Dollar to reflect FOMC minutes, IPCA, and domestic political scenario

- Bullish

- Minutes from the FOMC interest rate decision may reinforce the perception of a Federal Reserve that is more concerned with inflation, increasing bets on further rate hikes in the US this year, raising yields on Treasuries, and strengthening the USD globally.

- Flávio Bolsonaro's participation in a hearing in the US regarding tariffs against Brazil may increase political risk perceptions for national assets and negatively impact the BRL's performance.

- Bearish

- In Brazil, June's IPCA is expected to indicate signs of persistent inflationary pressures and increase bets on halting the Selic rate cut cycle, favoring foreign capital inflow and strengthening the BRL.

The week in review

- The Employment Situation Report (“payroll”) pointed to a cooling of the US labor market, with figures below expectations and downward revisions for the previous two months in net job creation.

- At the annual Central Bank Forum organized by the European Central Bank (ECB), Federal Reserve Chair Kevin Warsh stated that he believes inflation risks in the US have decreased, a comment interpreted as a less aggressive stance on combating inflation, contributing to the USD weakening last week.

- Despite the global USD weakening, the BRL did not follow this trend due to worsening risk perceptions for local assets as elections approach.

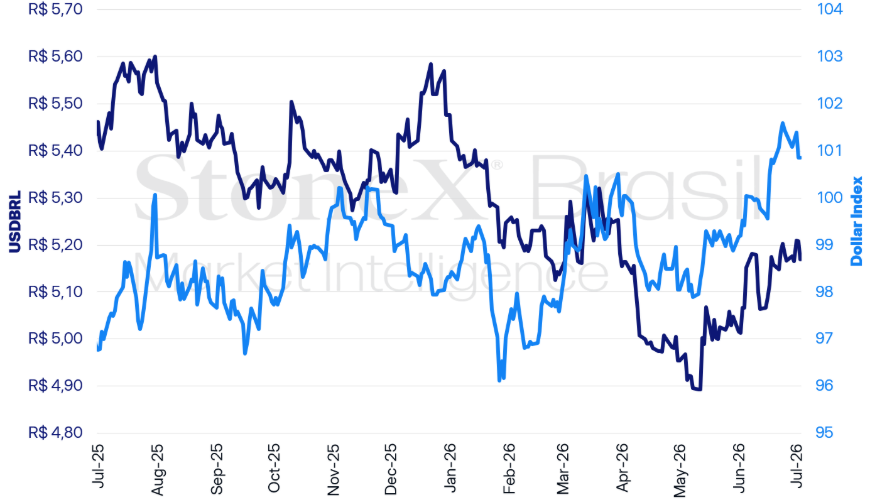

USDBRL and Dollar Index (points)

Source: StoneX cmdtyView. Design: StoneX.

USDBRL variations | Daily: -0.73% | Weekly: +0.04% | Monthly: +0.07% | Annual: -5.62% | Last 12 months: -4.35%

Dollar index variations | Daily: +0.00% | Weekly: -0.48% | Monthly: -0.34% | Annual: +2.58% | Last 12 months: +3.81%

KEY EVENT: FOMC minutes

Expected impact on the BRL exchange rate: bullish

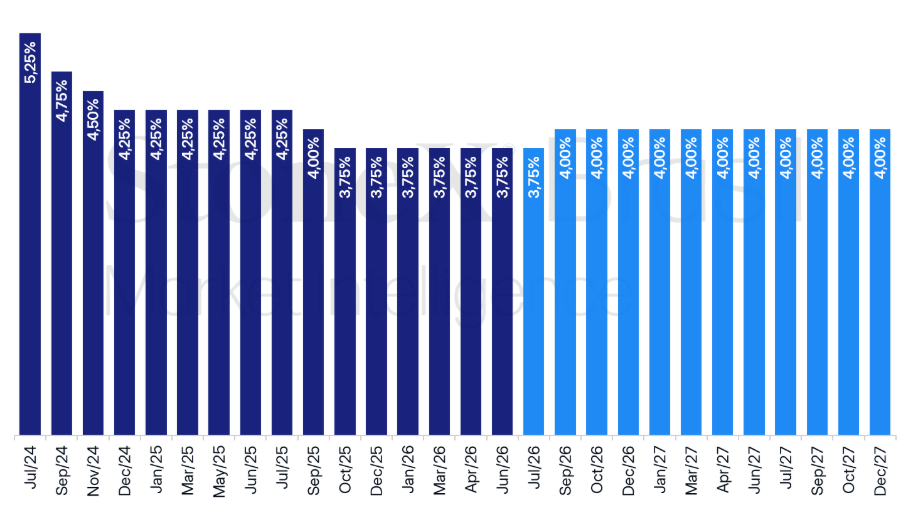

US historical and expected interest rates – updated on July 3, 2026

Source: CME FedWatch Tool. Design: StoneX. Refers to the highest probability bet in the interest rate futures market on the indicated date.

The currency market is expected to react to the release of the minutes from the last interest rate decision by the Federal Open Market Committee (FOMC) of the Federal Reserve (Fed), which surprised investors due to the number of Committee members anticipating further rate hikes in 2026 and Kevin Warsh's firm stance in defending price stability.

Why this matters: The document may reinforce the perception of the Fed's concerns about inflation above the target, suggesting a readiness to maintain higher interest rates to restore price stability.

- This, in turn, would raise yields on US Treasuries and favor foreign capital inflows into the country, strengthening the dollar globally.

Holding back: Although the publication of minutes occurs only three weeks after the FOMC decision, this week's document gains importance as it may offer clues about the trajectory of U.S. interest rates that the new Fed Chair, Warsh, refuses to provide.

- However, given the reformulation of the Federal Reserve's communication strategy, which has substantially shortened the decision statement, there is a risk that the minutes will also be truncated or less detailed than the standard under Jerome Powell.

Warsh's puzzle: Last week, during participation in a major European Central Bank event, Warsh continued to refuse to provide any kind of future expectations (“forward guidance”) or comment on the economic situation.

- The new Fed Chair's laconic style resembles that adopted during Alan Greenspan's tenure, considered unpredictable by investors.

- For example, although the new Fed Chair repeated the importance of price stabilization in the United States, it is unclear what he means by price stabilization or the timeline he envisions for achieving it.

- Warsh also stated that he believes inflation risks in the United States have decreased and reiterated that recent technological innovations will increase productivity and bring disinflationary effects to the country, comments interpreted as a less aggressive stance on combating inflation.

Payroll surprises in June: Last week, the Employment Situation Report surprised investors by showing much weaker-than-expected figures for the labor market.

- The US economy created a net balance of only 57,000 jobs in June, well below the median estimate of 110,000 jobs.

- Additionally, the numbers for April and May were revised downward by 74,000 jobs.

- The unemployment rate fell from 4.3% to 4.2% after 720,000 people exited the workforce.

- As a result, the participation rate dropped to 61.5%, the lowest level since March 2021.

Rate hike in doubt: These data raised doubts about the actual degree of heating in the US labor market, although more data are needed to establish whether there is indeed a trend change.

- Additionally, investor bets on new interest rate hikes by the Federal Reserve this year declined only slightly after the payroll release.

- One explanation for the modest shift in bets could be the concentration of negative performance in the leisure and hospitality sector, which recorded a net loss of 61,000 jobs.

- Restaurants and bars eliminated 32,900 jobs, while hospitality cut another 21,700 positions, contrary to expectations that the World Cup would boost hiring in the sector.

- Excluding this sector, the U.S. payroll would be 118,000 new jobs, close to the initial estimate.

June IPCA

Expected impact on the BRL exchange rate: bearish

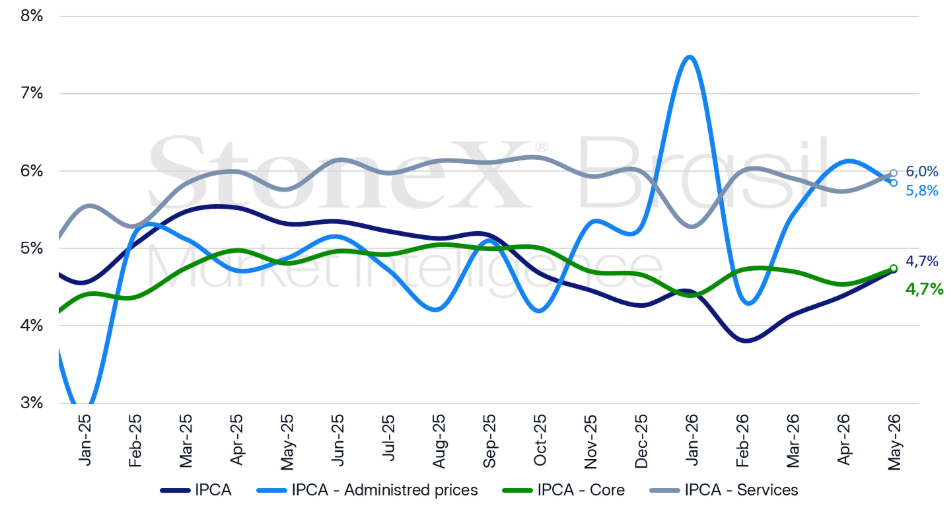

IPCA accumulated over 12 months - selected groups (%)

Source: Central Bank of Brazil. Design: StoneX.

In the domestic agenda, the release of June's Broad Consumer Price Index (IPCA) should help investors calibrate expectations for inflationary and monetary policy trajectories.

Why this matters: Signs of persistent inflationary pressures should increase bets on halting the interest rate cut cycle by the Monetary Policy Committee (Copom).

- This, in turn, should raise yields on domestic government securities and favor foreign capital inflows, boosting the real's performance.

Inflation concerns: Inflation concerns raise doubts about the continuity of the Selic rate cut cycle, especially after the IPCA exceeded tolerance bands in the last reading.

- In the minutes of the last Copom decision, a worsening of Brazil's inflation outlook was signaled compared to the previous meeting, and the Committee's inflation estimates were raised.

- On the other hand, the document noted that an important part of this worsening was due to “supply shocks,” such as rising oil and derivative prices caused by the Middle East conflict, and that there were high uncertainties about the extent and magnitude of these shocks.

- The lack of clear signaling by the monetary authority generates doubts among investors. On one hand, the worsening of the inflation outlook weighs in favor of halting the interest rate cut cycle, while the relief from “supply shocks” would allow these cuts to continue.

- In this context, the latest reading of the IPCA core, excluding volatile components like energy and food, indicated acceleration both monthly and over the last 12 months, suggesting that significant inflationary pressures may still exist.

Recent data: In the latest edition of the Focus Bulletin, the median projections pointed to a reading of 0.32% in June, which would be a slowdown from 0.58% recorded in the previous period.

- Despite the slowdown, the result would push inflation accumulated over the last 12 months from 4.72% to 4.81%, above the tolerance band of 4.5%.

- The latest reading of the Broad Consumer Price Index 15 (IPCA-15) showed a similar trajectory. Despite monthly deceleration, still elevated readings increased accumulated inflation.

- In the second-quarter Monetary Policy Report (MPR), the Central Bank raised its projections for accumulated inflation at the end of 2026 and 2027 to 5.2% (+1.3 p.p.) and 3.7% (+0.4 p.p.), respectively.

- In this scenario, inflation would only return to tolerance margins in the second quarter of 2027, indicating worsening price control after the Middle East conflict.

Brazilian political and electoral scenario

Expected impact on the BRL exchange rate: bullish

Last week, the BRL exchange rate was again pressured by perceptions of political risks for Brazilian assets due to investors' sensitivity to the presidential race.

- In this context, investors may react to the participation of pre-candidate Flávio Bolsonaro in a public hearing in Washington on Monday, July 7, regarding the proposed 25% tariffs on Brazil.

Why this matters: If Flávio's participation negatively impacts investors' perception of his chances of victory, it could increase political risk perceptions for national assets and weaken the real.

Fiscal concerns: In recent months, investors have already reacted negatively to news related to the electoral cycle, such as after the definition of pre-candidates Luiz Inácio Lula da Silva and Flávio Bolsonaro for the presidency.

- In practice, recent reactions from financial market agents reveal a preference for the election of a new president who could be more conservative in fiscal policy.

Worsening risk perception: Last week, the release of voter intention polls showing an increase in President Lula's lead over Flávio worsened investor risk perceptions for national assets.

- This risk perception intensified after the US Treasury Department announced sanctions against Brazilians and companies for alleged links to the criminal faction PCC.

- Both the imposition of punitive tariffs on Brazil and the designation of criminal factions as terrorist groups were US actions linked to the Bolsonaro family, representing sensitive points for the national electorate.

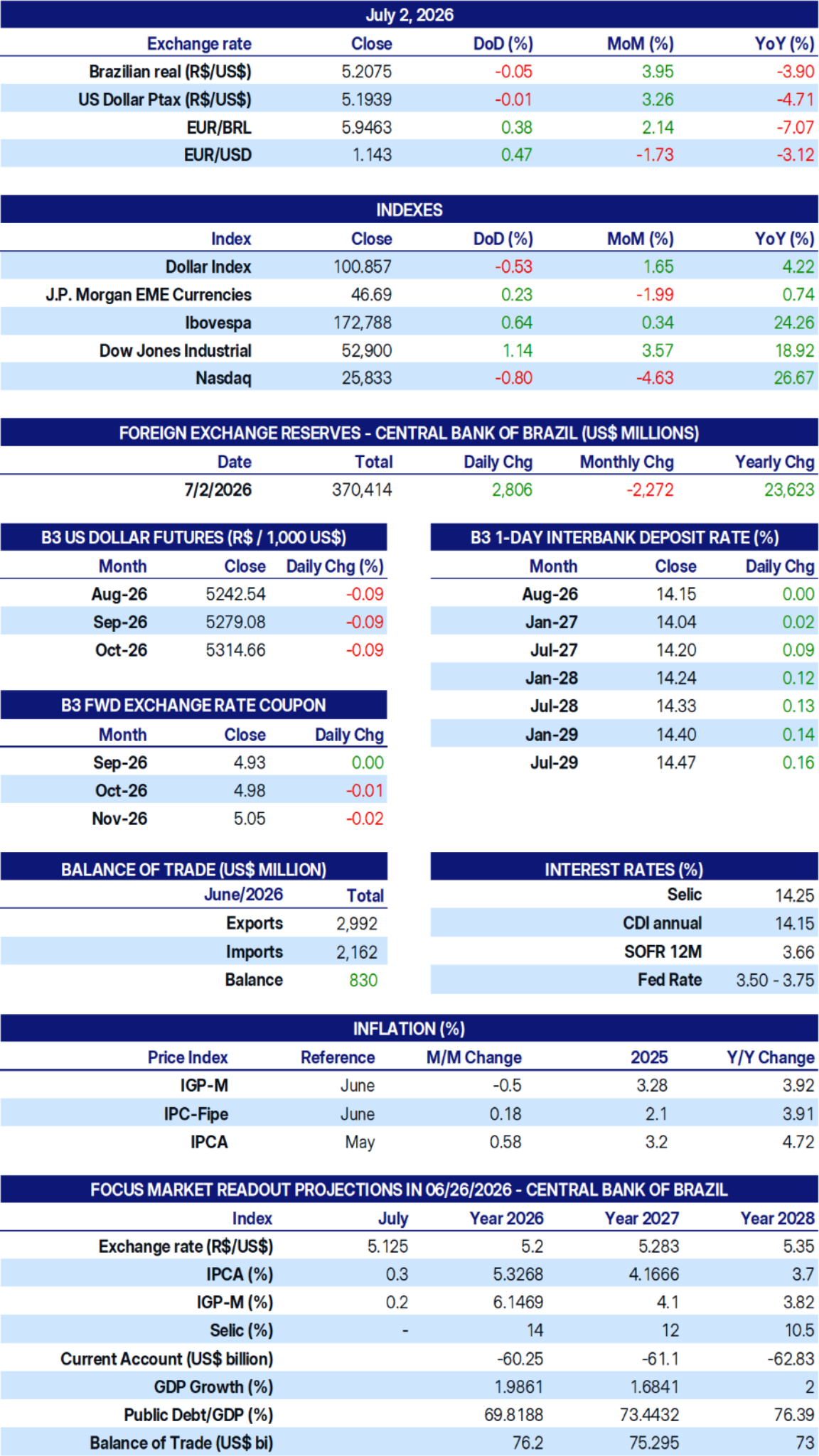

INDICATORS

Sources: Central Bank of Brazil; B3; IBGE; Fipe; FGV; MDIC; IPEA; and StoneX cmdtyView.