For anyone that was hoping for a phosphate miracle in the form of Chinese exports returning...sorry.

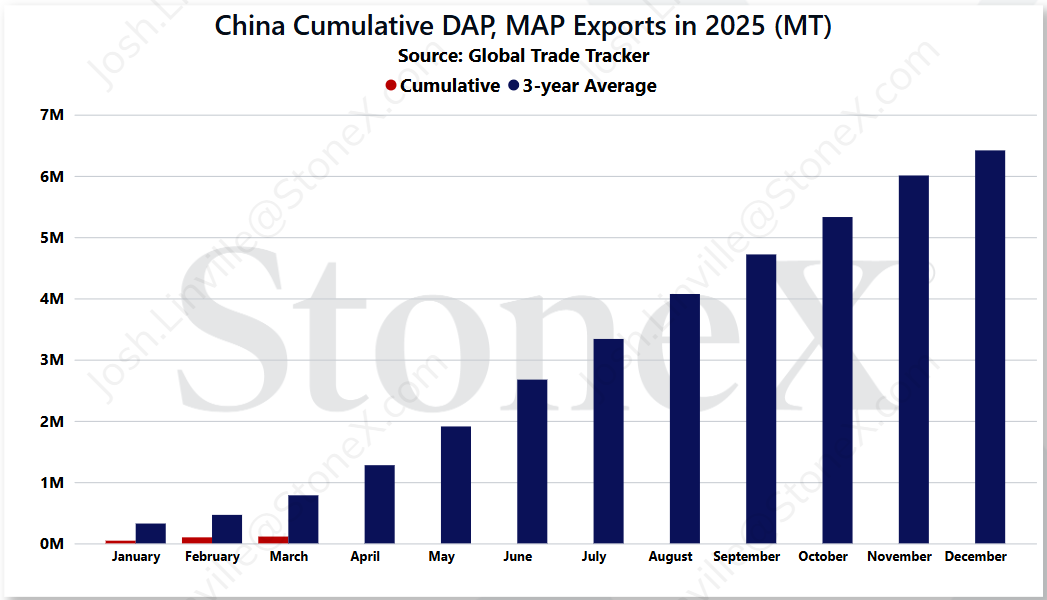

China's March export data showed another disappointing month. DAP/MAP exports barely got over 111K tons. How does this measure? The current 3-year average March cumulative total is just under 785K tons...but that is deceiving. If we go back to normal times (2021/22), the 3-year average thru March was 1.3M.

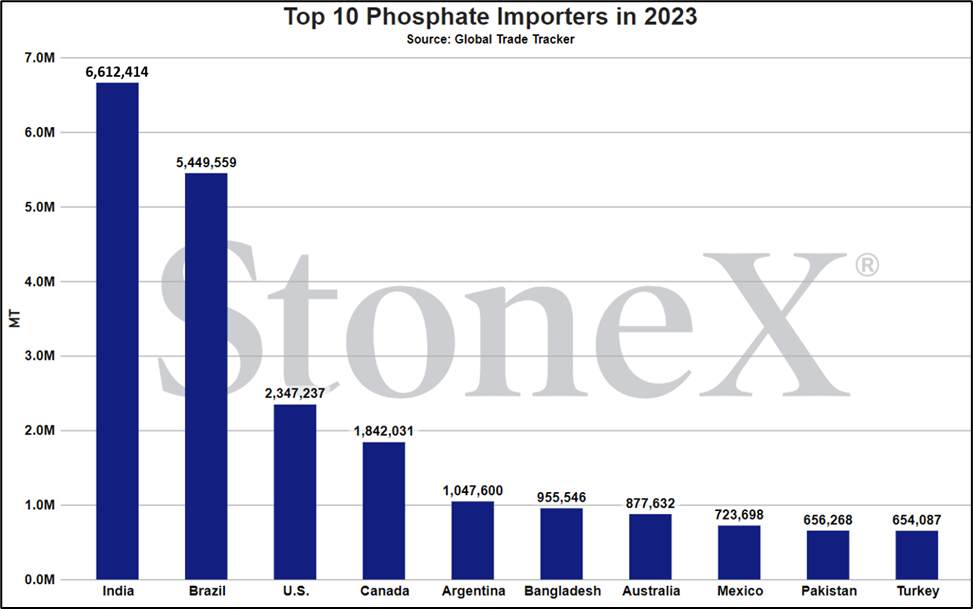

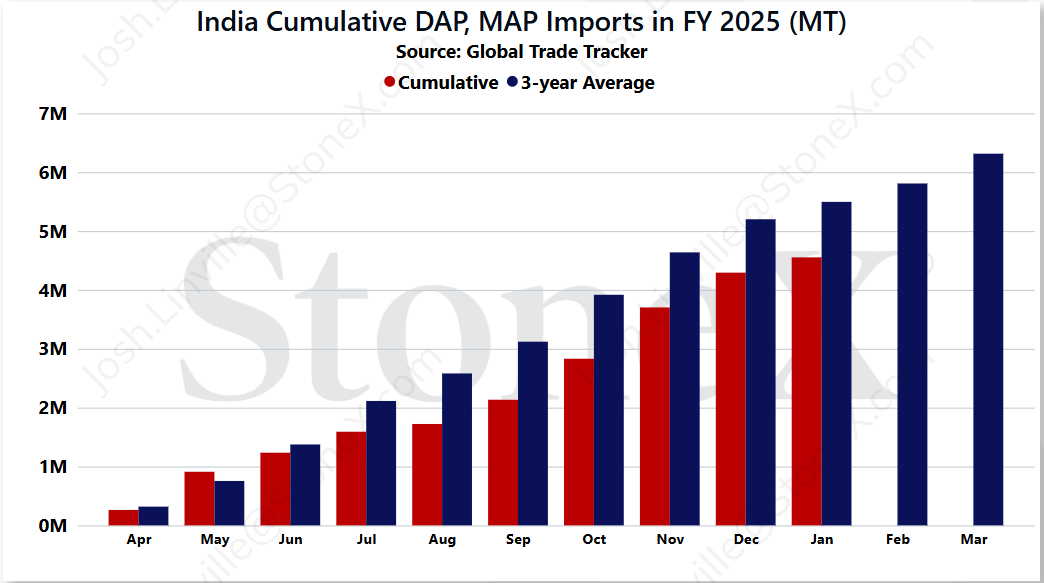

On the demand side, India is still struggling with today's new normal of tight global supplies. They continue to try and persuade the market with tactics that used to work but in today's world, have much less impact. As a result, stockpiles continue to be much lower than normal which means the largest global buyer is still in catch up mode.

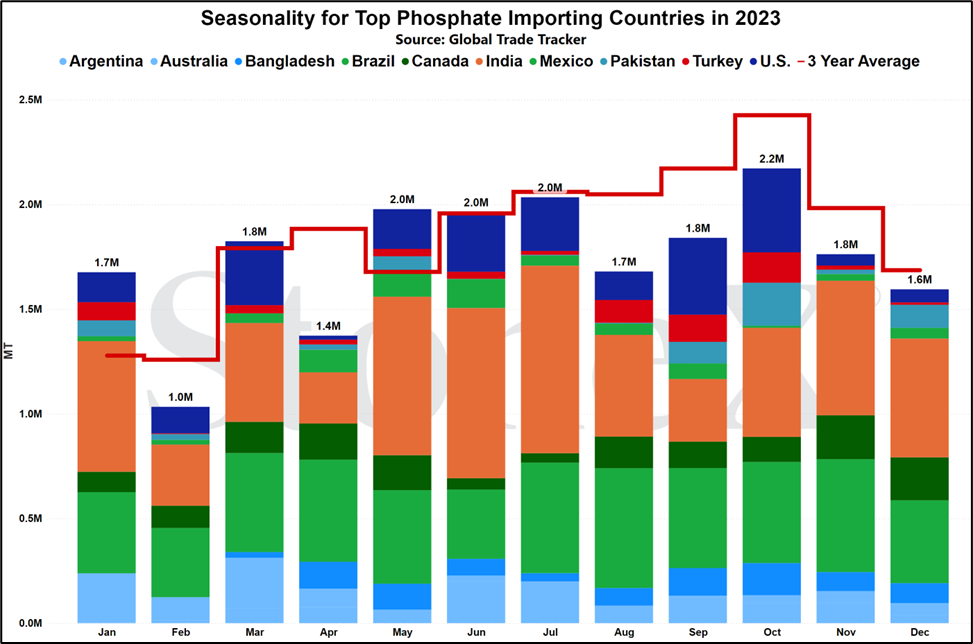

What does all of this mean? Normally, as the world heads into the summer months (for the Northern Hemisphere), global phosphate values fall to near their annual low's. This year so far appears to be bucking that trend.

Assuming Chinese exports remain low and India continues to buy at a frantic pace, it is hard to see values falling. The biggest bearish factor is how global buyers will react to the current extreme high price...but for some they have few options. This is a dream world for manufacturers.

List of new global production continues to grow

"Low prices cure low prices and high prices cure high prices."

From my early days in the fertilizer markets, this was a tried and true golden rule of not only fertilizer but markets in general.

When prices fall to very low prices, the market corrects itself. The highest cost manufacturers struggle as they are either barely breaking even or are losing money. The common response is to slow/stop production. Why continue if the market forces are creating a loss for your operation. The drop in supply eventually causes market values to rise.

The opposite holds true for the higher side...albeit at a slower pace. A very high price causes current market participants or new market entrants to create more supply either in the form of higher production rates or new production lines.

It appears that phosphate is going the route of more production to solve high prices.

There has been a growing list of rumored/announced new production lines in the world of phosphate:

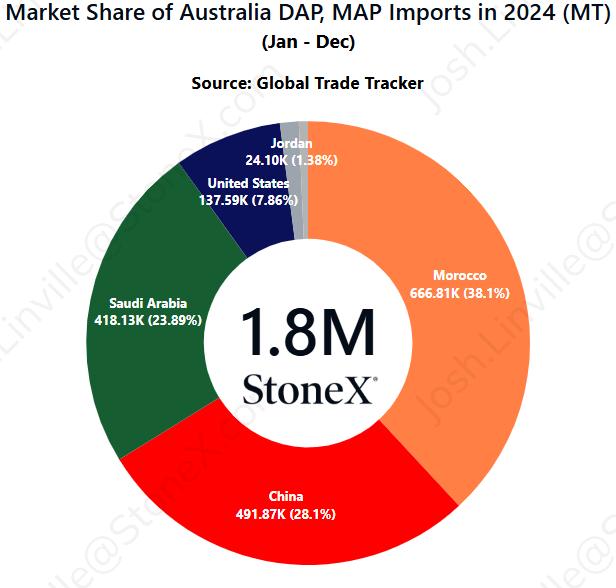

- Australia - a firm appears to be moving forward with a new mining/production facility that would add approximately 1M tons of phosphate per year. Likely these tons stay home in Australia, but still benefits the world by reducing their import needs.

- Morocco - OCP, Morocco's phosphate production company, is proceeding with new lines that will focus on TSP. This is a much less popular product globally...but is still phosphate. If OCP can build new demand for TSP, that will reduce those areas demand for DAP/MAP, freeing up that product for other global buyers.

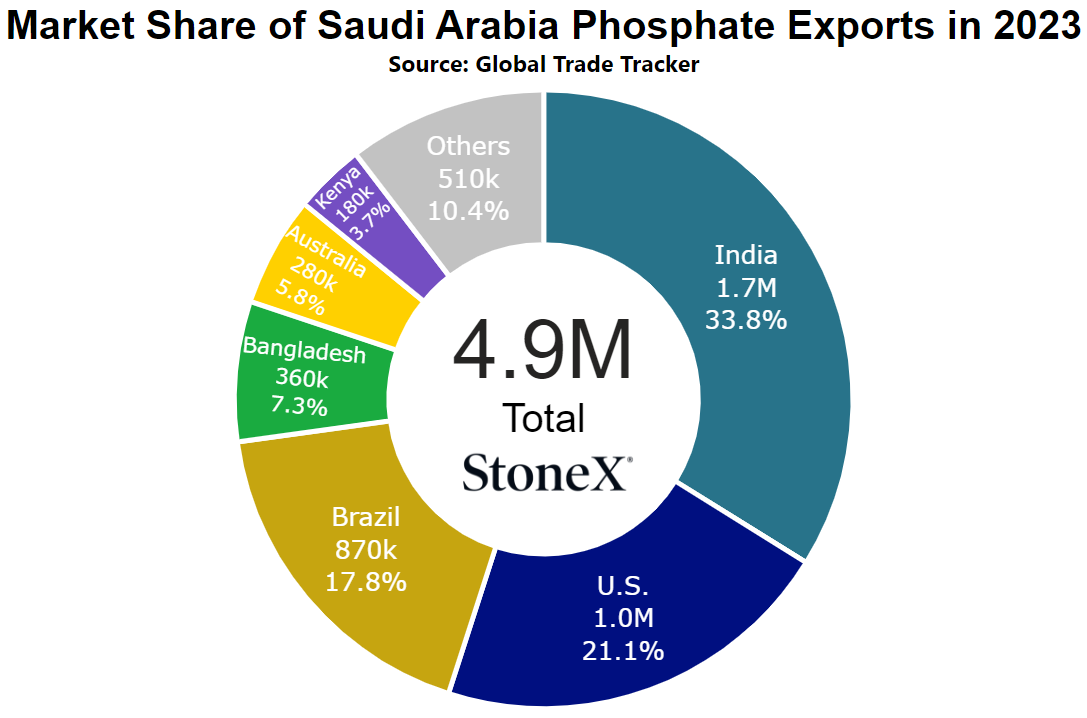

- Saudi Arabia - it sounds as though they are going forward with their 3rd phase of phosphate production. Details have been few, but hopefully real nonetheless.

- Norway - there was a huge phosphate rock reserve discover made in Norway and it sounds as though they will charge ahead with developing the area.

On top of these, there continues to be hope that U.S. production rates will return to their normal 80 - 90% range (Q4 '24 was set at 58%).

Fortunately, if/when this list of new tons start to become reality, they should add much needed supplies to a world that is begging for them.

Unfortunately, that is going to take time. Expanded/new production does not happen overnight. These types of situations do not take months, they take years.

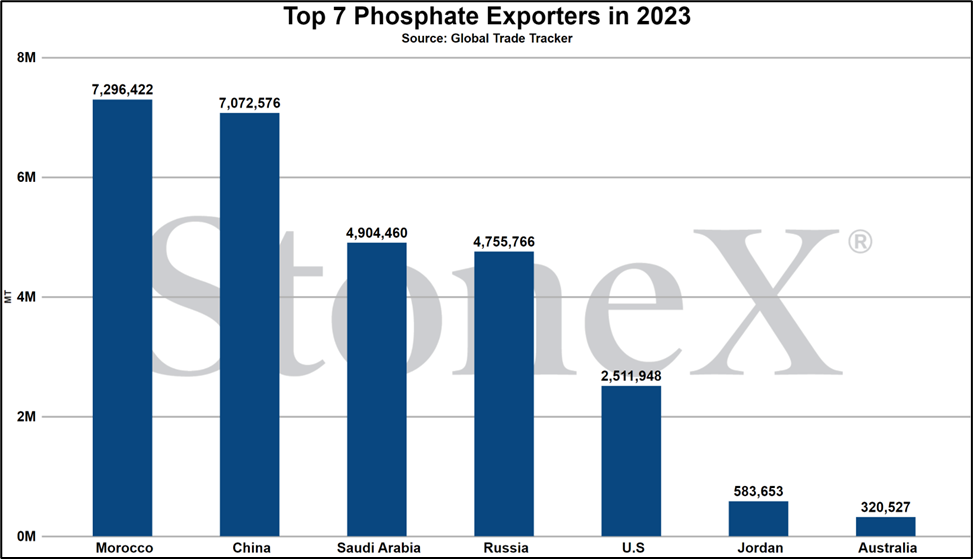

For the short term, from my vantage point, we have to keep watching China. Their exports remain dismal and continue to help support global phosphate prices. If they were to return to full, normal export rates, current global values would likely be a thing of the past.

For now, this list of new/expanded production acts as a light at the end of the tunnel...a very long, dark tunnel.

What does this mean for Aussie farmers?

This should mean much more available supply and eventual lower prices for Aussie farmers using phosphates...eventually.

Unfortunately, none of the projects listed are expected near term. In fact, I wouldn't hold my breath that anything makes enough progress to even help the 2026 phosphate run.

However, the fact that the list is growing is a good thing. It at least means there is hope in the future.

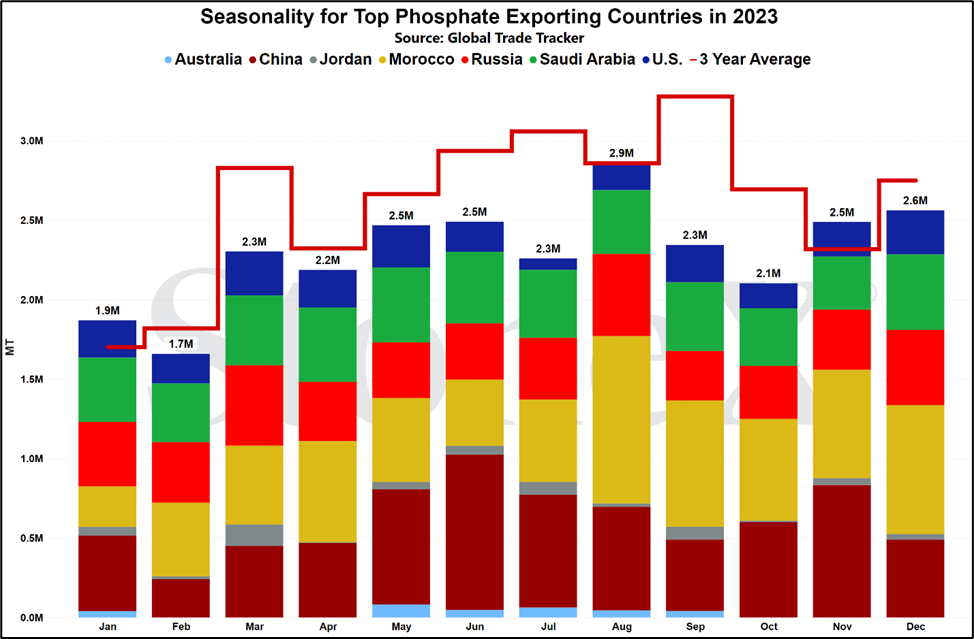

China's March export data shows lowest ever shipped for world's largest

Normally, China is the world's largest phosphate exporter, sending between 9 and 10M tons per year to the world.

We are not living in normal times.

For the last few years, those exports have shrunk.

- 2021 - 10M tons

- 2022 - 5.6M tons

- 2023 - 7.1M tons

- 2024 - 6.6M tons

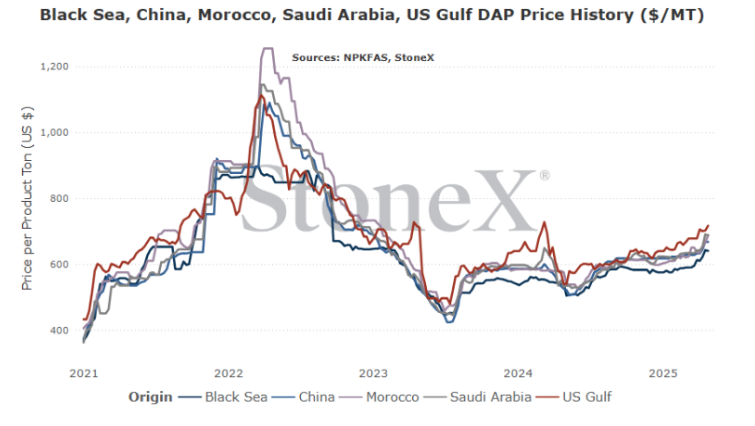

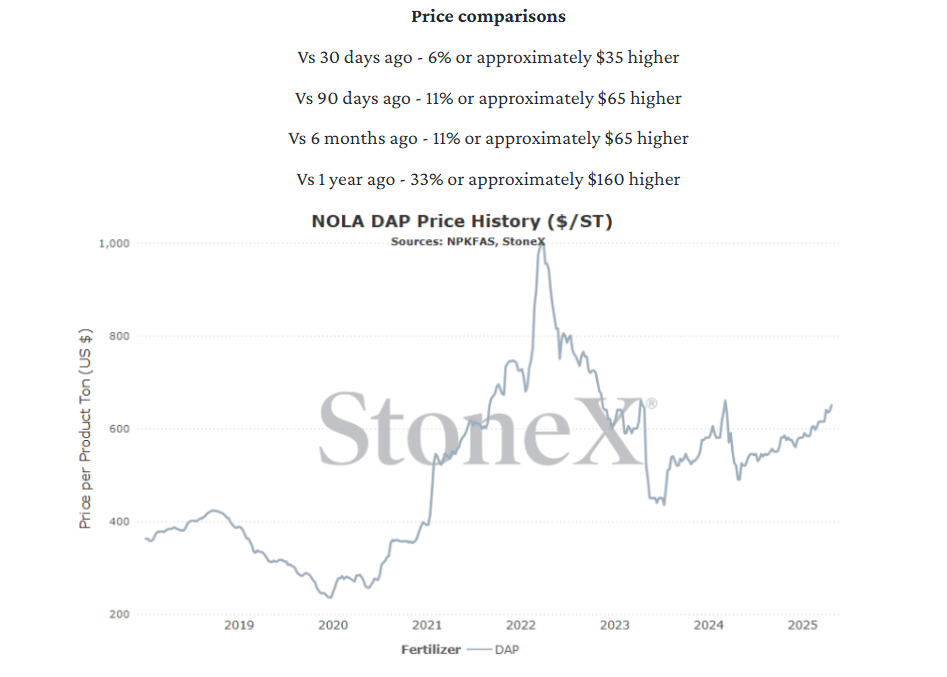

Why? Remember where the markets were in 2022. Global values skyrocketed. NOLA DAP, for example, hit $1,000 for the first time since 2008. Demand was high as grain prices skyrocketed. Supplies got tight.

And the Chinese government intervened.

From my uneducated POV, a communist governments most feared group is not an outside force. Rather, it is an uprising from within. Who is one of the largest blocks of people in China? Farmers.

Like urea, the government decided to take steps to intervene. Rather than allowing full exports, restrictions started to be put into place to limit the number of tons that flowed to the world. In doing this, domestic supplies rose well above sufficient levels and domestic prices fell vs the world. Both of these were HUGE for Chinese famers...and helps keep that large block of people happy.

Unfortunately, the rest of the world pays the price.

There has been lingering hope that the Chinese government would loosen these restrictions...but that has not been the case. 2025 has not started well with only just over 111K tons of DAP/MAP exported in the first quarter.

Now, there are still 9 months for them to catch up...but it is not looking promising so far. We have not seen/heard anything that leads us to believe an immediate return to form is coming. In fact, some have theorized that the government will loosen the restrictions any day now...but it will not matter as Chinese manufacturers do not have the supplies available to export and it may be June or after before they do.

If Chinese exports come back to 100%, it will be a huge bearish event for the world...I just wouldn't hold my breath on that happening right now.

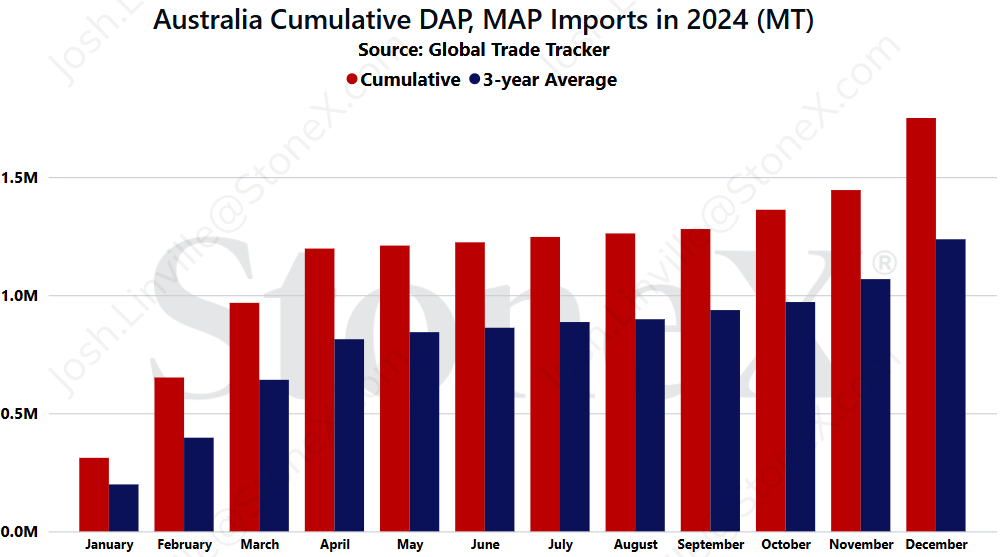

What does this mean for Aussie farmers?

The fact that China has slowed down so hard on exports means an extremely low chance that domestic values will fall this phosphate season.

China is the largest supplier in the world so when they cut back this hard, it is felt all over. Hopefully we are wrong about when they will return (sooner than later), but I'm not holding my breath.

India continues to struggle with the current phosphate market

The Indian phosphate market hasn't been a story. It has been more a soap opera.

Since last summer, the government has been struggling with its phosphate approach. For a bit of back story, India does not do fertilizer like the rest of the world in that farmers are not subject to global price volatility. Their price stays flat due to government intervention. In order to keep the price flat but still ensure enough imports flow, the government subsidizes importers the difference.

As you can imagine, for a country that imports millions of tons per year, this can be costly.

Last summer, global values were sliding. It had appeared that China was returning to normal export flows, the calendar was moving toward its typical annual low price period, and buyers were finally smelling blood in the water. India joined into the fray. It was voted and approved that they would reduce the subsidy rate in an effort to further pressure values. If global supplies were plentiful and prices were already weak, their reducing the subsidy rate would mean importers had to buy at lower prices to make it work. The hope was that global sellers/manufacturers would accept the lower netbacks.

They likely would have...if China didn't do an about face.

Suddenly, Chinese exports slowed down as the government put further restrictions in place and the Indian government was slow to respond. As 2024 progressed, the global markets did not turn around and as a result, imports slowed dramatically to the point that domestic stockpiles became a story. The largest voting block in India is farmers...and they do not take lightly to low stockpiles of phosphate. In later 2021, stockpiles were allowed to drop to severely low levels and farmers started to riot. This is how serious they are! The government does not want to lose power and their largest voting block is farmers, so it makes sense they want to keep them happy. While imports have been just good enough to keep from repeating that period, they remain very low and in need of faster flows.

But the world is making them pay and they are sick of it.

At the end of March, India continued to buy phosphate where and when it could...but prices continued to rise:

End of March - $640's CFR

Early April - $660's to $670's CFR

Mid-April - $680's to $690's CFR

Late April - $700 CFR...then the shocker.

Not long after $700 CFR was locked up, a reported purchase of $750 CFR was made...and that was the last straw from the government who was tired of paying what they saw as outrageously high prices. The brakes were set and set hard. It was questioned whether they would honor the $750 contract. Guidance was given that they would not support anything higher than $675 CFR.

And that is where we sit today...at a crossroads.

Path 1 - the world holds on higher prices and forces India's hand - India cannot wait on their new strategy forever. Eventually, they have to start bringing in supplies or face the wrath of their population. If global manufacturers/suppliers can hold out long enough for India to break, they should be able to name their price...which means the rest of the world has to deal with the same.

Path 2 - the world succumbs to India's "demands" - there is a chance global manufacturers look at the $675 CFR price and think "that is a pretty good number where we make a lot of margin. Maybe we just sell it and not rock the boat." I'm less optimistic this happens, but I think there is a chance. Phosphate manufacturers are doing really well right now on margins and we are moving into a slow demand period (even worse with prices as high as they are). If they drop for India, they may do the same for the rest of the world.

Unfortunately, at this time, I'm not sure where this goes but it remains a high watch point as it can/will have global ramifications.

As always, events halfway around the world matter to you regardless of where you farm.

What does this mean for Aussie farmer?

If India were not in the shape they are in, it would mean that Australian buyers represent one of the few nearby demand points in the world. Even with the China export situation, global position holders could still target Australia and the import boom could pressure values lower.

But that is not the case.

India still has a lot of buying left to do and that puts them in direct competition to you. More competition on the buy side is a win for manufacturers/suppliers.

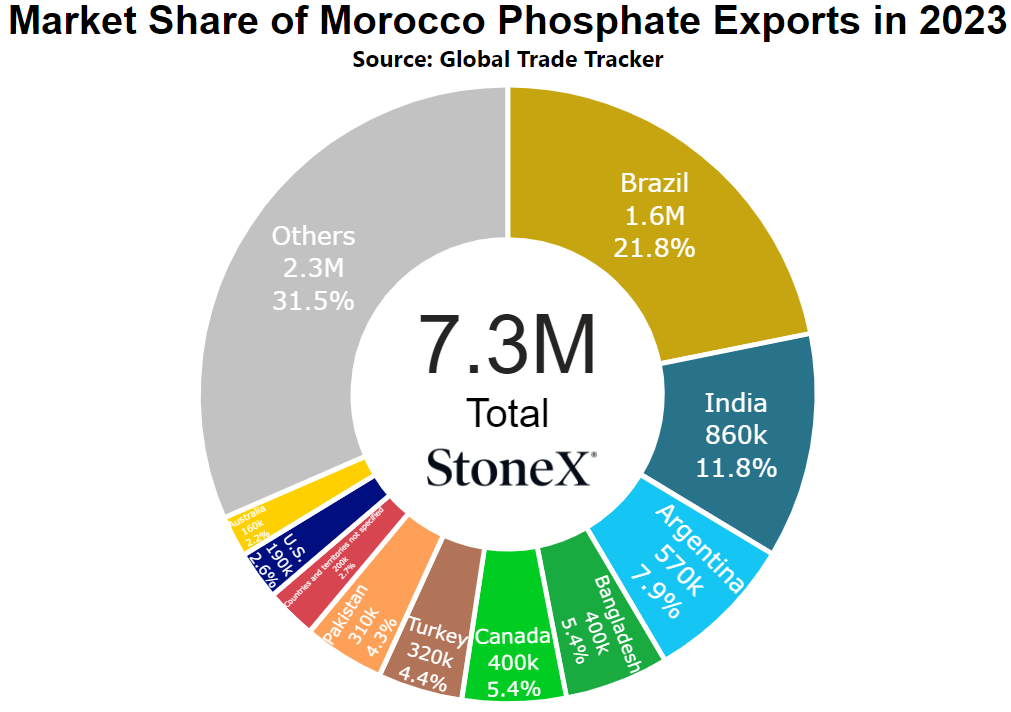

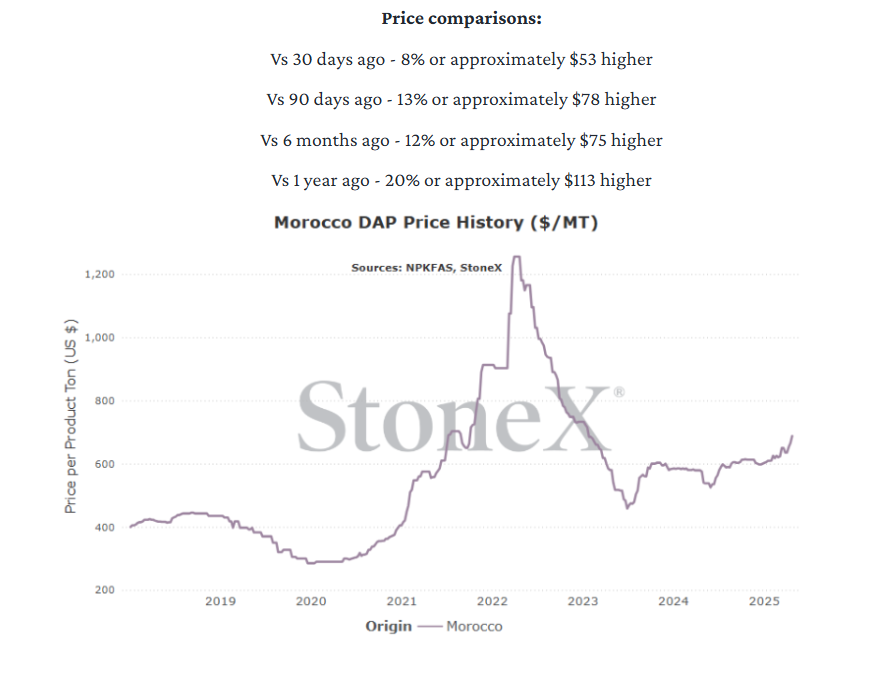

Morocco DAP price comparison

Number 1 global exporter in 2022

Black Sea DAP price comparison

Number 3 exporter of DAP/MAP in 2022

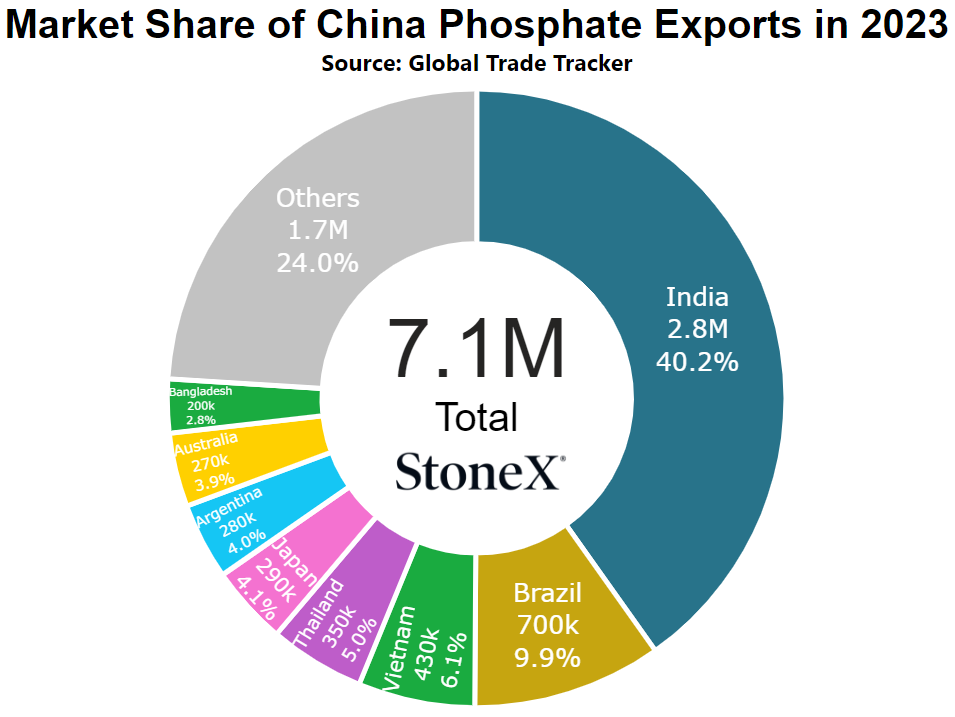

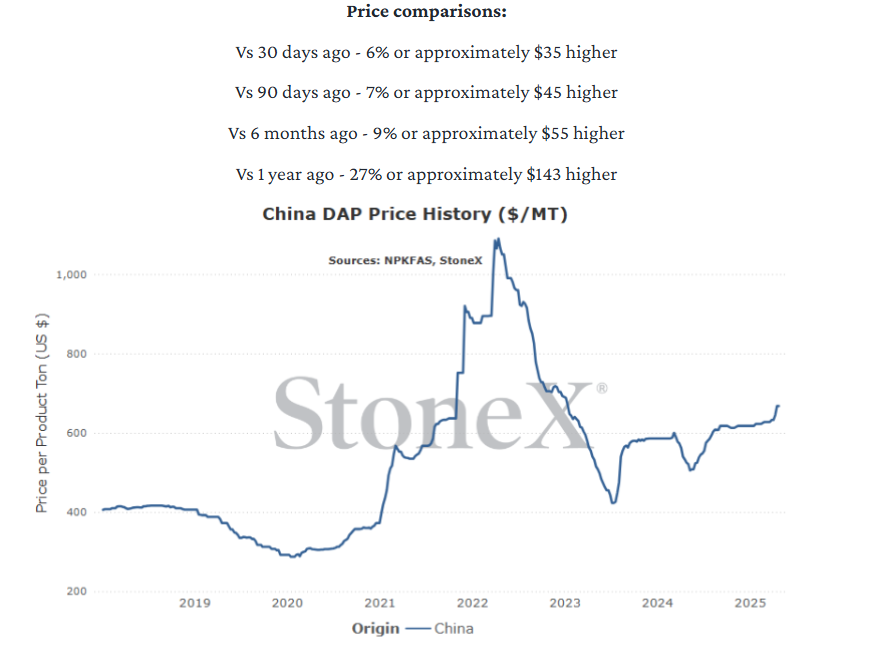

China DAP price comparison

Number 2 global exporter in 2022

Saudi Arabia DAP price comparison

Saudi Arabia DAP price comparison

Number 4 global exporter in 2022

- Chinese exports remain dismal – I do not care what corner of earth you read this from, when the world's largest exporter pulls back like China has done, it is felt. With some speculating that they may not return until June...if at all...this should continue to boost price ideas. That affects everyone.

- India continues to catch up – having the world's largest supplier pull so far back is bad. Having the world's largest buyer be behind on imports/low on stockpiles is baddererer!! To me, China is the cause but India continues to be the situation that proves the scenario. Normally, as we move into May and beyond, a lot of demand falls off. If India continues to buy, there is no reason for typical seasonal price patters to happen.

- Importers slow pace due to questionable demand/price risk – if I were an importer, I would struggle with today's market. Prices are incredibly high and under the right circumstance could go higher. However, if China suddenly started exporting again, the market could fall apart. Starting from these levels, that could be devastating. No doubt some are likely more conservative on position taking. If there is enough of that, Australia could see supplies get snug.

- China returns – is this expected today? No, but it is certainly possible. The fertilizer road is littered with folks saying "China WILL do this" or "China WILL NOT do that". As soon as you think you have a read on the country, they do the exact opposite. Today, the view is that China will not return to exporting until the 2nd half. That helps to prop up price ideas...which means if China does a 180 and starts exporting heavy, watch out for the downside price scenario.

- Global manufacturers are content to sell current values than to risk higher – India is trying to force the global markets hand by setting a $675 CFR price limit. Their hope is that the world will decide that is a solid price/margin and proceed. If, and that is a big if, the supply side goes that route, it could keep values tamped down. I'm not expecting this, but it is very much a watch point.

- Aussie demand falls due to high pricing – while this hasn't been seen/heard, it is still something being watched globally. Current phosphate values are high. There is no way around it. However, farmers may fight the higher price by cutting back on application rates. It may not take demand to zero, but even smaller percentages can equal large amounts of demand lost. Enough of that happens, and it could weigh on price ideas.

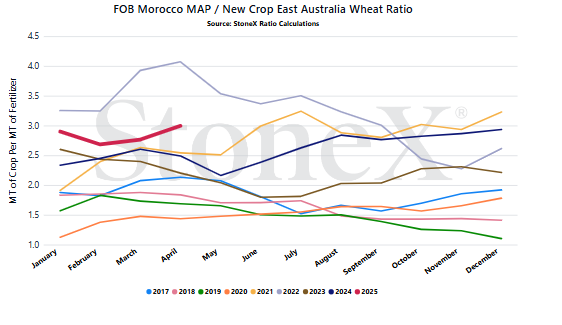

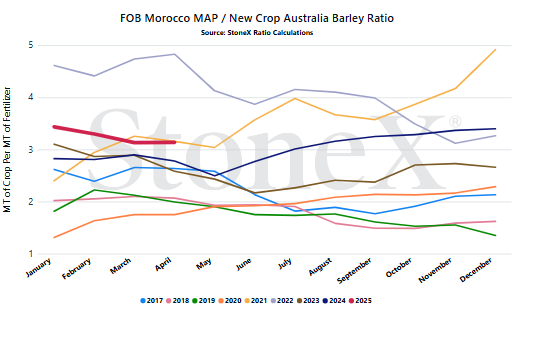

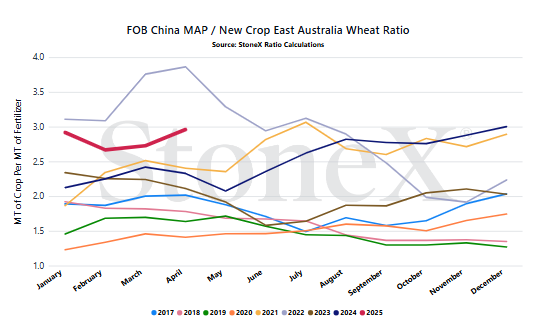

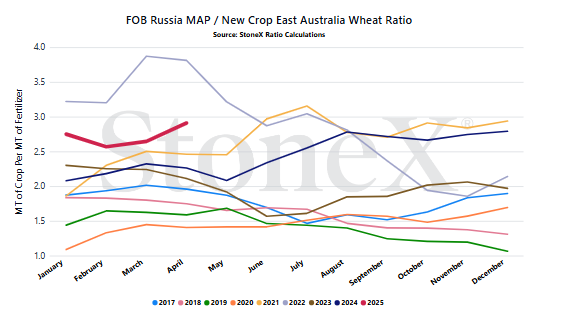

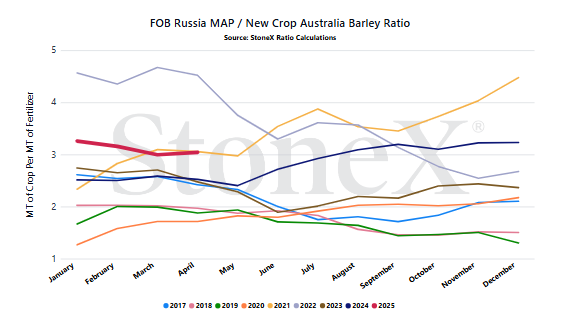

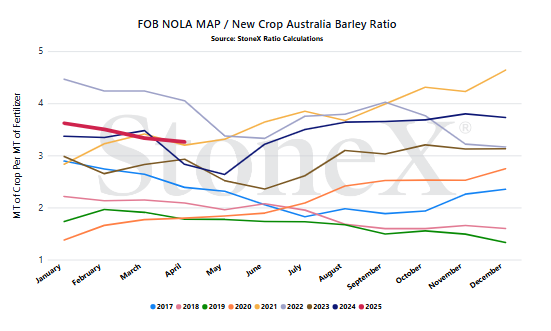

We believe that only looking at the flat price of either grains or fertilizer can be misleading:

-

Only selling grain can hurt you if fertilizer prices rise substantially

-

Only buying fertilizer can hurt you if grain prices fall

We look at the ratio "value" to get a better indication of where we are or how many bushels of X does it take to pay for 1 ton of fertilizer.

Would you rather:

-

Spend 4 ton of grain to pay for 1 ton of MAP

-

Spend 1.5 ton of grain to pay for 1 ton of MAP

When we compare the current ratio value against recent years, we start to see if we are high or low.

YOUR VALUES MAY LOOK DIFFERENT

![]()

- Chinese export flows - easily the most important focal point heading into May. China is tightening the global S&D in a way that I have never seen. We have seen higher prices (2008), but that was largely driven by demand. When 2008 demand stopped, prices plummeted. That is a key trait of a demand driven bull run, it rings hollow. This current run is a supply driven situation meaning it has a lot more staying power...and China is holding the keys.

- Indian imports flows - if it were only the China story, we could see things going quiet in the coming weeks/months. Sure, the lack of Chinese exports hurts global supplies, but without buyers to prove the story things could go quiet. Unfortunately today, it appears India needs to continue buying to rebuild stockpiles and prepare for their next season. Their approach should continue to tell and prove the tight supply story.

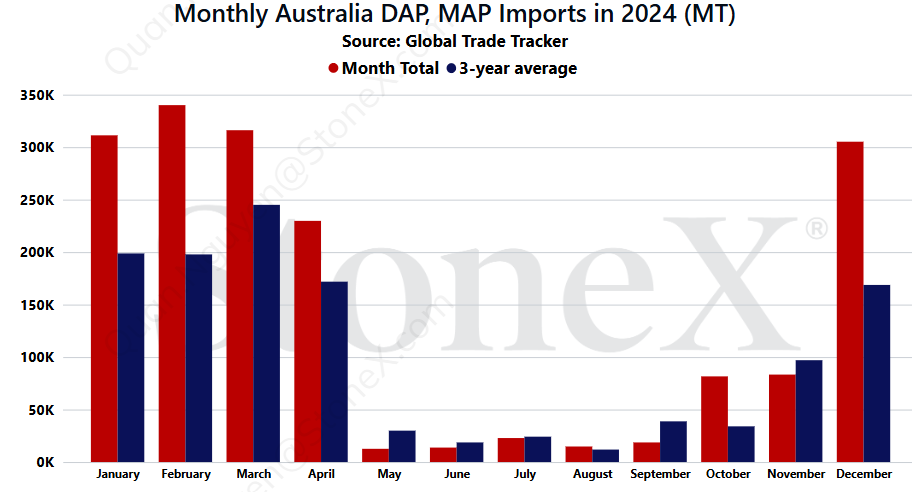

- Australia ending supplies/imports - given tight global supplies and the heightened price risk with where we are today, it makes sense that imports may slow substantially. Why bring in an additional vessel and run the risk of getting stuck with it? I cannot say that we have seen/heard anything like this happening, but we are watching close.

StoneX Ratio Calculation

The ratio calculation is derived from Bloomberg historical grains values as well as fertilizer values from StoneX, NPKFAS, and Argus.

The calculation is simply dividing the fertilizer price by each grain price.

All data was sourced from StoneX unless otherwise noted.