Weekly roundup for StoneX Bullion

Rhona O'Connell, Head of Market Analysis, EMEA & Asia

Tel: +44 203 580 6115 / mobile +44 7384 833897

23rd March 2026

Precious snapshot – hefty sell-off across the board then a reported Trump tweet turns everything around – for now

Last week gold was treading water; now it is under water and silver (as usual) has suffered even more.

Two key factors were behind the precipitous falls; the Middle East and the Fed meeting.

But there is a lot more involved.

As we write gold, which had dropped to a low of $4,126 (from $5,419 on 2nd March), has bounced by over $150 following a reported Tweet from President Trump to the effect that talks with Iran have been making solid progress over the weekend and that he has ordered a five-day moratorium on strikes on power plants and energy infrastructure. So this is not an outright ceasefire but potentially paves the way for further progress.

So gold and silver have now had their much-needed wash-out after their stellar performances of the past few months. To sum up briefly, the factors contributing to the falls were as follows: -

Liquidation / profit taking on concerns over potential rate hikes, or at least not much further easing – it was pretty significant that Chris Waller didn't call for a cut in last week's FOMC as he is one of the strongest proponents of easier monetary policy. The Committee held rates steady and there was a more hawkish tone than recently. For our commentary on the meeting and Jay Powell’s Press Conference, please see the link here.

Gold had already been getting edgy at prices over $5,200, suggesting that the market was crowded; silver perhaps not quite so much, but as is almost invariably the case, gold’s powerful move took silver with it, and to a greater extent.

Technicals, notably moving averages, exacerbating the situation.

Some likely distress selling against equity weakness although in % terms gold is down a lot further this month than the S&P (24% vs 10%).

Central Banks buying a lot less gold than in the past three years; this is not so important where tonnage is concerned but the knowledge of it will affect sentiment. The World Gold Council reports that net purchases in January were just five tonnes; this compares with a monthly average of 72tpm in 2025.

The same applies to ETFs, which have lost at least 96t. The latest figure from the World Gold Council was 4145.2t on 13th March, subsequent (incomplete) numbers from Bloomberg suggest a fall of at least 25t last week.

Stops were hit as prices came down, which exacerbated the speed of the moves.

From last Monday’s high to the lows so far were as follows: -

Gold; $5,038 to $4,099, or 29%

Silver;$81.64 to $60.96, or 25%

From the end-January peaks to today’s lows so far:

Gold $5595 to $4,099 or 31%

Silver; $121.65 to $60.96, - a thumping 50%.

Since the start of 2024, however, they are up by 113% and 185% respectively.

Silver ETFs have continued to lose metal, with the latest figures showing 25,289t, a fall of 1,573t or 6% since the start of the year. World silver mine production is ~27,000tpa.

On COMEX, silver inventories have continued to come off sharply over the past few weeks and, at 10,348t, are down by 6,183t since end-September and getting back towards the more normal 9,000-10,000t levels. This may take some of the volatility out of the market as it helps to ease London’s position. Gold inventories at 1,012t are 10% down for the year to date.

Among the Managed Money funds, gold positioning has increased slightly on both sides of the market with outright longs at 405t from 389t and shorts at 87t from 83t. Silver longs have contracted again to 2,053t from 2,132t and there has been a small increase in shorts, from 463t to 485t; as recently as mid-February they were 2,465t. So it is clear that short covering was a key silver driver (it usually is), even as long positions were contracting (they were 5,589t in early February).

Gold, one-year view; right down to the 200-day moving average

Source; Bloomberg, StoneX

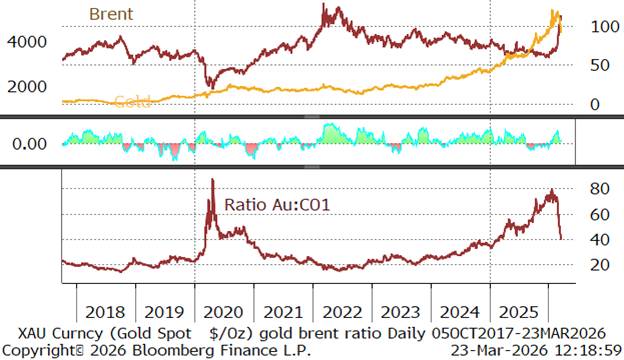

Gold:Brent ratio

Outlook: small bounce

The massive sell-price falls have taken both metals into oversold territory and with hostilities not over in the Middle East and the potential for further tension between Pakistan and Afghanistan after the Eid celebrations are over, we can probably expect some fresh buying interest. We still believe, however, that the highs are in for both metals.

Gold COMEX positioning, Money Managers (t)

COMEX Managed Money Silver Positioning (t)

Source for both charts: CFTC, StoneX

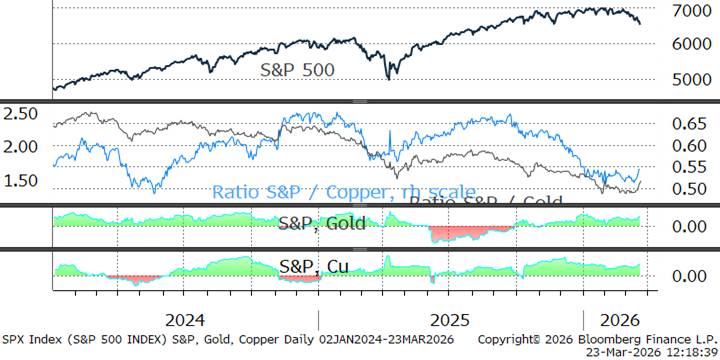

The S&P, gold and the dollar; gold:S&P tighter at 0.34

Source; Bloomberg, StoneX

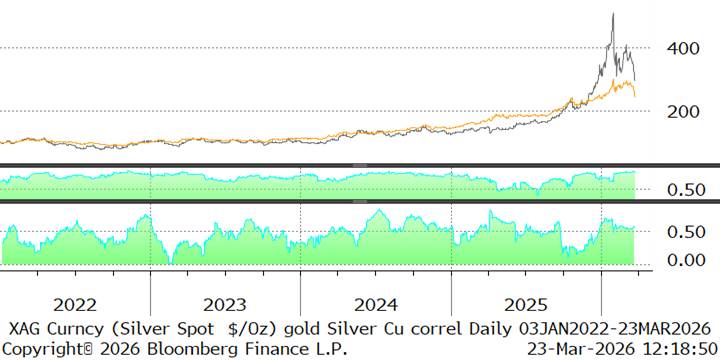

Gold, silver and copper; silver-gold 0.85; silver-copper, 0.56. Little changed

Silver, one-year view; on a Fib 61.8% retracement from the massive falls in January and early February

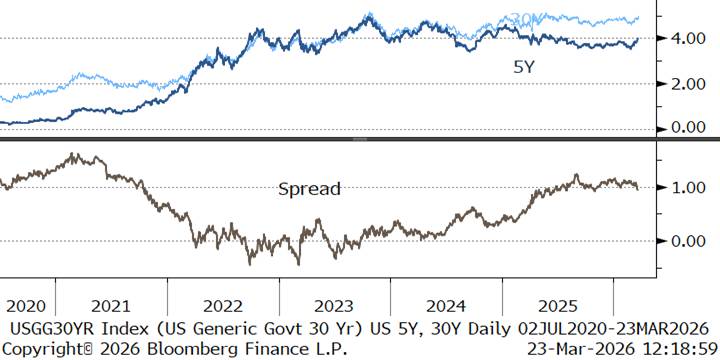

US five-year and 30-year yield

Source; Bloomberg, StoneX

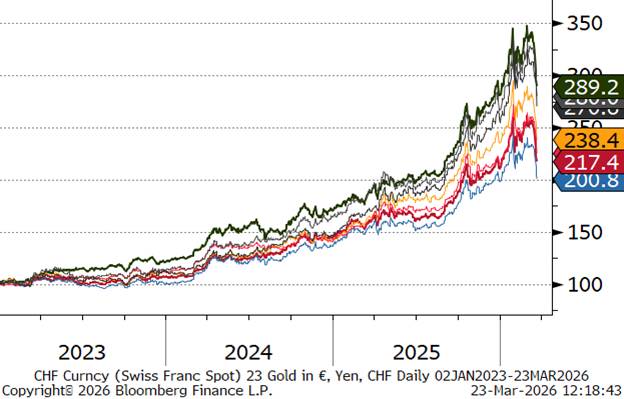

Gold in key local currencies. In yen terms, up 190% since the start of 2023; CHF is the smallest rise at “just” 101%

Source: Bloomberg, StoneX

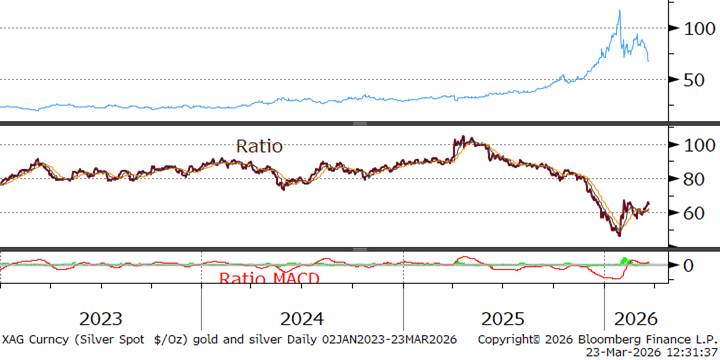

Gold:silver ratio; has been narrowing in the second half of February but widening slightly; latest at 62

Source: Bloomberg, StoneX

| | 23 March 2026 | Previous week | % change | Jan 2025 onwards | | | Range as % |

| | | | | | Min | Max | |

| Gold (pm LBMA price) | 4,562.55 | 5,044.60 | -9.56% | 72.41% | 1,985.10 | 5,405.00 | 172.28% |

| Silver (LBMA price) | 72.37 | 83.70 | -13.53% | 146.07% | 22.09 | 118.45 | 436.34% |

| Platinum (pm LBMA price) | 1,978.00 | 2,077.00 | -4.77% | 114.77% | 1,369.00 | 2,811.00 | 105.33% |

| Palladium (pm LBMA price) | 1,434.00 | 1,612.00 | -11.04% | 55.70% | 852.00 | 2,106.00 | 147.18% |

| S&P 500 | 6,506.48 | 6,632.19 | -1.90% | 10.15% | 4,688.68 | 6,978.60 | 48.84% |

| $:€ | 1.1572 | 1.1417 | 1.36% | 11.18% | 1.0244 | 1.2041 | 17.54% |

This material should be construed as market commentary and represents the opinions and viewpoints of the author, and does not reflect tailored advice associated with any specific account.

The views are current only through the date stated and are subject to change at any time based upon market or other conditions, and StoneX Group Inc. (“SGI”) disclaims any responsibility to update such views. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources. Past performance does not guarantee future results.

The StoneX Group Inc. group of companies provides financial services worldwide through its subsidiaries, including physical commodities, securities, exchange-traded and over-the-counter derivatives, risk management, global payments and foreign exchange products in accordance with applicable law in the jurisdictions where services are provided.

References to certain OTC products or swaps are made on behalf of StoneX Markets, LLC (SXM), a member of the National Futures Association (NFA) and provisionally registered with the U.S. Commodity Futures Trading Commission (CFTC) as a swap dealer. SXM’s products are designed only for individuals or firms who qualify under CFTC rules as an ‘Eligible Contract Participant’ and who have been accepted as customers of SXM.

StoneX Financial Inc. (SFI) is a member of FINRA/NFA/SIPC and registered with the MSRB. SFI is registered with the U.S. Securities and Exchange Commission (SEC) as a Broker-Dealer and with the CFTC as a Futures Commission Merchant and Commodity Trading Advisor. StoneX Financial (Canada) Inc. (SFCI) is registered in Canada and is a member of CIRO and CIPF. References to certain securities trading are made on behalf of the BD Division of SFI and are intended only for an audience of institutional clients as defined by FINRA Rule 4512(c). References to certain exchange-traded futures and options are made on behalf of the FCM Division of SFI. Wealth Management is offered through SA Stone Wealth Management Inc., member FINRA/SIPC, and SA Stone Investment Advisors Inc., an SEC-registered investment advisor, both wholly owned subsidiaries of SGI.

R.J. O’Brien & Associates, LLC (RJO) is registered with the CFTC as a Futures Commission Merchant and is a member of NFA.

StoneX Financial Ltd (SFL) is registered in England and Wales, company no. 5616586. SFL is authorized and regulated by the Financial Conduct Authority (FCA) (registration number FRN:446717) to provide services to professional and eligible customers including: arrangement, execution and, where required, clearing derivative transactions in exchange traded futures and options. SFL is also authorized to engage in the arrangement and execution of transactions in certain OTC products, certain securities trading, precious metals trading and payment services to eligible customers. SFL is authorized and regulated by the FCA under the Payment Services Regulations 2017 for the provision of payment services. SFL is a category 1 ring-dealing member of the London Metal Exchange. In addition SFL also engages in other physically delivered commodities business and other general business activities which are unregulated and not required to be authorized by the FCA.

This communication is issued in the European Economic Area by StoneX Financial Europe GmbH (SFEG). StoneX is the trade name used by STONEX GROUP INC. and all its associated entities and subsidiaries. StoneX Financial Europe GmbH (“SFEG”) is a securities trading firm registered in Germany under Company No. HRB 80844.

StoneX Financial Pte Ltd (Co. Reg. No 201130598R) (“SFP”) is regulated by the Monetary Authority of Singapore and is a Capital Markets Service Licence holder (for dealing in capital market products), an Exempt Financial Adviser (for advising on investment products and issuing or promulgating analyses/ reports on investment products) and a Major Payment Institution (for domestic and cross-border money transfer services).

SFP may distribute analysis/report produced by its respective foreign affiliates within the StoneX Group of companies pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations Recipients should contact SFP at (65) 6309 1000 for any matters arising from, or in connection with, this webinar.

StoneX APAC Pte. Ltd. (“SAP”) (Co. Reg. No 200616676W) is regulated as a Dealer (PS20190001002) under the Precious Stones and Precious Metals (Prevention of Money Laundering and Terrorism Financing) Act 2019 for purposes of anti-money laundering and countering the financing of terrorism.

StoneX Financial (HK) Limited (CE No.: BCQ152) (“SHK”) is regulated by the Hong Kong Securities and Futures Commission for Dealing in Securities and Dealing in Futures Contracts.

StoneX Financial Pty Ltd (ACN 141 774 727) holds an Australian Financial Service License (AFSL: 345646) for Dealing in Securities, Exchange-Traded Derivatives Contracts, OTC Derivatives Contracts and Foreign Exchange Contracts, and is regulated by the Australian Securities and Investments Commission.

StoneX Securities Co., Ltd. (“SSJ”) (Co. Reg. No 010401047199) is regulated by the Japanese Financial Services Agency as a Type-I Financial Instruments Business Operator (Kanto Local Finance Bureau (FIBO)No.291’), is a member of the Financial Futures Association of Japan for dealing and broking FX and FX Option transactions, and is a member of the Japan Securities Dealers Association for dealing and broking stock indices and option transactions.

Trading swaps and over-the-counter derivatives, exchange-traded derivatives and options and securities involves substantial risk and is not suitable for all investors. Past performance of any futures or option is not indicative of future success. Indicators are not a trading system and are not published as a specific trade recommendation. The information herein is not a recommendation to trade nor investment research or an offer to buy or sell any derivative or security. It does not take into account your particular investment objectives, financial situation or needs and does not create a binding obligation on any of the StoneX group of companies to enter into any transaction with you. You are advised to perform an independent investigation of any transaction to determine whether any transaction is suitable for you. No part of this material may be copied, photocopied or duplicated in any form by any means or redistributed without the prior written consent of StoneX Group Inc.

The report/analysis herein is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

© 2026 StoneX Group Inc. All Rights Reserved.