- Global production for 2023/24 estimated much above consumption, according to USDA;

- Still weak economic indicators;

- Absolute production record in Brazil and lack of storage;

- Fast pace of US planting;

- El Niño should be beneficial for US crop.

- Considerable crop losses in Argentina due to the weather;

- Record soybean imports by China in May;

- Chinese crush margins are more positive;

- Increase in mandatory biodiesel blending in Brazil;

- Forecast of drier weather for some of the US production region.

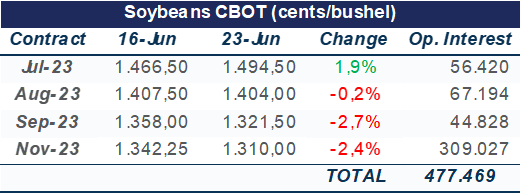

After the recent sharp highs, last week soybean prices in Chicago recorded a correction, with profit taking. The contract for July/23 still registered gains in the period, ending Friday (23) at 1494.5 cents per bushel, while the more distant contracts, referring to the new US crop, retreated. The contract for November ended at 1310 cents per bushel, a weekly decline of 2.4%.

In any case, weather conditions for the US continued to be the main factor moving the soybeans market, which is usual at this time.

Comparisons with 2012, when the country recorded a very large crop failure, are still present, but the weather still needs to be monitored in the coming weeks and months, bearing in mind that the most critical phase for soybeans, which is grain filling, is concentrated in August.

Even so, dry conditions in key regions of the Midwest have prevailed. The country's latest Drought Monitor, which is updated weekly, continued to show worsening conditions in producing states in the central and western grain belts. On the other hand, in addition to being still early, a positive point compared to 2012 is that very high, above normal temperatures have not prevailed.

Last weekend, beneficial rains were recorded further north in the Midwest, but the more central and southern areas continued to be under stress. For the next 10 days, weather forecasts raise concerns for areas in the northwest of the belt, which already includes regions with major drought conditions.

The last US crop progress report, referring to June 18, brought a new significant worsening of the conditions, with the good/excellent percentage falling 5 points, to 54%, below the same week in 2022 and the five-year average, which were at 68% in both cases. The highlight is the state of Illinois, which alternates with Iowa at first place in national production and where the percentage dropped from 47% to 33% in one week.

On Monday, the USDA will update data on conditions for US crops and the perspectives are that there will be a new drop in the good-excellent percentage, albeit less expressive. Even so, as mentioned, since there is still time for the development of plants and for them to go through key phases, if conditions improve in the coming weeks, there is room for a good crop, even if the productivity currently estimated by the USDA, at 3.5 tonnes per hectare is no longer achieved.

Also in the US, although news about the weather prevailed, the update of biofuels mandates by the Environmental Protection Agency (EPA) frustrated market expectations. The EPA will not increase requirements for RIN D4 (biomass-based diesel) in 2023, maintaining it at 2.82 billion gallons, expanding to 3.04 billion in 2024 and 3.35 billion in 2025. These volumes were below what refineries expected, betting on increases already this year. Even so, it should be noted that record volumes of renewable fuel should be blended with gasoline and diesel over the next three years. This EPA update weighed heavily on soybean oil prices in Chicago, as soybeans and meal continued to respond to weather concerns for the US crop.

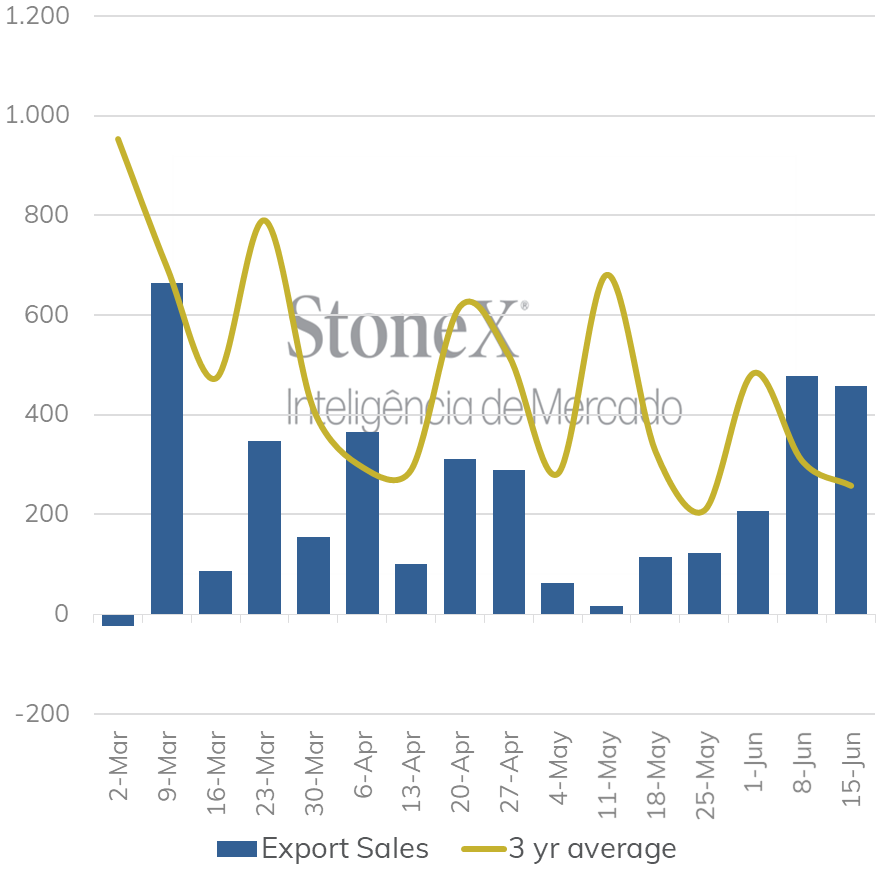

US export sales in the week ended June 15, were within expectations for the 2022/23 and 2023/24 crops, with net volumes at 457,500 and 167,800 tonnes, respectively. As has been highlighted in previous reports, sales of the current crop are weaker than in the same period last year and the US has even revised the estimated export figure for the 2022/23 cycle. However, even though it is still early, it is also important to point out that the accumulated negotiations for the 2023/24 season are considerably lower than those recorded at the same time in previous years.

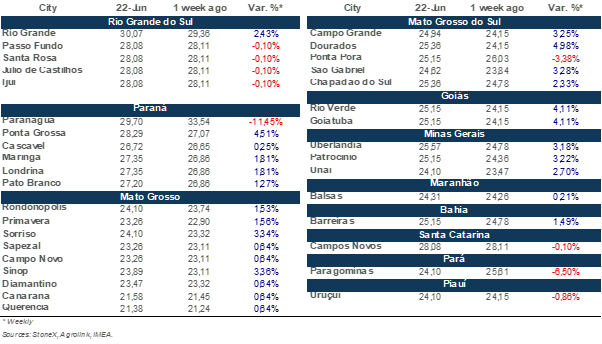

It should be noted that Brazilian soybean remains more competitive than US soybeans placed in China and that total shipments from Brazil in June are heading towards a result that could be a record for the month. Until June 16, 8.75 million tonnes were shipped, against 10 million in the month as a whole in 2022. Today (26), the data for the week ended last Friday (23) will be released.

Even with heated export volumes, the basis remains under pressure in the Brazilian market, given record harvest and lack of storage. With the progress of second-crop corn harvest, there are already reports of large piles of corn left in the open, which illustrates the lack of static capacity, whose growth does not follow the strong increase in grain production that Brazil registers.

This week, the weather should continue to be the main factor driving prices on the CBOT, in addition to the report on the position of stocks and planted area in the US, which will be released on Friday (30). Usually, these reports bring strong movement for prices in Chicago.