- Bullish

- An increasing move towards strategic stockpiling (e.g. Project Vault in the US, Section 232 tariffs), is expected to threaten the availability of above-ground stocks.

- The impact of the Iran War has renewed global efforts to reduce fossil fuel reliance, with future investment in the green transition, electrification and digitalisation set to underpin non-cyclical metals demand in the medium-term.

- Supply-side concerns remain prevalent, with an uncertain period ahead as US-Iran negotiations take place, set against the backdrop of future Section 301 and Section 232 tariffs.

- Bearish

- Western manufacturing faces headwinds from an altered path for US monetary policy, with our house view for no rate cuts this year, delaying a recovery in the global industrial cycle.

- China’s May hard data reading point to an uneven growth trajectory with a heavy reliance on exports as the engine of growth.

- Despite optimism for the Strait of Hormuz to return to normal traffic levels by July, elevated energy costs, insurance and freight costs will continue to create bottlenecks, negatively impacting demand for metal intensive end-uses such as automotives.

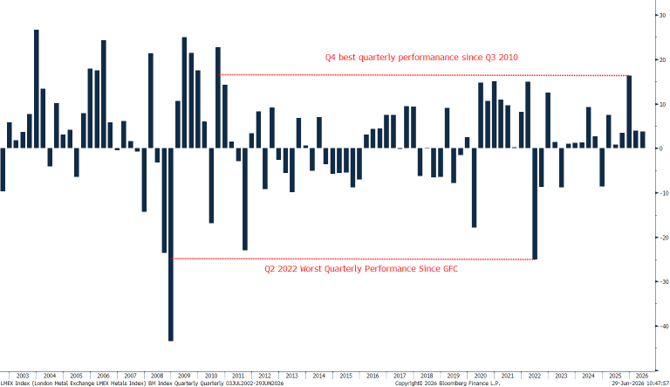

The base metal index is on track to post a gain of 4% in Q2, after hitting its highest level on record at the start of June, despite the Iran War threatening to stretch into its fourth month. Indeed, while the LMEX Index initially faced headwinds in the first three weeks of the conflict, falling to its lowest level of the year (and lowest level since December 2025), this was short lived, with new nominal highs being posted from April onwards. On a YTD basis, each metal in the suite is in the green (with the exception of lead), and over the course of the last three months, tin and copper have posted new nominal highs, while aluminium, zinc and nickel have posted multi-year highs.

LMEX Index Quarterly Price Performance

Source: Bloomberg, StoneX

LMEX Index Price Performance

Source: Bloomberg, StoneX

LMEX Index Price Performance 10Y

Source: Type or use Ctrl+Shift+V here to paste

So why have these industrial metals held on to such a strong performance in an environment in which global GDP growth has been downgraded?

We suspect the answer is three-fold.

- Firstly, the impact of the breakout of the Iran War created unforeseen and immediate supply risks for a handful of the suite (specially aluminium, nickel and copper), with these supply risks running ahead of demand destruction concerns.

- Secondly, the backdrop of heighted geopolitical tensions and rising inflation supported the desire to hold hard assets.

- Thirdly, the impact of the war has accelerated the need to move away from fossil fuel reliance, with critical mineral supply chain security at the forefront, underpinning strategic stockpiling and medium-term demand projections for metals like copper.

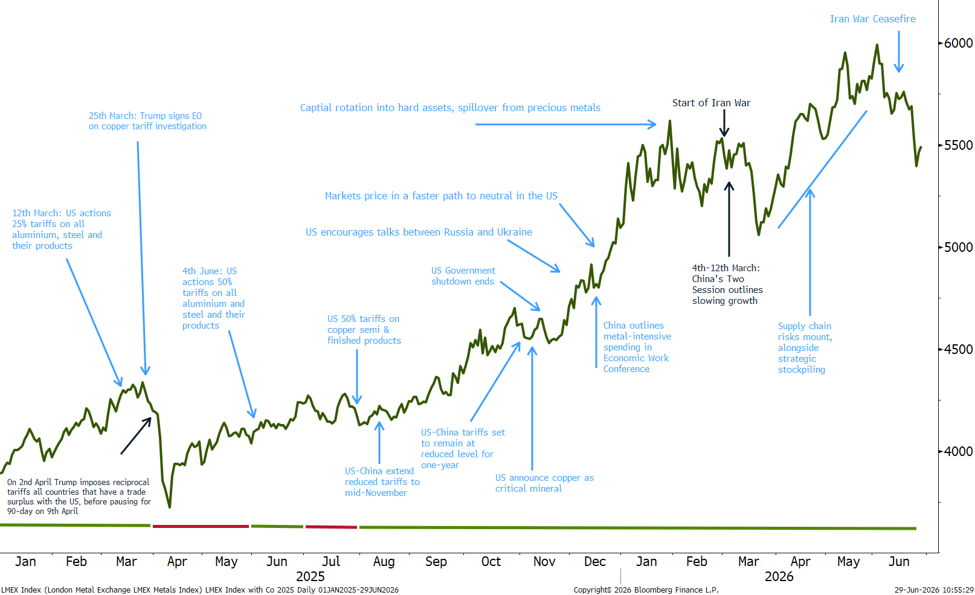

LME 3M Base Metal Price Performance 2026

Source: Bloomberg, StoneX

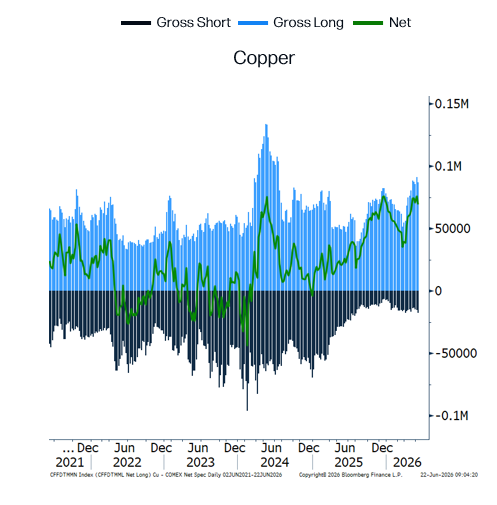

Positioning & Investment Flows

A key structural theme highlighted is the shift in speculative positioning across some LME & CME metals:

- Short positions have largely washed out versus last year.

- The rally is increasingly driven by investment allocation into hard assets, rather than traditional supply-demand tightening alone.

Two dominant macro drivers underpin this:

1.Geopolitical risk, which is encouraging defensive allocation into hard assets.

2.AI and electrification narratives, particularly for copper, attracting forward-looking investment flows.

However, we stress a critical nuance:

- The AI story is not yet a material demand driver (currently <2% of copper demand).

- Market pricing is therefore being supported by future expectations rather than current physical consumption, raising the risk that positioning is ahead of fundamentals in the short term.

COMEX Managed Money Positions

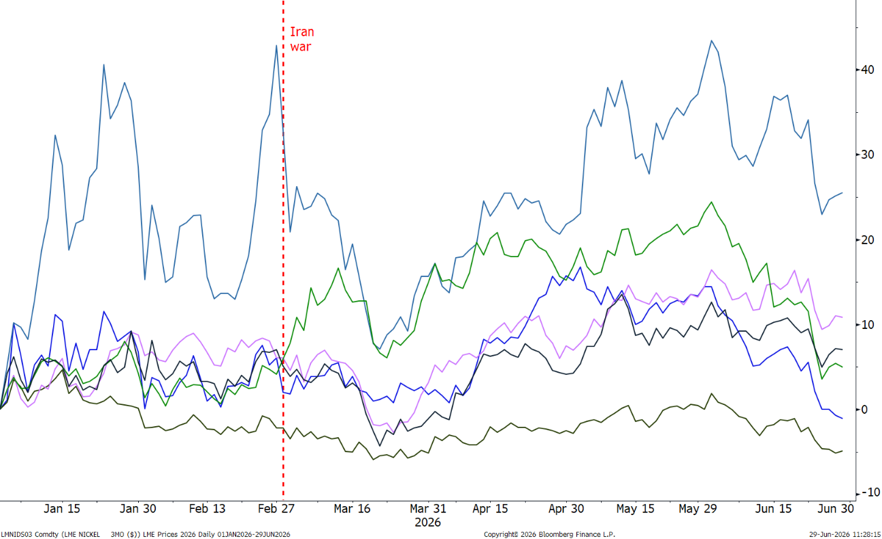

Taking a step back, despite the US and Iran having officially entered a 60-day period of negotiations to end the war, following the signing of a 14-point Memorandum of Understanding of 19th June (with an outline to return the Strait of Hormuz to pre-war volumes within 30 days), this remains a deal in theory only, and at the time of writing (29th June), traffic in the Strait is heavily restricted.

Looking at our base case, we maintain the view that the outlook for the macroeconomic landscape is more clouded than end-2025, in which downgraded global GDP and industrial production will have a lagged impact on global manufacturing. In addition to this, we see an altered path for US monetary policy, with our house view for zero rate cuts in 2026, from two 25bps cuts expected previously. Note, this delays the outlook for a recovery in the global industrial cycle, with falling yields having a net positive impact on base metals. Furthermore, the reduced expectation for rate cuts in 2026 has resulted in the US dollar rising to its strongest level in a year. Looking to China, May’s hard economic data readings have signalled the country’s ongoing struggle to boost domestic demand, and heavy reliance on exports, with weaker YTD Y/Y readings for GDP, industrial production and retail sales, while deepening declines were posted for property investment, property sales and fixed-asset investment. We have limited expectations for robust stimulus this year, which alongside deflationary pressures, record low consumer confidence, weak investment demand and increasing concerns for external demand (with exports accounting for one-third of GDP growth last year), could result in headwinds for China to meet its modest economic targets. Finally, the combination of an uncertain trade landscape holds potentially longer-term headwinds for global manufacturing and base metal demand overall, with the introduction of Section 301 tariffs (to replace temporary Section 122 tariffs on more than 60 countries, including China), in addition to ongoing and future Section 232 tariffs, set against ongoing conflicts (e.g. Russia-Ukraine, Iran-US).

A Brief Outlook on Key Trade Flows Dates

A Brief Outlook on Key Trade Flows Dates

30th June: The deadline for US Commerce Secretary Howard Lutnick to provide the US President with an update on the refined copper market and domestic refining capacity. Please see our article Copper Market Pivotal Moment: US Decision on Refined Tariffs 30th June.

1st July: North American Free Trade Agreement (US-Canada-Mexico) will expire.

7th July: Hearings will begin over public comments following the proposed implementation of Section 301 tariffs. The USTR has proposed 10% tariffs on imports from ~60 countries, including Canada, Mexico, the EU, Taiwan, and the UK. In addition to 12.5% tariffs are proposed for China, India, Japan, South Korea, Brazil, and Switzerland.

24th July: Section 122 tariffs will expire.

Source: Bloomberg, StoneX

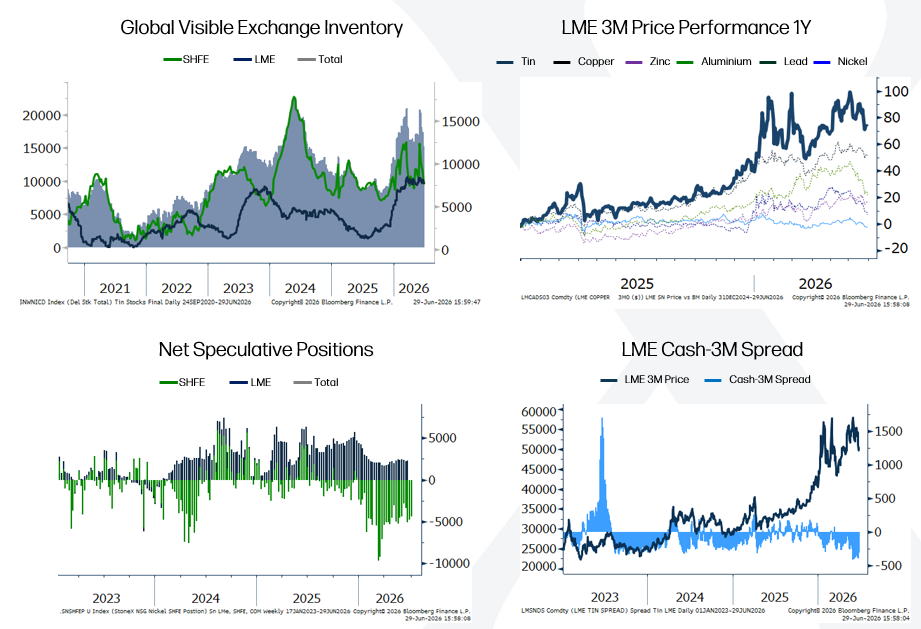

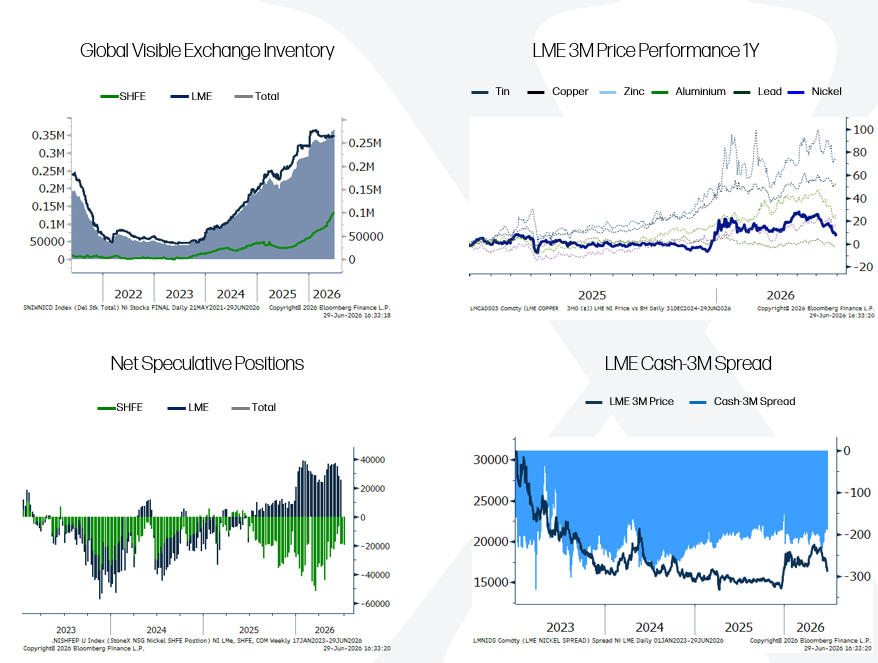

Tin is on track to be the best performing base metal in Q2 (+9.0%) and YTD (+25.7%), reaching a record high of $57,960/t on 2nd June. While supply risks have supported prices over the last three years, we believe recent gains have outpaced fundamentals and have increasingly been driven by tin's connection to AI investment, given its extensive use in semiconductors and data centres. Semiconductor demand is forecast to rise sharply to $1.51Tr in 2026, according to World Semiconductor Trade Statistics. However, despite AI-related growth, we estimate total tin consumption slowed both Q/Q and Y/Y in Q2. On the supply side, Indonesian exports remain constrained, down 19.3% YTD Y/Y following mine closures and tightening RKAB quotas. However, tin ore exports to China have improved overall (+71% YTD Y/Y), with record production in Q1 from Alphamin Resource’s Bisie mine in the DRC and increasing exports from Myanmar (the third largest producing country in the world and largest importer to China), with ore imports up three-fold YTD Y/Y (although remaining below 2024 levels). Given the tin market has posted its first quarterly surplus in Q1 since late 2024, accompanied by global stocks having jumped 31% YTD, we suspect LME speculative positioning is overstretched to the upside.

Source: Bloomberg, StoneX

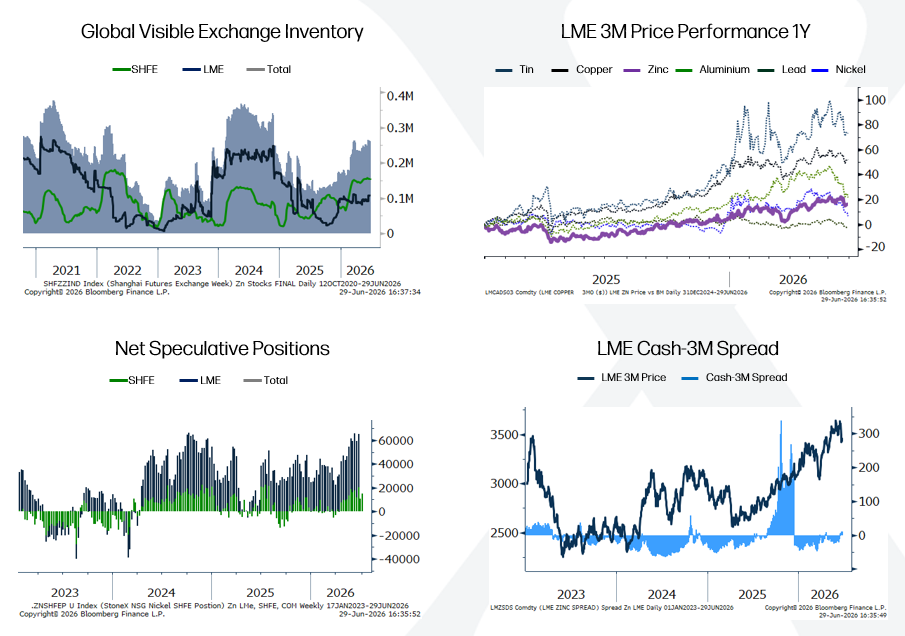

Zinc is on track to be the second best performing base metal of Q2 with gains (at the time of writing of 8.3%), placing zinc as the second best performing base metal YTD (12.1%). Price support has been driven by tightening supply conditions, with mine production from major mines (such as Antamina in Peru and Red Dog in Alaska) declining on falling ore grades, late-life production and mine plan adjustments. Meanwhile, despite record output at the world’s highest-grade zinc mine Kipushi in the DRC, natural disasters, extreme weather and geopolitical disruption in the Middle East, India and Australia have limited output. As a result, tightening ore availability has resulted in RCTCs falling into negative territory, to their lowest level on record, with imports of ore into China declining 19.3% Y/Y in May. However, despite this, Chinese refined production has accelerated, supported by by-product credits and high metal prices. Looking to the months ahead, as Chinese smelters enter their maintenance period in Q3, attention will be paid to the health of global stocks, particularly on the LME, with the forward curve currently in backwardation. Having said this, LME speculative gross longs for zinc are at their highest level on record, with extreme levels often accompanied by a sharp correction. Furthermore, we are currently entering the off-season for zinc demand, with frail demand dynamics stemming from zinc’s largest end-use in galvanizing steel, resulting in weak supply and demand dynamics at play.

Source: Bloomberg, StoneX

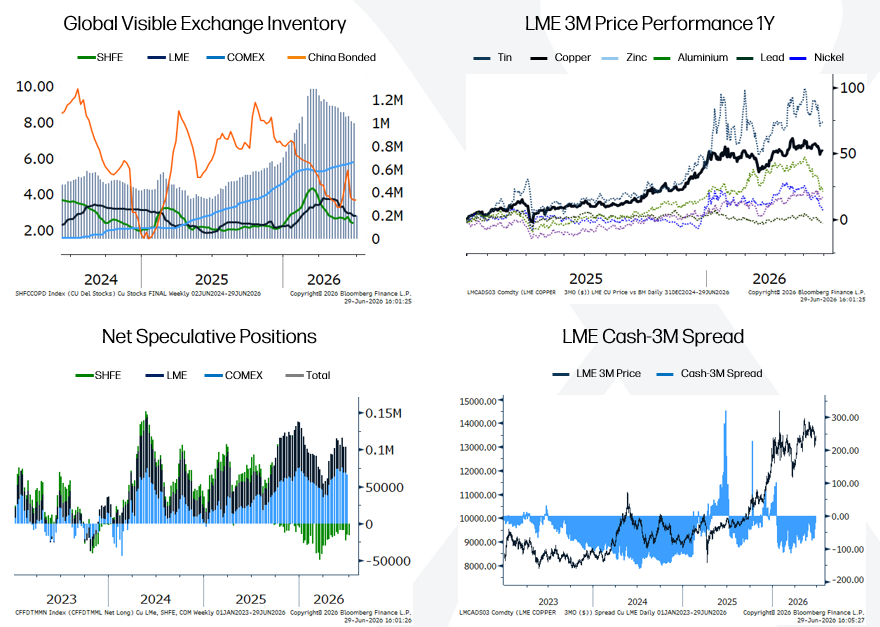

Copper is set to close Q2 as the third best performer, up 8.3%, reversing losses in Q1, with the LME 3M price breaching $14,000/t to a new record high by 13th May ($14,153/t). In a similar vein to tin, copper’s price performance has been highly influenced by future CAPEX investment on AI infrastructure, with the correlation between LME 3M copper and US technology stocks hitting its highest level since 2012 (despite end-use in this sector at less than 2% of total demand). In addition, bullish sentiment has stemmed from the growing desire to stockpile copper, with it being deemed a US critical mineral in November, while forecast flat mine production alongside regionally imbalanced above-ground stocks (64% on and off-warrant held in the US) has further encouraged the bullish narrative. In reality, while the copper concentrate balance remains in a historically wide deficit (in part based on smelting overcapacity), the refined market is relatively balanced, with record levels of monthly Chinese output benefiting from by-product credits, economies of scale and state-backed support. In addition, visible exchange stocks rose to their highest level on record by Q1, further demonstrating a well-supplied global market. With this said, in the months ahead, the single largest swing factor for the market will come from a decision on whether the US Administration will impose Section 232 tariffs on refined copper imports, with the US Commerce Secretary facing a deadline to report his recommendation to President Trump on 30th June. It is important to note that President Trump has no legal timeline to act on these findings. The White House outlined a potential scenario in which refined copper tariffs could be imposed at 15% by 2027, before being increased to 30% by 2028. As things stand, the COMEX-LME Dec/Dec arbitrage is pricing in tariffs at 3%, while over 1.2Mt is set to have entered the US since the investigation first opened in February 2025.

Source: Bloomberg, StoneX

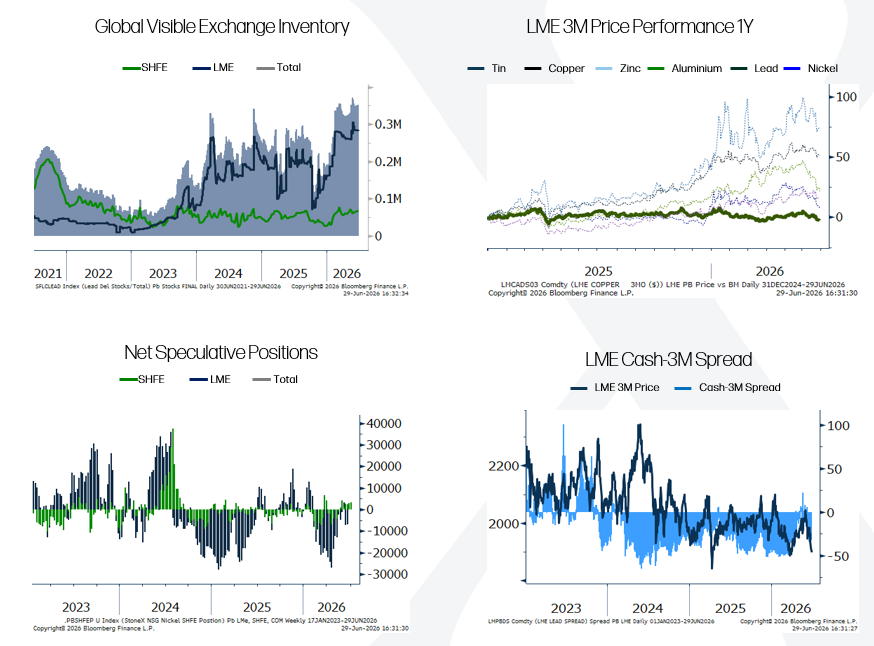

Lead continues to sit in the middle of the group in Q2, coming in flat, however, it holds the position as the worst performing base metal YTD. Lead’s price performance reflects a moderate backdrop for traditional industrial metal demand, set against a somewhat protected supply outlook, given lead’s unique fundamentals in which two-thirds of supply comes from secondary sources. As things stand, global lead stocks are hovering around their highest level since 2012, and it is the only base metal in a net short speculative positions across the LME and SHFE.

Source: Bloomberg, StoneX

Nickel is set to post losses over the course of Q2, while being the second weakest performer on a YTD basis (+0.3%). However, this does little to inform us of the decisive price action that nickel has experienced over the course of 18 months, in which nickel has held in a new trading range in 2026 $19,642-16,750/t, a stark difference from the 2025 range of $16,828-14,084/t. Behind this has been elevated supply concerns, at first purposely driven by the world’s largest producer Indonesia, moving to restrict RKAB license quotas, clamp down on illegal mining activities and introduce new mineral pricing formulas (sharply increasing ore costs for High Pressure Acid Leaching (HPAL) producers. However, the unforeseen impact of the Iran War further tightened supply conditions, with soaring sulfur prices and Indonesia’s heavy reliance on Middle Eastern sulfur for HPAL operations (~76%), resulting in capacity cutbacks. However, while Indonesia may move to expand RKAB production quotas by mid-year, the nickel risks posting a modest deficit in 2026 (the first since 2021). Having said this, years of oversupply and the fast tracking of Chinese and Indonesia brands onto the LME have resulted in global stocks hovering at their highest level on record.

Source: Bloomberg, StoneX

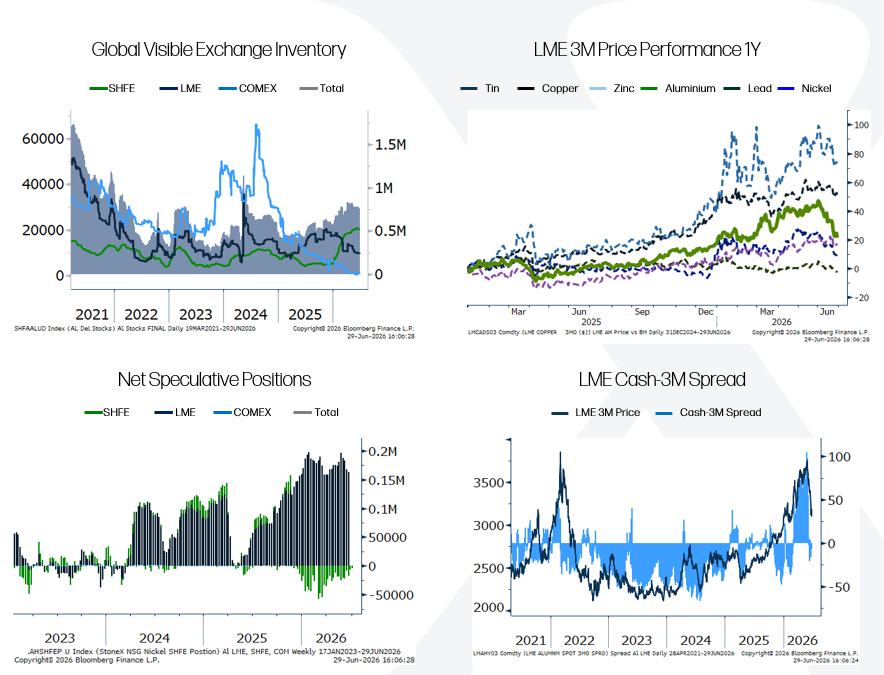

Aluminium is on course to close Q2 as the worst performing base metal with prices down 8.6% at the time of writing. This weak performance has been solely concentrated in the final month of the quarter, with markets moving to price in an end to the Iran War, set against record levels of Chinese refined output and a strengthening US dollar. The impact of an end to the Iran War has the most immediate knock-on impact to aluminium supply fundamentals of any base metal, given that the Middle East region accounts for 9% of global output with more than 80% of raw material imports and refined aluminium exports concentrated through the Strait of Hormuz. As things stand, we estimate as much as 3Mt of smelter capacity was taken offline since the war began via a combination of direct smelter damage to Emirates Global Aluminium Al Taweelah smelter complex in Abu Dhabi and reduced run rates in key producing countries including Bahrain, Qatar and Iran. Given this, and accounting for modest demand destruction in the months ahead, largely stemming from the automotive industry, which has suffered from a lack of Value-Added-Products (VAP) exports from the Middle East (a major global supplier), we expect the aluminum market will remain in a deficit ~1Mt this year. We expect aluminium prices to be well supported by dwindling global stocks, which are expected to fall to their lowest level since the GFC by end-Q2, however, the bringing online of Indonesia capacity over the course of H2 and speed of resumption of production and exports in the Middle Eastern will be a key factor. In addition, attention will be paid to developments over idled smelter capacity restarts, most notably the Mozel smelter in Mozambique and limitations on smelter utilization creep in China (set against the 45Mt capacity ceiling). Meanwhile, the realities in the physical market will be best monitored by regional premium.

Source: Bloomberg, StoneX