FX Weekly Overview (Brazil Issue)

Dollar to reflect US economic data, Central Bank minutes, inflation in Brazil, and the Middle East

Leonel Mattos

- Currencies

Quarterly Commodities Outlook is available for free now. Download your report →

By: Matt Weller, Head of Market Research

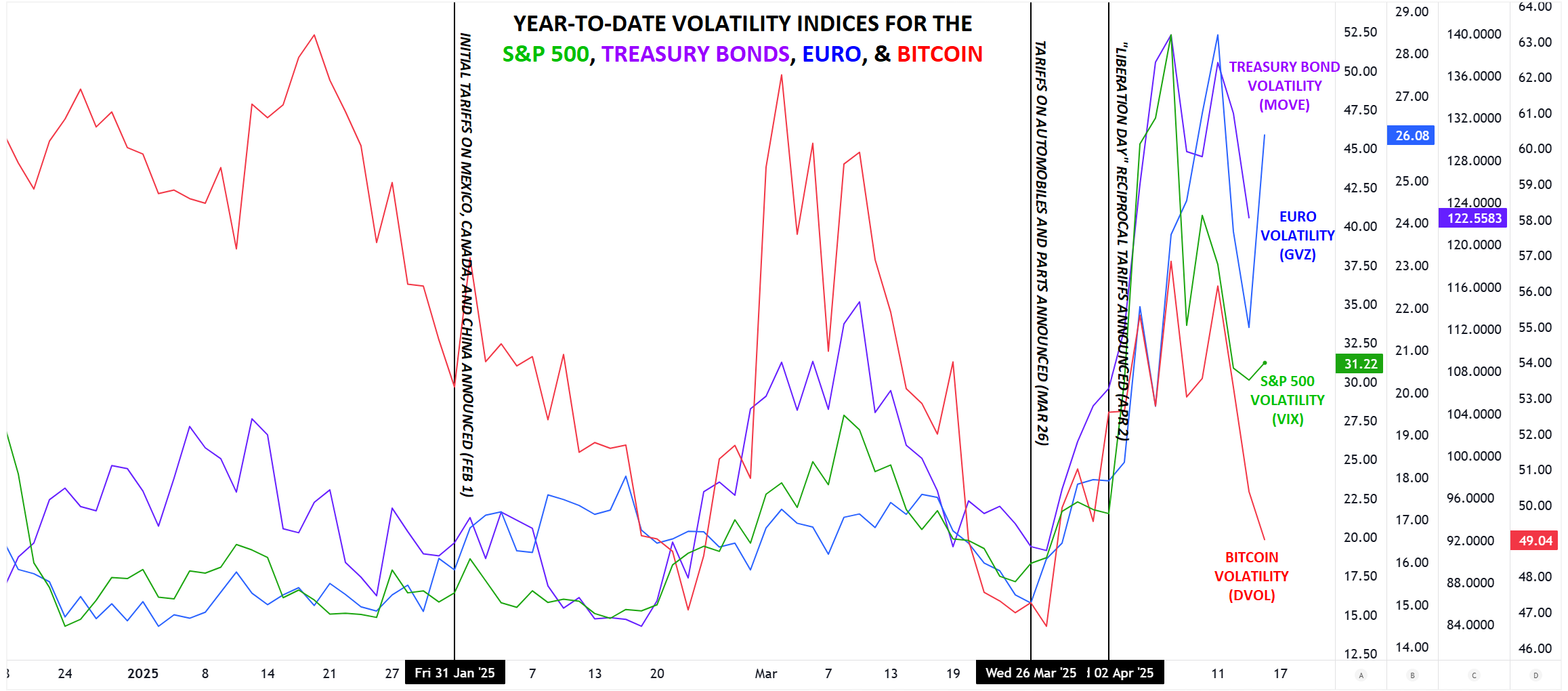

S&P 500, Treasury Bond, Gold, and Bitcoin Market Volatility Key Talking Points:

“Survive until 2025” was a mantra for many investors and businesses following the global recession scare in 2023 and 2024’s pervasive geopolitical uncertainty, spanning everything from elections in the UK, European Union, and US to military conflicts in Ukraine and the Middle East.

A bit over a quarter of the way through 2025 though, anyone looking for a decline in uncertainty should be on the lookout for a new mantra: “Exist and persist until 2026” perhaps? Below, we examine the timeline of US President Trump’s global trade war and its impact on volatility in major markets, highlighting relative changes in expected market moves in the stock, bond, currency, and crypto-asset markets:

Source: StoneX, TradingView

Below, we provide detailed volatility outlooks across major markets, beginning with equities.

In the chart above, the black vertical lines represent major escalations in the Trump administration’s tariff policy. The first black line marks the unexpected February 1st announcement of tariffs on China, Mexico, and Canada ostensibly over those countries’ failure to reduce the flow of fentanyl into the US. Broadly speaking, we saw a short-lived uptick in volatility that quickly died down as the tariffs on Mexico and Canada were quickly delayed.

The second black line shows the surprise tariff decree on automobiles and auto parts on March 26th, which essentially marks the low for expected volatility in major markets as traders started to realize that the upcoming “reciprocal tariffs” could be far more substantial and longer lasting than anticipated. Even relative to those increased expectations, the figures for the “Liberation Tariffs” still surprised traders, and the lack of progress toward any meaningful trade deals since then has left market volatility at historically high levels, even despite (or perhaps, because of) the 90-day suspension of most of those tariffs.

As of writing, volatility in the stock, bond and commodity markets remains relatively elevated, suggesting that market moves may be larger than most were predicting at the start of the year, though implied volatility in Bitcoin has declined from the start of the year.

Starting with the stock market, the VIX, Wall Street’s “Fear Gauge” of implied volatility in the S&P 500 sits above 30, down nearly 50% from the peak seen a couple weeks prior. At this level, the VIX suggests that options traders expect daily moves of nearly 2% in the S&P 500 and weekly moves of about 4.3%.

Compared to the average VIX reading of 19.5 since inception in 1990, stock market volatility is elevated, but still well below the peaks seen in the depths of the Great Financial Crisis, COVID pandemic, and even the brief “Volmageddon” surge in August of last year. For reference, the current reading is in the 97th percentile of all daily VIX readings over the last year, indicating that expectations for future volatility remain highly elevated. The outlook for major multinational earnings remains highly uncertain, but US corporations have proven adept at protecting their profit margins and continuing to generate consistent shareholder returns over longer-term time horizons regardless of international trade policies.

Like the stock market, implied volatility in the Treasury bond market is much higher than it has been most of the decade, but still below the peaks seen in Great Financial Crisis and the (non-)“transitory” inflation scare of 2022, roughly matching the peak seen in during the COVID pandemic. At current levels above 110, the MOVE sits at the 86th percentile of all daily readings over the last year.

Moving forward, the key factors for bond traders to monitor will be the stability and independence of the Federal Reserve’s interest rate policies, along with the broader appetite for holding US Treasuries amidst fears of record high debt loads and the ever-elusive “bond vigilantes.”

After a prolonged period of mostly low volatility over the last few years, expected market moves in the commodity market broadly, and gold in particular, have spiked to historically elevated levels. Per the CBOE’s GVZ index, implied market moves are higher than they’ve been since COVID (and the Greek Sovereign Debt Crisis and Great Financial Crisis before that), and in the 99th percentile of all readings over the last year.

With fractures emerging in long-maintained geopolitical and trading relationships, volatility in the commodity market may remain elevated in the near term until the outlines of a new, sustainable equilibrium come into sight. In other words, gold traders may want to prepare for prolonged volatility more akin to what we saw in the early 2010s rather than the subdued post-COVID average.

In contrast to the far more mature stock, bond, and commodity markets, traders in the relatively young crypto sector are accustomed to significant volatility. Indeed, volatility in the Bitcoin, the longest-standing cryptoasset, has generally declined since the blockchain’s “Genesis Block” in 2009. Looking at the above chart, the implied volatility in Deribit’s DVOL index is approaching 9-month lows. The index of implied volatility sits at just its 10th percentile of all daily readings over the last year.

Ultimately, growing acceptance of Bitcoin as an emerging asset class and a maturing set of increasingly institutional investors should continue to push Bitcoin’s volatility lower over time, regardless of US trade policy. A sustained global trade war might further encourage Bitcoin adoption as investors seek alternatives outside traditional finance, potentially leading to even lower volatility.

From a purely fundamental perspective, there is a case that we’ve already passed the peak in trade-driven uncertainty; after all, it’s difficult to surpass the ambiguity created by imposing – and then subsequently delaying – the most significant changes to global trade policy in at least a century. Progress toward trade deals, especially between the US and China, would likely reduce implied volatility. Even if tariffs remain historically high, traders would benefit from increased clarity, contrasting the unpredictable environment of recent months.

What are the major events and indicators on tap for the global economy that could charge volatility in markets and reshape deeper fundamental themes? Sign up for the updated Global Macro Calendar updated each week with a two week look ahead of the top events!

Sign Up

-- Written by Matt Weller, Global Head of Research

Check out Matt’s Daily Market Update videos on YouTube and be sure to follow Matt on Twitter: @MWellerFX

The subsidiaries of StoneX Group Inc. provide financial products and services, including, but not limited to, physical commodities, securities, clearing, global payments, risk management, asset management, foreign exchange, and exchange-traded and over-the-counter derivatives. These financial products and services are offered in accordance with the applicable laws in the jurisdictions in which they are provided and are subject to specific terms, conditions, and restrictions contained in the terms of business applicable to each such offering. Not all products and services are available in all countries. The products and services offered by the StoneX Group of companies involve risk of loss and may not be suitable for all investors. Full Disclaimer. This content is not intended for residents of any particular country, and the information herein is not advice nor a recommendation to trade nor does it constitute an offer or solicitation to buy or sell any financial product or service, by any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation. Please refer to the Regulatory Disclosure section for entity-specific disclosures. No part of this material may be copied, photocopied or duplicated in any form by any means or redistributed without the prior written consent of StoneX Group Inc. The information herein is provided for informational purposes only. This information is provided on an ‘as-is’ basis and may contain statements and opinions of the StoneX Group of companies as well as excerpts and/or information from public sources and third parties and no warranty, whether express or implied, is given as to its completeness or accuracy. Each company within the StoneX Group of companies (on its own behalf and on behalf of its directors, employees and agents) disclaims any and all liability as well as any third-party claim that may arise from the accuracy and/or completeness of the information detailed herein, as well as the use of or reliance on this information by the recipient, any member of its group or any third party.

© 2026 StoneX Group Inc. all rights reserved.

Our subscribers have access to comprehensive market analysis from StoneX spanning commodities, equities, currencies and more.

Dollar to reflect US economic data, Central Bank minutes, inflation in Brazil, and the Middle East

US indices have led sentiment to fresh highs this past week even as the fundamental backdrop struggles to present a solid foothold. Will thin liquidity aid or hamper the swell and what does the event risk ahead propose?

A softer run of U.S. data is doing more to move the U.S. dollar than any chart, with a jobs report and an inflation print set to land back to back. A cooler U.S. CPI report would hand the Federal Reserve room to ease, and that prospect is already loosening the dollar's grip.

Our market expertise, advanced platforms, global reach, culture of full transparency and commitment to our clients’ success all set us apart in the financial marketplace.

Reach

With access to 40+ derivatives exchanges, 180+ foreign exchange markets, nearly every global securities marketplace and numerous bi-lateral liquidity venues, StoneX’s digital network and deep relationships can take clients anywhere they want to go.

Transparency

As a publicly traded company meeting the highest standards of regulatory compliance in the markets we serve; our financials and record of accomplishment are matters of public record. StoneX’s commitment to “doing the right thing over the easy thing” sets us apart in the industry and helps us build respect, client trust and new partnerships.

Expertise

From our proprietary Market Intelligence platform, to “boots on the ground” expertise from award-winning traders and professionals, we connect our clients directly to actionable insights they can use to make more informed decisions and achieve their goals in the global markets.