- In 2024, key Bitcoin narratives include registered investment advisory (RIA) market, commodity status, the Bitcoin halving, and Layer 2 innovation

- Regulation in the US will continue to remain an unsolved wildcard – with no movement from US congress expected, and continued SEC lawsuits to dictate the near-term regulatory narrative

- Ethereum and layer 1 protocols poised for wider adoption, influenced by potential ETH ETF approval, regulatory clarity and protocol enhancements aimed at lowering transaction fees

- Other crypto narratives to watch in 2024 to include modular chains, real world assets (RWAs), decentralized physical infrastructure (DePIN), and meme coins

Digital Assets Are Here to Stay

In 2023, the US crypto market defied challenges, with significant price appreciation (+157% for BTC), a softer stance on Operation Chokepoint 2.0 and key developments such as Bitcoin (BTC) ETF approvals and decreasing risk asset correlations. Despite a vocal, and likely politically driven, agenda against crypto by SEC Chair Gensler and several members of Congress, we believe that crypto in the US is here to stay. The perception of Operation Chokepoint 2.0 eliminating crypto eased in the second half of 2023. While banks are still restrictive in many aspects of on and off-ramps, they have not shut these access points off completely. Several significant court rulings against the SEC, specifically rulings in the Ripple case and the Grayscale case, have opened up the path for wider digital asset adoption. To start the year, we saw the approval by the SEC and launch by issuers of the first spot-backed BTC ETF’s. With the largest traditional banks and established trading firms as initial Authorized Participants (APs) for the ETFs, the bellwether financial institutions are getting involved. And while the success of those products will be determined in the months and years ahead, we view this as a watershed moment in the long-term arc of digital asset adoption.

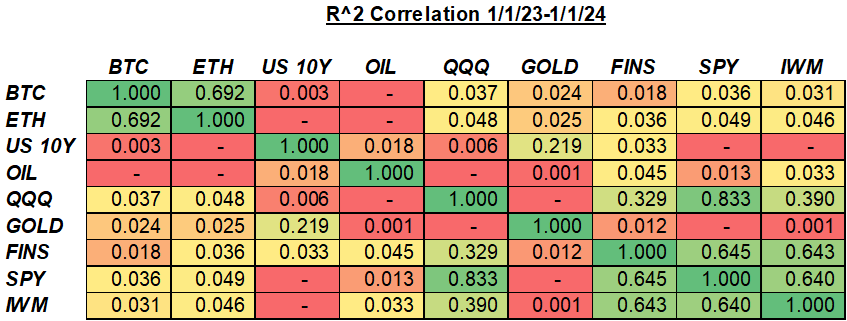

Referring to the aforementioned price action, which outperformed every other asset class, we would focus on the decreasing correlation between BTC and ETH (the “Majors”) and other risk assets. Over the course of 2023, we saw a steadily declining correlation between BTC and QQQ, IWM, and SPY.

Daily Correlation between BTC and IWM in 2023

Source: Bloomberg

Source: Bloomberg

This likely reflects the anticipation of a BTC ETF steadily pushing BTC prices higher in 2H 2023, but also the potential for longer term decoupling of crypto as a nascent asset class. As the case for crypto becomes widespread and real-world use cases evolve, we look forward to significant long-term flows of funds into the space, analogous to the adoption of the internet.

Bitcoin Narratives Set Up Positively for 2024

There are four narratives we want to focus on surrounding Bitcoin specifically, all of which could lead to increased adoption.

The money is coming. Estimates for the US RIA market alone are close to $5T of AUM. This market has been generally shut out of crypto markets due to the inability to buy spot tokens, costly and unwieldy futures products, and inefficient futures-based ETFs. Additionally, given the uncertain regulatory outlook, and general negative disposition by the SEC, many have shied away from even trying to participate. With BTC ETF approvals by the SEC, access to BTC price movement will be available at the touch of a button for this untapped market. In just 2 weeks of trading since launch, we’ve seen BTC ETFs become the second largest commodity-based ETF behind GLD (Gold). Looking at institutional flows, we see a similar dynamic playing out. Although CME futures are accessible to institutional funds and were widely used to gain exposure to the 2H price movement, the cost associated with holding and rolling them make them difficult to use as a long-term investment vehicle. Capital efficient ETFs allow asset managers of all sizes to easily participate without the previous frictions.

Bitcoin as a commodity. The designation of Bitcoin as a commodity by the Commodity Futures Trading Commission (CFTC) within the Commodity Exchange Act establishes a regulatory framework, affirming its economic significance. The statistically relevant correlation between hashrate, mining activities, and Bitcoin, underpinned by numerous academic studies, underscores the intricate relationship of cryptocurrency and energy. This interconnection places Bitcoin and its mining process in a parallel position to the energy derivative industry, analogous to the refining of oil. Recognizing Bitcoin's role as an energy derivative introduces a novel perspective on its production dynamics and energy consumption. As the cryptocurrency landscape continues to evolve, acknowledging Bitcoin's commodity status and its potential inclusion in major indices provides a robust foundation for understanding its market behavior and emphasizes its broader economic implications within the realm of commodities.

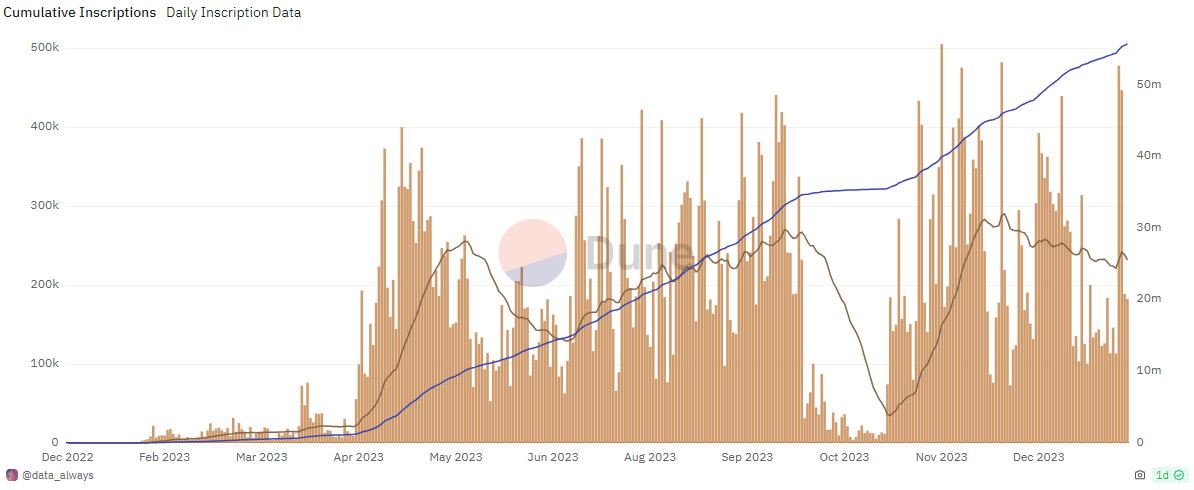

Bitcoin Layer 2 Narrative. Bitcoin Ordinals has expanded on the conventional use of the Bitcoin network, expanding its capabilities beyond simple peer-to-peer transfers. The surge in interest in ordinals during 2023 resulted in transaction fees reaching a two-year high, with non-fungible tokens (“NFTs”) and meme coins utilizing the BRC-20 token standard playing a prominent role. Ordinals, fully on-chain and inheriting Bitcoin's security characteristics, signify a powerful concept that extends the immutability of the world's most secure network to encompass digital ownership beyond currency. The economic viability of ordinals was facilitated by the Taproot upgrade (BIP 431), activated in November 2021, complemented by the 2017 SegWit upgrade. Currently, non-ordinals constitute 62% of transactions, BRC20 transactions make up 33%, and non-BRC-20 Ordinals transactions stand at 5%. The fees generated by ordinals contribute to supporting Bitcoin miners, and the activity on chain is catching the attention of innovators and developers.

Source: Dune Analytics

The Bitcoin halving shapes the network's monetary policy, occurring roughly every four years and reducing block rewards for miners. This leads to a substantial decrease in the inflation rate of newly minted Bitcoins. The most recent halving in May 2020 saw the block reward drop from 12.5 to 6.25 Bitcoins, and the next is anticipated to occur in April 2024, reducing the block reward to 3.125 BTC. This periodic reduction not only contributes to the scarcity of Bitcoin but also affects its supply dynamics. As new Bitcoin issuance decreases, miners, who secure the network, find themselves with less Bitcoin to sell. Historically, each halving has triggered price surges and prolonged bull markets, highlighting Bitcoin's unique scarcity with a fixed supply of 21 million Bitcoins. The halving events also emphasize the economic incentives in Bitcoin's design, as reliance on transaction fees increases with diminishing new supply, reemphasizing the potential importance of L2s and Ordinals on Bitcoin.

Regulations Will Continue to Be a Headwind in the US

Despite the progress made with the approval of the spot ETF, regulation will continue to weigh heavily on the entire industry throughout 2024. We note from SEC Chair Gensler’s comments following SEC ETF approval “Though we’re merit neutral, I’d note that the underlying assets in the metals ETPs have consumer and industrial uses, while in contrast bitcoin is primarily a speculative, volatile asset that’s also used for illicit activity including ransomware, [4] money laundering,[5] sanction evasion,[6] and terrorist financing.[7] While we approved the listing and trading of certain spot bitcoin ETP shares today, we did not approve or endorse bitcoin. Investors should remain cautious about the myriad risks associated with bitcoin and products whose value is tied to crypto.[8]" Not much of an endorsement. We see no change in the current path of using the courts to determine policy. Although they have lost a few high-profile cases, the SEC continues to score smaller victories in less covered, but adjacent cases. These will continue to buttress the SEC view that rules for crypto already exist and the industry should come into compliance. Two high profile cases to follow in the coming months will be the SEC v Coinbase and SEC v Binance, which could bring legal clarity to the SEC’s stance on certain tokens as securities.

The 2024 election will also serve as a guidepost for the future path of crypto legislation. We have seen several pro-crypto candidates, mostly Republicans such as Vivek Ramaswamy, positively talking about crypto as part of their platforms. Donald Trump recently came out against Central Bank Digital Currencies (“CBDCs”), which is generally a pro-crypto stance. On the other side, several high-profile Democrats, such as Sen. Warren, have made anti-crypto part of their broad campaign. While not fully pitting right versus left, it is clear that potential crypto legislation will be shaped by the next administration.

Finally, we note that although the US has not taken the lead on crypto policy, it doesn’t mean they are not watching what is happening globally. We have seen European regulators take the lead on regulating crypto with various initiatives that seem pro-crypto on the surface. Putting up the goal-posts is the first step to playing the game. We would expect the US regulators to watch closely at the success and failures of other regulators and incorporate various aspects of these policies into the final framework produced.

Other Crypto Narratives to Watch in 2024

Focus Shifts to Ethereum (ETH). The bullish 2023 narrative for BTC was largely around the launch of the ETF. The next place for institutional money to get ahead of this type of move would be to ETH. ETH is the second largest digital asset at ~$300B in total market cap and is the second most traded digital asset globally averaging ~10b/day in spot volume. It already has CME listed futures and a futures-based ETF product. Many who have gone down the crypto rabbit hole started with BTC and moved into ETH as their understanding of blockchain technology grew. A new investors base growing in BTC is likely to yield crossover into ETH. If any digital asset were to be up next for an ETF, it would likely be ETH. In fact, there are already multiple applications for an ETH ETF, including one from Blackrock. The earliest date for potential ETH ETF approval would be in May 2024, but we are skeptical that approval comes this early. We would view approval more likely to come in 2025 for several reasons. As noted above, the SEC admitted they only approved the BTC ETF because they lost in court. This may be the path issuers need to take to get an ETF approved. Despite a dim outlook for 2024 ETF approval, we do believe there are other narratives that will warrant attention to the ETH ecosystem.

One of the key narratives to observe is the upcoming Ethereum upgrade, EIP-4844, named the Cancun upgrade, represents a significant step in addressing Ethereum's key challenge—high gas fees—an obstacle to its widespread adoption. Set to roll out in Q1 of 2024, this upgrade, featuring Danksharding and leveraging 'blobs' to streamline transactions, is poised to substantially lower fees and boost transaction throughput. This development aligns with a broader trend in the blockchain space—increased interest in modularity. Modularity, encapsulating decentralized principles, involves segregating vital functions like execution, settlement, consensus, and data availability into specialized layers for customized efficiency. The adoption of modular frameworks, including rollups illustrated by projects like Celestia, underscores the industry's focus on task distribution across specialized chains, enhancing scalability and optimization. Ethereum's ongoing evolution of modular stacks continues to benefit the ETH token, as only ETH is accepted as the fee token for the base fee (the portion of the fee that is burned). This suggests that layer 2 solutions can enable users to make payments in any token of their choice, with the ultimate settlement taking place on Ethereum.

Real World Assets (RWA) and Tokenization

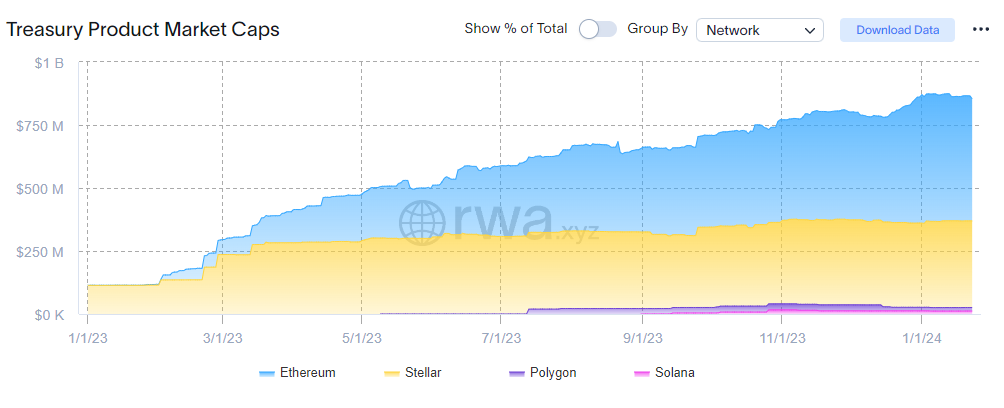

In the evolving landscape of 2024 crypto narratives, a notable trend involves Real-World Asset (RWA) tokenization, specifically in the context of tokenizing yield. Projects like Ondo Finance (ONDO) and Maple Finance (MAPLE) are at the forefront of this movement, exploring innovative ways to tokenize various real-world assets, including bonds and yields. Additionally, Ethereum is expected to play a significant role in this narrative, as it becomes a primary platform for bond issuance. Notably, Ethereum hosts $484 million in tokenized US treasuries, bonds, and cash equivalents, marking an impressive 880% year-over-year growth, with an average yield to maturity of 5.24% and weighted average maturity of 0.16 yrs. The fusion of RWA tokenization and ETH bond issuance signifies a dynamic shift in the crypto space, providing novel opportunities for investors to engage with traditional financial instruments in a decentralized manner. This narrative reflects ongoing endeavors to bridge the gap between the traditional financial realm and the emerging decentralized ecosystem.

Maple and TrueFi claim the highest total value of investments on chain, encompassing the cumulative value of all loans that each protocol has brought on chain, including private credit. Specifically, Maple records an impressive $1.8 billion, while TrueFi follows closely with $1.7 billion. In the domain of tokenized private credit, the cumulative value of all loans reaches $4.5 billion, featuring an average Annual Percentage Rate (APR) of 9.5%. These statistics underscore the substantial growth and maturation of RWA tokenization and its impact on the broader adoption and integration of blockchain technology.

Source: RWA.xyz

Traditional banking firms are acutely aware of the opportunities that blockchain presents to improve the rails of antiquated financial systems. Every major bank now has a growing team of experts examining new use cases for leveraging blockchain technology to either mitigate counterparty and settlement risks, lower costs, or both.

There are also real-world use cases for RWAs currently under various phases of adoption by the investment banking industry. These are mostly on private, permissioned, blockchains, but the evolution is underway. According to Broadridge, their permissioned chain (Distributed Ledger Repo (DLR) for Capital Markets) boasts over $70 billion per day in Repo transactions as of last summer. JPM launched their own private network (an Ethereum fork) which has been processing transactions for a few years and currently has multiple banks running proof of concepts (PoCs) for traditional financial assets. EMEA and APAC banks are further along with embracing the use of public blockchains, but these US "gateway blockchains" make for great PoCs while regulators continue to struggle to implement a framework that would allow for the technology to reach escape velocity.

Decentralized Physical Infrastructure (DePIN)

The DePIN ecosystem, that leverages blockchain and tokens for real-world infrastructure development, spans various sectors, including compute, wireless, data sales, and services. In the upcoming year, pivotal themes such as the convergence with AI, meme coins, zero knowledge technology, gaming, and privacy are expected to propel growth and foster innovation. Leading projects like Render, Helium, Arweave, Filecoin, and others, collectively holding a market cap of $21 billion, significantly contribute to the ecosystem's dynamic landscape. The ecosystem's unique position opens doors for innovative approaches, such as allowing users to anonymously sell their individual data through Zero-Knowledge proofs. This trackable but anonymous data would be able to contribute to machine learning models through decentralized rails, envisioning a future where individuals are compensated for their data. Any business that benefits from selling metadata (think car driving statistics, cell phone geo location, credit card data, etc.) is a prime target to be innovated on, allowing users to be rewarded for the data they provide towards algorithms.

Meme Coins

The intersection of meme coins with broader market trends, exemplified by Solana's successful Bonk airdrop, suggests a notable shift in market dynamics. Meme coins resemble the communal nature observed with NFTs. Buying into meme coins early creates a sense of community, akin to the camaraderie seen in NFT groups, and holding meme coins may lead to airdrops, mirroring the residual benefits of NFT ownership. Despite fungibility differences, meme coins, like NFTs in the previous bull market, exhibit a high beta potential. The Solana Phones' success, initially unnoticed in the smartphone market, gained traction when the BONK meme coin's decentralized application distributed 30 million BONK tokens to phone owners, essentially covering the cost of the phone and sparking a surge in demand. This model of combining meme coins with tangible rewards is gaining momentum, creating a compelling narrative for their potential success in this market cycle.

Sources: Bloomberg, Dune Analytics, Ethereum Foundation, Coinmarketcap