Ceasefire in Lebanon reverses Brent gains, but Strait of Hormuz deadlock maintains risk premium

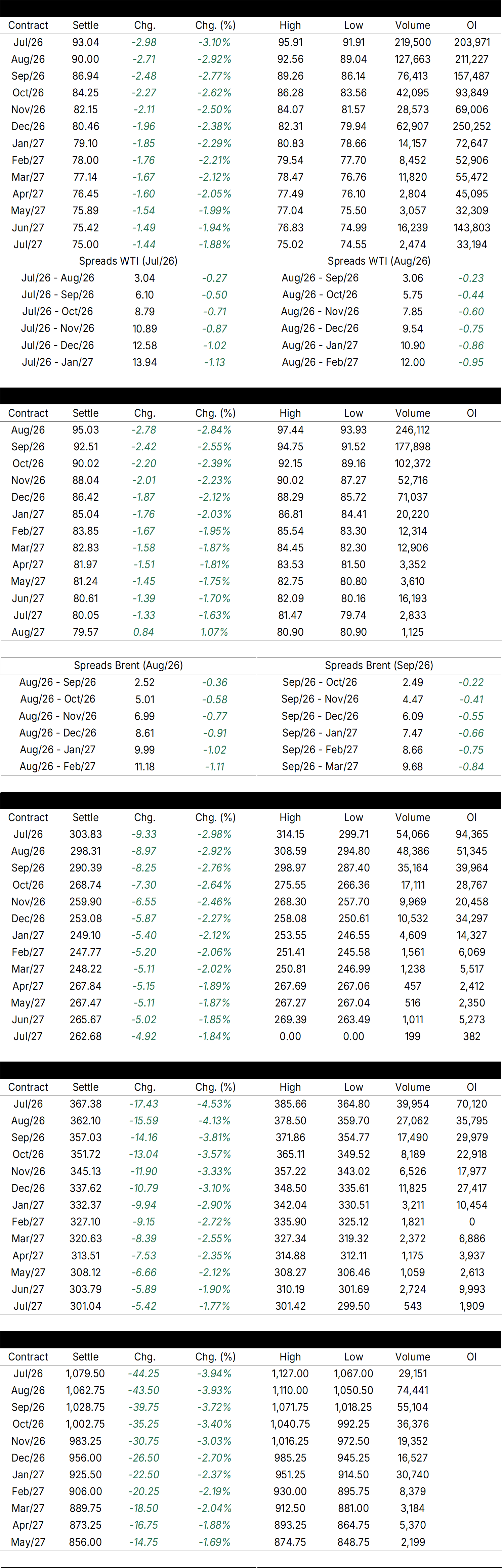

Yesterday (04), the most active Brent contract closed lower, dropping 2.8% to USD 95.03/bbl. WTI followed the movement, falling to USD 93.04/bbl (-3.1%). The session fully reversed the gains accumulated on Wednesday, when both contracts had advanced around 2% in response to the escalation of hostilities in the Gulf — including Iranian attacks on Kuwait airport and U.S. offensives near the Strait of Hormuz.

The trigger for the reversal was the announcement of a ceasefire between Israel and Lebanon, finalized overnight from Wednesday to Thursday, which reignited market participants' expectations of a broader agreement between Washington and Tehran, given that Iran had conditioned any negotiations with the U.S. on the end of Hezbollah-related conflicts in Lebanon.

This morning (05), Brent is trading around USD 95.1/bbl (+0.2%). Optimism regarding a peace negotiation remains fragile and subject to rapid reversals: Hezbollah leader Naim Qassem’s rejection of the ceasefire and the continuation of Israeli military operations in southern Lebanon have reintroduced uncertainty into the diplomatic landscape.

Market participants seem to be in a wait-and-see mode, trying to assess whether the agreement between Beirut and Washington has enough room to progress without the armed group’s adherence — a condition Iran still treats as indispensable.

Hezbollah rejects ceasefire and weakens U.S.-Iran agreement prospects

The U.S.-mediated ceasefire between the Lebanese government and Israel did not involve Hezbollah in the negotiations, and the group’s leader, Naim Qassem, publicly declared that "resistance will continue." Israel, in turn, continues to maintain troops in Lebanese territory since its invasion in March, and Defense Minister ישראל Katz categorically stated that the forces will not withdraw. With the agreement technically in effect but disregarded by two of the most relevant actors on the ground, the diplomatic reading of the market becomes much more uncertain.

Why this matters: Iran explicitly established the end of Hezbollah-related conflicts as a condition for any negotiation with Washington — and the group’s rejection of the ceasefire practically nullifies the symbolic value of the Israel-Lebanon agreement as a catalyst for broader de-escalation.

- In the short term, this reduces the likelihood of reopening the Strait of Hormuz and maintains the geopolitical risk premium embedded in prices, even though the market reacted with excessive optimism on Thursday.

- In the medium term, the continuation of the deadlock puts pressure on Iranian exports — already at their lowest level in six years, according to vessel tracking data — and restricts the flow of heavy crude oil destined for Asian refineries.

- Should Iran interpret the continuation of Israeli attacks in Lebanon as a violation of minimum conditions and resume offensive operations in the Gulf, the risk premium could be abruptly repriced.

What to expect? As long as Hezbollah maintains its stance rejecting the ceasefire and Israel does not reduce its presence in Lebanon, signs of U.S.-Iran diplomatic progress will remain fragile, and Brent is likely to continue fluctuating between USD 90 and USD 100/bbl, without a clear direction.

• If Iran formally signals acceptance of a preliminary agreement with Washington — even partially — oil futures could decline more extensively, given the size of the risk premium still embedded in the curves.

Mina al Fahal terminal attacked, but Oman confirms normal operation

The Mina al Fahal terminal in Oman, responsible for exporting 800,000 to 900,000 barrels per day of oil, was reportedly targeted by a drone attack that caused an explosion near the anchoring buoys. Three sources told Reuters that oil loading was temporarily suspended after the incident — but Petroleum Development Oman subsequently confirmed that operations had returned to normal.

Why this matters: Oman holds a unique strategic position in the current scenario: it is one of the few Gulf countries maintaining open diplomatic channels with Tehran while simultaneously exporting significant volumes of oil via an alternative route to the Strait of Hormuz. A confirmed attack on the Mina al Fahal terminal would represent a significant escalation, signaling that no regional export infrastructure is immune to the conflict — increasing the risk premium beyond already-blocked routes.

What to expect? The declared normalization of operations at Mina al Fahal should limit the immediate impact on prices, with the market absorbing the incident as a logistical issue. Should attacks on Omani terminals recur or be formally attributed to parties linked to the U.S.-Iran conflict, systemic risk perception around regional export infrastructure is likely to increase, with potential repricing in Brent futures contracts.

-

SPECIAL - Diesel imports rise in May

-

According to Comexstat data, diesel imports totaled 1.4 million m³ in May, marking an 18.5% increase compared to March but a slight decline of 3.5% compared to the same period last year.

The growth in purchases of U.S. product surprised, with the U.S. share rising from 9% (108,000 m³) in April to 27% (390,000 m³) in May. The increase is driven both by a rise in U.S. global exports — with the indicator jumping over 30% since the beginning of the Middle East conflict — and the drop in global fuel prices, which made the Brazilian market more attractive to U.S. exporters compared to other regions.

-

Russia remained the main supplier of the product to Brazil, with 73% (1.02 million m³) of the total share. The country managed to maintain volume even in the context of a nearly 20% production decline between March and May — with Ukrainian attacks affecting Russian processing centers. In the coming months, there are doubts about the country's capacity to export volumes seen in previous months, not only due to reduced supply but also due to the expectation of increased agricultural consumption.

In the year-to-date, the indicator totaled 6.4 million m³, marking a 3% decline compared to the same period last year. In addition to greater difficulty in acquiring products in the international market after the closure of the Strait of Hormuz, increased supply from Brazilian refineries also contributed to this scenario of lower diesel internalization, with Petrobras’ processing centers accelerating FUT and ensuring greater domestic supply.

Daily Table - Price variation in the previous session

Source: ICE, NYMEX. Prepared by: StoneX.

The StoneX Group Inc. group of companies provides financial services worldwide through its subsidiaries, including physical commodities, securities, exchange-traded and over-the-counter derivatives, risk management, global payments and foreign exchange products in accordance with applicable law in the jurisdictions where services are provided. References to over-the-counter (“OTC”) products or swaps are made on behalf of StoneX Markets LLC (“SXM”), a member of the National Futures Association (“NFA”) and provisionally registered with the U.S. Commodity Futures Trading Commission (“CFTC”) as a swap dealer. SXM’s products are designed only for individuals or firms who qualify under CFTC rules as an ‘Eligible Contract Participant’ (“ECP”) and who have been accepted as customers of SXM. StoneX Financial Inc. (“SFI”) is a member of FINRA/NFA/SIPC and registered with the MSRB. SFI is registered with the U.S. Securities and Exchange Commission (“SEC”) as a Broker-Dealer and with the CFTC as a Futures Commission Merchant and Commodity Trading Adviser. References to securities trading are made on behalf of the BD Division of SFI and are intended only for an audience of institutional clients as defined by FINRA Rule 4512(c). References to exchange-traded futures and options are made on behalf of the FCM Division of SFI . StoneX is a trading name of StoneX Financial Ltd (“SFL”). SFL is registered in England and Wales, Company No. 5616586. SFL is authorized and regulated by the Financial Conduct Authority [FRN 446717] to provide to professional and eligible customers including: arrangement, execution and, where required, clearing derivative transactions in exchange traded futures and options. SFL is also authorised to engage in the arrangement and execution of transactions in certain OTC products, certain securities trading, precious metals trading and payment services to eligible customers. SFL is authorised & regulated by the Financial Conduct Authority under the Payment Services Regulations 2017 for the provision of payment services. SFL is a category 1 ring-dealing member of the London Metal Exchange. In addition SFL also engages in other physically delivered commodities business and other general business activities which are unregulated and not required to be authorised by the Financial Conduct Authority. StoneX Group Inc. acts as agent for SFL in New York with respect to its payments services business. StoneX APAC Pte. Ltd. acts as agent for SFL in Singapore with respect to its payments services business. ‘StoneX’ is the trade name used by StoneX Group Inc. and all its associated entities and subsidiaries.

Trading swaps and over-the-counter derivatives, exchange-traded derivatives and options and securities involves substantial risk and is not suitable for all investors. Past performance of any futures or option is not indicative of future success. Indicators are not a trading system and are not published as a specific trade recommendation. The information herein is not a recommendation to trade nor investment research or an offer to buy or sell any derivative or security. It does not take into account your particular investment objectives, financial situation or needs and does not create a binding obligation on any of the StoneX group of companies to enter into any transaction with you. You are advised to perform an independent investigation of any transaction to determine whether any transaction is suitable for you. No part of this material may be copied, photocopied or duplicated in any form by any means or redistributed without the prior written consent of StoneX Group Inc.

© 2026 StoneX Group Inc. All Rights Reserved.