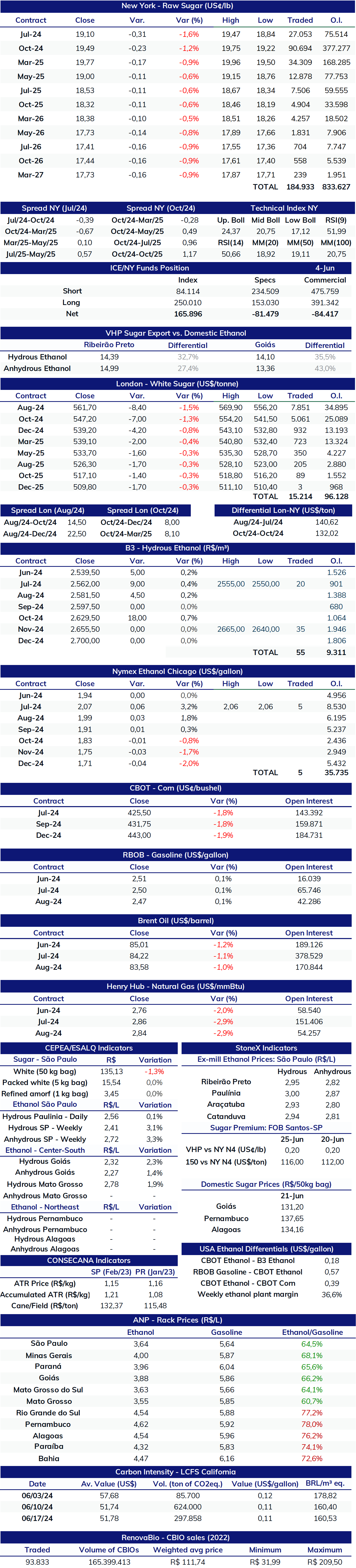

Last week (June 16 to June 22), hydrous ethanol prices in the state of São Paulo, the main consumer, closed at an average of BRL 3.64/liter. This was a constant value compared to the previous week. The spot market, on the other hand, saw a significant increase in the value of the biofuel - the StoneX indicator (base Ribeirão Preto, including taxes) went from BRL 2.83/liter to BRL 2.95/liter. At the pumps, the parity between ethanol and gasoline showed a subtle drop, from 64.77% to 64.53% in the state of São Paulo, which is still favorable to hydrous consumption.

Hydrous ethanol price* - (BRL/liter)

*In the Ribeirão Preto (SP) mills, with ICMS. Sources: StoneX, ANP. Design: StoneX.

*In the Ribeirão Preto (SP) mills, with ICMS. Sources: StoneX, ANP. Design: StoneX.

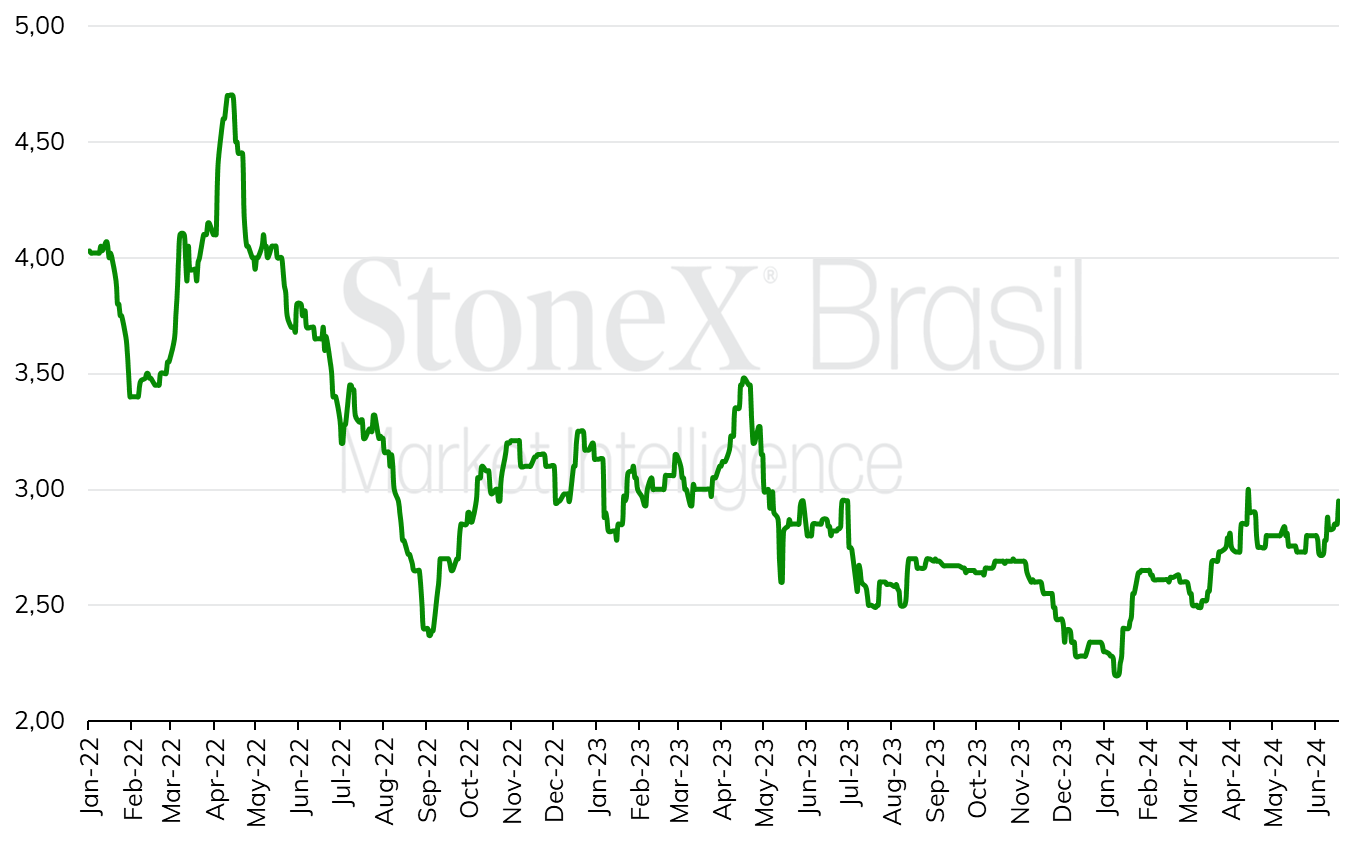

Last Thursday, the ANP released preliminary fuel consumption figures for the month of May. Following the trend of recent months, the figures show a strong increase in demand for hydrous ethanol at the pumps, at 1.85 million m³ during the fifth month of the year, an increase of 53.7% compared to the same period in 2023. The increase once again reflects the strong gain in hydrous ethanol's share of sales at service stations, as the biofuel has shown more favorable parity levels since June 2023 in the main consuming region.

As a result, the share of hydrous ethanol already represents 25.8% of the demand for light vehicle fuels in 2024, compared to 17.3% in the same period in 2023. Due to this increase, demand for gasoline continues to fall, standing at 3.64 million m³ in May, 12.8% less than in the same period last year, even though aggregate demand for the Otto cycle (hydrous ethanol + gasoline) remains high.

In this context, the trend should continue to be for high sales of hydrous ethanol in the coming months, both because of the growth in supply until the peak of the crop, between August and September, and because of the inertial behavior of demand, with end consumers getting used to filling up with ethanol after long months of favorable parity. However, the expectation is that parity could exceed 70% in São Paulo, especially in the first quarter of 2025, therefore reducing ethanol consumption by end consumers.

Parity between ethanol and gasoline in the state of São Paulo (%)

Source: ANP Design: StoneX

Source: ANP Design: StoneX

Daily recap

On Tuesday (25), raw and white sugar prices recorded a day of decline on the futures markets. Raw #11 was down 1.17%, ending the day at US¢ 19.49/lb for the most liquid contract (SBV4), with white down 1.47% over the period, ending the day at US$ 561.7/t. After climbing at the beginning of the week, prices continue to be pressured by the progress of the 2024/25 crop (Apr-Mar) in the Center-South and the progress of the rains in India. Sugar has bearish fundamentals due to the prospect of surpluses during the 2023/24 and 2024/25 seasons, whose balances are estimated at 3.9 MMT and 2.5 MMT, respectively, as a result of still high production in Brazil and a production recovery in players like Thailand and China.