The Federal Reserve has restarted its dovish policy shift and expectations are set high for how deeply they may cut. How far will they really go and what is the market’s potential response?

To sign up for the Trading Global Macro podcast, find it on your preferred podcast platform: Apple Podcasts, Spotify, or YouTube.

Talking Points:

The Federal Reserve cut its benchmark rate for the first time in 2025 at its September meeting

Despite the market’s aggressive ‘risk on’ reach, the market’s forecasts for rate cuts seem less aggressive, the FOMC’s own views are a step down and data is far less accommodative

With Fed Chairman Powell due to be step down in May, will the Fed really transition into a group that will fulfil the 200-300 bps of rate cuts the White House is calling for?

Where the Fed’s Expectations Sit Now

On September 17th, the Federal Reserved announced that it was lowering its benchmark lending rate by 25 basis points (bps) to a range of 4.00 – 4.25 percent. That was the first cut by the world’s largest central bank of 2025, and a move that its detractors suggest is coming far too late and well under scale. The debate around what path the Federal Open Market Committee (FOMC) ‘should’ follow is intense with many different opinions focusing on a range of priorities. That variation of possible outcomes can lead to a difficulty in ‘discounting’ the outlook which in turn raises the floor of volatility for capital markets like US equities, fixed income and FX markets – particularly for the Dollar.

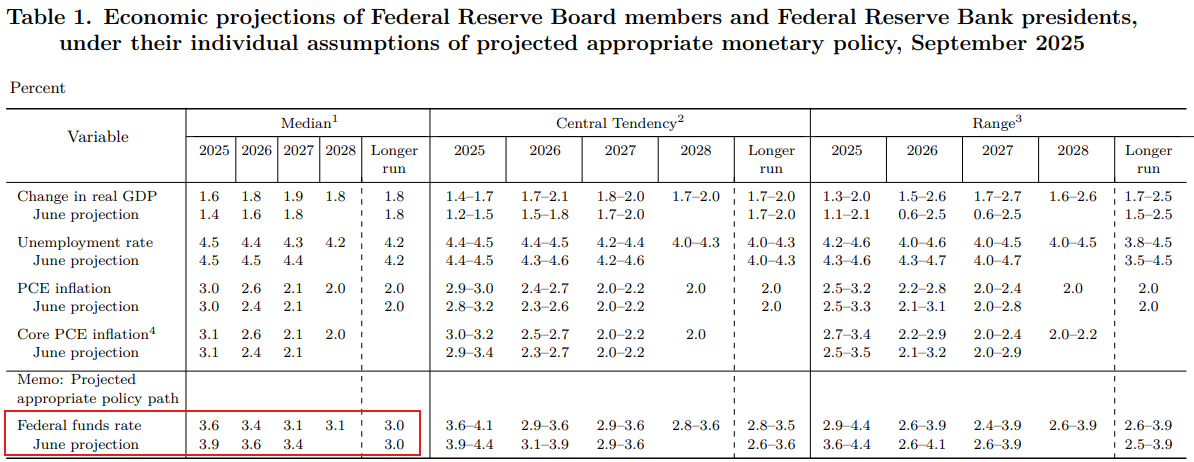

Before diving into the different groups with their competing expectations and priorities, it is worth first establishing a foundation of what the central bank itself expects to do. Looking to their Summary of Economic Projections (SEP) from the policy decision, the group downgraded its outlook for the benchmark rate through 2025 and 2026 to a range average of 3.6 and 3.4 percent. That is a 25bp stepdown from June’s forecasts. From current, that would represent another 50bps of cuts this year and one additional 25bps of easing next year. That is not much.

FOMC Summary of Economic Projections from September 2025 Meeting

Source: Federal Reserve

What Do the Markets Expect

At its present setting the US benchmark rate is higher than all of its major peers: European Central Bank; Bank of England; Bank of Canada; Bank of Japan; People’s Bank of China; Swiss National Bank and Reserve Bank of Australia. If its global counterparts were all at the end of their easing phase, there would be some inversion of the spreads – like with the US/UK and US/Australian differentials – but it is unlikely that this remains a one-sided adjustment.

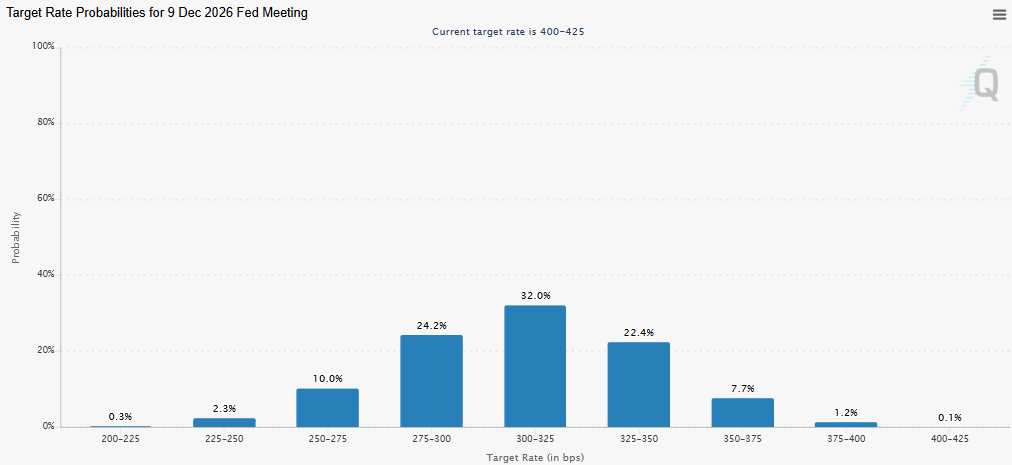

Another, moving target when it comes to rate expectations is the outlook of the market itself. There are different means for drawing expectations, but Fed Fund Futures provide perhaps the most direct market expression of the US interest rate path. According to the CME’s FedWatch tool, the probability of rates dropping ‘only’ to that 3.4 percent level by end of 2026 – as the FOMC expects – is only 22 percent. It is a sparse 9 percent probability that the rate will be higher than that level by the end of the period.

Interest Rate Forecasts Through End of 2026

Source: CME FedWatch Tool

There are Many Moving Parts in This Monetary Policy Course

When it comes to the variable possible bearings of US monetary policy moving forward, there are a few major considerations that can dramatically alter our course. Of course there is the trend behind the Fed’s stated ‘dual mandate’ which focuses on measured inflation growth (loosely 2 percent annual) and natural full employment. Those factors are fluid enough with the backdrop of growth trends and tariffs adding to price pressures. However, they are perhaps the most readily tracked of the moving parts.

Dispute over the balanced priority between price pressures and employment is a first stage consideration with the White House leading the charge. US President Donald Trump has suggested that the economy is in great condition, says there is ‘no inflation’ and has suggested that interest rates should be 300 bps lower than the current standing. A little more nuanced in the criticism is the claims that the data the central bank uses is flawed. Substantial downward revisions in the annual final jobs figures (through May) gave significant purchase to those concerns. Erosion of trust in the core data that dictates decision making can make it difficult for a group that adheres to ‘data dependency’.

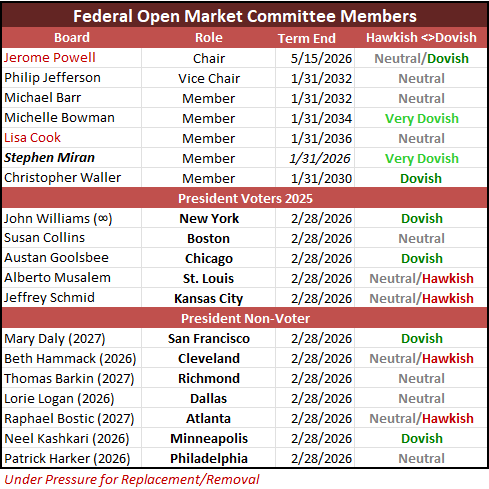

Another flashpoint for monetary policy direction is the pressure placed on the central bank decision makers themselves. President Trump has made very clear his lack of belief in Chairman Jerome Powell and may have even sought means to oust the leader before his term is complete. Whether pressured out early or not, a new Chairman will be in come May of next year who directs the central bank in a very different direction. Further, the effort to remove Board of Governors member Lisa Cook has raised concerns about the policy spectrum demographic – particularly after Stephen Miran joined from a White House role with a very dovish policy stance.

FOMC Member Relative Policy Stance

Source: John Kicklighter

Markets to Watch Through This Fundamental Lens

If we look out over 15 months, the path that sees the US benchmark rate 200 basis points higher or lower can have a profound impact on not just local markets. It can carry significant consequences for the financial markets where the dollar and US treasuries are among the most heavily used reserves.

For the US Dollar, the typical association is that lower benchmarks are treated as a lower yield to attract less foreign capital towards US assets. Inversely, a higher yield typically leads to greater appeal for the currency on that dimension. Of course, that doesn’t always prove to be the case. In a broadly low rate environment, there is also the chance of more restrictive economic conditions that may promote demand for ‘safer’ assets. The reserve status for the ‘greenback’ has reflected that role at periods in the past.

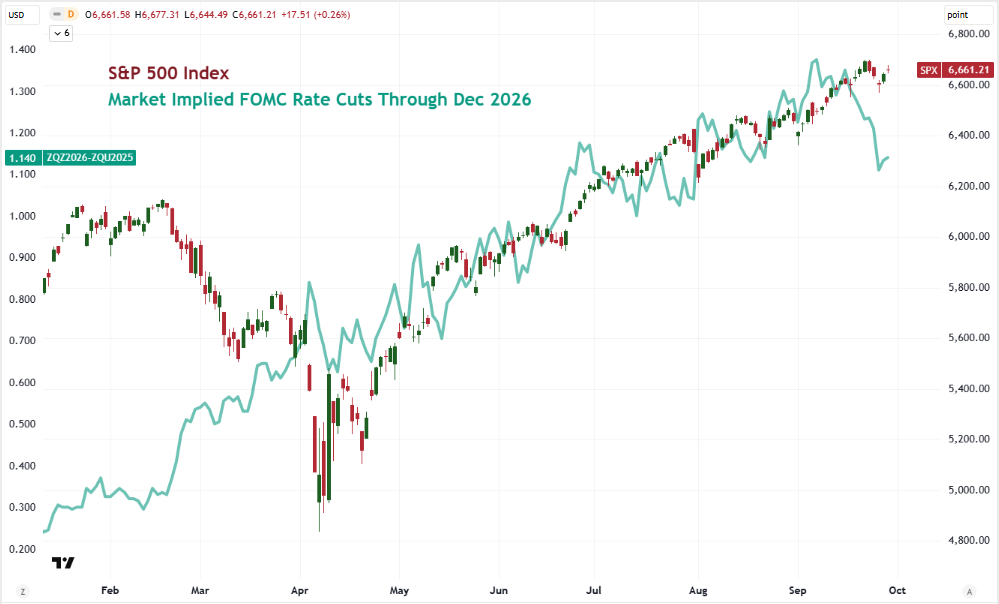

As for capital market benchmarks like the S&P 500, a lower rate environment increases the capital in the system. That infusion of liquidity in turn can translate into distribution towards assets whose growth can offset a deflationary fiat environment. Then again, if the prompt for lowering rates significantly is concern over economic potential or financial stability, such assets can be seen as unappealingly risky.

Chart of S&P 500 Overlaid with the Implied Aggregate Rate Cuts Through Dec 2026 (Daily)

Source: TradingView; Standard & Poor’s; CME

Follow the Global Macro Calendar

What are the major events and indicators on tap for the global economy that could charge volatility in markets and reshape deeper fundamental themes? Sign up for the updated Global Macro Calendar updated each week with a two week look ahead of the top events!

The subsidiaries of StoneX Group Inc. provide financial products and services, including, but not limited to, physical commodities, securities, clearing, global payments, risk management, asset management, foreign exchange, and exchange-traded and over-the-counter derivatives. These financial products and services are offered in accordance with the applicable laws in the jurisdictions in which they are provided and are subject to specific terms, conditions, and restrictions contained in the terms of business applicable to each such offering. Not all products and services are available in all countries. The products and services offered by the StoneX Group of companies involve risk of loss and may not be suitable for all investors. Full Disclaimer. This content is not intended for residents of any particular country, and the information herein is not advice nor a recommendation to trade nor does it constitute an offer or solicitation to buy or sell any financial product or service, by any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation. Please refer to the Regulatory Disclosure section for entity-specific disclosures. No part of this material may be copied, photocopied or duplicated in any form by any means or redistributed without the prior written consent of StoneX Group Inc. The information herein is provided for informational purposes only. This information is provided on an ‘as-is’ basis and may contain statements and opinions of the StoneX Group of companies as well as excerpts and/or information from public sources and third parties and no warranty, whether express or implied, is given as to its completeness or accuracy. Each company within the StoneX Group of companies (on its own behalf and on behalf of its directors, employees and agents) disclaims any and all liability as well as any third-party claim that may arise from the accuracy and/or completeness of the information detailed herein, as well as the use of or reliance on this information by the recipient, any member of its group or any third party.

Our market expertise, advanced platforms, global reach, culture of full transparency and commitment to our clients’ success all set us apart in the financial marketplace.

Reach

With access to 40+ derivatives exchanges, 180+ foreign exchange markets, nearly every global securities marketplace and numerous bi-lateral liquidity venues, StoneX’s digital network and deep relationships can take clients anywhere they want to go.

Transparency

As a publicly traded company meeting the highest standards of regulatory compliance in the markets we serve, our financials and record of accomplishment are matters of public record. StoneX’s commitment to “doing the right thing over the easy thing” sets us apart in the industry and helps us build respect, client trust and new partnerships.

Expertise

From our proprietary Market Intelligence platform, to “boots on the ground” expertise from award-winning traders and professionals, we connect our clients directly to actionable insights they can use to make more informed decisions and achieve their goals in the global markets.

Source: Federal Reserve

Source: Federal Reserve