Global values have been weak since the March edition. Could they push higher in April? Absolutely...but it would take a lot of things coming together to make that happen. Much like every parley bet I have taken, it never works out!!!

India has shocked the market in delaying their purchase tender. After failing as hard as they did in December and January, it was nearly a guarantee that they would make an announcement in February...until they didn't. The rest of the global buyers picked up on their approach and delayed their own purchases. The result has been a market largely void of demand which has sent values sliding.

While there is a path to higher prices from where we sit today, there are many more paths pointing lower. Buyers have made their will known and supplies have grown as a result. More importantly is the calendar. We are already nearing what would be considered typical summer reset months. That is going to weigh more and more on sellers minds.

If we see a situation where India announces their purchase tender and as a result, we see a lot of other major buyers step in, we could see a competition for tons that leads prices higher...but that is not our expectation. We are watching for prices to slide a bit as we look to May.

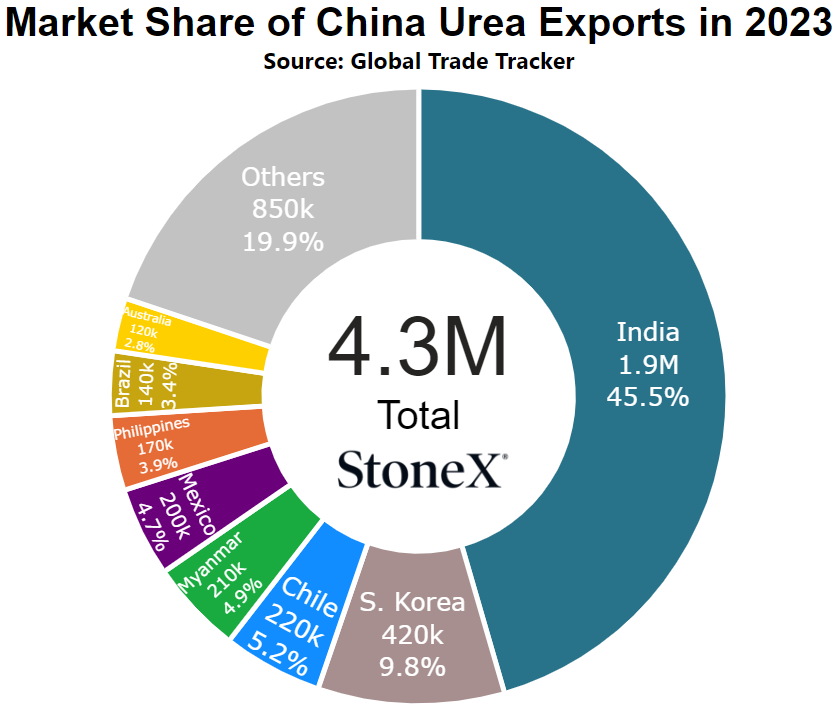

Chinese urea exports remain very low...will it every improve?

For those in the market that had been holding out hope that Chinese urea exports would return to start 2025 have been left disappointed.

China plays a major role in the global urea marketplace. Typically speaking, the global export marketplace ranges from 50 - 55M tons per year. To put China into context, their recent history had them around 10% of that total or around 5 - 5.5M tons per year. Their participation, or lack of participation, went a long way in determining the market. When they were exporting heavily, it was widely seen as a bearish signal as the market feared competing against a Chinese ton. When China scaled back on exports, it was widely seen as a bullish event.

The lack of Chinese exports has played a big part in global urea prices staying higher.

In late 2021/early 2022, global urea supplies were extremely tight and prices were skyrocketing. This caught the attention of the Chinese government. Rather than allow free market forces to dictate what was to happen, the Chinese government stepped in with two goals:

1. Ensure adequate supplies for Chinese farmers.

2. Lower domestic prices vs the world for domestic farmers

Fortunately for Chinese farmers, this strategy worked like a charm.

Unfortunately for the rest of the world, this strategy worked like a charm.

This story really came to a head last year (2024) when Chinese exports dipped to historically low ranges. Only around 266K tons TOTAL were shipped from Chinese ports. The result is that Chinese farmers have been enjoying some of the cheapest urea values in the world. We also continue to see and hear reports that point to extremely high inventory levels. This was seen by some as a sign of export hope as we began 2025.

January and February Chinese trade data sure disappointed that crowd.

Only 4,000 tons between the 2 months were exported. A country that normally exports north of 400K tons per month was unable to even reach 5 figures. Needless to say that this has disappointed those hoping for lower prices in the near term.

Now, there is still some hope that things will improve in 2025. We continue to see and hear that urea operating rates within China remain very high which basically means they are producing a lot of product every day. We also continue to see and hear that urea stockpiles in China remain at record high levels. So if inventories are at high levels and they are still producing a lot every day, the hope is that exports will have to resume. If that plays out, then global urea markets will trend lower for fear of the competition, giving global farmers a chance to lock in lower prices.

One word of caution, never expect China to do what you think it will do.

Most of the world looks at fertilizer from a free market perspective. We think that timing, pricing, etc. determine what will happen. That isn't always the case with China. They see things from a communist POV. One of the biggest dangers to communism is not outside forces. Rather, it is an uprising by its people. Who is one of the largest blocks of people in China? Farmers. By taking steps to keep domestic fertilizer prices low, that is seen as a win by the largest block of people. In recent months, the mere rumor that exports were going to start being allowed caused domestic Chinese values to rise. No doubt this was seen by government officials who will use this information going forward.

Hopefully as we move past the Chinese spring season, we will start to see exports resume and give global farmers some much needed relief. Until that time, the world continues to operate without one of its largest suppliers.

What does this mean for Aussie farmers?

Long story short: it means lower inventories/supplies and as a result, higher global prices.

China normally represents 10% of the global urea export marketplace. They were significantly lower than normal in 2024 and the January / February data for this year are much worse. Can their export flows improve thru 2025? Of course. That is a bearish factor we will be watching very closely. However, until we see those tons return, it sets an even higher price floor for the world.

Given that Australia is quickly moving toward its urea season and historically has seen a decent chunk of Chinese product be imported, importers have to continue to look to secondary and third supply points which generally brings with it higher logistical costs and longer shipment times.

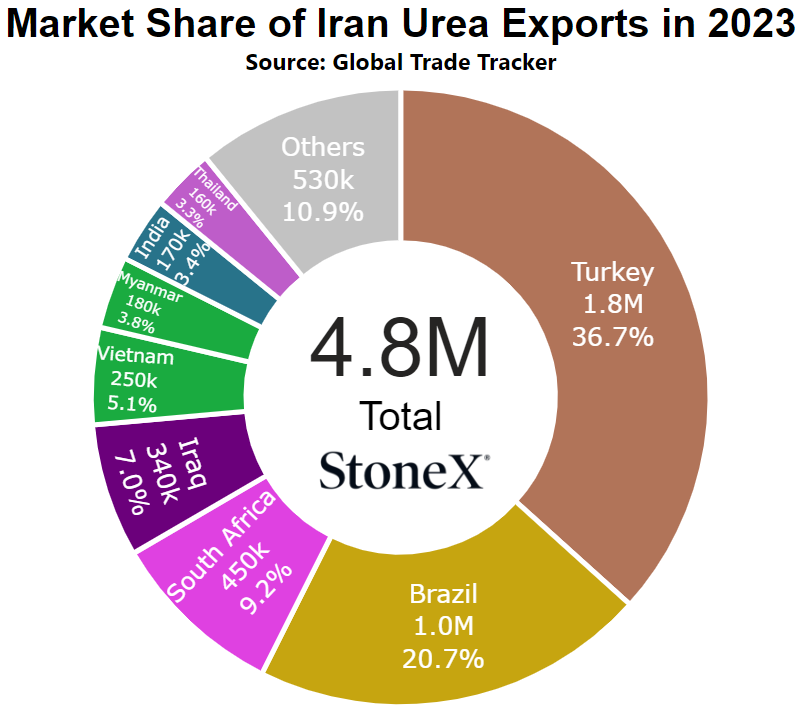

Iranian urea production back to 100%...but damage already done

Many in the urea global market looks at Iranian production/exports and thinks "they do not matter because I cannot do business with them".

I am here to tell you that is a VERY dangerous approach to the market.

Much of the free world looks at Iran as inconsequential due to long-term heavy sanctions. These sanctions means an inability to do business with their urea manufacturers. That ultimately means it is very easy to effectively write them off when looking at the overall market.

However, even though one cannot do business directly does not mean those tons do not matter to the overall global S&D.

The world spends a lot of time discussing Chinese export approaches due to their size. What I think many miss is Iran's typical size. In 2024, 4.8M tons left Iran for the world...nearly the same size that China would historically ship. So if we spend so much time and effort trying to figure out what China will or will not do, we should do the same for Iran.

So, back to these long term sanctions.

These have made it very hard for companies in Iran to do business. Not only is it hard to find global experts willing to come and work on facilities, it is also hard to secure parts needed to repair/replace old machinery. We believe 2025 started with this being an issue for their natural gas markets.

Very early in the year, we started to hear reports that Iranian urea production was slowing/stopping due to a lack of gas supplies. Some quickly decided that it was largely a short-term event that was tied to larger winter domestic demand. However, it lasted much longer than that. It wasn't until a couple weeks earlier that we finally heard production returning to normal rates. As is typical, firm details can be hard to find but we believe nearly two months of production was lost. That equates to around 750K tons.

In this current market, that loss hurts.

The global urea market is already dealing with a lack of Chinese exports and European production remains around 75% of normal. Those two events have removed most, if not all, of the excess product around the world. That means it is either very hard or impossible to lose more production like Iran. Having this happen in the lead up to the Northern Hemisphere spring season also doesn't help.

Fortunately, their production has returned which means worst case scenarios are now taken off the table but damage has been done...

What does this mean for Aussie farmers?

Long story short: this takes some higher price scenarios off the table and helps to settle the market.

European production has been at 75% for a while. Chinese exports are nearly non-existent. Having Iranian production offline was just another reason for global prices to move higher.

As mentioned, many around the world act as though Iran product doesn't matter since they cannot do business with them but even indirectly, they matter. Iran exports nearly as much as China used to. They are just under 10% of the global export marketplace. When their production was down, their typical buyers were forced to other supply points which pushed out their normal buyers. It causes a domino effect.

Whether someone buys from them or not, they matter. When their production was down, it supported price ideas. While their production returning will not make up for what was lost, it does at least stop the hemorrhaging.

If the global S&D is so tight, why are prices falling?

One of the big surprises of the last month is how bearish urea values have been. Global supplies are incredibly tight with Chinese exports extremely low, Europe still struggling with high nat gas prices, and Iranian production going offline for the better part of 2 months. Global production has struggled to keep up with global urea demand and the difference between the two today is relatively narrow.

Even with that situation, if you look below, you will see that a lot of price points went down over the last 30-days. What gives?

A lot of it goes to India who drug their feet on their hotly anticipated purchase tender.

For those new, India has been trying to buy a big block of tons since December. They announced mid-December their intention to buy 1.5M tons but only secured around 200K (going off memory on these numbers). After falling so short, they announced a fresh tender in January for 1.5M tons. They did better, but still well short with just under 600K tons secured.

Many in the industry, myself included, thought that we would see them return mid-February for a third try. The global urea market heated up on price with buyers scurrying to lock up prices before they went higher. Mid-February came and went...no tender. Late-February came and went...still no tender. Once the calendar turned to March, many started to ponder just how long they could wait to buy. Other global buyers started to see some price pressure and opted to hold back in hopes of further price deterioration.

As fertilizer does, when demand goes quiet, prices tend to slide and slide they have.

However, last week saw India announce their tender. They are looking for...you guessed it, 1.5M tons!! 800K for west coast ports and 700K for east coast ports. The return of India has helped the urea market find its footing and prices have been on the rebound. As I write this, many of the global values are even closer to where they were before the slide.

This is just the fertilizer market. There was some surprise that India could wait as long as they could, but everyone knew they had to come back. Regardless, prices slid. Now, no one is surprised that India did announce the tender...but prices are up anyways. Sometimes the emotion of a market can dictate price better than the fundamentals.

At the end of the day, global supplies are still very snug so seeing this correction higher isn't a surprise...but we will need to see how long it lasts because the summer months are looming.

What does this mean for Aussie farmers?

Long story short: it provided a small/short window for importers to secure a few vessels at a lower price.

This story was pretty short lived. It started with prices starting to show weakness in late February and was in place until the India tender last week. Now, prices have jumped. Not back to their previous high's, but higher.

This should be a reason to have a conversation with your supplier. They may have some cheaper tons (vs today's replacement values) that they can offer. This will not be a deep layer as the world is now higher priced (will that hold, who knows). It is worth a conversation for at least a layer.

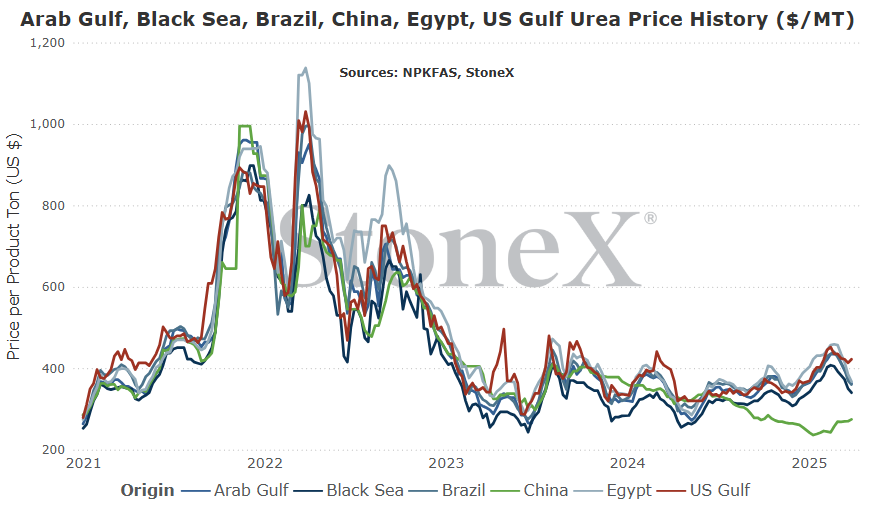

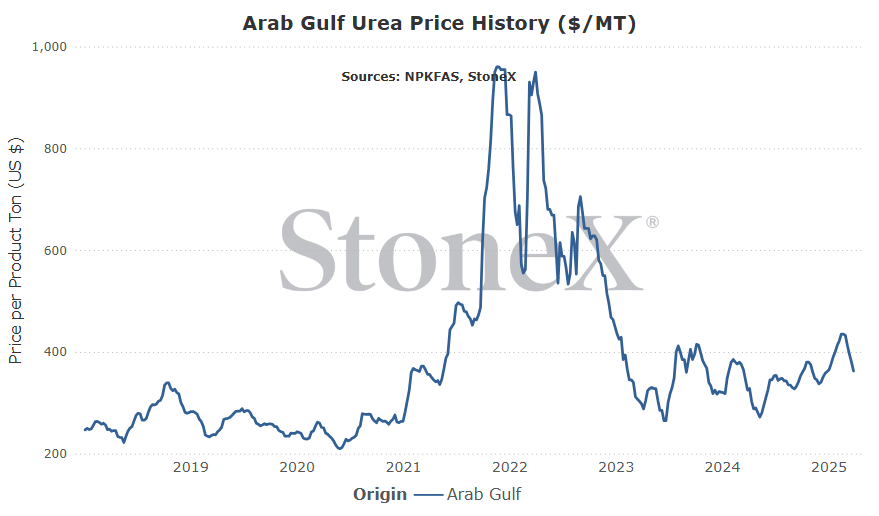

Vs 30 days ago - -16% or approximately $70 lower

Vs 90 days ago - -1% or approximately $3 lower

Vs 6 months ago - 3% or approximately $10 higher

Vs 1 year ago - 12% or approximately $38 higher

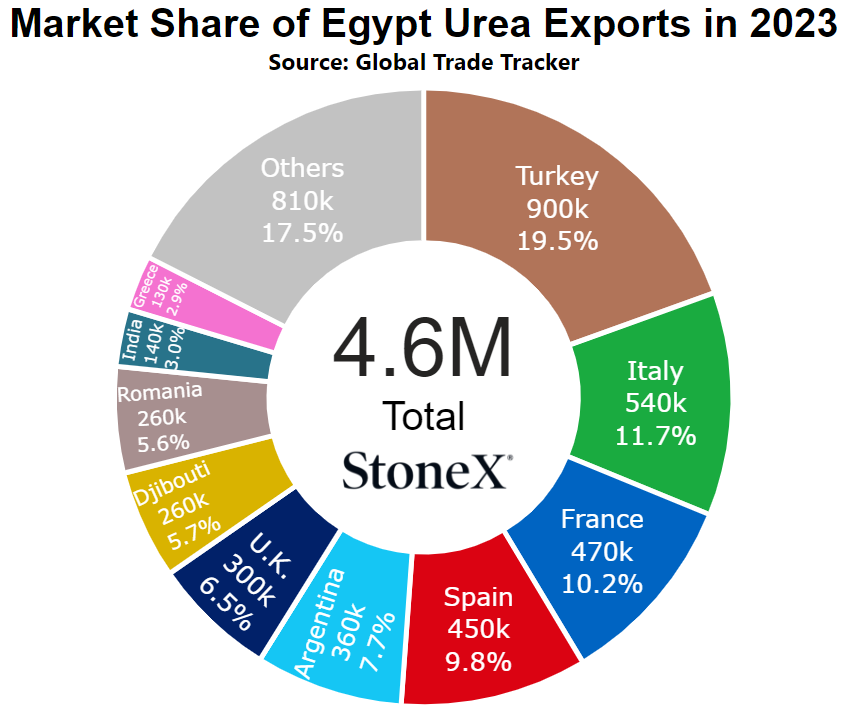

Egypt

Number 4 global exporter in 2022

Price comparisons

Vs 30 days ago - -20% or approximately $90 lower

Vs 90 days ago - -9% or approximately $37 lower

Vs 6 months ago - -1% or approximately $5 lower

Vs 1 year ago - 11% or approximately $37 higher

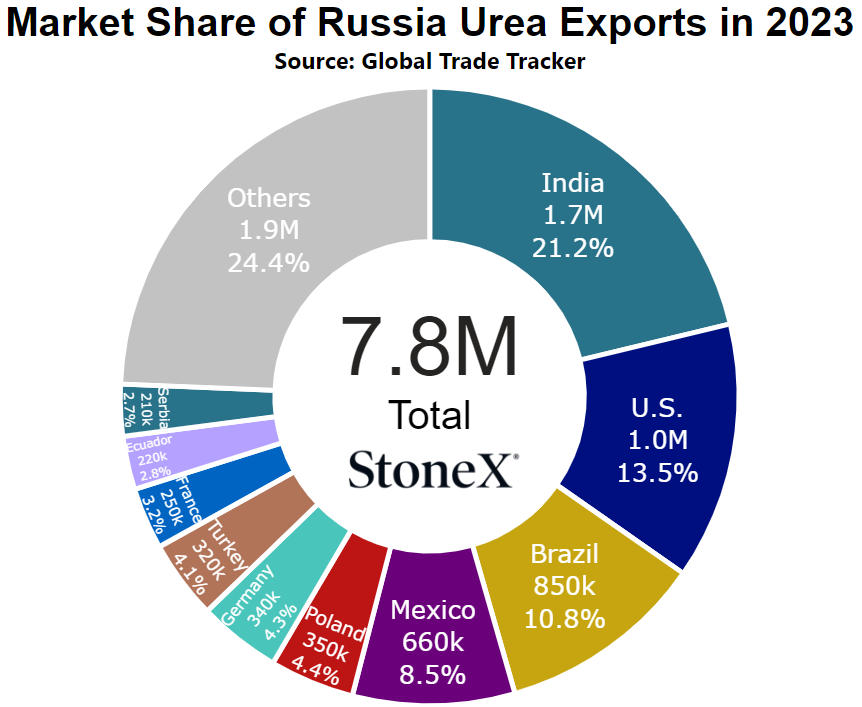

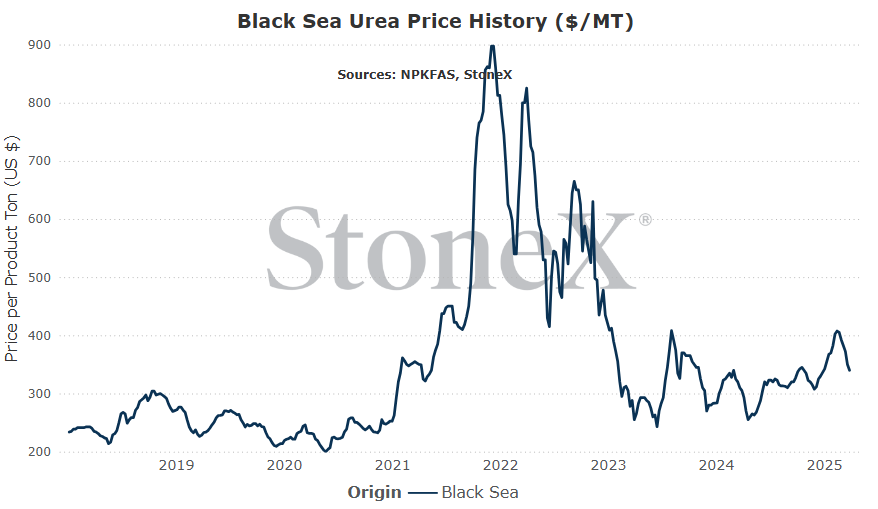

Black Sea

Number 1 global exporter in 2022

Price comparisons

Vs 30 days ago - -13% or approximately $53 lower

Vs 90 days ago - -1% or approximately $3 lower

Vs 6 months ago - 4% or approximately $13 higher

Vs 1 year ago - 11% or approximately $35 higher

China

Number 9 global exporter in 2022

Price comparisons

Vs 30 days ago - 2% or approximately $6 higher

Vs 90 days ago - 14% or approximately $33 higher

Vs 6 months ago - 1% or approximately $2 higher

Vs 1 year ago - -17% or approximately $56 lower

- India is met with other buyers/proud sellers - India took their sweet time with their purchase tender announcement, but that delay worked to their favor. Had they announced in mid-February as we previously believed, it would have been more fuel to the bullish fire. By delaying to now, their shipment window goes well into summer months and removes a lot of bullish potential. If other global buyers mostly stay away/quiet, it is likely this tender will not push prices higher. However, if buyers come from the woodwork, different story. That is one of the bigger things we are watching. Who follows India, if anyone.

- Any further unexpected production outages - the world just got done withstanding almost 2 months of Iranian nitrogen production being offline. This, in combination with a lack of Chinese exports and continued European production issues, made an already tight global urea S&D that much tighter. Hopefully, Iran will be the last surprise...but there are no guarantees. The global S&D is racing on the edge of a razor. Any little push to further reduce supplies will have an impact.

- India proceeds with locking up 1.5M and the world reacts - this would be more about market interpretation. If India locks up 1.5M and some other buyers step up, the global traders could view this as the world mopping up excess product. They would view supplies as low and see that as a reason to push prices higher. Honestly, this bull factor is weak. I'm not a believer in it...but I've been wrong before. I've seen situations where the fundamentals point one picture, but the market goes the complete other direction. It is all about interpretation.

- Chinese exports return/rumor to return - China continues to be a huge reason why global urea values are as high as they are. They historically represent 10% of the global export market at 5 to 5.5M tons per year. In 2024, they only exported 266K tons and 2025 has started WELL below that pace. However, you can never count China out. There have been rumors that the government will revisit export programs. This may be a full return with free market fundamentals driving it (not likely). This might be a quantity ceiling. This might be a short timeframe. Each scenario would play out differently but each would likely cause values to dip on their return...if it happens.

- India shocks the world and delays or lowers the tonnage on this tender - with the way India delayed their tender and the fact that their next application season is coming quickly, this is not a very high expectation...but we have been surprised before. IPL, India's importing agency for this tender, announced their desire to secure 1.5M tons. We could see them get upset with high offers and decide to scale back the number of tons they secure. We could see them decide to try the tender again. Any form of this would likely gut the global urea market and send prices lower.

- U.S. tariffs anger the world, causing urea to flow to Australia as a result - there are a lot of countries that were unhappy with Trump's announcement of wide ranging tariffs. The U.S. has seen with phosphate tariffs that even when it makes sense to send product to the U.S. with the tariff in place, they still opt to go elsewhere. If urea producers/countries take the same approach, they will be looking to other markets. Australia is high on that list and could have values softer.

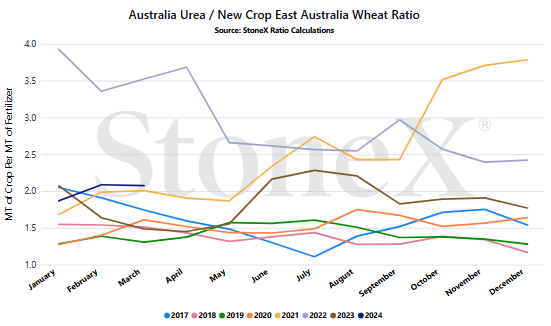

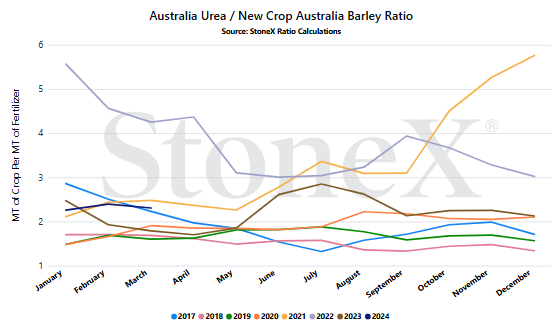

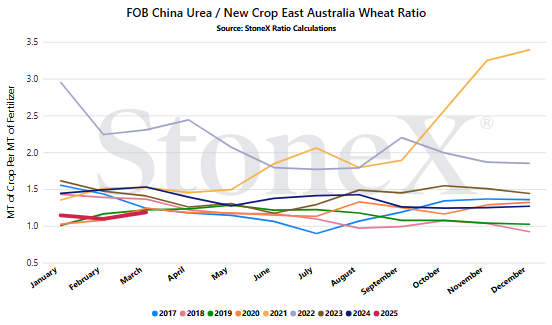

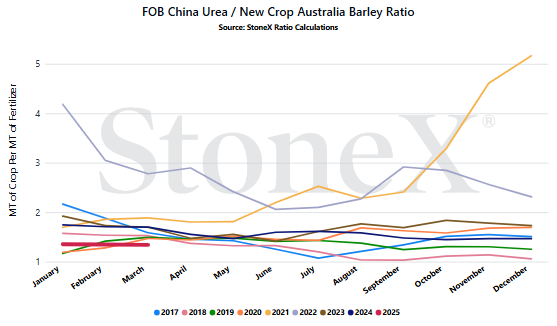

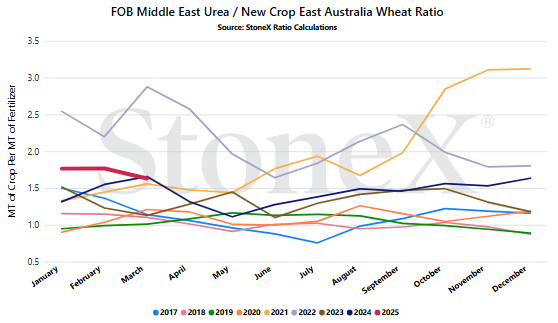

We believe that only looking at the flat price of either grains or fertilizer can be misleading:

-

Only selling grain can hurt you if fertilizer prices rise substantially

-

Only buying fertilizer can hurt you if grain prices fall

We look at the ratio "value" to get a better indication of where we are or how many bushels of X does it take to pay for 1 ton of fertilizer.

Would you rather:

-

Spend 135 bushels to pay for 1 ton of urea

-

Spend 55 bushels to pay for 1 ton of urea

When we compare the current ratio value against recent years, we start to see if we are high or low.

YOUR VALUES MAY LOOK DIFFERENT

This is a work in progress section! We plan on looking at the relationship between Aussie grains and global price points (and hopefully Aussie specific locations, though that data is hard to secure, very protected). Big reason why we are still in the "trial" stage of this newsletter!!!!

- Chinese governments export policies - a large reason why global and domestic prices are as high as they is due to Chinese urea export restrictions. China typically represents around 10% of the global export marketplace and 2024 saw them reduced to just over 260K tons. January/February 2025 export data pace makes 2024 look huge in comparison. More worrisome is that there continues to be rumors that this will become a more permanent strategy where tons, if exported, are done on a defined quantity and a defined period. As long as China isolates itself, global farmers will pay a higher price.

- How do global urea producers react to U.S. tariffs - this could be huge for Aussie urea buyers. If the world shuts down U.S. shipments as a result of the tariffs, they will be looking for alternatives. Australia will be a bright beacon on the horizon for them. We could see Australia get very popular and as a result, we could see prices lower with an armada of ships on the way.

- Whether Russia/Ukraine peace leads to lower European gas values - the new U.S. administration continues to push hard for peace between Russia and Ukraine. There is a lot of hope that if this is successful, it will mean a return to "normal" relations between Europe and Russia. Now, whether it will or will not remains to be seen but peace certainly wouldn't hurt. In the best case scenario, peace is found, relations between Europe and Russia return, work starts to repair the Nordstream pipeline which was attacked during the early days, and eventually cheap Russian gas returns to Europe which will allow European based nitrogen production to return to near normal levels. That sentence was 3+ lines long which should give you an idea of how long this would take to play out. It is not a short term event, rather a longer term hope. If European production can return, global prices can mellow out even further.

- How long can buyers stay out, will it be a windfall when they return - the biggest surprise of 2025 has been how well global buyers have been able to stay out. This story has really been focused on India who was WIDELY expected to announce a purchase tender in mid-February. Since then, global buyers have taken India's approach and drug their feet as well...but for how long? If India steps in, will others take that as a sign of a near term price floor and purchase as well? Can there be enough demand at this point in the calendar to support values? I'm losing faith by the day. I think we are simply too close to summer, but we will see.

StoneX Ratio Calculation

The ratio calculation is derived from Bloomberg historical grains values as well as fertilizer values from StoneX, NPKFAS, and Argus.

The calculation is simply dividing the fertilizer price by each grain price.

All data was sourced from StoneX unless otherwise noted.