EIA Weekly Nat Gas Storage Update

EIA Weekly Nat Gas Storage Update

Tom Pawlicki

- Energy

By: Tom Pawlicki, Senior Specialist, Market Intelligence

Former Venezuelan President Maduro’s capture early Saturday morning by US forces started the initial clean-up of one of several geopolitical issues with which oil markets have been tracking. While initial reactions may anticipate the country’s oil production rising, it is likely to take a considerable amount of time and investment before production and exports from the country begin to rise.

In President Trump’s Saturday morning press conference after Maduro’s capture, he talked about the Maduro’s arrest as being a law enforcement action due to Maduro’s being an indicted drug warlord. However, President Trump also spent time discussing oil, both in regards to getting back prior US investments in Venezuela and with the investment that US companies are ready to make. Estimates today suggest a cost of at least $100 bln over 10 years.

It would be natural to assume that Venezuela will see potential increases in oil production, but that is unlikely as the country’s infrastructure is in a state of disrepair. Pipelines have been pillaged for scrap metal and drilling platforms have been dismantled and sold for parts. President Trump also said that the oil embargo would remain in place, which could indicate that Venezuelan oil will continue to have difficulty being exported. With Maduro’s unelected Vice-President Delcy Rodríguez taking over as acting president, it will remain to be seen whether she will be acceptable to US leadership and allow political conditions to stabilize. There is also the issue of neighboring countries to consider, with President Trump and Secretary of State Marco Rubio discussing Colombia, Cuba and even Mexico. Given those countries’ interconnections with Venezuela, the oil market may feel the need to maintain a degree of geopolitical risk premium. Those factors may better explain why oil prices rallied nearly $1.00/bbl today instead of falling.

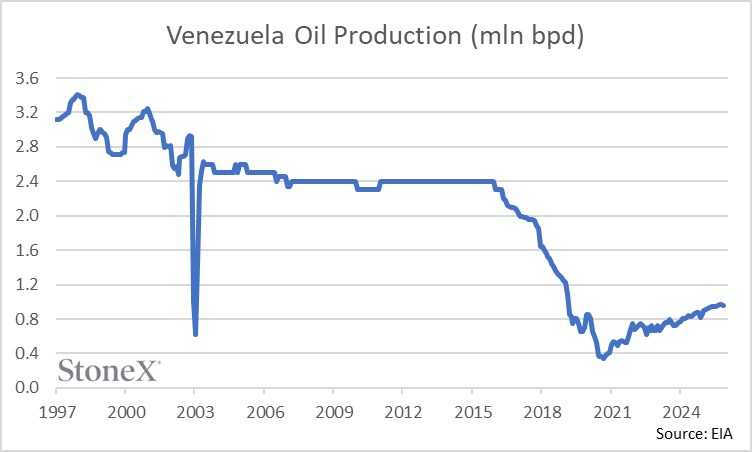

The US EIA has published Venezuelan oil production data going back to 1997. It shows production reaching a peak of 3.41 mln bpd in December 1997 and a sharp decline in late-2002. The decline was the result of a large-scale oil and general strike organized by groups opposed to Hugo Chavez starting on December 2. Production was nearly flat for 12 years from 2004-2016 but started to decline in 2016 due to the price collapse in 2014-2015. In those two years, WTI oil prices fell from $107.70/bbl to $34.50/bbl due to a boom-bust cycle in US shale. That forced Venezuela’s investments in maintenance and oilfield development to drop substantially. President Trump in his first term added sanctions on Venezuela’s oil in 2018 &2019, which caused production to drop further.

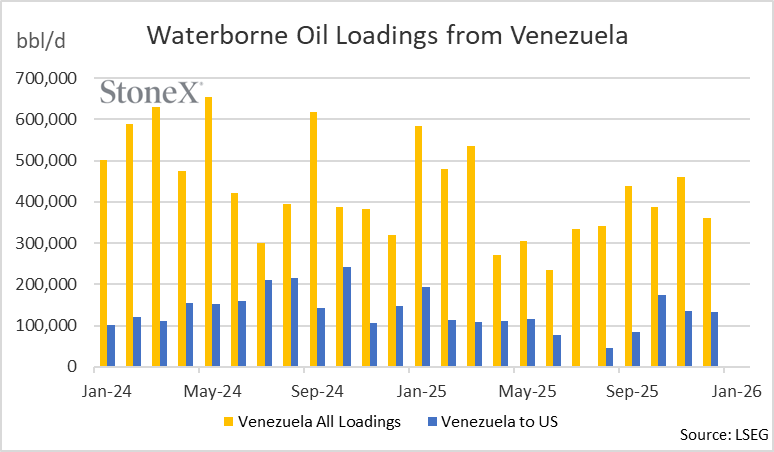

Although prices are higher now compared to 2015 at $58/bbl, it’s uncertain whether that is high enough to encourage massive new investment, considering the political risks still inherent in the country. The oil market is also oversupplied due to OPEC+ increases in output in 2025. The cartel halted its production hikes during Q1 2026 which could offer support to oil prices, but a resumption of output hikes later in the year could put the idea of Venezuelan investment under pressure yet again. Venezuelan production has rebounded from lows made in 2020 but is still significantly below the levels from the 2000s and 2010s. Monthly waterborne exports show numbers around 300,000-400,000 bpd, with exports to the US typically reaching 100,000-200,000 bpd due to shipments from Chevron.

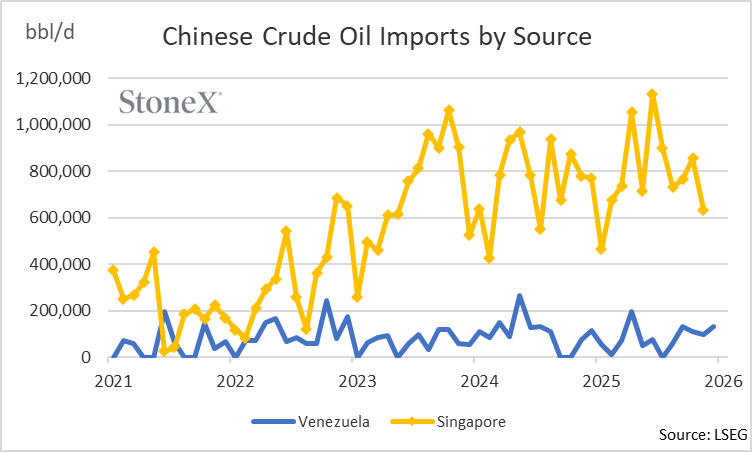

Some Venezuelan oil is shipped to China, but the exact quantities may be uncertain. Reuters data on waterborne shipments to China show an average of 82,000 bpd in 2025, which would equate to roughly 15 VLCC loadings during the year. That number seems small considering the constant use of a shadow fleet. China has been investing in Venezuela and spoke out against the capture of Maduro. The impact on China of a reduction in its influence in South America was discussed today by StoneX’s Arlan Suderman. China’s imports from Venezuela are uncertain, due to the transshipment through intermediary countries. China imported 779,000 bpd from Singapore in 2025 even though that country does not produce much crude oil. It is believed that most of China’s imports from Singapore are from sanctioned sources such as Russia, Iran and Venezuela and reclassified as coming from Singapore.

The lengthy time to repair and redevelop Venezuela’s oil industry should explain the relatively small and even positive reaction by the oil market today. It may also be worth considering past examples for analogs. The capture of Maduro is similar to Operation Just Cause in Panama to get Manuel Noreiga. Panama is not an oil producing country, but it is strategic because of the Panama Canal. The US started the operation on December 20, 1989 with oil at $21.21/bbl. Noreiga surrendered on January 3, 1990 with oil at $23.68/bbl. The price that day rose 79c/bbl, and prices finished the month of January at $22.68/bbl.

Small price moves were also seen during the overthrow of Muammar Gaddafi in Libya. It started on September 15, 2011 with the National Transitional Council being recognized as the official government. Prices were $89.40/bbl that day. Gaddafi was captured and killed on October 20, 2011, with oil prices at $85.81/bbl. Prices finished October at $93.19/bbl. Libya’s oil production had slowed to a trickle in the months leading up to Gaddafi’s end and rebounded to pre-crisis levels within six months.

While political conditions in Venezuela experienced a large change over the weekend, the country is unlikely to experience much immediate change in oil production. Assuming the government stabilizes and welcomes investment, that investment will take several years to bear fruit. Past examples suggest that oil prices don’t usually witness large reactions to these kinds of geopolitical events.

This material should be construed as market commentary and represents the opinions and viewpoints of the author, and does not reflect tailored advice associated with any specific account.

The views are current only through the date stated and are subject to change at any time based upon market or other conditions, and StoneX Group Inc. (“SGI”) disclaims any responsibility to update such views. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources. Past performance does not guarantee future results.

The StoneX Group Inc. group of companies provides financial services worldwide through its subsidiaries, including physical commodities, securities, exchange-traded and over-the-counter derivatives, risk management, global payments and foreign exchange products in accordance with applicable law in the jurisdictions where services are provided.

References to certain OTC products or swaps are made on behalf of StoneX Markets, LLC (SXM), a member of the National Futures Association (NFA) and provisionally registered with the U.S. Commodity Futures Trading Commission (CFTC) as a swap dealer. SXM’s products are designed only for individuals or firms who qualify under CFTC rules as an ‘Eligible Contract Participant’ and who have been accepted as customers of SXM.

StoneX Financial Inc. (SFI) is a member of FINRA/NFA/SIPC and registered with the MSRB. SFI is registered with the U.S. Securities and Exchange Commission (SEC) as a Broker-Dealer and with the CFTC as a Futures Commission Merchant and Commodity Trading Advisor. StoneX Financial (Canada) Inc. (SFCI) is registered in Canada and is a member of CIRO and CIPF. References to certain securities trading are made on behalf of the BD Division of SFI and are intended only for an audience of institutional clients as defined by FINRA Rule 4512(c). References to certain exchange-traded futures and options are made on behalf of the FCM Division of SFI. Wealth Management is offered through SA Stone Wealth Management Inc., member FINRA/SIPC, and SA Stone Investment Advisors Inc., an SEC-registered investment advisor, both wholly owned subsidiaries of SGI.

R.J. O’Brien & Associates, LLC (RJO) is registered with the CFTC as a Futures Commission Merchant and is a member of NFA.

StoneX Financial Ltd (SFL) is registered in England and Wales, company no. 5616586. SFL is authorized and regulated by the Financial Conduct Authority (FCA) (registration number FRN:446717) to provide services to professional and eligible customers including: arrangement, execution and, where required, clearing derivative transactions in exchange traded futures and options. SFL is also authorized to engage in the arrangement and execution of transactions in certain OTC products, certain securities trading, precious metals trading and payment services to eligible customers. SFL is authorized and regulated by the FCA under the Payment Services Regulations 2017 for the provision of payment services. SFL is a category 1 ring-dealing member of the London Metal Exchange. In addition SFL also engages in other physically delivered commodities business and other general business activities which are unregulated and not required to be authorized by the FCA.

This communication is issued in the European Economic Area by StoneX Financial Europe GmbH (SFEG). StoneX is the trade name used by STONEX GROUP INC. and all its associated entities and subsidiaries. StoneX Financial Europe GmbH (“SFEG”) is a securities trading firm registered in Germany under Company No. HRB 80844.

StoneX Financial Pte Ltd (Co. Reg. No 201130598R) (“SFP”) is regulated by the Monetary Authority of Singapore and is a Capital Markets Service Licence holder (for dealing in capital market products), an Exempt Financial Adviser (for advising on investment products and issuing or promulgating analyses/ reports on investment products) and a Major Payment Institution (for domestic and cross-border money transfer services).

SFP may distribute analysis/report produced by its respective foreign affiliates within the StoneX Group of companies pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations Recipients should contact SFP at (65) 6309 1000 for any matters arising from, or in connection with, this webinar.

StoneX APAC Pte. Ltd. (“SAP”) (Co. Reg. No 200616676W) is regulated as a Dealer (PS20190001002) under the Precious Stones and Precious Metals (Prevention of Money Laundering and Terrorism Financing) Act 2019 for purposes of anti-money laundering and countering the financing of terrorism.

StoneX Financial (HK) Limited (CE No.: BCQ152) (“SHK”) is regulated by the Hong Kong Securities and Futures Commission for Dealing in Securities and Dealing in Futures Contracts.

StoneX Financial Pty Ltd (ACN 141 774 727) holds an Australian Financial Service License (AFSL: 345646) for Dealing in Securities, Exchange-Traded Derivatives Contracts, OTC Derivatives Contracts and Foreign Exchange Contracts, and is regulated by the Australian Securities and Investments Commission.

StoneX Securities Co., Ltd. (“SSJ”) (Co. Reg. No 010401047199) is regulated by the Japanese Financial Services Agency as a Type-I Financial Instruments Business Operator (Kanto Local Finance Bureau (FIBO)No.291’), is a member of the Financial Futures Association of Japan for dealing and broking FX and FX Option transactions, and is a member of the Japan Securities Dealers Association for dealing and broking stock indices and option transactions.

Trading swaps and over-the-counter derivatives, exchange-traded derivatives and options and securities involves substantial risk and is not suitable for all investors. Past performance of any futures or option is not indicative of future success. Indicators are not a trading system and are not published as a specific trade recommendation. The information herein is not a recommendation to trade nor investment research or an offer to buy or sell any derivative or security. It does not take into account your particular investment objectives, financial situation or needs and does not create a binding obligation on any of the StoneX group of companies to enter into any transaction with you. You are advised to perform an independent investigation of any transaction to determine whether any transaction is suitable for you. No part of this material may be copied, photocopied or duplicated in any form by any means or redistributed without the prior written consent of StoneX Group Inc.

The report/analysis herein is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

© 2026 StoneX Group Inc. All Rights Reserved.

Our subscribers have access to comprehensive market analysis from StoneX spanning commodities, equities, currencies and more.

EIA Weekly Nat Gas Storage Update

Summary of the weekly U.S. EIA Natural Gas Storage Report – NG storage for the U.S. and by region.

June 4 – Crude oil prices dropped along with Treasury yields after yet another ceasefire agreement was reached between Israel and Lebanon, raising hopes of a peace agreement with Iran. Yet, stocks are mixed this morning, with the Dow higher and the S&P and Nasdaq lower. The VIX is again trading near 16 this morning, while the dollar index fell back into its comfort zone near 99.2 following yesterday’s rally. Yields on 10-year Treasuries are trading near 4.46%, while yields on 2-year Treasuries are trading near 4.03%. WTI crude oil is trading near $93 per barrel, while Brent trades near $95 per barrel. Wheat prices again managed a modest bounce overnight, but corn and soybean prices saw more follow-through selling on their recent downward momentum, with July corn hitting new contract lows on favorable Midwest weather and emerging demand concerns.

Our market expertise, advanced platforms, global reach, culture of full transparency and commitment to our clients’ success all set us apart in the financial marketplace.

Reach

With access to 40+ derivatives exchanges, 180+ foreign exchange markets, nearly every global securities marketplace and numerous bi-lateral liquidity venues, StoneX’s digital network and deep relationships can take clients anywhere they want to go.

Transparency

As a publicly traded company meeting the highest standards of regulatory compliance in the markets we serve; our financials and record of accomplishment are matters of public record. StoneX’s commitment to “doing the right thing over the easy thing” sets us apart in the industry and helps us build respect, client trust and new partnerships.

Expertise

From our proprietary Market Intelligence platform, to “boots on the ground” expertise from award-winning traders and professionals, we connect our clients directly to actionable insights they can use to make more informed decisions and achieve their goals in the global markets.