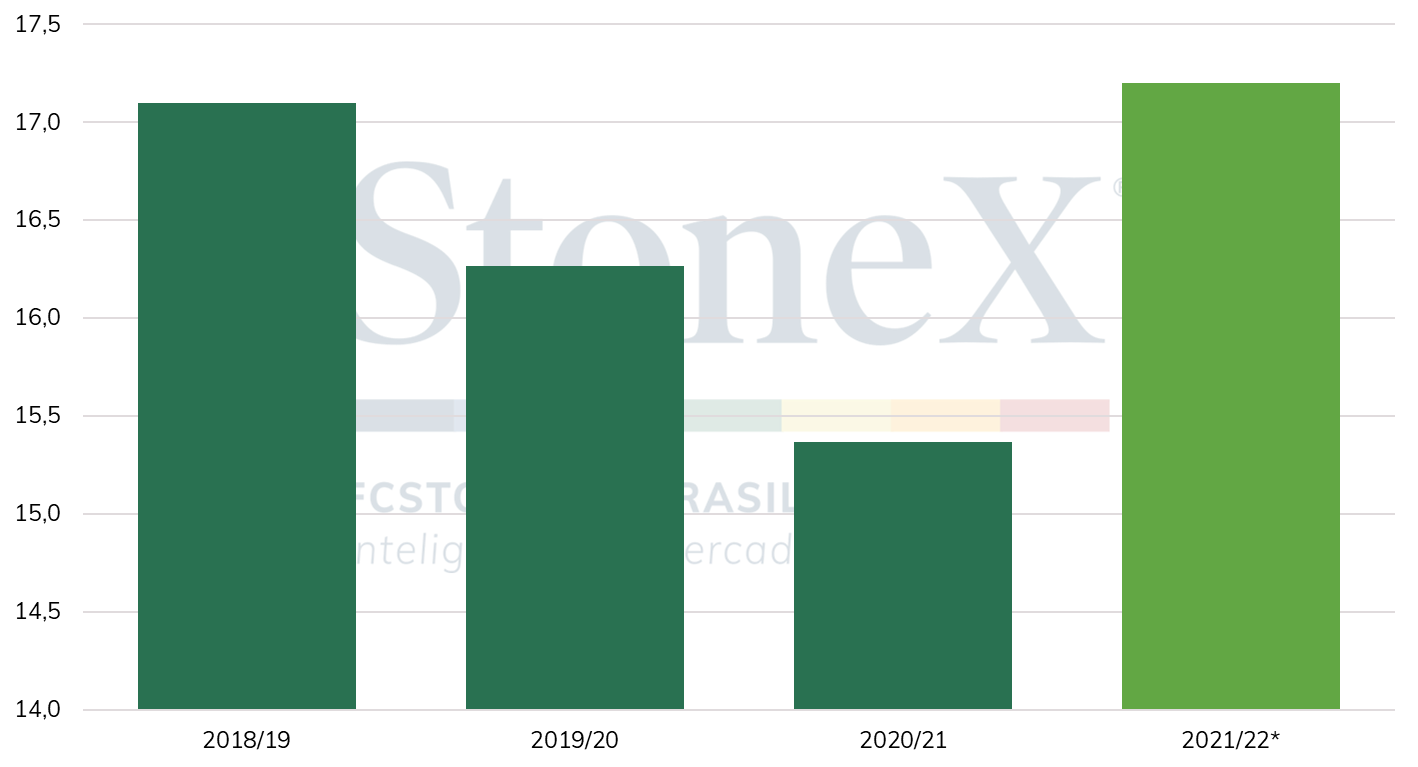

*Estimated. Sources: European Commission & StoneX. Design: StoneX.

In a long-term horizon, however, demand for sugar can be reduced by changes in consumption patterns, which tends to make the region a net sugar exporter from 2027/28.

On the 2022/23 crop, the allowed use of neonicotinoids continues to be one of the main discussions about beet crops’ productivity. Although France has approved its use, Germany has not allowed applications in order to mitigate environmental damage, which, on the other hand, can hinder beets’ productive potential in the country.

This condition is aggravated by the warmer temperatures of recent weeks, a trend that is expected to continue until the beginning of April and which, consequently, increases the risk of aphid infestation. In light of this weather situation, the United Kingdom also approved the use of neonicotinoids in 2022.

In terms of rains, models also point to within-normal moisture in the coming months, which is positive for field work advancement, as well as development of the crops that will be processed in the next cycle.

Although the allowed use of neonicotinoids and the prospects of regular rainfall may favor beet productivity in some countries, there is little room for production gains via acreage increase. Specifically in France, the Ministry of Agriculture (Agreste) forecasts a 3% YoY area decline in 2022/23, which may be close to 400,000 hectares. If confirmed, this may be the fifth consecutive crop with planted area loss in the country. A similar scenario is expected for Poland, given higher attractiveness of cereals and rapeseed, which also present lower production costs.

Based on this discussion, we expect a slight drop in sugar production by the bloc in 2022/23. These points will need to be closely monitored in the coming weeks in order to assess the productive potential of the European Union and the United Kingdom.

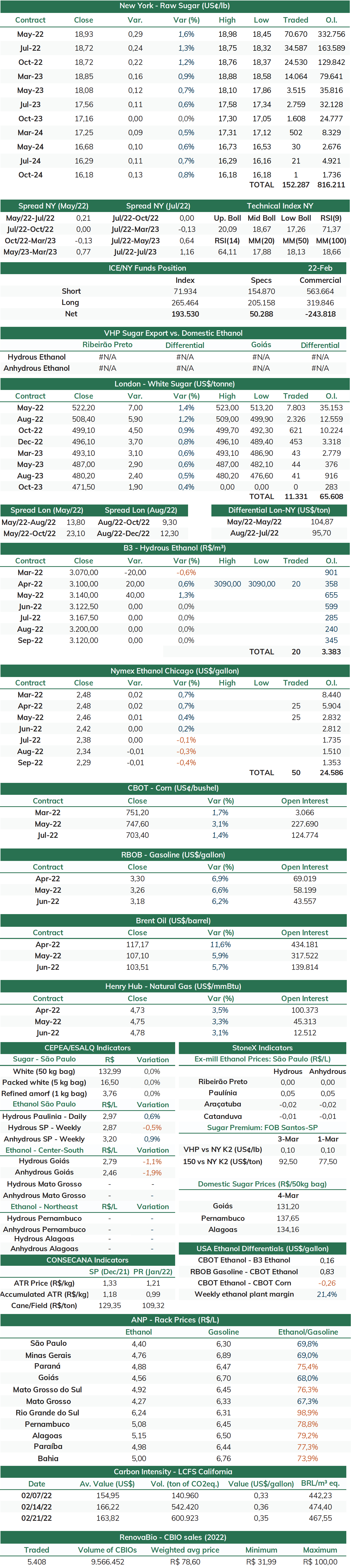

Finally, the market also monitors the move higher in the energy complex, which could stimulate Indian investments to reach E20 by 2023 in order to decrease its dependence on the global oil sector. Following this dynamic, the sugar #11 May/22 contract closed the ICE/NY session accumulating a daily increase of 1.6% to 18.93 c/lb. However, the 9-day RSI already exceeds 70 points, indicating an overbought situation in the market.