Top Global Macro Event Risk This Week: US Employment Data; US ISM Manufacturing and Services PMIs; China Trade and FX Reserves

Talking Points:

- Liquidity will be stifled over the coming week with the US market a notable gap owing to the Thanksgiving holiday closure

- Broader macro themes seem to have lost a significant amount of weight as far as dictating market trends, which shifts the focus to acute and local impacts from key events

- China’s economic course via industrial profits, the Fed’s favorite inflation indicator and key emerging market 3Q GDP releases are top event risk this week

Liquidity rebounds and so does the global macro-economic calendar over the coming trading week. The S&P 500’s open at a record high will draw actively upon the scheduled event risk ahead to fulfill - or contradict - the justification of speculative enthusiasm that seems increasingly at odds with the mix of the fundamental backdrop. It will be important to factor in the anticipation typical of this time of the year.

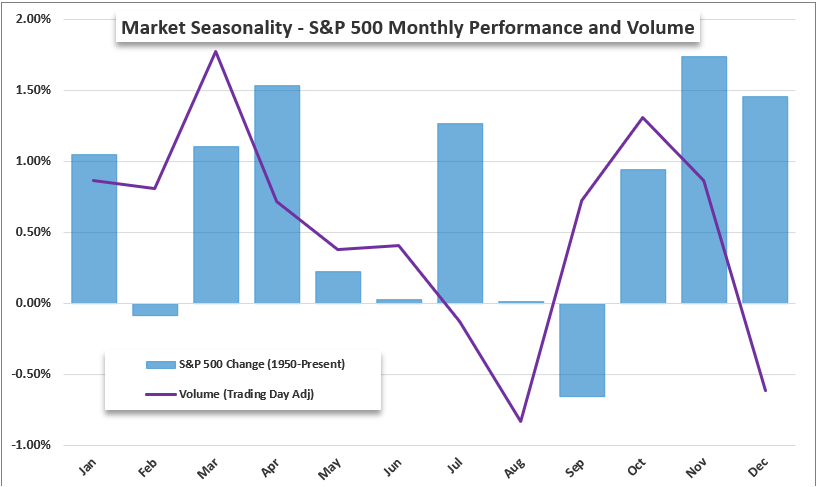

Chart of S&P 500 Average Weekly Performance and Volume for Past 100 and 75 Years

Source: TradingView, John Kicklighter

We are leading into the final stretch of the year with the back half of the month notably mired in the ‘holiday’ drawdown which materially diminishes liquidity. Yet, before we get to that progressive slide into the end of the year, there is a range of meaningful event risk that will perhaps find its zenith with the FOMC rate decision on December 18th. Before we get to that peak, however, there are some notables that we should be watching for this week.

Table of Major Global Macro Events Scheduled for Week

Source: John Kicklighter, StoneX

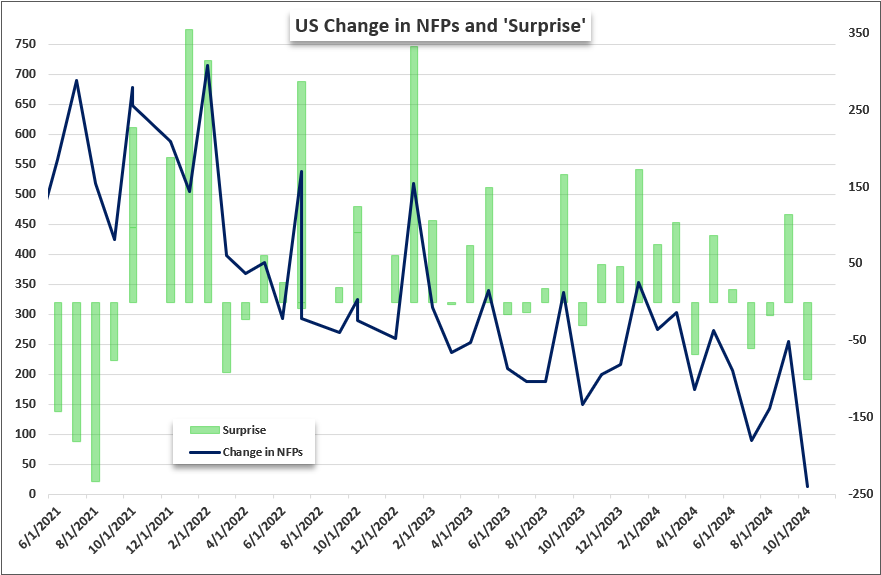

Top of mind through this week is the November employment data for the United States. There is perhaps more impact to be found in this data run through recognition alone than actual potential for fundamental upheaval, but volatility is volatility. The outlook for FOMC rate cuts this month now sees a one-in-three chance that the central bank won’t change rates at all, when not long ago a 25 bp cut was all but certain and larger moves out into 2025 was fully backed in.

It’s hard to say what is discounted at this point – thematically rather than through absolute measures like Fed Fund futures – because of the dramatic reversal in forecasts. That said, the concern around labor conditions deteriorating has been held up as the driving force for a dovish Fed shift as inflation has cooled substantially. Of course, the change in nonfarm payrolls (NFPs) is the most anticipated reading of the data run; but its Friday release leaves more anticipation than drive through the week. That said, the sensitivity to this theme in general will likely raise the profile of earlier readings like Thursday’s Challenger Job Cuts, Wednesday’s ADP private payrolls or Tuesday’s Job Openings and Quits from JOLTs.

Chart of US NFPs and the Level of ‘Surprise’ Relative to Forecasts

Source: US Bureau for Labor Statistics, John Kicklighter

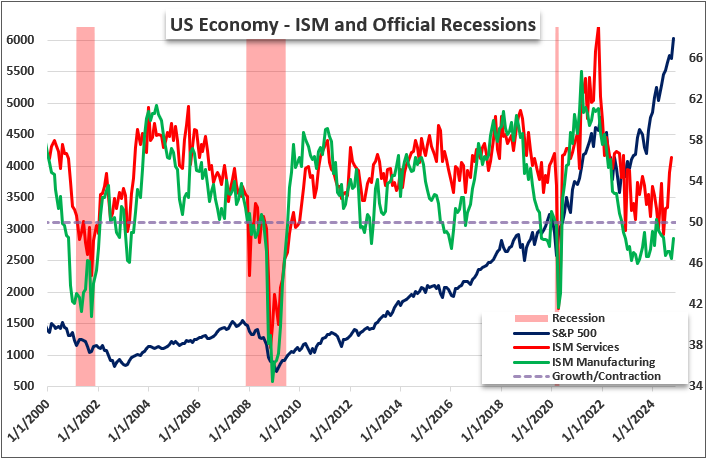

Keeping the focus on the United States, another fundamental perspective that will receive a meaningful update is a timely update on its economic health via the ISM’s Manufacturing and Service sector activity readings for November. These are good proxies for not only the economic contribution of these crucial sectors of the largest economy in the world, but they also offer important insight on employment and inflation trends. Between the two, the manufacturing survey due Monday carries less overall weight when it comes to reflecting upon the broader economy.

However, the Trump administration’s trade policies seem to focus far more attention upon this area with tariffs aimed at predominantly attempting to restore factory-based jobs. While there will be some degree of sentiment for what’s ahead in this month’s update, it is more likely a baseline setting reading. In contrast, the service sector (‘non-manufacturing’) survey is much more indicative of actual US GDP. That said, this reading has had an uneven record as a preeminent driver for the US dollar and capital markets over the past months. If anything, this will be a good litmus test to see whether the markets are focused on economic activity in general.

Chart of ISM (Daily)

Source: ISM, John Kicklighter

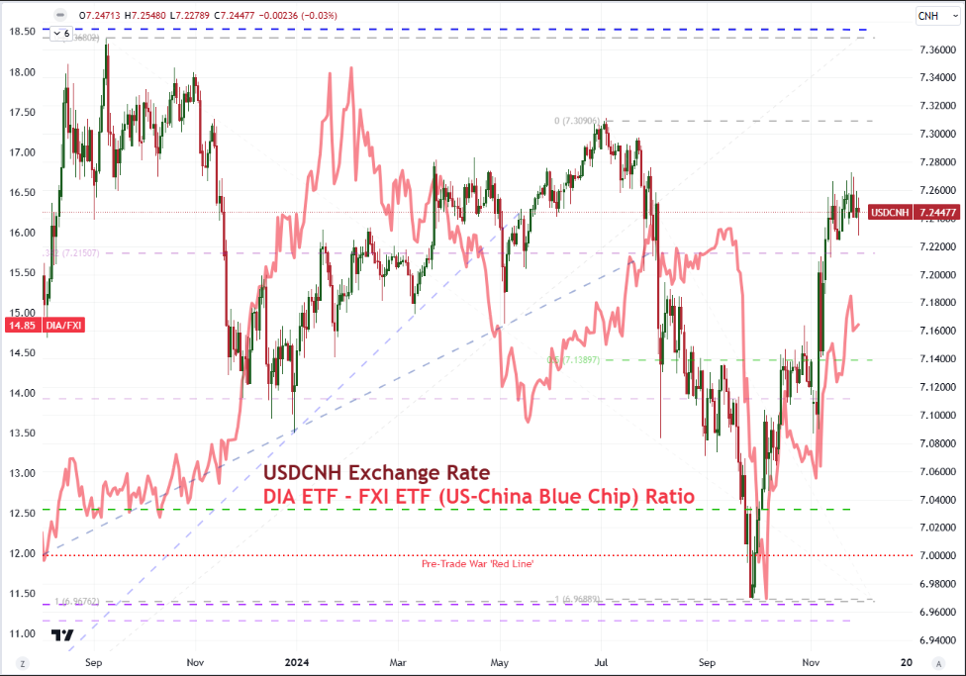

Finally, a third fundamental focus should go to the general health of China. We have seen fresh repo lines announced this past week to extend a mix of programs aimed at stimulus economic and financial activity in the struggling country. It is perhaps too early to see the fruits of these measures – not that the globe will necessarily take results at face value when they do show up – but we can at least get a sense of the backdrop for which these efforts are integrating. Notably, there are some Caixin PMIs on Monday (manufacturing) and Wednesday (services and composite); but my attention is actually turned to the close of the week, On Saturday, we are due China’s November trade balance and potentially the foreign exchange reserves for the same month.

Given the threats of additional tariffs coming from the Trump Administration, greatest attention will be paid for the health of this economic measure to highlight current weakness and to establish place-setter for trends moving forward. As for the reserves, the financial levers China has been pulling domestically and the seeming stability of the USDCNH seems to belie significant efforts being made to keep a controlled economy from succumbing to heavy global winds.

Chart of USDCNH and FXI China Large Cap ETF (Daily)

Source: TradingView, John Kicklighter

-- Written by John Kicklighter, Global Head of Content