Every year, markets deliver at least a few surprises, and 2025 was no different. Among the major economic and political developments - from the application and reversal of massive reciprocal tariffs to the intensified appetite for AI-related exposure to a US government shutdown - these are a few highlights that top Matt Weller’s and John Kicklighter’s lists.

Talking Points:

There were plenty of market surprises in terms of fundamental developments or unexpected market moves, but the more astounding developments proved more foundational in nature

An erosion of the traditional fundamental order – policy influence, key event risk impact and erosion in the quality of data – can change the trading landscape

Why USDJPY and Gold turned out to be two of the most surprising markets of 2025

To sign up for the Trading Global Macro podcast, find it on your preferred podcast platform: Apple Podcasts, Spotify, or YouTube.

This past year, risk appetite held firm through a macro tariff jolt that nearly tipped the S&P 500 into an official, technical ‘bear market’. For many, that would be surprise enough, but the activity through the year exposed perhaps more deeply rooted abnormalities. A material drop in policy-market influence, a fading impact from key event risk and growing questions over the quality of key data series seems to have changed the landscape.

Looking back over these anomalies isn’t simply an academic exercise. It can help us to understand systemic shifts in the tectonic nature of the market. Determining why markets responded (or failed to respond) to supposed major catalysts in 2025 may be one of the most important guides for navigating 2026.

And with those considerations in mind, we look at the top surprise from particular markets of the past year to gauge whether those moves are perhaps a reflection of the structural upheaval – rather than intrinsic fundamental developments that traders typically look for explanation..

A Year of Big Policies and Small Reactions

Perhaps the most striking development of 2025 was the disparity between major policy shifts and the market’s surprisingly muted reaction.

The Liberation Day tariff rollout was delivered with uncertainty, inconsistency, and in some cases conflicting messages about rates and targeted regions. Historically, such conditions would weigh on business investment expectations and risk sentiment through the medium to long term.

Yet following the sharp April selloff - one that nearly earned the S&P 500 it ‘bear market’ status – sentiment snapped back with remarkable speed. By early summer, most of the tariff-driven losses had been erased and record highs were soon restored. That recovery seemed to ignore or discount the lasting inflation concern, growth restriction and international upheaval that lasted further into the year.

Two broad dynamics may help to explain this distortion rather than define new conditional norms:

Faster Rotation of Investor Priorities - Markets may not be dwelling on single dominant narratives for long. Themes such as interest-rate expectations, recession fears, tariff policy, and earnings growth can cycle out of top relevancy more quickly. And, when no single concern remains dominant, the market’s tendency to rotate will increase.

AI and Other Sentiment-Driven Themes Fuel Complacency - Despite policy uncertainty, expectations for continued revenue expansion and ongoing productivity gains from AI-related investment overshadowed macro concerns. Even the strongest policy shocks had trouble competing with the “ever-rising profits” mindset that defined 2025

Chart of S&P 500 and Key Geopolitical Dates (Daily)

Source: John Kicklighter, Standard & Poor’s

Event Risk Like the NFPs and FOMC Rate Decision Lose Traction

One of the perhaps subtler, but more consequential, surprises was the sharp moderation in market sensitivity to scheduled event risk.

After the tariff shock faded, realized volatility collapsed. Measures like the average true range trended sustainably lower, resulting in smaller swings and corrections to the larger bull trend over time. This period was punctuated by consequential and frequently surprising updates via traditionally-impactful event risk – such as the US CPI and Change in NFPs – that seemed to be received more as mild noise rather than true catalysts of serious swings or trend development.

This was especially notable given the underlying conditions:

Inflation re-accelerated during parts of the year

Nonfarm payrolls trended lower

A federal government shutdown that materially boosted political uncertainty

Any of these would normally serve as a spark to something larger for the capital markets. Instead, the market seemed to move on without as much as formally acknowledging the update. The lowered signal power was perhaps most on display with the December FOMC rate cut where the central bank cut rates, restarted its QE at a slower pace and poured cold water on expectations for significant cuts in 2026. Despite all of that, equities kept to their slow grind higher and the Dollar held its own large range.

Chart of the S&P 500 with Key FOMC Decisions, 5-Day / 20-Day ATR Ratio (Daily) Source: John Kicklighter, Standard & Poor’s

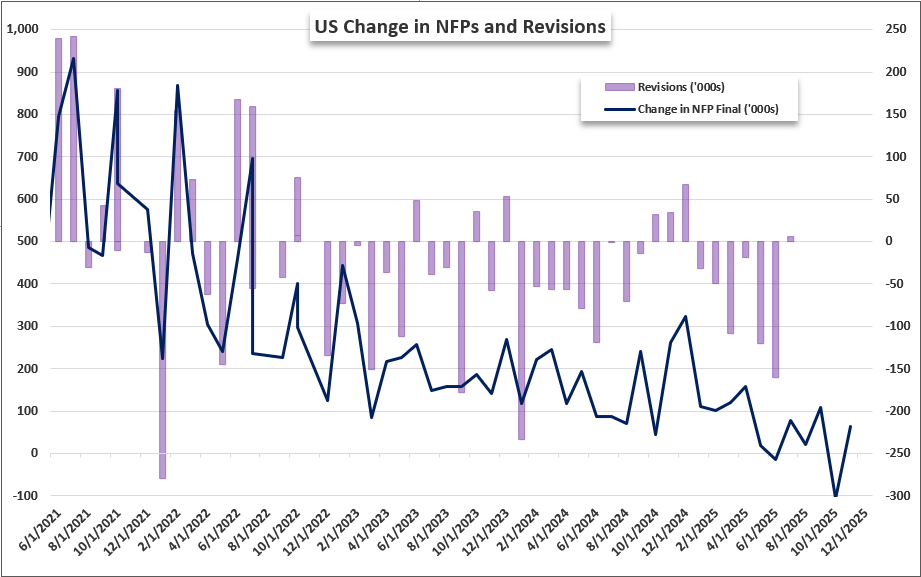

Confidence in Core Data is Fading

Another major shift in 2025 was a growing scepticism about the quality and reliability of survey-based economic indicators.

A big story in 2025 was the substantial revisions for past released NFP numbers, which drew serious criticism from market participants and from the White House. Meanwhile, the favored inflation indicator, the CPI, saw an increasing disconnect between the headline reading as it moved backed towards the target rate while Americans remarked that they felt that affordability of homes, groceries and other necessitates was increasingly moving out of reach. Explanations of changing data collection mythologies and stagnating response rate to surveys would spread to the mainstream.

A reflection here may be the nature of sentiment itself. Consumer sentiment reports swung sharply following Election Day - almost entirely along political lines - despite no rapid change in underlying economic conditions. In a world where perception increasingly diverges from measurement, markets appear to be leaning less on traditional economic data and more on:

This recalibration may further help explain why event risk failed to drive sustained market moves and there remains little consistency in dominant fundamental themes.

Chart of NFPs and Revisions (Monthly) Source: US Bureau of Labor Statistics, John Kicklighter

Top Suprises Among Top Markets: USDJPY and Gold

USD/JPY was perhaps one of the most ‘conflicted’ markets of 2025 – or at least the one that most thoroughly deviated from its traditional fundamental drivers. Historically, the pair has hewed closely to the carry trade reflected in yield differentials as well as the ebb and flow of risk appetite trends. After decades of zero or near zero rates, the Japanese Yen has adopted the role of the consummate ‘funding currency’. That remains to this day even as the BOJ slowly raises its rate. Meanwhile, low yield potential urges Japanese investors to invest abroad for meaningful returns; which translates into a directional flow when global risk aversion leads those same investors to repatriate their capital.

Despite these norms, the typically-strong correlation between the USDJPY exchange rate and US-Japan 2-year yield differential (the tenor most associated to monetary policy) has diverged extraordinarily. The low volatility environment could be argued to be an environmental backdrop that would keep the drive towards the higher yield, but the direction of that yield differential conflicts with that narrative – not to mention recent spikes have all but been ignored.

Chart of USDJPY Overlaid with US-Japan 2-Year Yield Spread, VIX Inverted (8 Hour)

Source: TradingView.com

No retrospective on 2025 would be complete without reflecting upon the extraordinary performance of gold. Rising from roughly $2,600 to over $4,300 per ounce over the course of the year, the more than 66 percent increase on the year was one of the strongest among major markets. Notably, this move occurred despite real yields that bottomed out at historically-higher levels and the perception of financial risks holding to low levels, which is not especially supportive of such a robust performance for the precious metal.

What could have driven this counter-macro surge? More systemic concerns over the stability of traditional fiat currency could be a meaningful driver. Along similar lines, long-term inflation uncertainty and declining trust in institutions as well as economic data can benefit the more ‘transparent’ fundamentals of the metal.

Gold has existed for millennia, but few expected a near doubling in a year that did not feature a major financial crisis or geopolitical shock. Its performance may be a referendum on broader structural issues that continue to simmer beneath the surface.

Chart of Spot Gold and the 20-Day Rate of Change (Daily)

The subsidiaries of StoneX Group Inc. provide financial products and services, including, but not limited to, physical commodities, securities, clearing, global payments, risk management, asset management, foreign exchange, and exchange-traded and over-the-counter derivatives. These financial products and services are offered in accordance with the applicable laws in the jurisdictions in which they are provided and are subject to specific terms, conditions, and restrictions contained in the terms of business applicable to each such offering. Not all products and services are available in all countries. The products and services offered by the StoneX Group of companies involve risk of loss and may not be suitable for all investors. Full Disclaimer.

This content is not intended for residents of any particular country, and the information herein is not advice nor a recommendation to trade nor does it constitute an offer or solicitation to buy or sell any financial product or service, by any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation. Please refer to the Regulatory Disclosure section for entity-specific disclosures.

No part of this material may be copied, photocopied or duplicated in any form by any means or redistributed without the prior written consent of StoneX Group Inc. The information herein is provided for informational purposes only. This information is provided on an ‘as-is’ basis and may contain statements and opinions of the StoneX Group of companies as well as excerpts and/or information from public sources and third parties and no warranty, whether express or implied, is given as to its completeness or accuracy. Each company within the StoneX Group of companies (on its own behalf and on behalf of its directors, employees and agents) disclaims any and all liability as well as any third-party claim that may arise from the accuracy and/or completeness of the information detailed herein, as well as the use of or reliance on this information by the recipient, any member of its group or any third party.

Currencies

The subsidiaries of StoneX Group Inc. provide financial products and services, including, but not limited to, physical commodities, securities, clearing, global payments, risk management, asset management, foreign exchange, and exchange-traded and over-the-counter derivatives. These financial products and services are offered in accordance with the applicable laws in the jurisdictions in which they are provided and are subject to specific terms, conditions, and restrictions contained in the terms of business applicable to each such offering. Not all products and services are available in all countries. The products and services offered by the StoneX Group of companies involve risk of loss and may not be suitable for all investors. Full Disclaimer. This content is not intended for residents of any particular country, and the information herein is not advice nor a recommendation to trade nor does it constitute an offer or solicitation to buy or sell any financial product or service, by any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation. Please refer to the Regulatory Disclosure section for entity-specific disclosures. No part of this material may be copied, photocopied or duplicated in any form by any means or redistributed without the prior written consent of StoneX Group Inc. The information herein is provided for informational purposes only. This information is provided on an ‘as-is’ basis and may contain statements and opinions of the StoneX Group of companies as well as excerpts and/or information from public sources and third parties and no warranty, whether express or implied, is given as to its completeness or accuracy. Each company within the StoneX Group of companies (on its own behalf and on behalf of its directors, employees and agents) disclaims any and all liability as well as any third-party claim that may arise from the accuracy and/or completeness of the information detailed herein, as well as the use of or reliance on this information by the recipient, any member of its group or any third party.

Our market expertise, advanced platforms, global reach, culture of full transparency and commitment to our clients’ success all set us apart in the financial marketplace.

Reach

With access to 40+ derivatives exchanges, 180+ foreign exchange markets, nearly every global securities marketplace and numerous bi-lateral liquidity venues, StoneX’s digital network and deep relationships can take clients anywhere they want to go.

Transparency

As a publicly traded company meeting the highest standards of regulatory compliance in the markets we serve, our financials and record of accomplishment are matters of public record. StoneX’s commitment to “doing the right thing over the easy thing” sets us apart in the industry and helps us build respect, client trust and new partnerships.

Expertise

From our proprietary Market Intelligence platform, to “boots on the ground” expertise from award-winning traders and professionals, we connect our clients directly to actionable insights they can use to make more informed decisions and achieve their goals in the global markets.