Dollar to Reflect Inflation Data in Brazil and the US, Copom Minutes, Geopolitical Uncertainties in the Middle East, and the Brazilian Electoral Scenario

- Bullish

- The release of Copom minutes may reinforce expectations of further cuts to the Selic rate despite a challenging inflationary scenario, reducing the attractiveness of domestic bonds and weakening the BRL.

- A stronger reading for June's PCE index is expected to strengthen expectations of higher US interest rates for a longer period, favoring returns on US bonds and strengthening the dollar globally.

- Concerns about sustaining the provisional agreement between the US and Iran are likely to heighten investors' geopolitical risk perception, undermining the performance of risky assets such as the BRL.

- Bearish

- News about alleged involvement of government-affiliated Congress members with Banco Master could harm voting intentions for Luiz Inácio Lula da Silva and reduce political risk perception for domestic assets, strengthening the BRL.

The Week in Review

- The United States and Iran signed an agreement to allow a 60-day ceasefire and reopen navigation in the Strait of Hormuz, although new conflicts between Israel and Lebanon brought uncertainty over its sustainment.

- The Federal Reserve surprised by adopting a firm stance against inflation and pointing to the possibility of rate hikes still in 2026.

- The Central Bank of Brazil surprised by suggesting further cuts to its baseline interest rate (Selic) despite worsening inflation estimates.

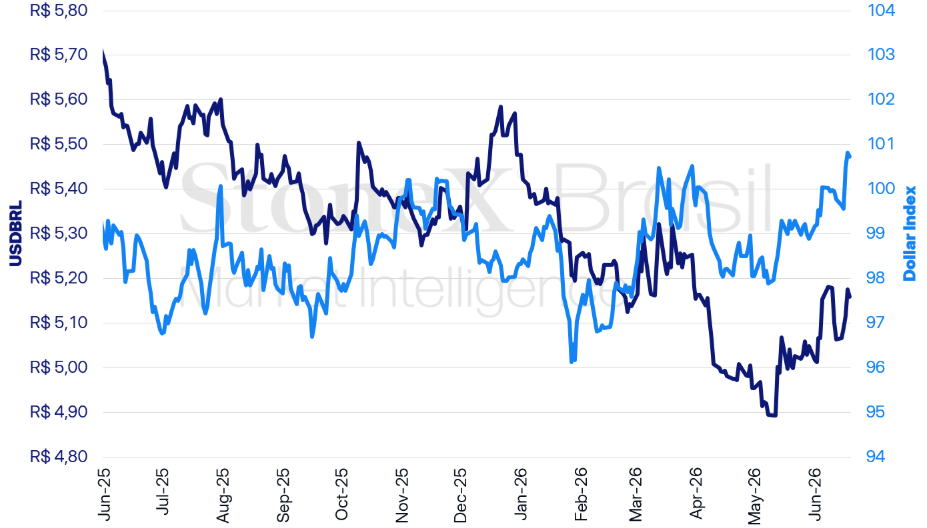

USDBRL and Dollar Index (points)

Source: StoneX cmdtyView. Design: StoneX.

USDBRL Variations | Daily: -0.30% | Weekly: +1.89% | Monthly: +2.20% | Annual: -5.80% | Over 12 months: -6.22%

Dollar Index Variations | Daily: -0.09% | Weekly: +0.96% | Monthly: +1.86% | Annual: +2.45% | Over 12 months: +1.85%

KEY EVENT: Copom Minutes and RPM

Expected Impact on the BRL Exchange Rate: Bullish

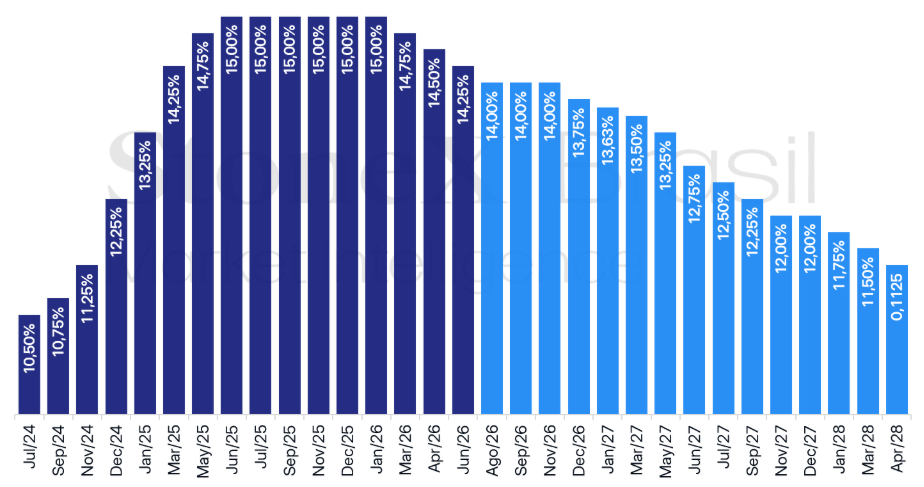

Brazil: Historical and Expectations for Interest Rates – Focus Bulletin from June 12, 2026

Source: Central Bank of Brazil. Design: StoneX.

The currency market is expected to react to the release of the minutes from the last decision by the Central Bank's Monetary Policy Committee (Copom), which was poorly received by investors as it suggested the continuation of the Selic rate cuts cycle despite rising inflation expectations.

Why This Matters: The indication to continue the cycle of cuts comes in a context of inflation persistently above the target and a more aggressive stance by the Federal Reserve.

- This, in turn, simultaneously reduces expectations for the Selic rate while expectations for US interest rates increase, harming Brazil's interest rate differential and decreasing the attractiveness of domestic bonds, devaluing the BRL.

Contradictions: The decision minutes may provide more details about apparent contradictions in the Statement that caused noise among investors.

- On the one hand, Copom reduced the baseline interest rate (Selic) by 0.25 percentage points for the third consecutive time, to 14.25% per year, as was largely anticipated by financial market agents.

- Additionally, the Statement suggested the continuation of the cycle of Selic cuts, by stating that “the total magnitude of the calibration [cuts] cycle will be determined in light of new information.”

- On the other hand, the Committee indicated that inflation estimates continued to rise in the “relevant horizon” of monetary policy and made the inflation risk balance more bullish by adding that “demand stimuli” could generate greater pressure on prices.

Extended Horizon: The statement was also poorly received for mentioning the first quarter of 2028 as an “alternative” for the relevant horizon of monetary policy, one quarter longer than the horizon usually used by Copom.

- This was interpreted as an “improvisation” to justify further cuts to the Selic rate.

- Central Bank simulations point to inflation within the target only for the first quarter of 2028.

- For the fourth quarter of 2027, the horizon that would be relevant by previous standards, the expectation for the IPCA rose from 3.5% to 3.7%.

- The Central Bank's intention seems to have been to signal that a more restrictive interest rate level was not needed at this moment, as a significant part of inflationary pressure would result from supply shocks and anticipated inflation convergence slightly beyond the usual timeframe.

- However, the fact is that this “alternative” raised questions about the Central Bank's credibility in seeking price stabilization and worsened the risk perception of domestic assets.

Monetary Policy Report (RPM): In this context of noise and questions about the Central Bank's credibility, investors should also monitor the release of the June RPM, the most comprehensive analysis by the Central Bank on the domestic and international macroeconomic environment, including projections for Brazil's main macroeconomic indicators for the coming years.

- In particular, investors will focus on inflation projections amid the discussion about extending the relevant horizon for monetary policy.

IPCA-15: Amid attention to Brazilian monetary policy, the June National Consumer Price Index 15 (IPCA-15) should reinforce the perception of worsening inflation dynamics in the country.

- Median estimates point to a 0.7% rise in the indicator in June, after a 0.62% increase in May, mainly driven by rising food prices.

- The core IPCA-15, which excludes volatile components like food and energy, should remain in the range between 0.4% and 0.5%, suggesting more widespread and persistent inflationary pressure, particularly in the services sector.

US Economic Data

Expected Impact on the BRL Exchange Rate: Bullish

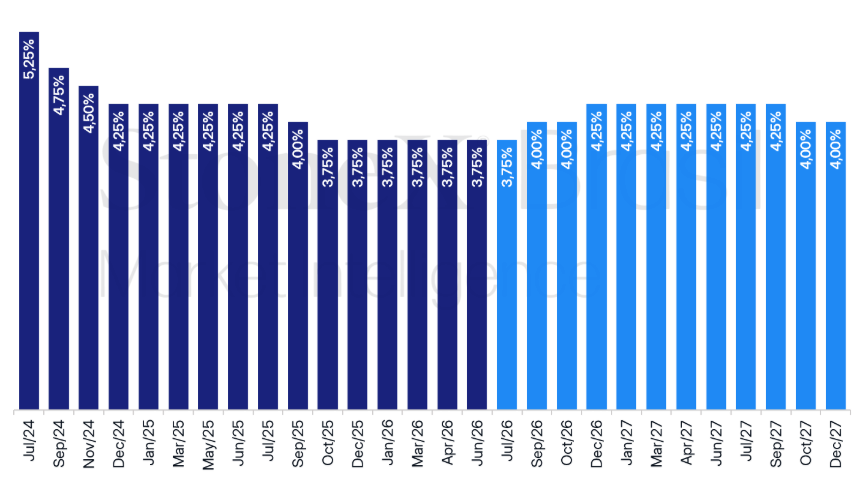

US: Historical and Expectations for Interest Rates – Updated June 19, 2026

Source: CME FedWatch Tool. Prepared by: StoneX. Refers to the market's most probable interest rate futures bets on the indicated date.

Investors should also react to the release of US economic data, particularly the May Personal Consumption Expenditure Price Index (PCE), a metric used by the Federal Reserve to monitor inflation in the country.

- Median estimates point to a 0.4% monthly rise in the indicator, but core acceleration, excluding volatile components like food and energy, from 0.2% in May to 0.3% in June.

- This acceleration is expected to result from higher prices for airline fares, health costs, and financial administration fees.

- Personal income is expected to have expanded by 0.4% in the month, driven by strong labor market performance, supporting a 0.6% growth in personal consumption.

Why This Matters: A stronger inflation reading in the country should consolidate expectations for higher interest rates for a longer period in the country.

- This, in turn, tends to raise yields on US Treasury bonds (Treasuries) and attract foreign capital, strengthening the USD globally.

Fed's Firm Tone: Last week, the Federal Open Market Committee (FOMC) kept its benchmark interest rate unchanged in the range between 3.50% and 3.75% per year and surprised financial market participants with the number of Committee members who anticipated further rate hikes still in 2026 and Kevin Warsh's firm stance on price stability.

- This resulted in increased bets on US interest rate hikes, suggesting the Fed should prioritize combating inflation in the short term, which boosted the dollar index (DXY), an index measuring the dollar's global strength, to its highest level in over a year.

Warsh's First Meeting as Fed Chair: Another highlight was the statements by the new Federal Reserve chairman, Kevin Warsh, indicating possible changes in the monetary authority's structure.

- Warsh announced the creation of five task forces for “essential” topics for conducting monetary policy, namely, communication, balance sheet, data source dependency, productivity and jobs, and inflation analysis structures.

- Warsh believes these task forces are likely to make their final suggestions before the end of the year.

- Additionally, the decision statement was shortened and removed any mention of future expectations by the Committee. According to the chairman, “it is inappropriate” for a central bank to offer “forward guidance,” i.e., guidance on how it anticipates the economic outlook evolving.

- Finally, the expectation was that Trump's nominee would be more aligned with the president's ideas favoring rate cuts. It's still early to draw conclusions, but his initial remarks suggested a firmer tone against inflation (“hawkish”) rather than flexible (“dovish”).

Middle East Disagreements

Expected Impact on the BRL Exchange Rate: Bullish

Lack of consensus among the US, Iran, and Israel continues to generate uncertainty in financial markets, raising doubts about the feasibility of the memorandum of understanding signed between the US and Iran earlier this week.

- Israel refuses to vacate southern Lebanon and continues to clash with Hezbollah militants, violating one of the agreement's conditions.

- As a result of conflicts between the countries, the negotiation meeting scheduled for last Friday (19) was canceled.

Why This Matters: Concerns about sustaining the provisional agreement among the US, Israel, and Iran are likely to heighten investors' geopolitical risk perception, undermining the performance of risky assets such as the BRL.

In Detail: The memorandum of understanding signed last week provided for the suspension of military confrontations on all fronts, including Lebanon, for 60 days, while the countries continued negotiating more complex issues like Iran's nuclear program and a permanent peace agreement.

- However, Israel stated it was not part of this agreement and maintained its occupation in southern Lebanon, continuing its clashes with Hezbollah militants.

- Additionally, Iran announced it would “control” the Strait of Hormuz in partnership with Oman after the 60-day ceasefire ends, challenging one of the US's firmest demands.

Strait of Hormuz: Due to renewed tensions in the Middle East, reports indicated reduced traffic through the Strait of Hormuz just one day after reports of gradual resumption of flows in the region.

- Investors fear the countries will not reach an agreement within the 60-day period established by the memorandum of understanding.

- As such, signs that the countries are not close to a lasting resolution could raise oil prices, sustaining global inflationary pressures.

Brazilian Political and Electoral Scenario

Expected Impact on the BRL Exchange Rate: Bearish

The government leader in the Senate, Jaques Wagner, was targeted by Federal Police (PF) operations in the new stage of Operation Compliance Zero, which investigates an alleged illicit scheme of fraud involving Banco Master.

Why This Matters: Investors are increasingly sensitive to the approaching October presidential elections, reacting intensely to Brazilian political news.

- In practice, recent reactions from financial market agents reveal a preference for electing a new president who could be more fiscally conservative.

- Therefore, accusations of alleged irregularities against government-affiliated Congress members could harm voting intentions for Luiz Inácio Lula da Silva and reduce political risk perception for domestic assets, strengthening the real.

In Detail: The senator was identified in investigations as a beneficiary of alleged economic advantages in exchange for supporting measures in Congress that would favor Banco Master.

- The Federal Police states that a company “associated with Jaques Wagner's family nucleus” allegedly received BRL 3.5 million from a “legal entity linked to Augusto Ferreira Lima's nucleus,” a former Banco Master partner.

- Additionally, alleged receipt of a property as bribe payment involving the two mentioned names is also under investigation.

- The senator denied the accusations and stated he never received funds from Banco Master.

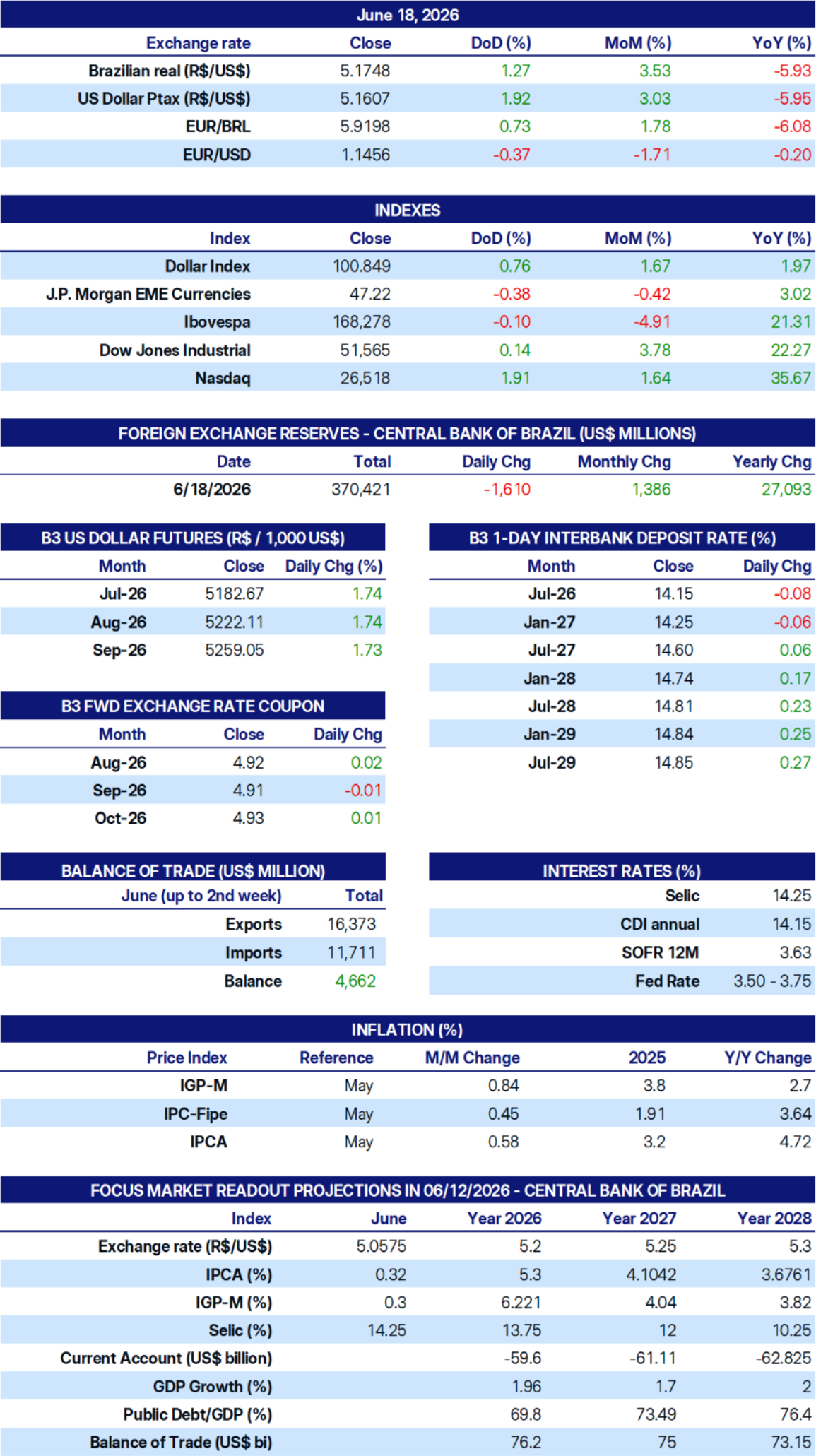

INDICATORS

Sources: Central Bank of Brazil; B3; IBGE; Fipe; FGV; MDIC; IPEA and StoneX cmdtyView.