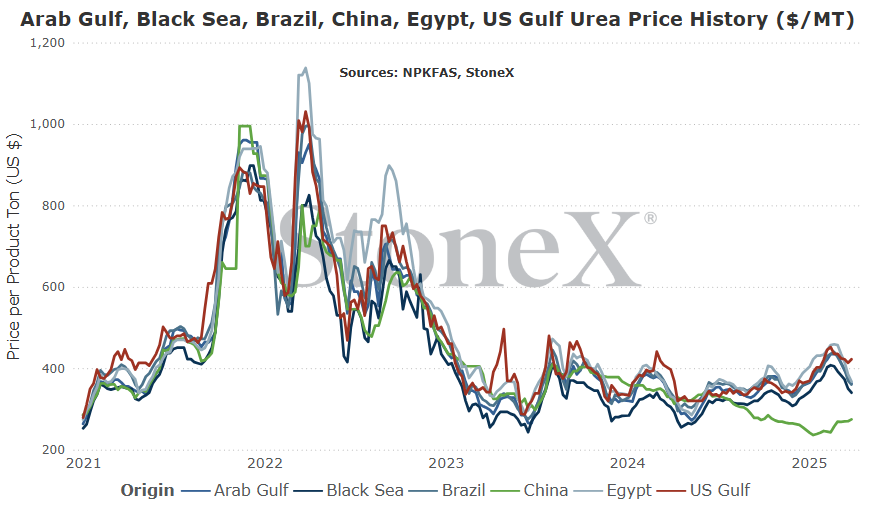

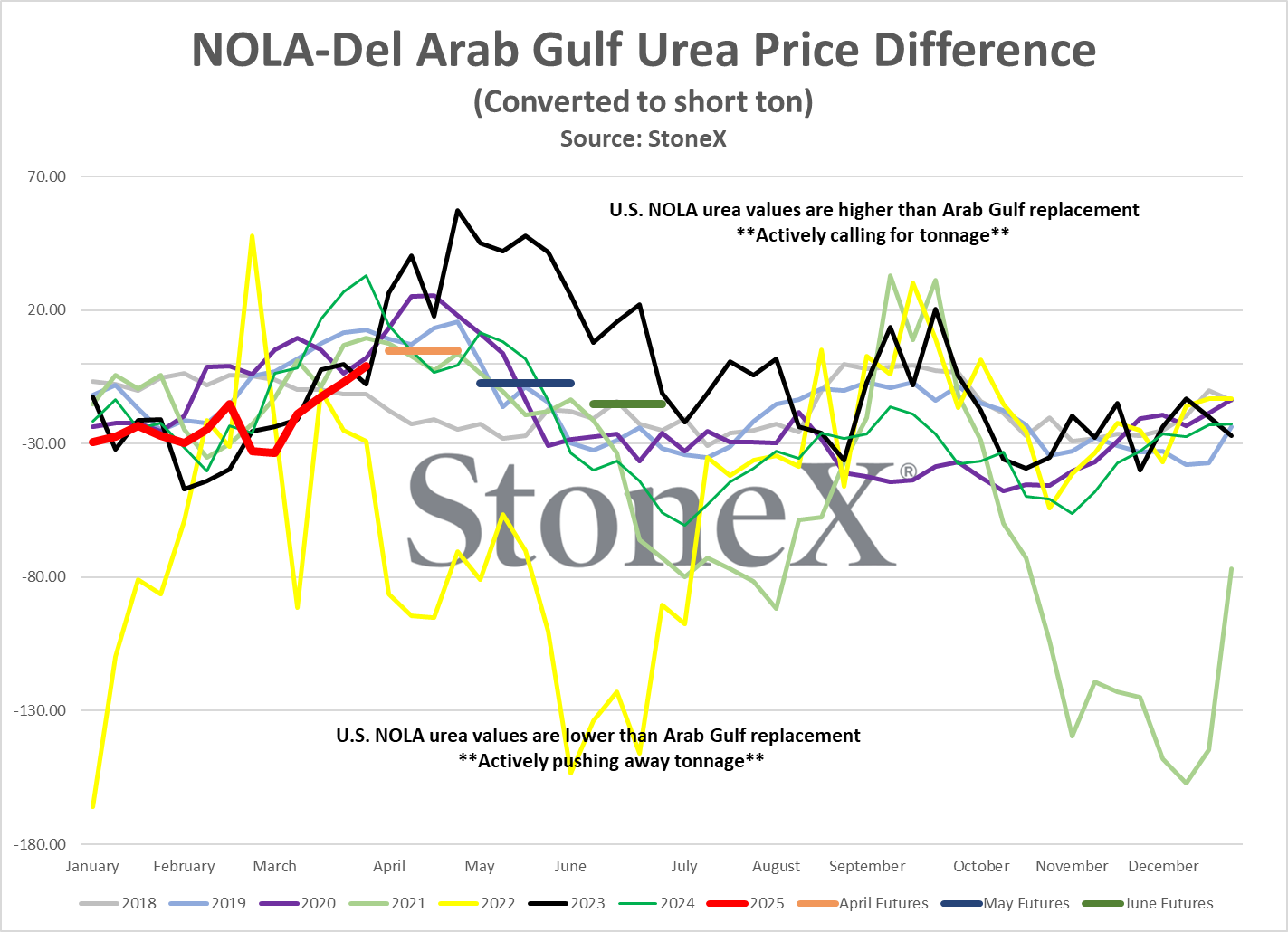

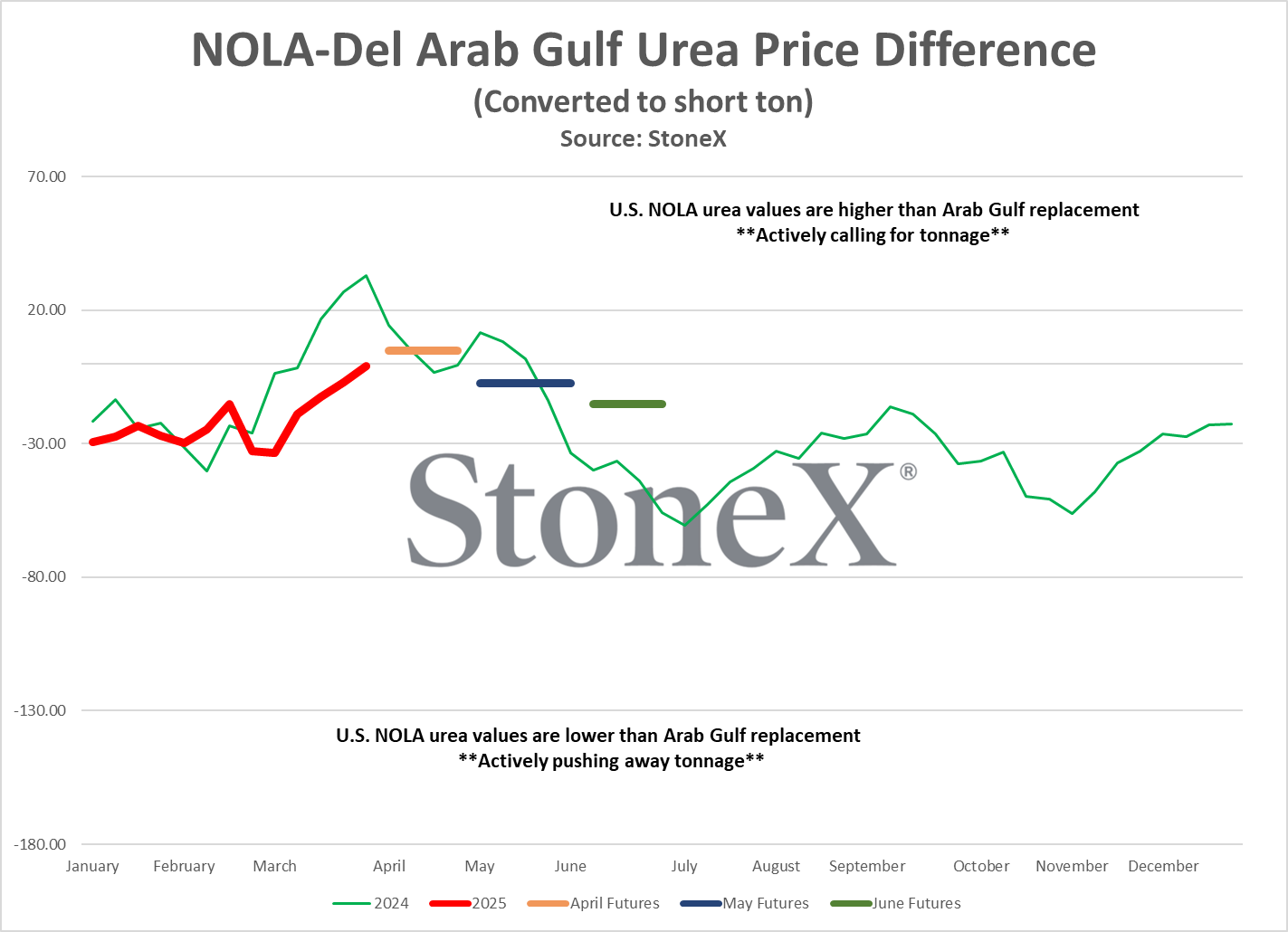

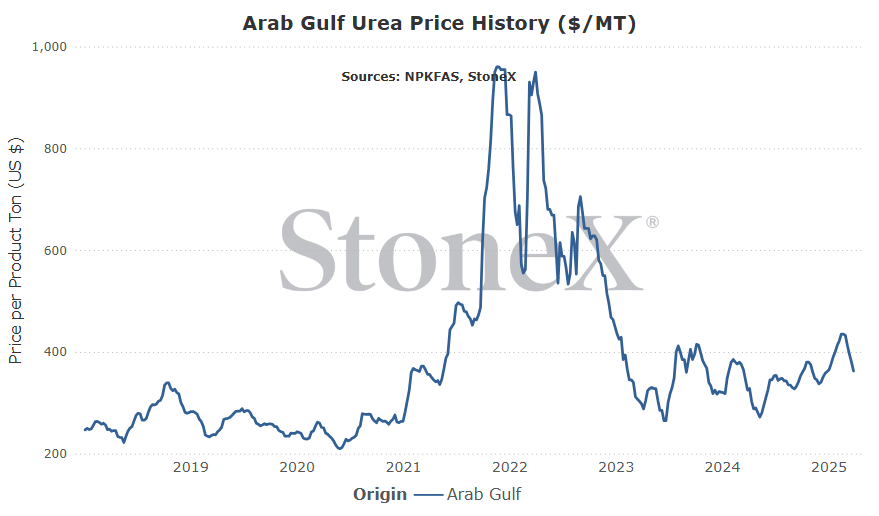

The intention of the below graphs are not to use to say "my price should be X based on this graph". These prices are derived from an FOB price point average. The intent is to show major global price movement trends. Your values will likely have significant basis difference (similar to your local grain price being different than the traded market price).

This graph is labeled as MT in USD currency.

What does this mean for farmers?

Long story short: more price support in the leadup to spring.

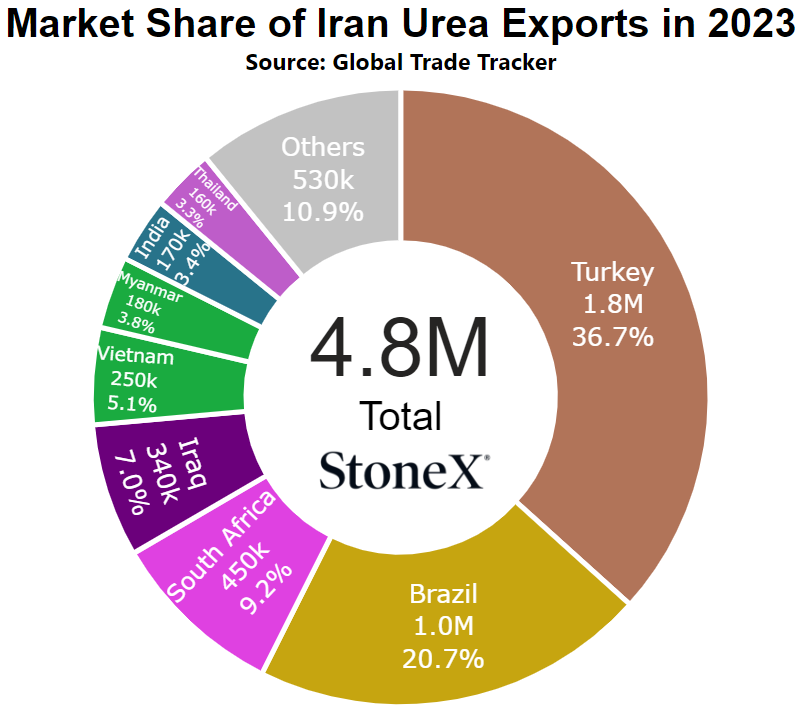

This was the hit that the global urea market didn't need. China feel 5M tons short on exports last year and started 2025 even lower. Europe continues to produce at 75% of normal which is around 3 - 3.5M tons per year that is missing. Losing another 750K tons of Iranian production isn't the help we needed to see prices lower.

Again, this does not mean prices cannot drop or be volatile (as has been the case). It does, however, raise the price floor a little more.

The global urea market does not have a lot of excess length due to all these issues so anytime something like Iran happens, it gets felt.

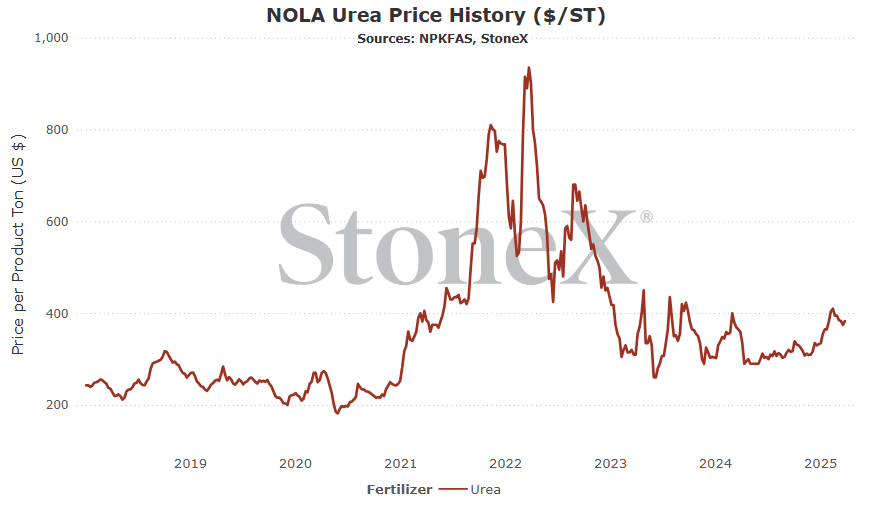

NOLA/New Orleans, Louisiana

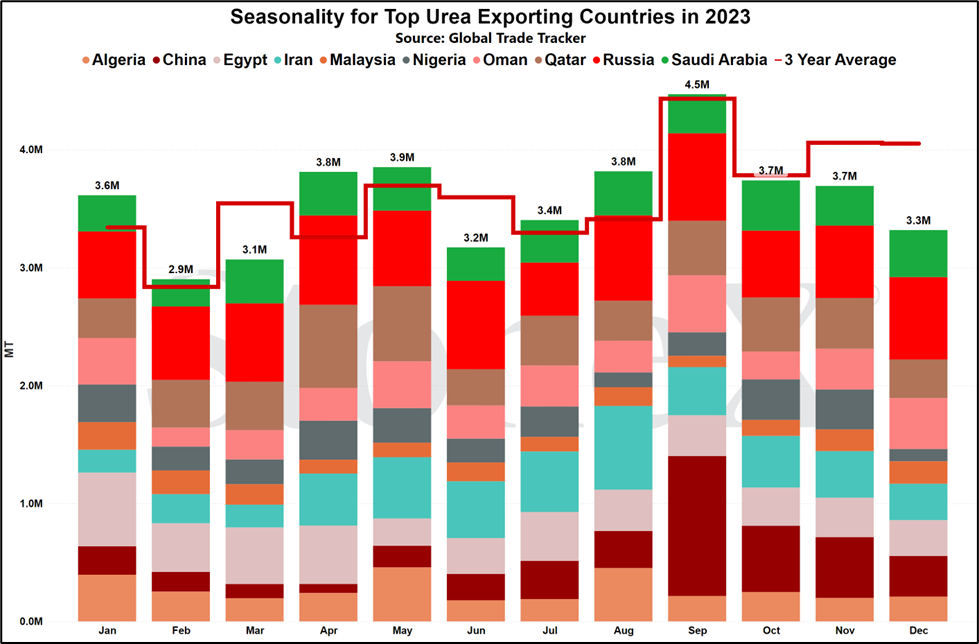

Number 3 global importer in 2022

Price comparisons

Vs 30 days ago - -3% or approximately $12 lower

Vs 90 days ago - 14% or approximately $48 higher

Vs 6 months ago - 21% or approximately $66 higher

Vs 1 year ago - 6% or approximately $23 higher

U.S. Midwest Average

Vs 30 days ago - -6% or approximately $31 lower

Vs 90 days ago - 16% or approximately $63 higher

Vs 6 months ago - 24% or approximately $90 higher

Vs 1 year ago - -2% or approximately $9 lower

U.S. Southern Plains Average

Vs 30 days ago - -3% or approximately $13 lower

Vs 90 days ago - 17% or approximately $68 higher

Vs 6 months ago - 24% or approximately $88 higher

Vs 1 year ago - -7% or approximately $35 lower

U.S. Northern Plains Average

Vs 30 days ago - -6% or approximately $31 lower

Vs 90 days ago - 9% or approximately $39 higher

Vs 6 months ago - 24% or approximately $87 higher

Vs 1 year ago - -3% or approximately $14 lower

Middle East

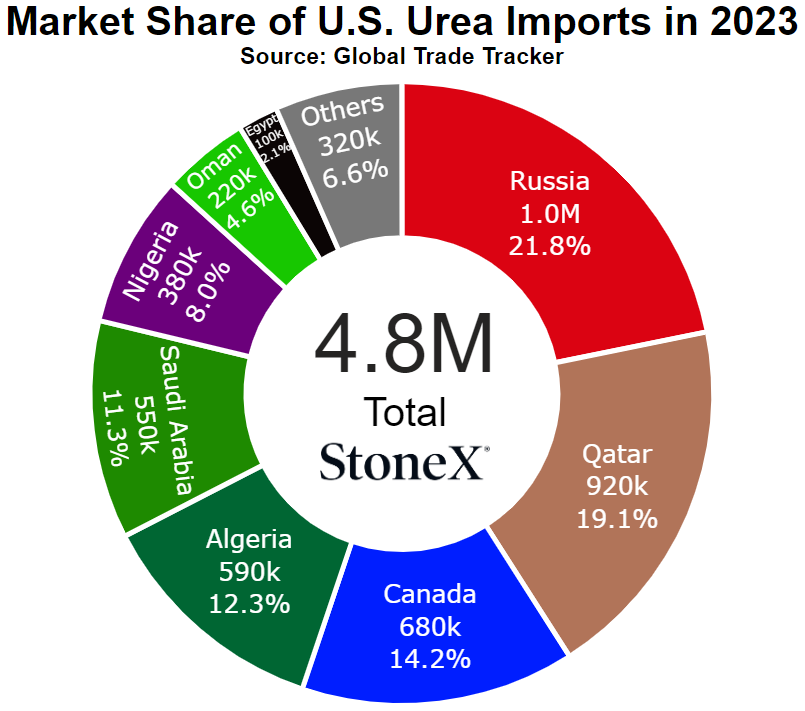

Number 1 exporter (as a region, not as individual nations)

Vs 30 days ago - -16% or approximately $70 lower

Vs 90 days ago - -1% or approximately $3 lower

Vs 6 months ago - 3% or approximately $10 higher

Vs 1 year ago - 12% or approximately $38 higher

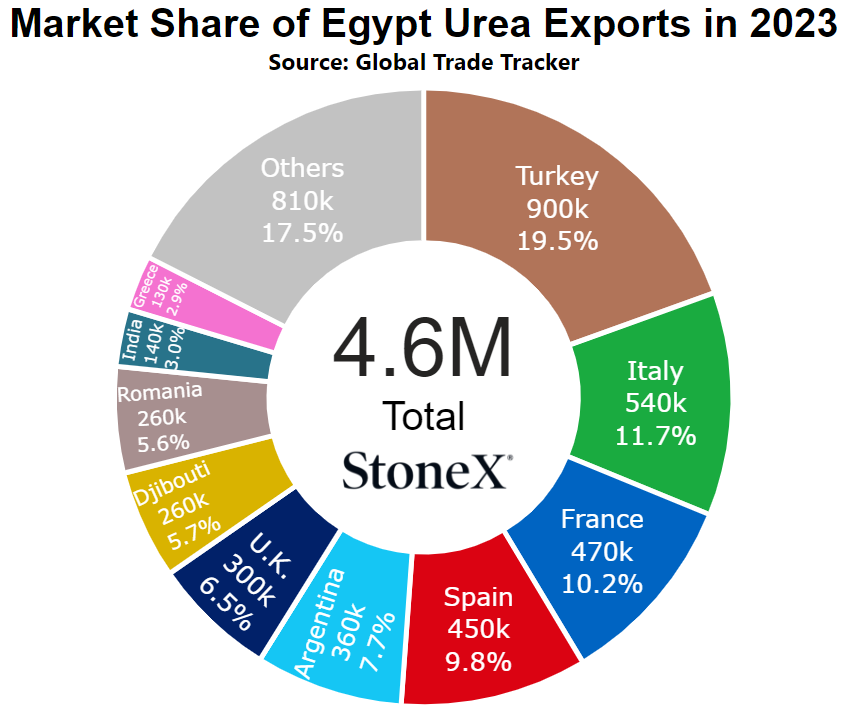

Egypt

Number 4 global exporter in 2022

Price comparisons

Vs 30 days ago - -20% or approximately $90 lower

Vs 90 days ago - -9% or approximately $37 lower

Vs 6 months ago - -1% or approximately $5 lower

Vs 1 year ago - 11% or approximately $37 higher

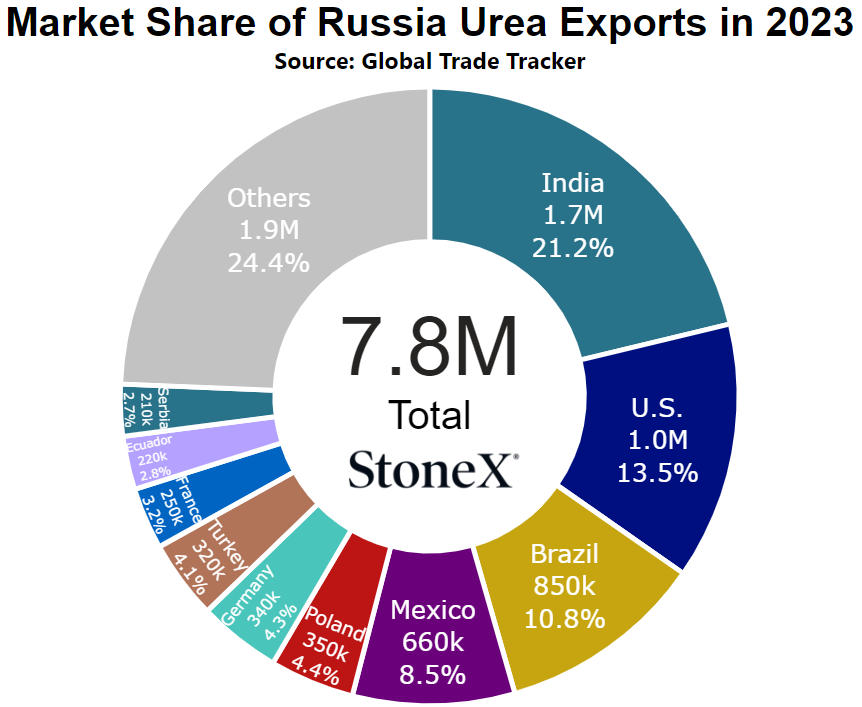

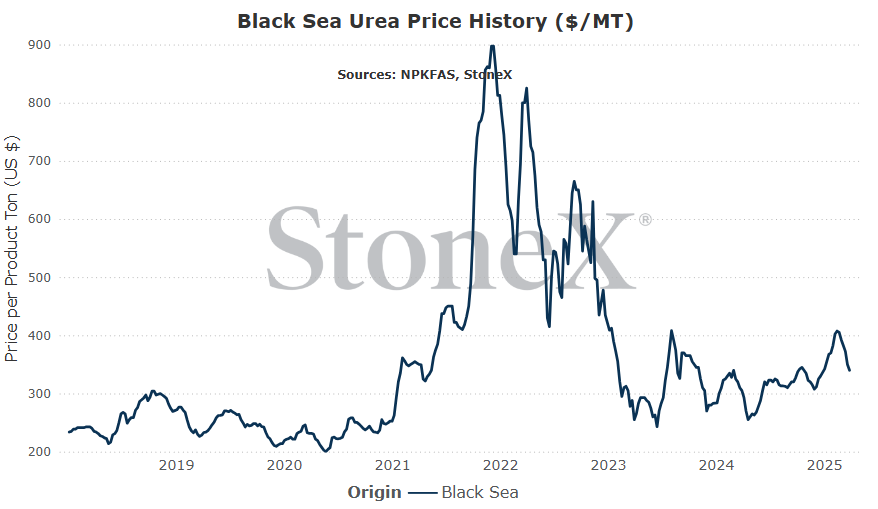

Black Sea

Number 1 global exporter in 2022

Price comparisons

Vs 30 days ago - -13% or approximately $53 lower

Vs 90 days ago - -1% or approximately $3 lower

Vs 6 months ago - 4% or approximately $13 higher

Vs 1 year ago - 11% or approximately $35 higher

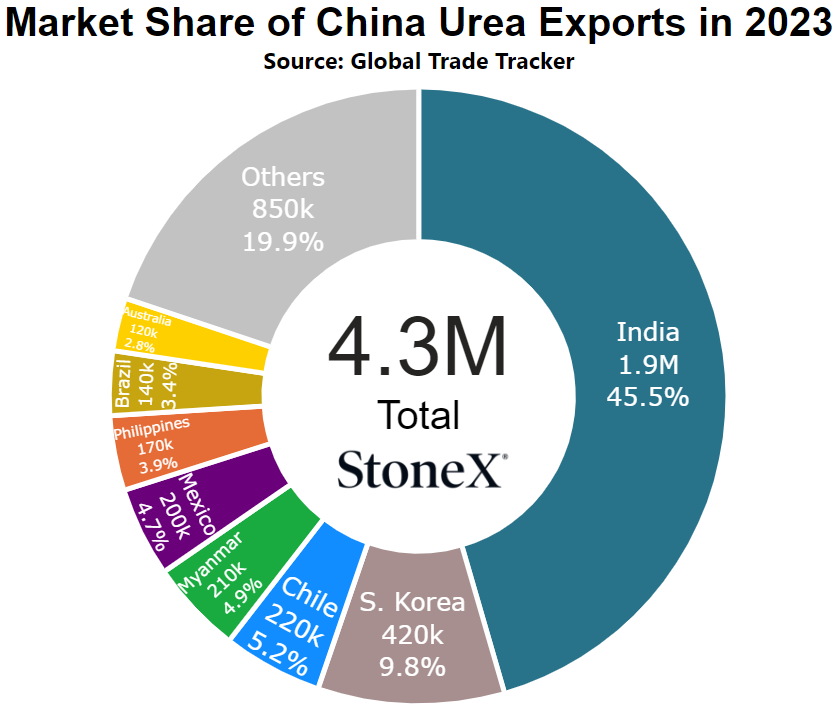

China

Number 9 global exporter in 2022

Price comparisons

Vs 30 days ago - 2% or approximately $6 higher

Vs 90 days ago - 14% or approximately $33 higher

Vs 6 months ago - 1% or approximately $2 higher

Vs 1 year ago - -17% or approximately $56 lower

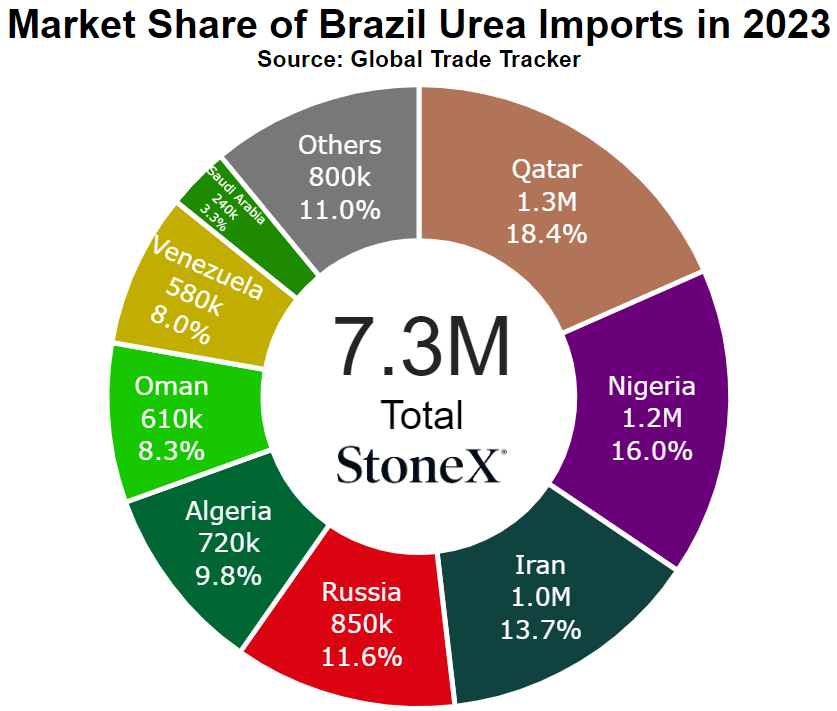

Brazil

Number 2 global importer in 2022

Price comparisons

Vs 30 days ago - -16% or approximately $68 lower

Vs 90 days ago - -2% or approximately $8 lower

Vs 6 months ago - -1% or approximately $5 lower

Vs 1 year ago - 6% or approximately $20 higher

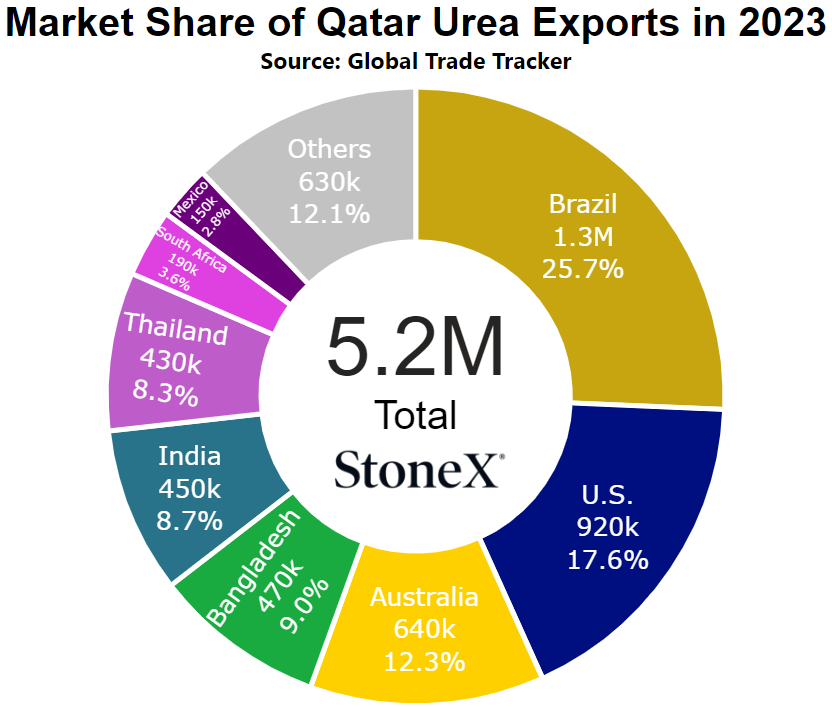

- India is met with other buyers/proud sellers - India took their sweet time with their purchase tender announcement, but that delay worked to their favor. Had they announced in mid-February as we previously believed, it would have been more fuel to the bullish fire. By delaying to now, their shipment window goes well into summer months and removes a lot of bullish potential. If other global buyers mostly stay away/quiet, it is likely this tender will not push prices higher. However, if buyers come from the woodwork, different story. That is one of the bigger things we are watching. Who follows India, if anyone.

- N.A. markets struggle with NH3 application/UAN supplies - there is a lot of nitrogen demand for the spring 2025 N.A. season. This is especially seen with U.S. corn acres continuing to rise. Now, if all 3 nitrogen products are decently supplied, then the boost to nitrogen demand for each isn't massive. However, if a larger area struggles with spring NH3 application, that can push a massive amount of nitrogen demand to urea. We are also watching/worried about UAN supplies with more production issues. This can also shove a lot of new nitrogen demand to urea which it wasn't expecting. Either of those happen, do not be surprised to see inventories tight and prices higher.

- Any further unexpected production outages - the world just got done withstanding almost 2 months of Iranian nitrogen production being offline. This, in combination with a lack of Chinese exports and continued European production issues, made an already tight global urea S&D that much tighter. Hopefully, Iran will be the last surprise...but there are no guarantees. The global S&D is racing on the edge of a razor. Any little push to further reduce supplies will have an impact.

- Chinese exports return/rumor to return - China continues to be a huge reason why global urea values are as high as they are. They historically represent 10% of the global export market at 5 to 5.5M tons per year. In 2024, they only exported 266K tons and 2025 has started WELL below that pace. However, you can never count China out. There have been rumors that the government will revisit export programs. This may be a full return with free market fundamentals driving it (not likely). This might be a quantity ceiling. This might be a short timeframe. Each scenario would play out differently but each would likely cause values to dip on their return...if it happens.

- N.A. imports continue at a heavy pace - imports of urea to N.A. have been surprisingly high. NOLA values have been well below global comparisons meaning international producers have been willing to take discounts to send product here. This is certainly not something we saw coming. If the import pace continues well above expectations, that keeps a lid on price ideas. If imports pick up the pace, it could shove price ideas lower.

- India shocks the world and delays this tender - with the way India delayed their tender and the fact that their next application season is coming quickly, this is not a very high expectation...but we have been surprised before. IPL, India's importing agency for this tender, announced their desire to secure 1.5M tons. We could see them get upset with high offers and decide to scale back the number of tons they secure. We could see them decide to try the tender again. Any form of this would likely gut the global urea market and send prices lower.

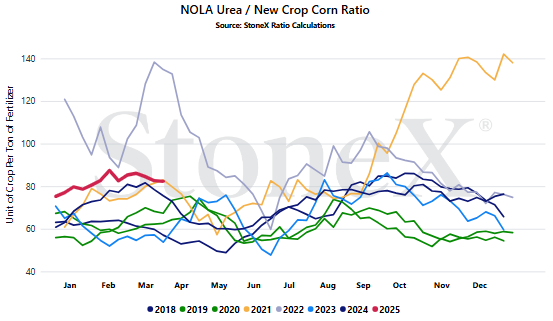

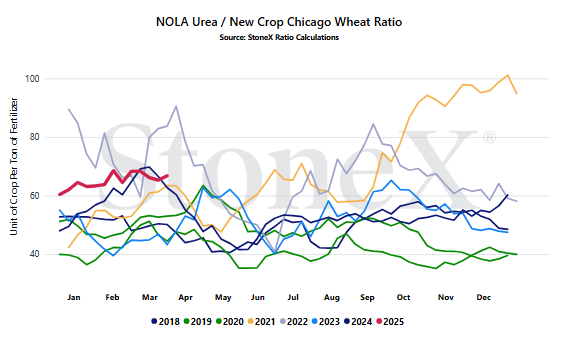

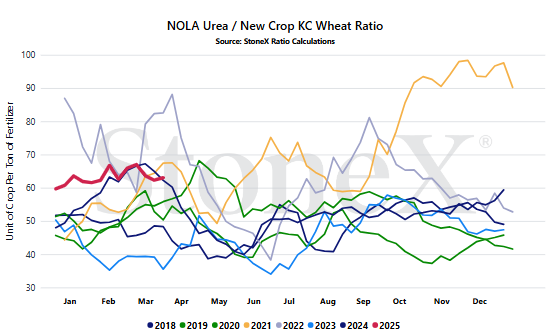

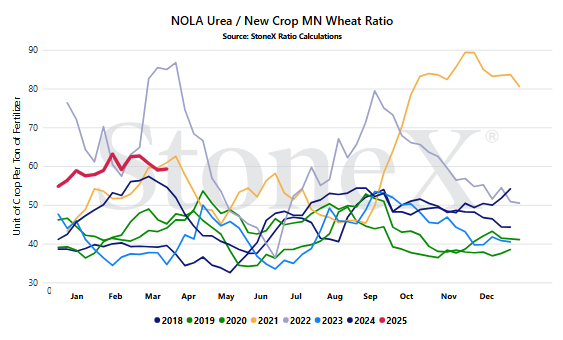

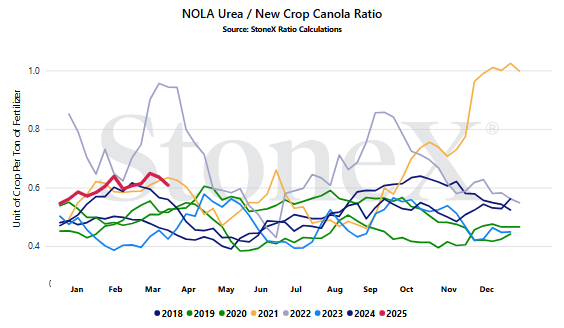

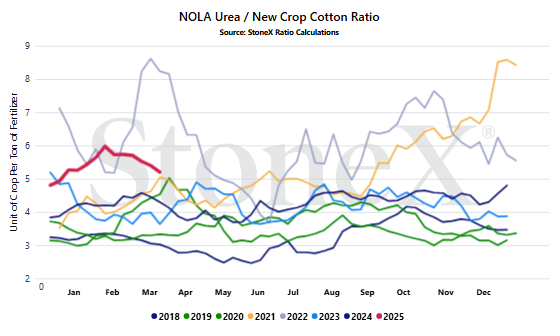

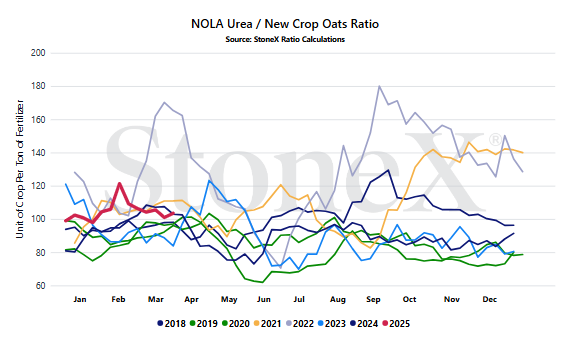

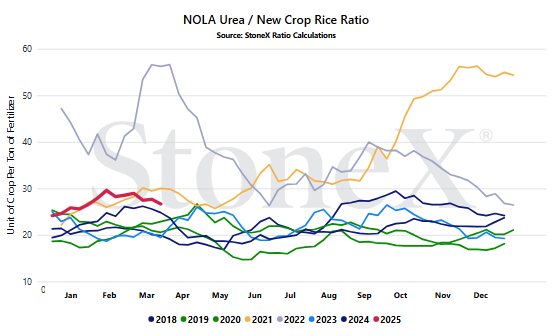

We believe that only looking at the flat price of either grains or fertilizer can be misleading:

- Only selling grain can hurt you if fertilizer prices rise substantially

- Only buying fertilizer can hurt you if grain prices fall

We look at the ratio "value" to get a better indication of where we are or how many bushels of X does it take to pay for 1 ton of fertilizer.

Would you rather:

- Spend 135 bushels to pay for 1 ton of urea

- Spend 55 bushels to pay for 1 ton of urea

When we compare the current ratio value against recent years, we start to see if we are high or low.

YOUR VALUES WILL LOOK DIFFERENT

This graph looks at the NOLA urea price vs the flat grain price. There are no logistics on either product. Your location will look different due to fertilizer logistical costs, grain basis, etc.

- Chinese governments export policies - a large reason why global and domestic prices are as high as they is due to Chinese urea export restrictions. China typically represents around 10% of the global export marketplace and 2024 saw them reduced to just over 260K tons. January/February 2025 export data pace makes 2024 look huge in comparison. More worrisome is that there continues to be rumors that this will become a more permanent strategy where tons, if exported, are done on a defined quantity and a defined period. As long as China isolates itself, global farmers will pay a higher price.

- Whether Russia/Ukraine peace leads to lower European gas values - the new U.S. administration continues to push hard for peace between Russia and Ukraine. There is a lot of hope that if this is successful, it will mean a return to "normal" relations between Europe and Russia. Now, whether it will or will not remains to be seen but peace certainly wouldn't hurt. In the best case scenario, peace is found, relations between Europe and Russia return, work starts to repair the Nordstream pipeline which was attacked during the early days, and eventually cheap Russian gas returns to Europe which will allow European based nitrogen production to return to near normal levels. That sentence was 3+ lines long which should give you an idea of how long this would take to play out. It is not a short term event, rather a longer term hope. If European production can return, global prices can mellow out even further.

- How long can buyers stay out, will it be a windfall when they return - the biggest surprise of 2025 has been how well global buyers have been able to stay out. This story has really been focused on India who was WIDELY expected to announce a purchase tender in mid-February. Since then, global buyers have taken India's approach and drug their feet as well...but for how long? If India steps in, will others take that as a sign of a near term price floor and purchase as well? Can there be enough demand at this point in the calendar to support values? I'm losing faith by the day. I think we are simply too close to summer, but we will see.

- Weaker global markets vs rising domestic demand - this will be a frustration for many. Global values and even some along the coastlines have been falling...yet inland prices have been stagnant. It takes time for those cheaper tons to arrive, but it does paint a more promising picture for sidedress periods. This is not something I would have expected to see as a possibility a month or two earlier.

StoneX Ratio Calculation

The ratio calculation is derived from Bloomberg historical grains values as well as fertilizer values from StoneX, NPKFAS, and Argus.

The calculation is simply dividing the fertilizer price by each grain price.

All data was sourced from StoneX unless otherwise noted.