Daily Coffee Report 8/6/26

Daily coffee report

StoneX Coffee Team

- Coffee

By: Leonardo Rossetti, Market Intelligence Analyst

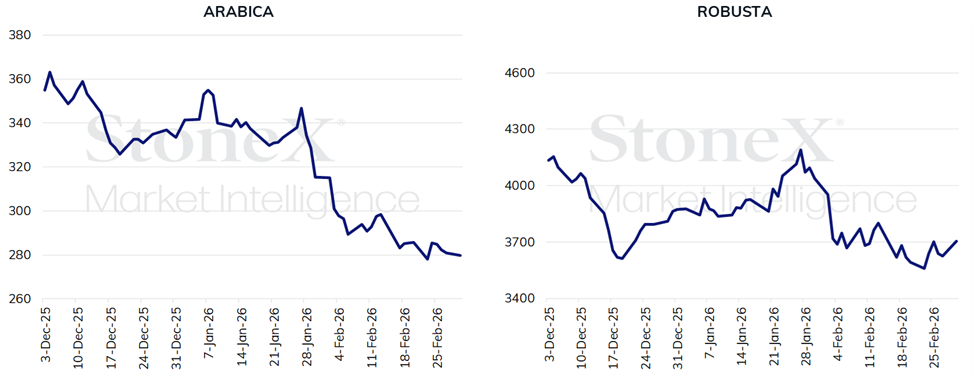

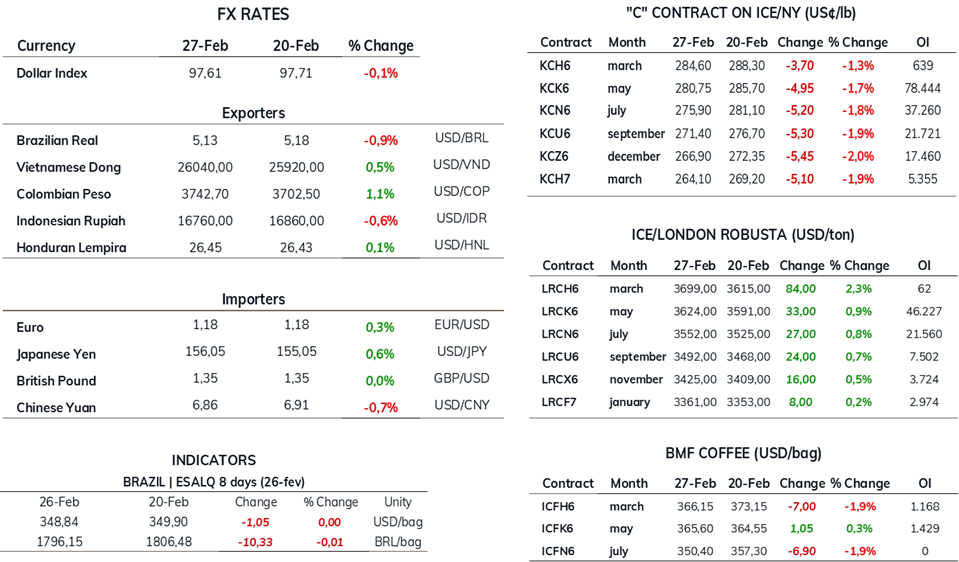

The past week delivered mixed results for coffee futures, with arabica prices falling in New York and robusta prices rising in London. The May arabica contract showed a weekly drop of 1.7%, closing at US¢ 280.75/lb. Meanwhile, in London, despite volatility throughout the week, robusta managed to end with a modest gain of 0.9%, priced at USD 3,624/ton.

In Brazil, optimism persisted, keeping the market under pressure. Positive expectations for the upcoming crop and favorable weather conditions have solidified a low-price scenario, with corrections being punctual and narrow, at least during the first semester.

Regarding arabica, the market remains pressured mainly due to the outlook for ample supply from Brazil's harvest. The incoming crop in the next few months is likely to reinforce the bearish trend and further pressure country differentials.

Arabica coffee futures prices (US¢/lb) robusta coffee (USD/ton)

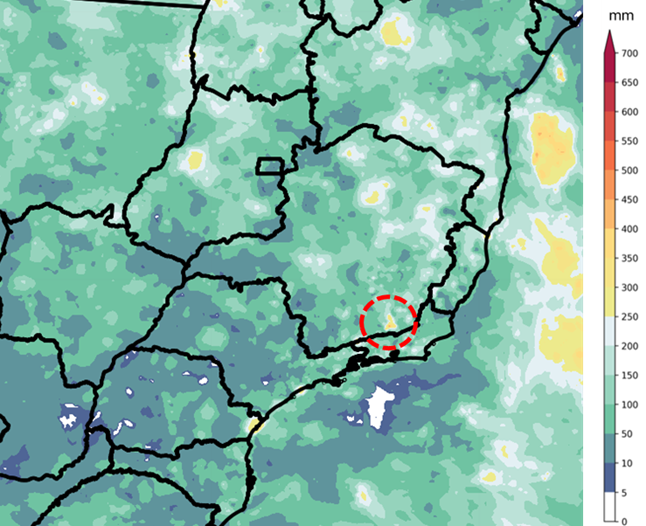

Excess rainfall in Zona da Mata: Throughout the week, the market monitored heavy rainfall that caused flooding in some towns in Zona da Mata — Brazil's second-largest arabica-producing region. However, StoneX's weather maps indicated that critical points were isolated and did not result in significant damage to the crops.

Rainfall history over the last 14 days in Brazil's Southeast region

Recovery in certified stocks: As anticipated last week, certified stocks saw an uptick. ICE reported an increase of almost 20,000 bags, reaching 477,000 bags on Friday (27), the highest level since October last year.

Why it matters: Although still below the average of recent years, the recovery — combined with the expectation of more bags being submitted for grading — helps mitigate the perception of tight global availability. While not a precise reflection of global stocks, certified stocks act as a last-resort reserve and a relevant gauge of available supply.

Robusta with slight gains: Robusta posted modest advances driven by weather instabilities in Vietnam, which may disrupt local dynamics in the short term. Following the return of Asian holidays, the market regained momentum, with producers trying to hold back part of production in anticipation of higher prices, although trade is expected to pick up in the coming weeks. Weather conditions in the country remain under scrutiny.

Brazilian physical market: The Cepea indicator ended the week showing an arabica coffee price of R$ 1,797.6/bag, down 0.5%. Meanwhile, the robusta coffee indicator marked a 1.0% decline, priced at R$ 1,032.7/bag.

What could shift the market's bearish bias?

In a moment of predominantly optimistic perspectives across most major producing countries, except Colombia, new climate instability seems to be the factor most likely to bring volatility to the market.

In this context, while an El Niño scenario already appears highly probable for the second half of the year, monitoring the intensity of the phenomenon will be critical during the pre-flowering period. While a weak El Niño could have positive effects by bringing rainfall to the coffee belt, higher intensity, with significant warming, could raise concerns.

Therefore, based on current monitoring models, this could be the primary factor driving an increased perception of risk among traders and investors, providing more sustained support.

For this week: Alongside weather conditions in Brazil and Vietnam, traders should monitor upcoming releases of Vietnam's export figures and Colombia's production data for February. Preliminary Brazilian export data for last month will also be published by Secex.

Geopolitical conflict: On Monday, coffee futures prices appeared to be closely linked to heightened geopolitical tensions in the Middle East, particularly stemming from rising crude oil futures.

Long-term impact: Over the medium to long term, however, the effect could take a different trajectory.

Despite the transition of ENSO La Niña to neutrality, some residual effects of the phenomenon persist, contributing to weather disruptions across several regions.

Vietnam: In Vietnam, heavy rainfall in the Central Highlands — the main producing region — raised concerns during the final development stage of some fruits for the 2025/26 crop, increasing the risk of fungal diseases, hindering drying processes, and even causing fruit drop from later flowerings.

StoneX weather maps indicate that rainfall is expected to continue over the next two weeks but at more moderate levels, which may help normalize conditions. Nonetheless, the situation remains under market scrutiny.

Colombia: In Colombia, torrential rains persist and may pressure differentials in the short term, exacerbating the already challenging scenario observed in January and February — a period when 30-day anomaly maps showed volumes well above average. Heavy rainfall has caused blockages, landslides, and erosion in production areas.

The 60-day anomaly maps indicate accumulations ranging from 60% to 100% above historical averages for the period across almost the entire country, harming flowering and, consequently, fruit formation in the coming months. The severity of the situation has prompted the government to implement emergency financial aid measures. The forecast for the next seven days suggests less intense rainfall, which may bring partial relief; however, there’s a risk of renewed intensity in the following week, requiring continuous monitoring.

For more details on historical data and forecasts for these countries, access the climate map dashboard.

Keurig Dr Pepper quarterly results

Last Tuesday (24), Keurig Dr Pepper (KDP) released its Q4 and full-year 2025 results.

Why it matters: Given its size and the widespread use of Keurig systems in the U.S., its figures provide valuable insights into domestic consumption behavior in one of the world’s leading coffee consumer markets.

Details: In 2025, the coffee division’s revenue remained stable, with slight annual growth (+0.6%).

Luckin Coffee quarterly results

Market participants also monitored the release of Luckin Coffee’s Q4 2025 results on Wednesday (26).

Why it matters: Due to its operational scale and rapid expansion pace, Luckin’s figures provide direct insights into coffee demand in the world’s largest emerging consumer market.

INDICATOR TABLE

The StoneX Group Inc. group of companies provides financial services worldwide through its subsidiaries, including physical commodities, securities, exchange-traded and over-the-counter derivatives, risk management, global payments and foreign exchange products in accordance with applicable law in the jurisdictions where services are provided. References to over-the-counter (“OTC”) products or swaps are made on behalf of StoneX Markets LLC (“SXM”), a member of the National Futures Association (“NFA”) and provisionally registered with the U.S. Commodity Futures Trading Commission (“CFTC”) as a swap dealer. SXM’s products are designed only for individuals or firms who qualify under CFTC rules as an ‘Eligible Contract Participant’ (“ECP”) and who have been accepted as customers of SXM. StoneX Financial Inc. (“SFI”) is a member of FINRA/NFA/SIPC and registered with the MSRB. SFI is registered with the U.S. Securities and Exchange Commission (“SEC”) as a Broker-Dealer and with the CFTC as a Futures Commission Merchant and Commodity Trading Adviser. References to securities trading are made on behalf of the BD Division of SFI and are intended only for an audience of institutional clients as defined by FINRA Rule 4512(c). References to exchange-traded futures and options are made on behalf of the FCM Division of SFI . StoneX is a trading name of StoneX Financial Ltd (“SFL”). SFL is registered in England and Wales, Company No. 5616586. SFL is authorized and regulated by the Financial Conduct Authority [FRN 446717] to provide to professional and eligible customers including: arrangement, execution and, where required, clearing derivative transactions in exchange traded futures and options. SFL is also authorised to engage in the arrangement and execution of transactions in certain OTC products, certain securities trading, precious metals trading and payment services to eligible customers. SFL is authorised & regulated by the Financial Conduct Authority under the Payment Services Regulations 2017 for the provision of payment services. SFL is a category 1 ring-dealing member of the London Metal Exchange. In addition SFL also engages in other physically delivered commodities business and other general business activities which are unregulated and not required to be authorised by the Financial Conduct Authority. StoneX Group Inc. acts as agent for SFL in New York with respect to its payments services business. StoneX APAC Pte. Ltd. acts as agent for SFL in Singapore with respect to its payments services business. ‘StoneX’ is the trade name used by StoneX Group Inc. and all its associated entities and subsidiaries.

Trading swaps and over-the-counter derivatives, exchange-traded derivatives and options and securities involves substantial risk and is not suitable for all investors. Past performance of any futures or option is not indicative of future success. Indicators are not a trading system and are not published as a specific trade recommendation. The information herein is not a recommendation to trade nor investment research or an offer to buy or sell any derivative or security. It does not take into account your particular investment objectives, financial situation or needs and does not create a binding obligation on any of the StoneX group of companies to enter into any transaction with you. You are advised to perform an independent investigation of any transaction to determine whether any transaction is suitable for you. No part of this material may be copied, photocopied or duplicated in any form by any means or redistributed without the prior written consent of StoneX Group Inc.

© 2026 StoneX Group Inc. All Rights Reserved.

Our subscribers have access to comprehensive market analysis from StoneX spanning commodities, equities, currencies and more.

Daily coffee report

August 6 – This morning’s stronger-than-expected U.S. labor data offered markets some relief, reinforcing confidence in the economy while giving the Fed greater flexibility to raise rates should inflationary pressures reaccelerate in next week’s July data. Stock futures are pointing to a mixed open to start the day, with the tech-heavy Nasdaq showing the most weakness. The VIX has fallen notably from yesterday’s spike above 18.4 as it starts the day hovering just below the 16-mark. The dollar is quietly higher as it trades just above 99.8, holding in the tight range seen thus far this week as traders continue to digest data to shape expectations for the Fed’s next move, which we’ll dive into in more depth below. Long-term treasury yields have relaxed slightly from their recent spike, with 30-year yields starting the day trading just above 5.19%, while 10-year yields trade above 4.64%, and 2-year yields sit below 4.22%. Crude oil is modestly higher to start the session after sharp declines earlier in the week, with nearby WTI up 1.8% to trade at $76.40 and nearby Brent up 2.4% to trade at $81.40. Meanwhile, the ags are quietly mixed to start the day.

Daily coffee report

Our market expertise, advanced platforms, global reach, culture of full transparency and commitment to our clients’ success all set us apart in the financial marketplace.

Reach

With access to 40+ derivatives exchanges, 180+ foreign exchange markets, nearly every global securities marketplace and numerous bilateral liquidity venues, StoneX’s digital network and deep relationships can take clients anywhere they want to go.

Transparency

As a publicly traded company meeting the highest standards of regulatory compliance in the markets we serve, our financials and track record are matters of public record. StoneX’s commitment to “doing the right thing over the easy thing” sets us apart in the industry and helps us build respect, client trust and new partnerships.

Expertise

From our proprietary Market Intelligence platform to “boots-on-the-ground” expertise from award-winning traders and professionals, we connect our clients directly to actionable insights they can use to make more informed decisions and achieve their goals in the global markets.