US Bank Earnings; US CPI; China GDP: Top Event Risk Ahead

Talking Points:

- The major US equity indices are on the verge of more significant technical shifts as demonstrated by the S&P 500 and its head-and-shoulders pattern

- Key themes are important for establishing necessary follow through, so key events like US bank earnings and CPI taping growth and rate forecasts

- China’s economy is increasingly in focus with trade pressures swelling, but traditional macro is on tap this week with the country’s 4Q GDP

The global macro, economic docket hosts some serious event risk over the coming week; but that isn’t what raises the risk of tangible market movement. Rather, looking to the fundamental backdrop and the market’s observance of themes, there has been a more serious shift afoot. We can see that weight in the performance of the S&P 500 leaning heavily on the support of its head-and-shoulders pattern or the growing reference to ‘bearish’ terms and concerns in social and search measures.

S&P 500 with Volume and 100-Day Moving Average (Daily)

Source: John Kicklighter, TradingView

On a purely historical basis, the third week of the fiscal year averages a positive performance for a benchmark like the S&P 500 but volatility is also higher. That natural degree of sensitivity paired with ‘a reason to be concerned’ creates a much more dangerous environment for sentiment moving forward.

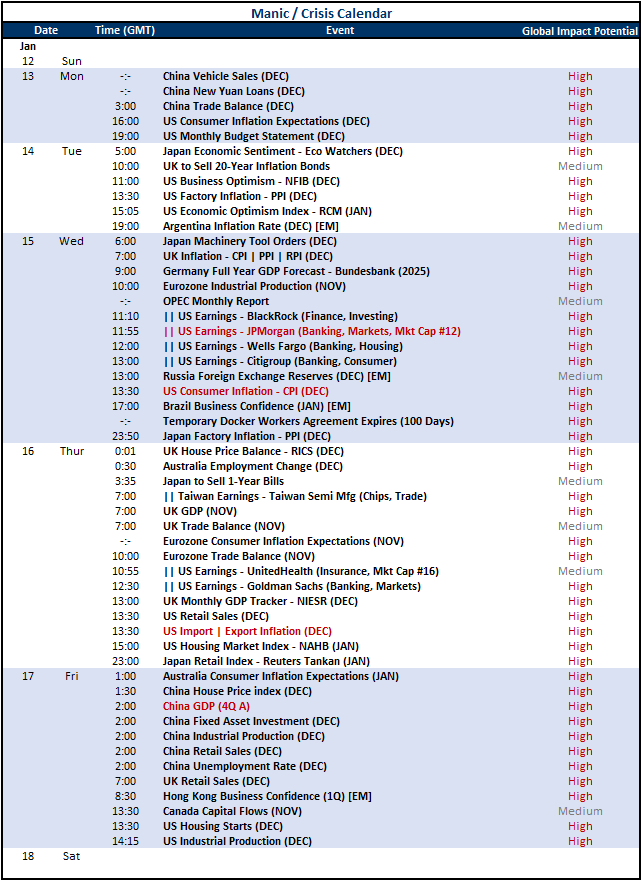

Calendar of Major Global Macro Events Scheduled for Week

Source: John Kicklighter, StoneX

Amid this sensitivity to meaningful fundamental developments, it is particularly important to watch for scheduled updates that will tap into deeper (and conveniently overlooked) concerns. With monetary policy, trade and growth themes all on unstable ground; the typical ‘victory lap’ event of US corporate earnings can shift into a potential threat from reliable bullish benefactor. As is the norm, the major players in the financial sector are set to report their past quarter’s performance. There is both an aggregate and detail consideration to these corporate reportings.

Should the likes of JPMorgan, Citibank and BlackRock all disappoint or come disappointingly in-line; broader markets may pay the price. That said, look to those unique perspectives like market health (JPM), consumer wealth (C) and investment trends (BRK) among other financial aspects. Also, it is worth noting the planned release of Taiwan Semiconductor Manufacturing’s performance as an insight into tech via AI.

S&P 500 Overland with the SPDR Financial ETF and 10-Day Correlation (Daily)

Source: John Kicklighter, TradingView

In addition to CFA-favored financial considerations, this week’s docket will also hit squarely on the macroeconomic interests through the December US CPI release. We have seen a massive swing in FOMC rate expectations in relatively few months thanks to FOMC messaging and key data. The US central bank operates on a dual mandate between ‘full employment' and low but steady inflation objective (considered 2.0 percent). This past week, the fear that labor markets would crack as a precursor to an economic stall fell apart with an upside surprise.

That shifted the attention back on price pressures which seemed to have already bottomed out as of late in both the US and the rest of world. A steady reading from CPI could still feed the concerns that further accommodation is off the table. Should it tighten even modestly, the opposite could generate a disproportionate market response.

Chart of S&P 500 Overlaid with Implied Rate Cuts by FOMC in 2025 (Daily)

Source: John Kicklighter, TradingView

Finally, in the list of top profile event risk to keep tabs on for the week, the Chinese 1Q advanced GDP report and key December readings will be high priority. Usually, these kind of figures are just very recognizable, but international market participants take them with a heavy dose of salt.

The veracity of the data is frequent questioned, but the flow of capital always taints the interpretation of the figures. Yet, we have seen both Chinese capital market benchmarks (like the Shanghai Composite) and the local currency (the yuan) suffer from significant pressure. It’s hard to ignore when trade wars are one of the systemic focal points. Should the data post a measurable miss, the market is unlikely to overlook the update.

Chart of Shanghai Composite Overlaid with Tencent (Daily)

Source: John Kicklighter, TradingView

-- Written by John Kicklighter, Global Head of Content