Gold 2026 Outlook: What to Expect After a Huge 2025

By: Fawad Razaqzada, Market Analyst

Gold is starting 2026 after ending one of its strongest years on record. Fuelled by aggressive central bank buying, a global interest rate cutting cycle and elevated safe-haven demand, the metal ended 2025 nearly 65% better off, posting its fifth consecutive monthly gain in December as well as a hat-trick of positive annual returns. The key question now is whether gold can hold on to those gains as we move through 2026. While the metal has made a positive start to the year and the long-term bullish case remains intact, meaning selling gold aggressively is still difficult to justify, the macro backdrop looks more finely balanced this year than last. Central bank demand may not be as relentless at elevated prices, much of the global easing cycle may already be priced in, bond yields remain high, and easing geopolitical tensions could gradually reduce gold’s safe-haven appeal. As a result, 2026 may not be super bullish for gold, and the metal could be heading for a long-overdue consolidation rather than a repeat of 2025’s explosive rally.

Gold 2026 outlook: A potentially hawkish year for central banks

Gold has enjoyed a remarkable run in 2025, rising about 65% on the year. The metal surged higher at the start of the year, pausing for breather during the summer months, before extending the rally in the second half of the year. Some bullish momentum was lost in mid-October after the metal hit a record peak of $4381. The metal then bounced back heading into the final weeks of 2025, before breaking out to a new record above $4,500, where the rally faltered in the closing days of December. But that wasn’t enough to prevent the metal making another positive return on the month.

After such a powerful rally in 2025, that caused the already-overbought prices to get even more stretched, we are not expecting gold to make any groundbreaking gains in 2026. Granted, the metal may go on to achieve that $5K hurdle, which would point to a further roughly 10% upside above the December’s high, the macro backdrop may not be as welcoming for gold as has been the case in 2025 and earlier. Indeed, the list of reasons why the rally could start to cool is growing steadily. We are alert to the possibility of a short-term reversal — but only when the charts confirm. More on this in the technical analysis section of this gold 2026 outlook guide.

After the Fed and most other central banks trimmed rates in 2025 as inflation eased, expectations for further policy easing have fallen sharpy. For some central banks, one or two additional cuts might be forthcoming. For others, a long pause or even a hike in interest rates may may well be the case in 2026. The Bank of Japan has indicated that it needs to further normalise it monetary policy while central banks in Australia, New Zealand and Canada, among others, have signalled the end of their easing cycles. The European Central Bank has turned neutral amid mild improvement in data and Germany’s big fiscal stimulus, while the fallout from Trump’s tariffs haven’t been as bad as feared.

If the broad global policy narrative shifts towards gradual tightening or at least “less easing” in 2026, it becomes far harder for gold to extend its rally without fresh catalysts.

Will central banks continue to buy gold?

Much of gold’s strength in recent times has been driven by strong central-bank demand — especially from China. The country’s role remains pivotal shaping the gold 2026 outlook. Will the PBOC and other central banks continue to purchase gold at these elevated prices?

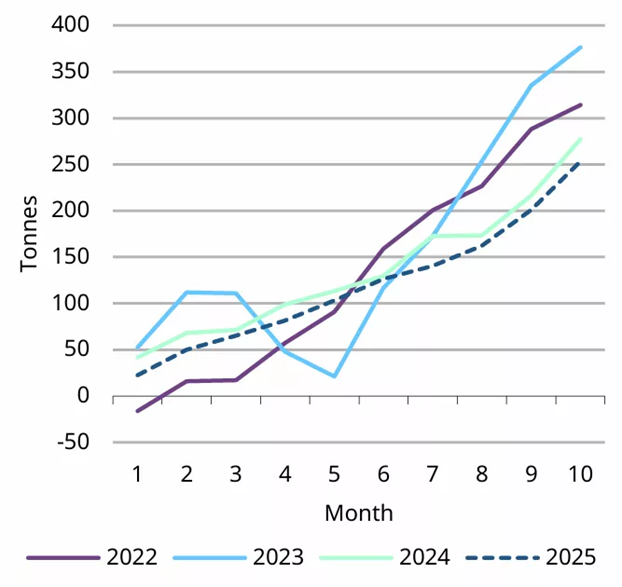

Chart 1: Central bank gold buying

Source: World Gold Council

According to the World Gold Council, central bank demand for gold totalled 53 tonnes in October 2025, which was +36% m/m increase. Central bank buying has been strong throughout the year as per the above chart. It hasn’t just been the PBOC, but in October, buying remained concentrated among a small number of central banks, led by the National Bank of Poland.

However, the pace of central bank buying in 2025 was slower compared to the previous few years, no doubt due to the significantly higher prices.

Chart 2: Central bank gold buying trend

Source: World Gold Council

While purchases ramped up from the National Bank of Poland (83t), Kazakhstan (41t) and most other emerging-market central banks, People’s Bank of China has slowed down its purchases.

If the PBOC further tempers its buying at these elevated price levels, leveraged positions could unwind quickly on realisation of cooling Chinese demand. Indeed, we have already seen several central banks reducing their gold reserves in 2025, including those in Singapore and Uzbekistan. At some point, the opportunity to make a handsome profit will be too tempting to ignore.

What other factors could undermine the rally?

Much of gold’s strength in recent times has been driven by familiar factors: geopolitical uncertainty around Russia and Ukraine, ongoing discussion about de-dollarisation, and consistently strong central-bank demand. These factors have acted as reliable supports throughout 2025. But once you strip them back, the rally is arguably running a little thin on new fuel. For the gold 2026 outlook, this raises an important question: how much upside is left?

From a geopolitical front, there were glimmers of risks easing up until the first week of January: slow-moving peace conversations in Ukraine, a ceasefire in Gaza, and more stable trade relations between Washington and Beijing. In theory, each of these should trim gold’s safe-haven demand, yet the metal has barely reacted. Granted, some of this has been due to the recent tensions between the US and Venezuela which took a dramatic turn with the capture of Nicolás Maduro. Whether this will keep gold’s haven appeal supported in the slightly longer run remains to be seen.

Meanwhile, the softer US dollar throughout 2025 helped maintain a floor, but it remains to be seen how much further the dollar selling will continue, especially if there is a supply side shock that boosts inflation again – for example from oil prices. Japan may well be another wildcard. Rising JGB yields, driven by expectations of policy normalisation by the BoJ, may spark concerns about the unwinding of the carry trade, hurting all sorts of leveraged positions including precious metals. Yet this hadn’t been the case in 2025, with the USD/JPY rising above 155.00 handle, threatening to push even higher.

In summary

In 2026, the gold outlook is far more finely balanced. While the bullish case is likely to remain intact in as far as the long-term is concerned, some of the factors that pushed gold to repeated all-time highs may become less dominant. Central bank buying, the direction of global bond yields, and how much easing is truly left in the pipeline will matter more than ever. With geopolitical risks (outside of Venezuela) showing signs of stabilising and real yields remaining elevated, gold may need fresh catalysts to extend its rally. In short, the trend is still constructive, but after such an exceptional run, the margin for disappointment is growing and the risk of a corrective phase in 2026 should not be underestimated.

Much of the additional gold purchases we saw beyond those driven by macro factors were undoubtedly driven by speculative interest in 2025 with traders looking to take advantage of a strong bullish trend. Will that continue in 2026 remains to be seen, but the technical trend was unambiguously still bullish at the start of the year.

Gold 2026 outlook: Technical levels that matter

While momentum indicators continued to signal ‘overbought’ as they have done throughout 2025, until such a time we see a bearish reversal, there is no point in entertaining the idea of shorting gold aggressively. Granted, counter-trend trades will present themselves here and there, but if those higher highs and higher lows are not violated, the path of least resistance will remain to the upside.

Source: TradingView.com

With gold breaking to above $4,550, clearing the old high at $4,381, we now have a short-term level to watch as potential support. This $4,381 level was the high made in October, before it finally gave way during the December rally. Below that, there are a few other short-term levels to watch too, including $4250, $4200 and $4100. But that $4K hurdle is the key support now and the line in the sand, as a break back below it could be significant for the gold 2026 outlook from a technical perspective. Below $4K, there is a trend line that comes in somewhere between this psychological hurdle and the next big level at $3500.

In terms of resistance, well there wasn’t much with prices at record highs. If we move above $4,500 again, keep an eye on the next round handles such as $4,600, $4,700 and so on. Even if we see a mini shakeout, for as long as the series of higher highs and higher lows remain intact, I wouldn’t rule out the possibility of gold potentially reaching $5,000 next. However, in the event we witness a clear reversal signal, that’s when we will proactively start looking for bearish opportunities in gold. So do keep an eye out for our daily gold analysis content.

The bigger picture for gold in 2026

Taken together, the gold 2026 outlook is a balancing act. On one side sit geopolitical risks, central-bank demand and the ever-present possibility of market turbulence — all supportive of gold. On the other sit elevated global yields, the potential end of the monetary easing cycle, and the risk of China stepping back from adding to its reserves. Gold may well remain elevated, but sustaining further gains from here will require either a fresh geopolitical jolt or a clear dovish shift in global rate expectations — neither of which is guaranteed.

So, as we look ahead to 2026, the gold outlook is far more finely balanced than in 2025. The longer-term bullish case remains intact and there’s still little incentive to be aggressively bearish, but the tailwinds that powered gold through 2025 may not blow as strongly. Central bank demand, the direction of global yields, and how much easing is truly left in the pipeline will matter more than ever. With some of the geopolitical risks showing signs of stabilising and real yields remaining elevated, gold may need fresh catalysts to extend its rally. In short, the trend is still constructive, but after such an exceptional run, the margin for disappointment is growing and the risk of a corrective phase in 2026 should not be underestimated.

Global Macro

This material should be construed as market commentary and represents the opinions and viewpoints of the author, and does not reflect tailored advice associated with any specific account.

The views are current only through the date stated and are subject to change at any time based upon market or other conditions, and StoneX Group Inc. (“SGI”) disclaims any responsibility to update such views. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources. Past performance does not guarantee future results.

The StoneX Group Inc. group of companies provides financial services worldwide through its subsidiaries, including physical commodities, securities, exchange-traded and over-the-counter derivatives, risk management, global payments and foreign exchange products in accordance with applicable law in the jurisdictions where services are provided.

References to certain OTC products or swaps are made on behalf of StoneX Markets, LLC (SXM), a member of the National Futures Association (NFA) and provisionally registered with the U.S. Commodity Futures Trading Commission (CFTC) as a swap dealer. SXM’s products are designed only for individuals or firms who qualify under CFTC rules as an ‘Eligible Contract Participant’ and who have been accepted as customers of SXM.

StoneX Financial Inc. (SFI) is a member of FINRA/NFA/SIPC and registered with the MSRB. SFI is registered with the U.S. Securities and Exchange Commission (SEC) as a Broker-Dealer and with the CFTC as a Futures Commission Merchant and Commodity Trading Advisor. StoneX Financial (Canada) Inc. (SFCI) is registered in Canada and is a member of CIRO and CIPF. References to certain securities trading are made on behalf of the BD Division of SFI and are intended only for an audience of institutional clients as defined by FINRA Rule 4512(c). References to certain exchange-traded futures and options are made on behalf of the FCM Division of SFI. Wealth Management is offered through SA Stone Wealth Management Inc., member FINRA/SIPC, and SA Stone Investment Advisors Inc., an SEC-registered investment advisor, both wholly owned subsidiaries of SGI.

R.J. O’Brien & Associates, LLC (RJO) is registered with the CFTC as a Futures Commission Merchant and is a member of NFA.

StoneX Financial Ltd (SFL) is registered in England and Wales, company no. 5616586. SFL is authorized and regulated by the Financial Conduct Authority (FCA) (registration number FRN:446717) to provide services to professional and eligible customers including: arrangement, execution and, where required, clearing derivative transactions in exchange traded futures and options. SFL is also authorized to engage in the arrangement and execution of transactions in certain OTC products, certain securities trading, precious metals trading and payment services to eligible customers. SFL is authorized and regulated by the FCA under the Payment Services Regulations 2017 for the provision of payment services. SFL is a category 1 ring-dealing member of the London Metal Exchange. In addition SFL also engages in other physically delivered commodities business and other general business activities which are unregulated and not required to be authorized by the FCA.

This communication is issued in the European Economic Area by StoneX Financial Europe GmbH (SFEG). StoneX is the trade name used by STONEX GROUP INC. and all its associated entities and subsidiaries. StoneX Financial Europe GmbH (“SFEG”) is a securities trading firm registered in Germany under Company No. HRB 80844.

StoneX APAC Pte. Ltd. (“SAP”) (Co. Reg. No 200616676W) is regulated as a Dealer (PS20190001002) under the Precious Stones and Precious Metals (Prevention of Money Laundering and Terrorism Financing) Act 2019 for purposes of anti-money laundering and countering the financing of terrorism. SAP is an “Approved International Trading Company” authorized to act as a “Spot Commodity Broker” under the Commodity Trading Act.

StoneX Financial Pte Ltd (Co. Reg. No 201130598R) (“SFP”) is regulated by the Monetary Authority of Singapore and is a Capital Markets Service Licence holder (for dealing in capital market products), an Exempt Financial Adviser (for advising on investment products and issuing or promulgating analyses/ reports on investment products) and a Major Payment Institution (for domestic and cross-border money transfer services).

SFP may distribute analysis/report produced by its respective foreign affiliates within the StoneX Group of companies pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations Recipients should contact SFP at (65) 6309 1000 for any matters arising from, or in connection with, this webinar.

StoneX APAC Pte. Ltd. (“SAP”) (Co. Reg. No 200616676W) is regulated as a Dealer (PS20190001002) under the Precious Stones and Precious Metals (Prevention of Money Laundering and Terrorism Financing) Act 2019 for purposes of anti-money laundering and countering the financing of terrorism.

StoneX Financial (HK) Limited (CE No.: BCQ152) (“SHK”) is regulated by the Hong Kong Securities and Futures Commission for Dealing in Securities and Dealing in Futures Contracts.

StoneX Financial Pty Ltd (ACN 141 774 727) holds an Australian Financial Service License (AFSL: 345646) for Dealing in Securities, Exchange-Traded Derivatives Contracts, OTC Derivatives Contracts and Foreign Exchange Contracts, and is regulated by the Australian Securities and Investments Commission.

StoneX Securities Co., Ltd. (“SSJ”) (Co. Reg. No 010401047199) is regulated by the Japanese Financial Services Agency as a Type-I Financial Instruments Business Operator (Kanto Local Finance Bureau (FIBO)No.291’), is a member of the Financial Futures Association of Japan for dealing and broking FX and FX Option transactions, and is a member of the Japan Securities Dealers Association for dealing and broking stock indices and option transactions.

Trading swaps and over-the-counter derivatives, exchange-traded derivatives and options and securities involves substantial risk and is not suitable for all investors. Past performance of any futures or option is not indicative of future success. Indicators are not a trading system and are not published as a specific trade recommendation. The information herein is not a recommendation to trade nor investment research or an offer to buy or sell any derivative or security. It does not take into account your particular investment objectives, financial situation or needs and does not create a binding obligation on any of the StoneX group of companies to enter into any transaction with you. You are advised to perform an independent investigation of any transaction to determine whether any transaction is suitable for you. No part of this material may be copied, photocopied or duplicated in any form by any means or redistributed without the prior written consent of StoneX Group Inc.

The report/analysis herein is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

Our market expertise, advanced platforms, global reach, culture of full transparency and commitment to our clients’ success all set us apart in the financial marketplace.

Reach

With access to 40+ derivatives exchanges, 180+ foreign exchange markets, nearly every global securities marketplace and numerous bi-lateral liquidity venues, StoneX’s digital network and deep relationships can take clients anywhere they want to go.

Transparency

As a publicly traded company meeting the highest standards of regulatory compliance in the markets we serve, our financials and record of accomplishment are matters of public record. StoneX’s commitment to “doing the right thing over the easy thing” sets us apart in the industry and helps us build respect, client trust and new partnerships.

Expertise

From our proprietary Market Intelligence platform, to “boots on the ground” expertise from award-winning traders and professionals, we connect our clients directly to actionable insights they can use to make more informed decisions and achieve their goals in the global markets.