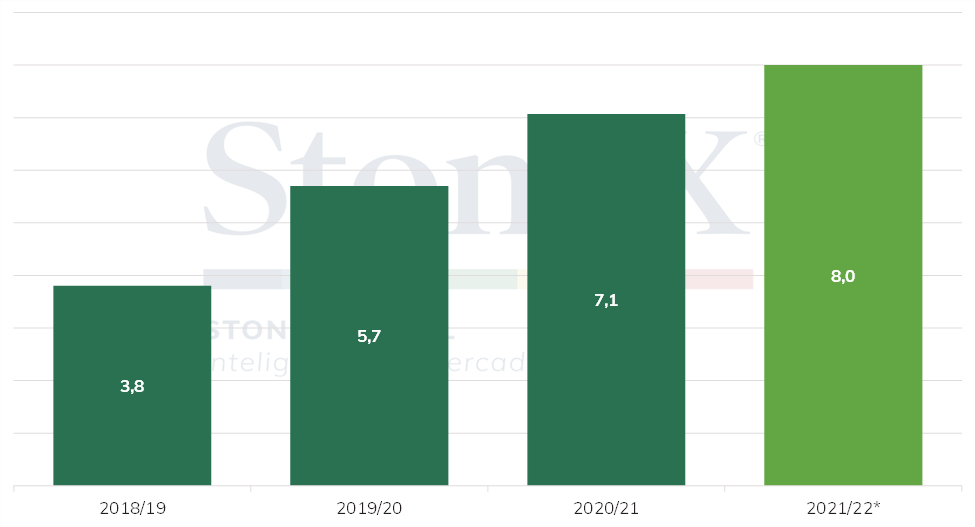

Mills are expected to direct a record volume abroad in the current season

On Monday, bearish factors prevailed for crude oil futures, amid the spread of Covid-19 in China and greater optimism about an agreement between Russia and Ukraine. Following this movement, the #11 May/22 contract closed the ICE/NY session quoted at 19.59 c/lb, accumulating a loss of 0.1% in relation to Friday’s closing.

The good performance of the 2021/22 crop (Oct-Sept) in India also makes raw sugar’s S&D balance more comfortable. In fact, sugar production should reach a record in Maharashtra and Karnataka, amid sugarcane fields productivity gains. On the other hand, in Uttar Pradesh, use for ethanol production and lower sugar extraction rates may pressure supply at the end of the crop, which is projected to reach 10 million tonnes, a volume that falls below ISMA expectations by 200,000 tonnes.

Our estimates are that the Asian country will have the potential to produce about 33.2 million tonnes of sugar in the current cycle, allowing exports to remain strong. This view is supported by growing international demand, as well as by the increased competitiveness of the Indian product at the expense of other players, particularly amid firm ocean freight prices.

According to indications, India has already contracted about 7.0 million tonnes for export, showing that allocation of sugar abroad could renew the highs recorded in the 2020/21 cycle, of 7.1 million tonnes. Given the recent performance, it seems likely that the country has the potential to export 8.0 million tonnes in the current season..

Sugar exports by India (million tonnes)

Source: ISMA. Design: StoneX.

If that comes true, our calculations point to ending stocks of 6.2 million tonnes, while New Delhi aims to start the 2022/23 crop with 6 to 7 million tonnes of reserves, a volume that would be enough to supply domestic demand at the end of this year. The great concern, therefore, revolves around the progress of Indian mills’ negotiations with the outside world, which could jeopardize the country’s food security.

In light of this situation, India discusses the possibility of restricting exports, placing a limit of 8.0 million tonnes for the current season, which acts as a support factor for sugar futures. If approved, this policy would go against the aid granted to the local sugar sector in order to facilitate increased allocation of sugar to the international market, reducing the product’s surplus in the domestic market. Given the expansion of ethanol production, it is clear that sugar output in India should have a lower global share in the coming years.

This measure would also aim to contain inflation, amid high food prices in the domestic market. This is not limited to India, as the conflict between Russia and Ukraine may also cause other players to give preference to domestic consumption, limiting sugar exports. As a result, it seems likely that the London New York differential (White Premium), used as a proxy for the refining margin, will continue to operate at sustained levels, even though the spread of Covid-19 and logistical barriers will be a point of attention for international demand for sugar.

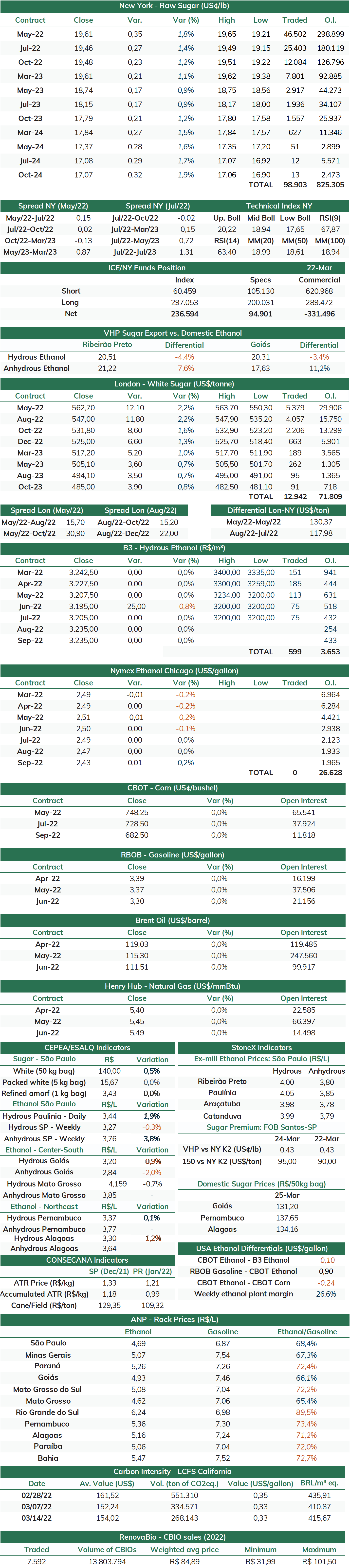

indicaTors