Weekly Base Metal Macro Economic Slides

Base Metals LME Report by Natalie Scott-Gray

Natalie Scott-Gray

- Base Metals

By: Natalie Scott-Gray, Senior Metals Demand Analyst, EMEA and Asia region

“As a consequence of the new position restrictions imposed by the Exchange, LME trading volumes and open interest have dropped to the multi-year lows as traders and investors are remaining on the sidelines and are rapidly cutting their exposure to the LME as a result of the March short squeeze”.

“The growing reluctance of market participants to trade in this market is also limiting further potentials of any sizeable short-selling activity. The decline in liquidity was accompanied by a lower speculative activity. In mid-May, net long positions of investment funds declined by over –60% comparing with mid-February, which reflects widespread unease among the market participants. However, one may see all this as a viable opportunity for the nickel producers and users to minimize the speculative component of the LME nickel pricing and start concluding deals based on the physical market fundamentals. An alternative pricing mechanism could be in sight for the physical market in order to avoid speculative price volatility”.

“In spite of certain challenges in logistics and deliveries of equipment, spares and consumables due to the complicated geopolitical situation, the Company’s operations remain unaffected.”

“ The company continues to fulfil all its obligations in full, our clients do not pull out of contracts, therefore, our trade and cash flows remain fully on schedule and in accordance with the existing contractual agreements. We see that our customers are keen to enhance their cooperation with the Company even further as Nornickel has proved its status as a highly reliable business partner through many decades of seamless co-operation and regardless of external geopolitical shocks.”

“Taking into account the current situation, Norilsk Nickel confirms the previously announced nickel production guidance from our own Russian feed for 2022 to be within the earlier announced range of 205-215 kt Ni.”

“It is important to remember that the exclusion of Russian nickel from the trade system would be disastrous for the LME and the global nickel market as Nornickel’s share in high-grade nickel production was about 20% in 2021. The potential impact on the European market would be even larger given nickel’s essential role in achieving the long-term goals of the European Green Deal and carbon neutrality as well as the importance of the low-carbon nickel for the EU battery programme, which implicitly relies on Nornickel’s ESG-compliant metal”.

“However, history shows that current prices are still likely to impact the demand negatively. In 2007, when nickel price averaged above $37,000/t, the market recorded a 4% decline in nickel use. Therefore, in our base case scenario, we expect the 2022 primary nickel demand growth to slow down to +11% as opposed to the 2021 level of +17% reflecting the current price environment, high inflation across major economies and uncertain macroeconomic outlook”.

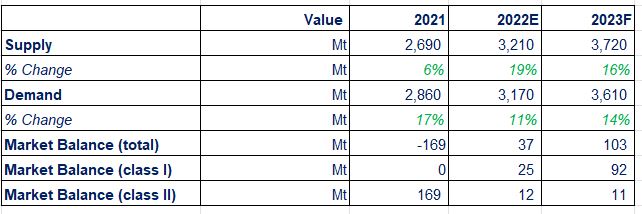

SUPPLY & DEMAND FORECASTS - BROKEN DOWN

TABLE OF FORECAST NICKEL SUPPLY, DEMAND & MARKET BALANCE

In more detail:

Output to be driven by “huge growth” in Indonesian NPI capacities (1.1Mt, +33% Y/Y), in addition to growth from nickel compounds for EV batteries (the launch of HPAL capacities and NPI-to-matte conversion lines)

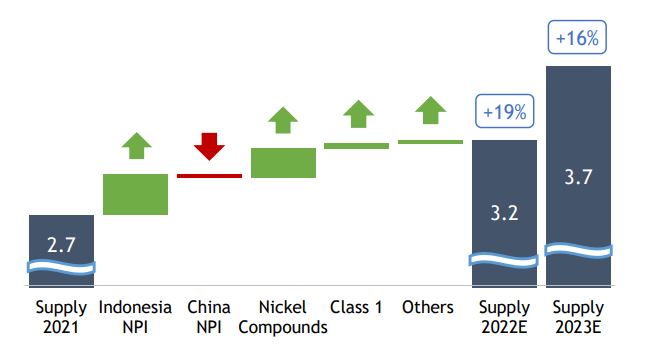

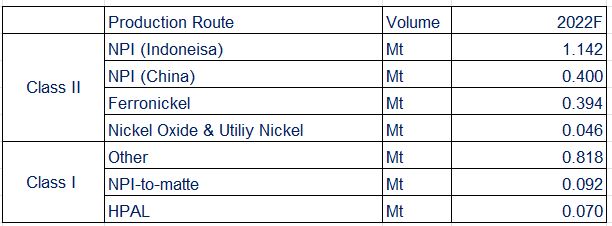

Production of Class II Material

• NPI output within Indonesia is set to reach 1.142 Mt in 2022 (with 0.428Mt domestically absorbed, 0.684Mt available to China and 0.03Mt for global export), meanwhile output in China is set to fall by 6% Y/Y given lower imports from the Philippines (which was partially offset by imports from New Caledonia, Guatemala and Cote d’Ivoire.)

• Ferronickel output is set to reach 0.394Mt in 2022 (+5% Y/Y), driven in part by the return of production at Eramet’s Doniambo and South 32’s Cerro Matoso. Meanwhile, Antam will launch and expand output from its second plant in Halmahera. By 2023, output should rise to 0.411Mt (+4% Y/Y) on the back of Onça Puma’s ramp-up to its designed capacity, Koniambo’s step-up after the second furnace restart, as well as the Burmese Tagaung Taung’s and the Japanese Pamco Hachinohe plant operations returning to their normal production rates.

• Nickel Oxide & Utility Nickel will expand modestly to 0.046Mt in 2022 (+11% Y/Y), driven by reinvestment by Punta Gorda in Cuba, in addition to resumption of production at the Matsuzaka refinery in Japan. Nornickel expects that total production in 2023 will remain relatively flat at 0.048Mt (+3% Y/Y).

Production of Class I Material

• NPI-to-matte conversion output is forecast reach 0.092 Mt in 2022. This will be driven by Tsingshan switching eight RKEF lines to matte production in Morowali (Indoneisa), in addition to CNGR and Huayou launching their own production later in the year.

• HPAL nickel capacity within Indonesia is set to reach 0.07Mt in 2022 (driven by output from the JV between Lygend and Harita, in addition to PT Huayue Nickel and Cobalt operations). By 2023, total output is set to jump to 0.15Mt (upon the ramp up of production from PT QMB New Energy Materials and PT Huafei Cobalt).

• Nickel sulphide production to reach 0.818Mt in 2022 (+5% Y/Y) and hit 0.832Mt (+2% Y/Y) by 2023, as major producers benefit from repairs and maintenances completed over 2021-2022. For more detail here (please see the original report here).

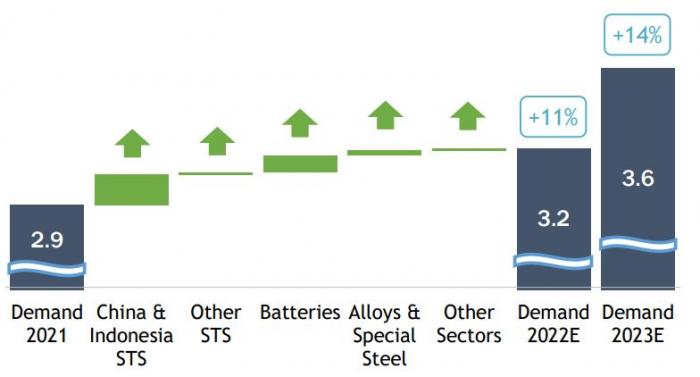

Demand

CHART OF CONSUMPTION GLOBAL IN 2022

TABLE OF GLOBAL CONSUMPTION IN 2022

In more detail:

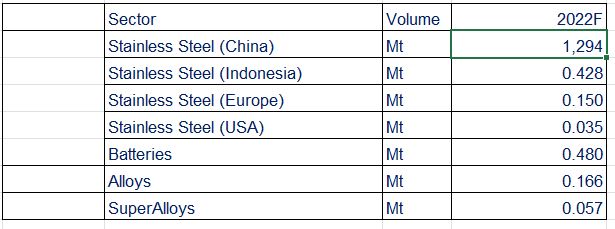

Stainless Steel

• Chinese stainless-steel output to jump by 5% Y/Y, translating into a 10% Y/Y increase in primary nickel demand at 1,294Mt. It is forecast that 2.2 Mt of new capacity is to be launched in 2022 (1.7 Mt by Delong and

0.500Mt by a JV of TISCO and Xinhai). Despite high stainless-steel prices, 300 series production YTD has performed better than 200 series, highlighting little to no substitution.

• Indonesian stainless-steel output is set to expand by 12% Y/Y in 2022 to 5.600 Mt, translating into 0.428Mt of primary nickel demand (+12% Y/Y). Please note, Tsingshan is expected to ramp up 0.600Mt of new capacity in Morowali this year.

• European stainless-steel output is set to moderate this year at 7.000Mt, translating into 0.150Mt of primary nickel demand. The key driver behind this moderation has arisen from escalating energy and raw material costs, exacerbated by the military conflict in Ukraine. Meanwhile, high imports of stainless-steel into the EU from Asian countries is expected to continue over the year.

• U.S. stainless production is set to reach 2.400Mt in 2022, resulting in 0.035Mt of primary nickel demand. While business has remained robust so far this year, with mills being able to pass on higher raw material costs to the buyers, it is expected that activity will slow from Q3 onwards. Please note, in the longer-term, domestic output could be bolstered by the $1Tr Bipartisan Infrastructure Deal approved last year.

Batteries

Alloys & Super Alloys

WHAT ARE THE MAJOR CHANGES TO THE FORECAST SINCE THE NOVEMBER REPORT?

2022 consumption outlook remains almost unchanged

• Stainless steel +9% Y/Y (12% Indonesia, 10% China)

• Batteries +27% Y/Y

• Non stainless +8% Y/Y (strong oil & gas + aerospace)

2022 supply only marginally downgraded from 3.240Mt to 3,210Mt (20% growth down to 19% growth)

• Continued Indonesian NPI growth (+33% Y/Y)

• HPAL + NPI-to-matte (Indonesia, Australia, New Caledonia)

• Solid battery scrap

• FeNi downgraded to 5% growth in 2022 from 11% previously (high energy prices, geopolitical tensions in Eastern Europe)

Market Balance Lowered to 47,000t from 57,000t in November

This material should be construed as market commentary and represents the opinions and viewpoints of the author, and does not reflect tailored advice associated with any specific account.

The views are current only through the date stated and are subject to change at any time based upon market or other conditions, and StoneX Group Inc. (“SGI”) disclaims any responsibility to update such views. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources. Past performance does not guarantee future results.

The StoneX Group Inc. group of companies provides financial services worldwide through its subsidiaries, including physical commodities, securities, exchange-traded and over-the-counter derivatives, risk management, global payments and foreign exchange products in accordance with applicable law in the jurisdictions where services are provided.

References to certain OTC products or swaps are made on behalf of StoneX Markets, LLC (SXM), a member of the National Futures Association (NFA) and provisionally registered with the U.S. Commodity Futures Trading Commission (CFTC) as a swap dealer. SXM’s products are designed only for individuals or firms who qualify under CFTC rules as an ‘Eligible Contract Participant’ and who have been accepted as customers of SXM.

StoneX Financial Inc. (SFI) is a member of FINRA/NFA/SIPC and registered with the MSRB. SFI is registered with the U.S. Securities and Exchange Commission (SEC) as a Broker-Dealer and with the CFTC as a Futures Commission Merchant and Commodity Trading Advisor. StoneX Financial (Canada) Inc. (SFCI) is registered in Canada and is a member of CIRO and CIPF. References to certain securities trading are made on behalf of the BD Division of SFI and are intended only for an audience of institutional clients as defined by FINRA Rule 4512(c). References to certain exchange-traded futures and options are made on behalf of the FCM Division of SFI. Wealth Management is offered through SA Stone Wealth Management Inc., member FINRA/SIPC, and SA Stone Investment Advisors Inc., an SEC-registered investment advisor, both wholly owned subsidiaries of SGI.

R.J. O’Brien & Associates, LLC (RJO) is registered with the CFTC as a Futures Commission Merchant and is a member of NFA.

StoneX Financial Ltd (SFL) is registered in England and Wales, company no. 5616586. SFL is authorized and regulated by the Financial Conduct Authority (FCA) (registration number FRN:446717) to provide services to professional and eligible customers including: arrangement, execution and, where required, clearing derivative transactions in exchange traded futures and options. SFL is also authorized to engage in the arrangement and execution of transactions in certain OTC products, certain securities trading, precious metals trading and payment services to eligible customers. SFL is authorized and regulated by the FCA under the Payment Services Regulations 2017 for the provision of payment services. SFL is a category 1 ring-dealing member of the London Metal Exchange. In addition SFL also engages in other physically delivered commodities business and other general business activities which are unregulated and not required to be authorized by the FCA.

This communication is issued in the European Economic Area by StoneX Financial Europe GmbH (SFEG). StoneX is the trade name used by STONEX GROUP INC. and all its associated entities and subsidiaries. StoneX Financial Europe GmbH (“SFEG”) is a securities trading firm registered in Germany under Company No. HRB 80844.

StoneX APAC Pte. Ltd. (“SAP”) (Co. Reg. No 200616676W) is regulated as a Dealer (PS20190001002) under the Precious Stones and Precious Metals (Prevention of Money Laundering and Terrorism Financing) Act 2019 for purposes of anti-money laundering and countering the financing of terrorism. SAP is an “Approved International Trading Company” authorized to act as a “Spot Commodity Broker” under the Commodity Trading Act.

StoneX Financial Pte Ltd (Co. Reg. No 201130598R) (“SFP”) is regulated by the Monetary Authority of Singapore and is a Capital Markets Service Licence holder (for dealing in capital market products), an Exempt Financial Adviser (for advising on investment products and issuing or promulgating analyses/ reports on investment products) and a Major Payment Institution (for domestic and cross-border money transfer services).

SFP may distribute analysis/report produced by its respective foreign affiliates within the StoneX Group of companies pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations Recipients should contact SFP at (65) 6309 1000 for any matters arising from, or in connection with, this webinar.

StoneX APAC Pte. Ltd. (“SAP”) (Co. Reg. No 200616676W) is regulated as a Dealer (PS20190001002) under the Precious Stones and Precious Metals (Prevention of Money Laundering and Terrorism Financing) Act 2019 for purposes of anti-money laundering and countering the financing of terrorism.

StoneX Financial (HK) Limited (CE No.: BCQ152) (“SHK”) is regulated by the Hong Kong Securities and Futures Commission for Dealing in Securities and Dealing in Futures Contracts.

StoneX Financial Pty Ltd (ACN 141 774 727) holds an Australian Financial Service License (AFSL: 345646) for Dealing in Securities, Exchange-Traded Derivatives Contracts, OTC Derivatives Contracts and Foreign Exchange Contracts, and is regulated by the Australian Securities and Investments Commission.

StoneX Securities Co., Ltd. (“SSJ”) (Co. Reg. No 010401047199) is regulated by the Japanese Financial Services Agency as a Type-I Financial Instruments Business Operator (Kanto Local Finance Bureau (FIBO)No.291’), is a member of the Financial Futures Association of Japan for dealing and broking FX and FX Option transactions, and is a member of the Japan Securities Dealers Association for dealing and broking stock indices and option transactions.

Trading swaps and over-the-counter derivatives, exchange-traded derivatives and options and securities involves substantial risk and is not suitable for all investors. Past performance of any futures or option is not indicative of future success. Indicators are not a trading system and are not published as a specific trade recommendation. The information herein is not a recommendation to trade nor investment research or an offer to buy or sell any derivative or security. It does not take into account your particular investment objectives, financial situation or needs and does not create a binding obligation on any of the StoneX group of companies to enter into any transaction with you. You are advised to perform an independent investigation of any transaction to determine whether any transaction is suitable for you. No part of this material may be copied, photocopied or duplicated in any form by any means or redistributed without the prior written consent of StoneX Group Inc.

The report/analysis herein is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

© 2026 StoneX Group Inc. All Rights Reserved.

Our subscribers have access to comprehensive market analysis from StoneX spanning commodities, equities, currencies and more.

Base Metals LME Report by Natalie Scott-Gray

Last week in New York, StoneX hosted its fourth annual Natural Resources Summit, alongside Copper Club Week. In the article below we discuss the outlook for copper in the year ahead, based on the key questions asked by market players over the course of the week.

Copper's relationship with artificial intelligence has become one of the most influential narratives in commodity markets, helping propel prices to record highs. Yet while investors continue to price in a future shaped by data centres and electrification, the reality of copper demand today remains far more measured.

Our market expertise, advanced platforms, global reach, culture of full transparency and commitment to our clients’ success all set us apart in the financial marketplace.

Reach

With access to 40+ derivatives exchanges, 180+ foreign exchange markets, nearly every global securities marketplace and numerous bilateral liquidity venues, StoneX’s digital network and deep relationships can take clients anywhere they want to go.

Transparency

As a publicly traded company meeting the highest standards of regulatory compliance in the markets we serve, our financials and track record are matters of public record. StoneX’s commitment to “doing the right thing over the easy thing” sets us apart in the industry and helps us build respect, client trust and new partnerships.

Expertise

From our proprietary Market Intelligence platform to “boots-on-the-ground” expertise from award-winning traders and professionals, we connect our clients directly to actionable insights they can use to make more informed decisions and achieve their goals in the global markets.