Top Global Macro Event Risk This Week: China Rate Decision; Nvidia Earnings; November PMIs

Talking Points:

- China is the only major central bank updating its monetary policy mix, and the economic backdrop and incoming Trump administration is sharpening the focus

- The US market’s top market cap stock is due to report earnings this week and Nvidia’s strength or weakness may spread to the broader market

- Thematically, the November PMIs will cross the wires towards the end of the week, but will this series’ tame impact of late be overridden by the importance of its contents – growth?

The turn in risk appetite to close out this past week was unmistakable with Friday’s substantial gap lower for the likes of the Nasdaq 100 and S&P 500 leading to sizable weekly retreats from record highs – and the NDQ to its first 5-day slide since January. As impressive as the retreat was this past week, it really stands out because of the consistent and bullish trend that preceded it. Low volatility and a prevailing wind will naturally be confronted with corrections over a long enough time frame, but that doesn’t necessarily mean that the markets have seen a systemic shift in course.

Adding to the complication around charting the map ahead is the contrast between the seasonal expectations for the 47th week of the year (which averages the third worse weekly loss for the SPX of the calendar year) versus the lack of clarity around what would really take up the banner of a meaningful bearish trend moving forward. Looking at the economic calendar this week, there isn’t a high-profile event upon which we could set a reliable expectation that a systemic trend will be defined. Nevertheless, there are top events to be monitored.

Table of Major Global Macro Events Scheduled for Week

Source: John Kicklighter, StoneX

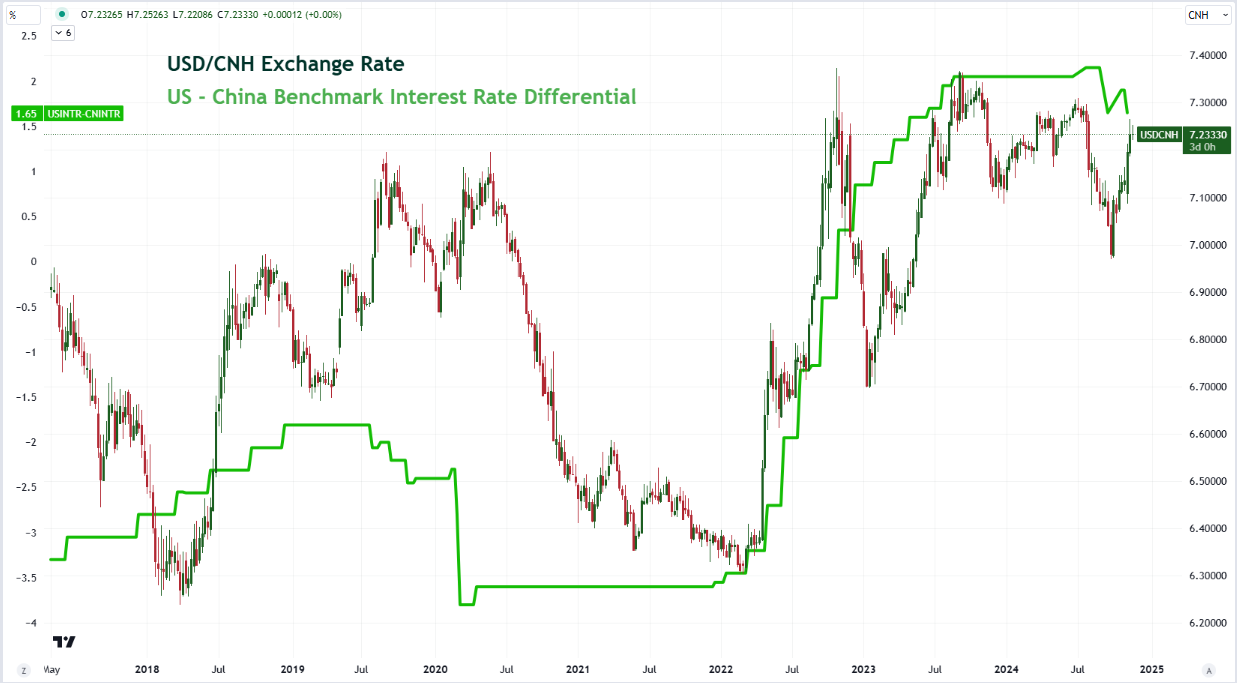

While it has taken something of a back seat among the major systemic drivers of late, the wavering of the Chinese growth machine remains a serious threat to global expansion and capital flow. We aren’t due any key economic health checks for the second largest economy in the world over the coming week – not that most take them at face value – but we are expecting the decision around the equivalency of China’s benchmark interest rate.

The PBOC’s 1-year loan prime rate (along with the 5-year) is due Wednesday morning. Though there have a been a few cuts recently, authorities are expected to hold at this particular meeting following the run of (arguably underwhelming) stimulus programs announced in the past weeks. This is a reminder that regardless of the efforts being made, it is not exactly clear what can really re-establish confidence in the incredible multi-decade rise in this country’s economic status.

Chart of USD/CNH and US-China Benchmark Rate Differential (Weekly)

Source: TradingView, John Kicklighter

In a significant deviation from the global macro, speculators will find one of the more pointed updates to weigh in on over the coming week: the earnings report from Nvidia. The majority of the major US companies have already reported their corporate figures and there has been a general trend of ‘better than expected’ results, but share response to this bias was notably deviating from textbook expectations. After the run of top market cap tech reports a few weeks back, we are left with the last of the Magnificent 7 to release its stats.

Nvidia is the largest company by market cap and has been the fastest growing among its peers with a particular connection to a surge in popularity around AI. That makes it prone to be a speculative interest flashpoint. That puts a lot of weight around its potential impact. That said, given the other tech leaders ticker vs report performance, it is worth keeping a greater awareness for any disproportionate bearish responses to any disappointment.

Chart of Nasdaq 100 Overlaid with Nvidia and the 10-Day Correlation (Daily)

Source: TradingView, John Kicklighter

For the third, top fundamental listing, there is a lot to pick from: like UK or Japanese CPI, US housing data or even the G20 summit. However, I am more keen on the end-of-week thematic consideration around November developed world PMIs. These are good (and timely) proxies for economic activity for some of the largest economies in the world. In turn, that is a better reflection of the global growth course.

Most of the major players expected to list for the month softened this past month with the notable exception of the United States. That represents a particular implication for overall risk appetite as we plot the course of traditional fundamentals, but it also carries weight as far as the performance of the US Dollar relative to its major counterparts. Just remember: with a Friday release date, there will be limited capacity for follow through on any theme momentum with the onus of the weekly liquidity drain.

Chart of USDJPY and US-Japan 2-Year Yield Spread (Daily)

Source: TradingView, John Kicklighter

-- Written by John Kicklighter, Global Head of Content

The subsidiaries of StoneX Group Inc. provide financial products and services, including, but not limited to, physical commodities, securities, clearing, global payments, risk management, asset management, foreign exchange, and exchange-traded and over-the-counter derivatives. These financial products and services are offered in accordance with the applicable laws in the jurisdictions in which they are provided and are subject to specific terms, conditions, and restrictions contained in the terms of business applicable to each such offering. Not all products and services are available in all countries. The products and services offered by the StoneX Group of companies involve risk of loss and may not be suitable for all investors. Full Disclaimer. This content is not intended for residents of any particular country, and the information herein is not advice nor a recommendation to trade nor does it constitute an offer or solicitation to buy or sell any financial product or service, by any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation. Please refer to the Regulatory Disclosure section for entity-specific disclosures. No part of this material may be copied, photocopied or duplicated in any form by any means or redistributed without the prior written consent of StoneX Group Inc. The information herein is provided for informational purposes only. This information is provided on an ‘as-is’ basis and may contain statements and opinions of the StoneX Group of companies as well as excerpts and/or information from public sources and third parties and no warranty, whether express or implied, is given as to its completeness or accuracy. Each company within the StoneX Group of companies (on its own behalf and on behalf of its directors, employees and agents) disclaims any and all liability as well as any third-party claim that may arise from the accuracy and/or completeness of the information detailed herein, as well as the use of or reliance on this information by the recipient, any member of its group or any third party.

© 2026 StoneX Group Inc. all rights reserved.