA/SIPC and registered with the MSRB. SFI is registered with the U.S. Securities and Exchange Commission (SEC) as a Broker-Dealer and with the CFTC as a Futures Commission Merchant and Commodity Trading Advisor. StoneX Financial (Canada) Inc. (SFCI) is registered in Canada and is a member of CIRO and CIPF. References to certain securities trading are made on behalf of the BD Division of SFI and are intended only for an audience of institutional clients as defined by FINRA Rule 4512(c). References to certain exchange-traded futures and options are made on behalf of the FCM Division of SFI. Wealth Management is offered through SA Stone Wealth Management Inc., member FINRA/SIPC, and SA Stone Investment Advisors Inc., an SEC-registered investment advisor, both wholly owned subsidiaries of SGI.

R.J. O’Brien & Associates, LLC (RJO) is registered with the CFTC as a Futures Commission Merchant and is a member of NFA.

StoneX Financial Ltd (SFL) is registered in England and Wales, company no. 5616586. SFL is authorized and regulated by the Financial Conduct Authority (FCA) (registration number FRN:446717) to provide services to professional and eligible customers including: arrangement, execution and, where required, clearing derivative transactions in exchange traded futures and options. SFL is also authorized to engage in the arrangement and execution of transactions in certain OTC products, certain securities trading, precious metals trading and payment services to eligible customers. SFL is authorized and regulated by the FCA under the Payment Services Regulations 2017 for the provision of payment services. SFL is a category 1 ring-dealing member of the London Metal Exchange. In addition SFL also engages in other physically delivered commodities business and other general business activities which are unregulated and not required to be authorized by the FCA.

This communication is issued in the European Economic Area by StoneX Financial Europe GmbH (SFEG). StoneX is the trade name used by STONEX GROUP INC. and all its associated entities and subsidiaries. StoneX Financial Europe GmbH (“SFEG”) is a securities trading firm registered in Germany under Company No. HRB 80844.

StoneX Financial Pte Ltd (Co. Reg. No 201130598R) (“SFP”) is regulated by the Monetary Authority of Singapore and is a Capital Markets Service Licence holder (for dealing in capital market products), an Exempt Financial Adviser (for advising on investment products and issuing or promulgating analyses/ reports on investment products) and a Major Payment Institution (for domestic and cross-border money transfer services).

SFP may distribute analysis/report produced by its respective foreign affiliates within the StoneX Group of companies pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations Recipients should contact SFP at (65) 6309 1000 for any matters arising from, or in connection with, this webinar.

StoneX APAC Pte. Ltd. (“SAP”) (Co. Reg. No 200616676W) is regulated as a Dealer (PS20190001002) under the Precious Stones and Precious Metals (Prevention of Money Laundering and Terrorism Financing) Act 2019 for purposes of anti-money laundering and countering the financing of terrorism.

StoneX Financial (HK) Limited (CE No.: BCQ152) (“SHK”) is regulated by the Hong Kong Securities and Futures Commission for Dealing in Securities and Dealing in Futures Contracts.

StoneX Financial Pty Ltd (ACN 141 774 727) holds an Australian Financial Service License (AFSL: 345646) for Dealing in Securities, Exchange-Traded Derivatives Contracts, OTC Derivatives Contracts and Foreign Exchange Contracts, and is regulated by the Australian Securities and Investments Commission.

StoneX Securities Co., Ltd. (“SSJ”) (Co. Reg. No 010401047199) is regulated by the Japanese Financial Services Agency as a Type-I Financial Instruments Business Operator (Kanto Local Finance Bureau (FIBO)No.291’), is a member of the Financial Futures Association of Japan for dealing and broking FX and FX Option transactions, and is a member of the Japan Securities Dealers Association for dealing and broking stock indices and option transactions.

Trading swaps and over-the-counter derivatives, exchange-traded derivatives and options and securities involves substantial risk and is not suitable for all investors. Past performance of any futures or option is not indicative of future success. Indicators are not a trading system and are not published as a specific trade recommendation. The information herein is not a recommendation to trade nor investment research or an offer to buy or sell any derivative or security. It does not take into account your particular investment objectives, financial situation or needs and does not create a binding obligation on any of the StoneX group of companies to enter into any transaction with you. You are advised to perform an independent investigation of any transaction to determine whether any transaction is suitable for you. No part of this material may be copied, photocopied or duplicated in any form by any means or redistributed without the prior written consent of StoneX Group Inc.

The report/analysis herein is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

© 2026 StoneX Group Inc. All Rights Reserved.

Our subscribers have access to comprehensive market analysis from StoneX spanning commodities, equities, currencies and more.

Politics, economic, geopolitics and investor sentiment

Silver is showing greater technical weakness than gold, raising questions about whether the broader precious metals complex is entering a more challenging phase. While long-term bullish arguments remain intact, deteriorating momentum and key support tests suggest silver may face deeper downside risks before a sustainable recovery emerges.

Today's commodity market news and analysis/advisory guidance.

Our market expertise, advanced platforms, global reach, culture of full transparency and commitment to our clients’ success all set us apart in the financial marketplace.

Reach

With access to 40+ derivatives exchanges, 180+ foreign exchange markets, nearly every global securities marketplace and numerous bilateral liquidity venues, StoneX’s digital network and deep relationships can take clients anywhere they want to go.

Transparency

As a publicly traded company meeting the highest standards of regulatory compliance in the markets we serve, our financials and track record are matters of public record. StoneX’s commitment to “doing the right thing over the easy thing” sets us apart in the industry and helps us build respect, client trust and new partnerships.

Expertise

From our proprietary Market Intelligence platform to “boots-on-the-ground” expertise from award-winning traders and professionals, we connect our clients directly to actionable insights they can use to make more informed decisions and achieve their goals in the global markets.