Traders Are Eager and Anxious of Full Blown Risk Off, But Weigh the Probabilities

By: John Kicklighter, Head of Market Research

Risk appetite has extended its retreat through this past week and fears of a full-blown reversal are growing. While the pause in the advance raises anxiety, a lack of fundamental themes and key event risk along with seasonal expectations should be considered in gauging probabilities.

Talking Points:

Another week’s retreat for a range of risk assets was met with a breadth of rotation out of top performing market benchmarks like US tech stocks

Key technical levels still stand, however, such as the S&P 500’ and Dow Jones Industrial Average’s multi-month rising trend channel and 50-day moving average support

Top event risk this week comes in the second half of the week with: Nvidia earnings; the delayed change in US NFPs and October PMIs

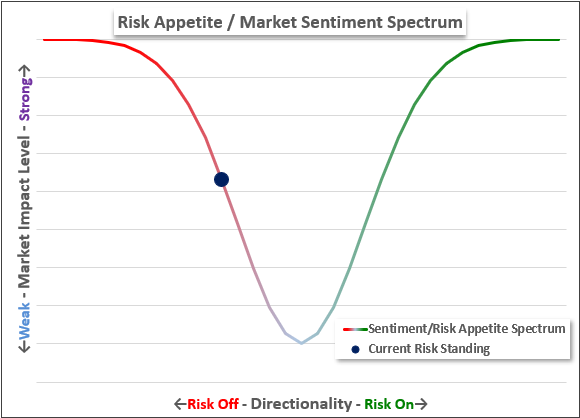

Risk Appetite Is Listing Heavily but Complacency Is Powerful

The benchmarks of risk appetite – including my preference of major US equity indices – extended this past week the shudder that has rippled through the financial system in November. Some of the key ingredients for a systemic shift in sentiment via these capital market guides is in place: there has been a rise in implied volatility measures across multiple asset classes; internal rotation shows pullback in some of the top performing assets of past weeks and months (eg mega cap tech stocks) and the thematic fundamental balance has tipped out of favor. Yet, despite the alignment of these elements, there remains a tangible lack of conviction in the form of a more productive and committed unwinding.

Sure, volatility has picked up counter to the seasonal norms, but the pickup is occurring from significantly lower levels. The relatively more intense retreat from favored risk assets (tech stocks vs broader equities, small caps compared to large blue chips, crypto, etc) is to be expected in a broader pullback as tempo higher is often matched in retreats. As for the waning traction and pressure behind key fundamental themes like trade, economic uncertainty and rate forecasts; that can work both ways. The absence of a strong fundamental guide may trip up the bulls looking for justification to add into stretched prices, but it also sustains the reticence to proactively unwind a position built and maintained by FOMO (fear of missing out).

S&P 500 with 50-Day Moving Average and Consecutive Days Above/Below (Daily) Source: TradingView.com, Standard & Poor’s

As we await the definitive bolt of fundamental lightning, I will keep closer tabs on technicals. While chart analysis is not given the same credibility as fundamentals when the latter is heavy; when the compass dial is spinning, major levels and trends on the same top level benchmarks can exert far more influence. In the assessment of maintaining the larger bull trend (whether passive or reasserted) or seeing fear taking over the backdrop sentiment, my first line of technical assessment will be the distinct rising trend channels for the likes of the S&P 500 and Dow Jones Industrial Average both of which happen to line up support to their respective 50-day simple moving averages.

S&P 500 with 50-Day Moving Average and Consecutive Days Above/Below (Daily) Source: TradingView.com, Standard & Poor’s

A Thinned Docket but With Heavy Hitters

While the market looks to be technically in a position where it can be easily provoked, triggering a substantial move while the backdrop lacks for fundamental champions puts a significant burden on event risk to overcome the reticence. Looking to the global macro docket, the top tier listings with capacity to reignite critical fires are thin. The tepid docket is further complicated by the uncertainty around the release of key economic data from the US following the reopening of the government. It is important to keep close watch for updated release times and dates for important readings like the overdue CPI. Potential US reports aside, there is trader-worthy fodder that should top our threat assessment radar through the coming week. The most critical listings happen to be concentrated to the back half of the week, but market participants should keep tabs on the current throughout the week to garner a sense of the backdrop for which the event risk will land.

Calendar of Top Global Macro Event Risk Source: John Kicklighter

The King of Earnings Season Comes at a Lull in AI Conviction

If we were to boil down the macro listings through the next week to a mere three listings, the first high profile release that holds a high capacity to seize the financial headlines comes after the US market close on Wednesday. Top market cap US stock Nvidia will reports its quarterly figures at 21:20 GMT on November 19th, and the company hasn’t seen its top line earnings miss expectations in three years – which seemed to have been a one off. Within the stock market, there is considerable weight to afford to NVDA given its size, but there is far more fundamental influence to this particular company than its simple standing in the depth charts.

For many, this ticker stands as the leader of the major tech firms that have paced US equity indices and the popular AI theme that has carried optimism far and wide. While an objective reading of the company’s performance metrics would be convenient, there is likely to be a heavy skew from underlying speculative assumptions. Notably, the past five earnings reports have seen NVDA drop following a technical beat from the company – and alongside an unflappable confidence in the transformative value of artificial intelligence to the financial system and economy. How will the response adapt should we enter the release with the past two weeks’ retreat unresolved?

Chart of Nvidia Stock Price with 100-Day SMA (Daily) Source: TradingView.com

Finally, NFPs and a Market Eager for the Update

As far as what scheduled event risk carries the greatest potential to single-handedly set course for the broader market, the Nvidia earnings has a strong claim to the throne. However, if there were any other report that would reasonably be in a position to compete for our collective attention it would be the first US employment report in two months. The September nonfarm payrolls – and accompanying employment data – was due for release on Friday, October 3rd. However, Congress was unable to reach a budget resolution by midnight September 30th and so the federal government was shut. This latest shutdown ran for a record breaking 43 days before it both houses agreed to a appropriations bill and President Trump signed the agreement on November 12th.

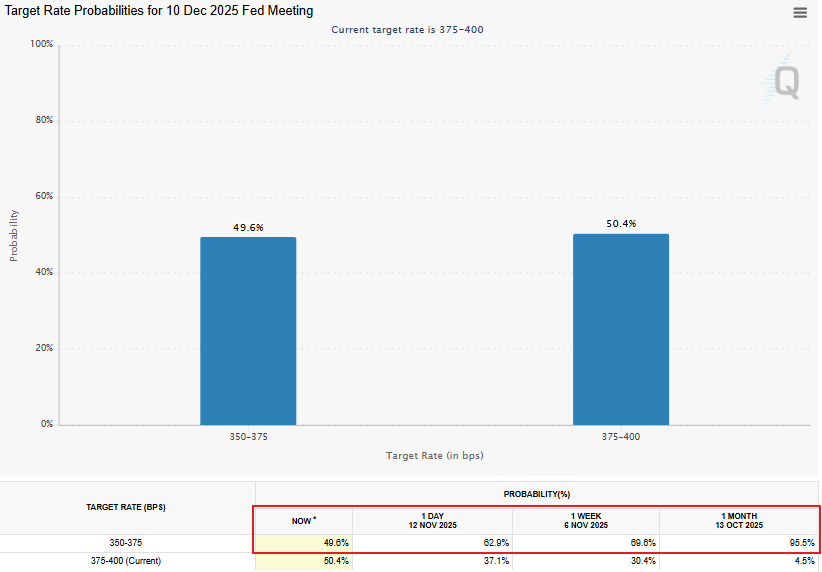

Even though the country’s data agencies are reopened, it remains unclear when we can expect the previous data readings – or if we will see certain data points at all, as it has been suggested by the White House that the October CPI may not be furnished at all. That said, there is one important backdated update due on Thursday at 13:30 GMT: the September NFPs. Notably, in the context of the Fed’s dual mandate (full employment and a two percent inflation target), inflation pressures present the hawkish threat while the softening labor stats are the dovish leg. If the dated jobs figures show sustained pressure on this growth figure, the recent drop in December FOMC rate forecasts – from approximately 96 percent certainty a month ago to less than 50 percent this past week – may find motivation for resurgence which in turn can revive stimulus-motivated risk appetite.

Probabilities for December 10 FOMC Decision Source: CME, Fed Funds Futures

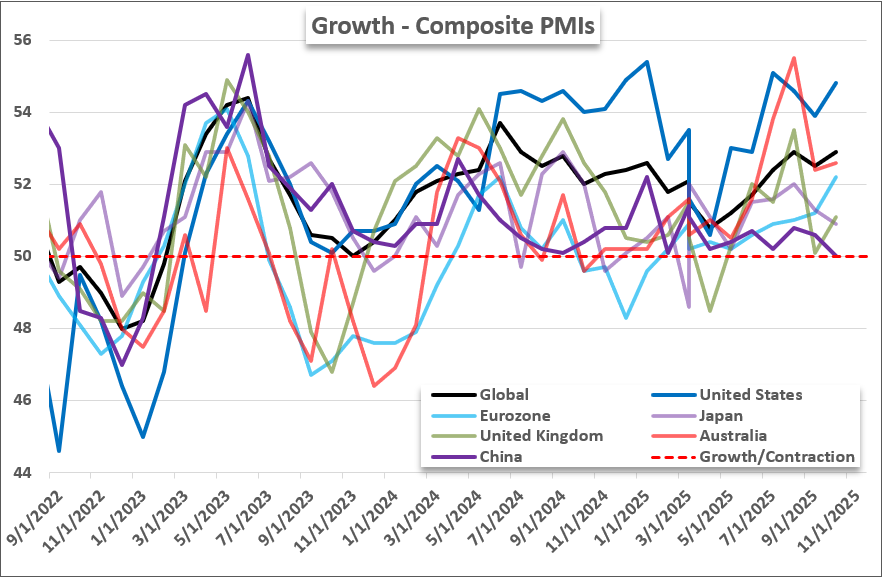

A Global Economic Update from the Timely PMIs

The final, top fundamental theme to monitor through this coming week is the timely, global growth reflection provided by the S&P Global PMI figures for November. This data tap a number of important wells from which deeper trends emerge. Most notably, this is a broad and timely read of economic health during a period where the outlook is particularly opaque through both the general trend and due to the gap in official data (out of the US). Despite the fading light in many ancillary economic feeds, the ‘composite’ figure trends of these major economies has generally trended towards growth through this past month’s update. This could provide a countertrend lift against growing concerns and the pullback in speculative positioning. Then again, if the data deteriorates, it could heap onto the broadening concerns and add a traditional weight to the otherwise speculative focus. Historically, this is not an established market-moving event risk for indices, exchange rates and other macro markets; but context is everything.

Composite PMIs for Major Economies (Monthly) Source: S&P Global

-- Written by John Kicklighter, Global Head of Content

The subsidiaries of StoneX Group Inc. provide financial products and services, including, but not limited to, physical commodities, securities, clearing, global payments, risk management, asset management, foreign exchange, and exchange-traded and over-the-counter derivatives. These financial products and services are offered in accordance with the applicable laws in the jurisdictions in which they are provided and are subject to specific terms, conditions, and restrictions contained in the terms of business applicable to each such offering. Not all products and services are available in all countries. The products and services offered by the StoneX

Group of companies involve risk of loss and may not be suitable for all investors. Full Disclaimer.

This content is not intended for residents of any particular country, and the information herein is not advice nor a recommendation to trade nor does it constitute an offer or solicitation to buy or sell any financial product or service, by any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation. Please refer to the Regulatory Disclosure section for entity-specific disclosures.

No part of this material may be copied, photocopied or duplicated in any form by any means or redistributed without the prior written consent of StoneX Group Inc. The information herein is provided for informational purposes only. This information is provided on an ‘as-is’ basis and may contain statements and opinions of the StoneX Group of companies as well as excerpts and/or information from public sources and third parties and no warranty, whether express or implied, is given as to its completeness or accuracy. Each company within the StoneX Group of companies (on its own behalf and on behalf of its directors, employees and agents) disclaims any and all liability as well as any third-party claim that may arise from the accuracy and/or completeness of the information detailed herein, as well as the use of or reliance on this information by the recipient, any member of its group or any third party.

Currencies

The subsidiaries of StoneX Group Inc. provide financial products and services, including, but not limited to, physical commodities, securities, clearing, global payments, risk management, asset management, foreign exchange, and exchange-traded and over-the-counter derivatives. These financial products and services are offered in accordance with the applicable laws in the jurisdictions in which they are provided and are subject to specific terms, conditions, and restrictions contained in the terms of business applicable to each such offering. Not all products and services are available in all countries. The products and services offered by the StoneX Group of companies involve risk of loss and may not be suitable for all investors. Full Disclaimer. This content is not intended for residents of any particular country, and the information herein is not advice nor a recommendation to trade nor does it constitute an offer or solicitation to buy or sell any financial product or service, by any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation. Please refer to the Regulatory Disclosure section for entity-specific disclosures. No part of this material may be copied, photocopied or duplicated in any form by any means or redistributed without the prior written consent of StoneX Group Inc. The information herein is provided for informational purposes only. This information is provided on an ‘as-is’ basis and may contain statements and opinions of the StoneX Group of companies as well as excerpts and/or information from public sources and third parties and no warranty, whether express or implied, is given as to its completeness or accuracy. Each company within the StoneX Group of companies (on its own behalf and on behalf of its directors, employees and agents) disclaims any and all liability as well as any third-party claim that may arise from the accuracy and/or completeness of the information detailed herein, as well as the use of or reliance on this information by the recipient, any member of its group or any third party.

Our market expertise, advanced platforms, global reach, culture of full transparency and commitment to our clients’ success all set us apart in the financial marketplace.

Reach

With access to 40+ derivatives exchanges, 180+ foreign exchange markets, nearly every global securities marketplace and numerous bilateral liquidity venues, StoneX’s digital network and deep relationships can take clients anywhere they want to go.

Transparency

As a publicly traded company meeting the highest standards of regulatory compliance in the markets we serve, our financials and track record are matters of public record. StoneX’s commitment to “doing the right thing over the easy thing” sets us apart in the industry and helps us build respect, client trust and new partnerships.

Expertise

From our proprietary Market Intelligence platform to “boots-on-the-ground” expertise from award-winning traders and professionals, we connect our clients directly to actionable insights they can use to make more informed decisions and achieve their goals in the global markets.

Source: S&P Global

Source: S&P Global