USDBRL to reflect tensions in the Middle East and data from the US, Brazil, and the Eurozone

- Bullish

- The interruption of talks between the US and Iran has heightened geopolitical risks and boosted oil prices. However, it has also strengthened Brazilian assets tied to the sector, contributing to a more resilient Brazilian real during some trading sessions.

- Rumors of Christine Lagarde’s resignation, though denied, have raised concerns about potential instability in the Eurozone, keeping the market focused on her statements and the ECB minutes. A stronger euro could weaken the global dollar, benefiting the real.

- Bearish

- The release of the Payroll report may confirm the resilience of the US labor market, reinforcing the perception that the Fed is not in a hurry to cut interest rates. This scenario supports Treasury yields and tends to strengthen the dollar against the real.

- Brazilian data this week could reinforce signs of economic slowdown and more persistent inflation, increasing the likelihood of a deeper Selic rate cut and pressuring the real due to the narrowing interest rate differential.

The week in review

- Last week’s highlight was in the political sphere. Following the US Supreme Court’s overturning of tariff hikes, President Donald Trump imposed new 10% tariffs on all countries, effective Tuesday (24).

- Despite the 10% tariff, the figure was below a second announcement by Trump, which suggested a 15% rate. This discrepancy heightened uncertainties surrounding US trade policy.

- Additionally, rounds of negotiations between the US and Iran remain in focus. What began promisingly on Thursday (26) fell through regarding discussions on Iran’s nuclear program and economic sanctions, raising risk perceptions of armed conflict and driving oil futures higher.

- On the economic front, the most relevant data was the Broad Consumer Price Index 15 (IPCA-15). The indicator showed faster-than-expected price acceleration—despite a drop in the 12-month accumulated rate—reducing the likelihood of a substantial interest rate cut by the Monetary Policy Committee (Copom).

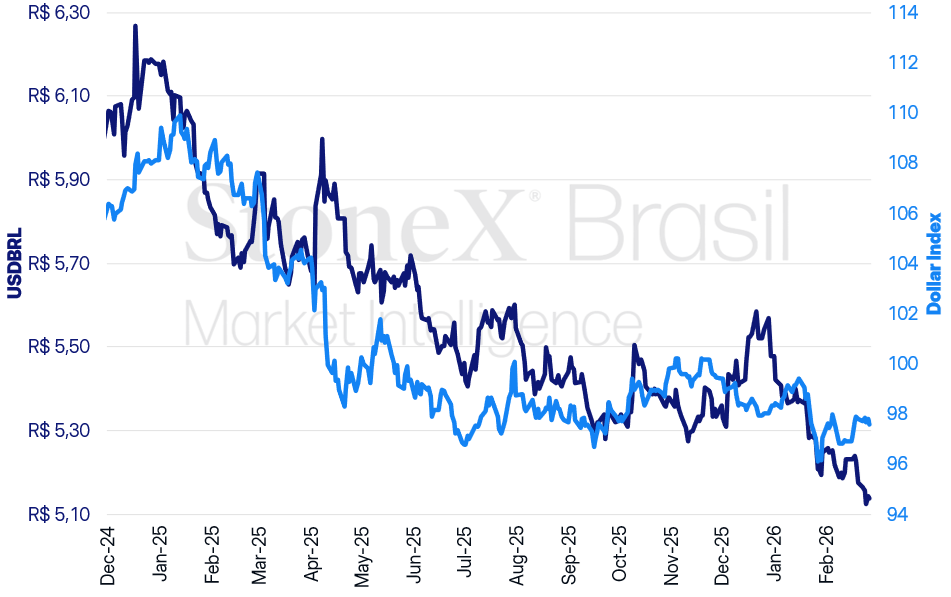

USDBRL and Dollar Index (points)

Source: StoneX cmdtyView. Developed by StoneX.

USDBRL Variations

Daily: -0.60% | Weekly: -0.99% | Monthly: -2.32% | Annual: -6.42% | Over 12 Months: -10.90%

Dollar Index Variations

Daily: -0.16% | Weekly: -0.11% | Monthly: +0.68% | Annual: -0.64% | Over 12 Months: -8.10%

KEY HIGHLIGHT: US Labor Market Data

Expected Impact on USDBRL: Bullish

The main focus for the upcoming week will be the release of the employment situation report (“Payroll”) on Friday (6), which should help investors reassess their views on the US labor market.

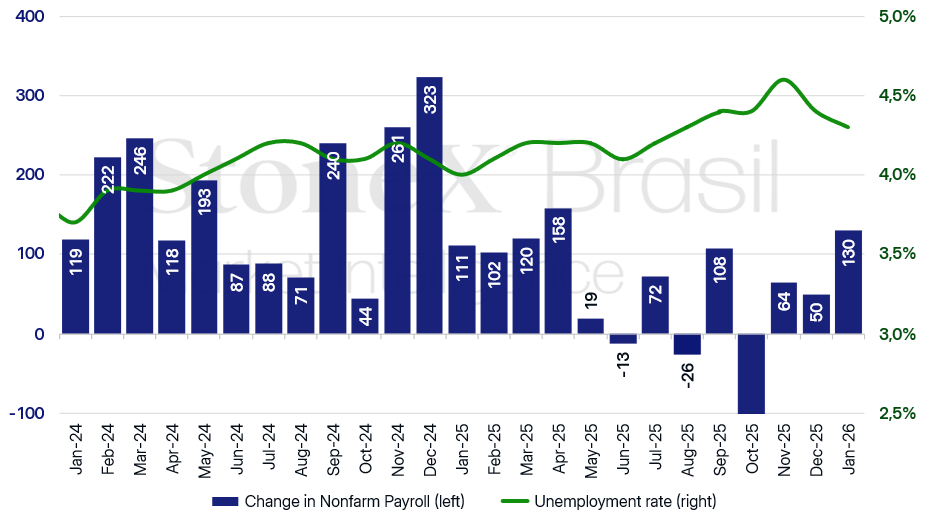

- The latest nonfarm payroll data for January indicated the creation of 130,000 new jobs, compared to estimates of just 70,000.

- This strong result lowered the unemployment rate to 4.3%, despite projections of stabilization at 4.4%.

- This scenario suggests that the US labor market remains resilient, despite high inflation and slowing economic activity.

Why this matters: Economic activity, labor market trends, and inflation continue to play a decisive role in the Federal Reserve’s monetary policy decisions.

- If the Payroll report reinforces perceptions of resilience in the US labor market, expectations for swift rate cuts could diminish, potentially boosting Treasury yields and strengthening the dollar globally.

Overview: While the last Payroll report highlighted resilience in the US labor market, contradictory signals from economic activity and inflation data have muddled investor expectations.

- The preliminary Q4 GDP reading showed 1.4% annualized growth, falling short of the 2.8% annualized forecast, signaling a slowdown in economic activity.

- Conversely, the Personal Consumption Expenditures (PCE) Index—favored by the Federal Open Market Committee (FOMC)—increased slightly from 2.8% to 2.9% year-on-year, exceeding the 2.0% target.

Commitment to Price Stability: In the latest FOMC meeting minutes, the Fed expressed caution regarding further rate cuts.

- A notable point was the possibility of additional rate hikes if inflation stays above the 2% target, reaffirming the Fed’s commitment to price stability.

- Despite cooling economic activity, elevated inflation levels in the past month may deter immediate rate cuts.

Change in Total Urban Employment (thousands) and US Unemployment Rate (%)

Source: U.S. Bureau of Labor Statistics (BLS), Federal Reserve Bank of St. Louis. Developed by StoneX.

Data from Brazil

Expected Impact on USDBRL: Bearish

This week will feature the release of key economic indicators, providing investors with insights on Brazil’s economic activity and labor market.

- The most significant report will be the Q4 GDP reading.

- Additionally, labor market data from PNAD and CAGED will be released.

Why this matters: In its last monetary policy meeting, the Copom signaled an intention to lower the Selic rate on March 18, with the magnitude of the cut dependent on economic indicators.

- Clear signs of slowing economic activity and inflationary deceleration could increase bets for a larger rate cut, potentially weakening domestic assets and the real.

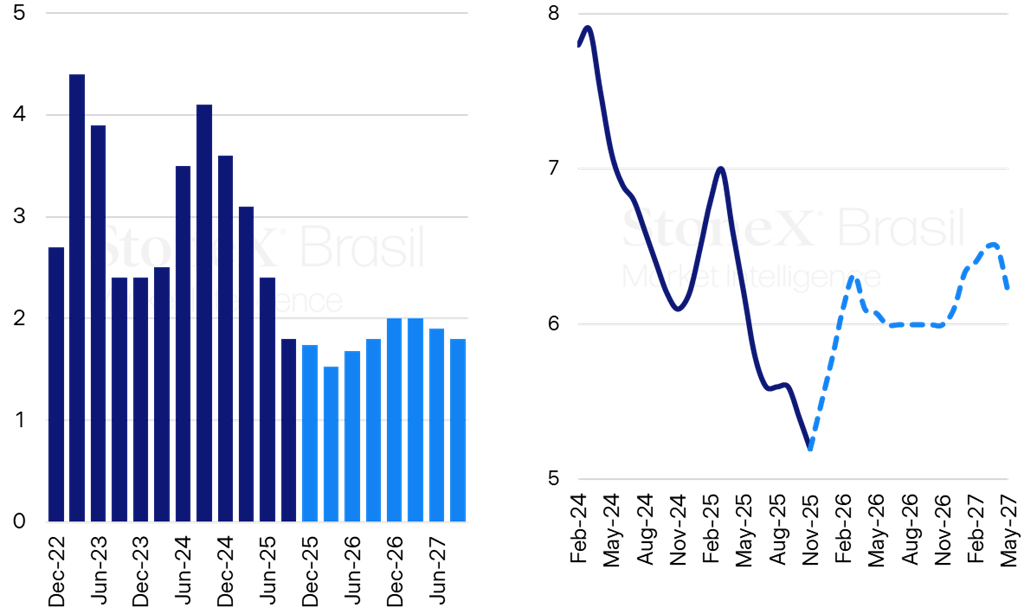

Economic Activity: The latest Q3 GDP reading showed 0.1% growth.

- The Central Bank’s Economic Activity Index (IBC-Br), often seen as a GDP preview, indicated 0.4% growth in Q4 2025, suggesting modest economic expansion at the year-end.

- However, December’s Monthly Service Survey (PMS)—Brazil’s largest economic sector—and the Monthly Trade Survey (PMC) showed a 0.4% decline.

- The upcoming PMI and industrial production figures, alongside GDP data, will provide a clearer view of Brazil’s economic trajectory.

Labor Market: December’s PNAD data recorded a historic low unemployment rate of 5.1%.

- In contrast, December’s CAGED report showed a net loss of 618,180 formal jobs, reflecting seasonal patterns of higher layoffs.

- January’s estimates project a net gain of 90,000 jobs.

- Despite economic slowdown signs, labor market resilience persists.

Inflation as a focal point: The IPCA-15, released Friday (27), serves as a preview for the IPCA. February’s prices rose 0.84%, exceeding expectations of 0.60%.

- While monthly inflation increased, the 12-month accumulated rate dropped from 4.50% to 4.10%, reflecting the exclusion of February 2025’s data.

- Still, the higher-than-expected inflation raised concerns about price stability, casting doubt on larger Selic cuts, such as 0.75-point reductions.

- Copom’s latest communication emphasized “serenity” in monetary policy decisions, signaling caution on larger rate cuts without solid data.

Brazil’s GDP (%) (left) and Unemployment Rate (%) (right)

Source: IBGE. Developed by StoneX.

US-Iran Talks in Geneva Come to a Halt

Expected Impact on USDBRL: Bearish

Negotiations between Washington and Tehran ended without an agreement, with Iranian officials emphasizing the need to separate “nuclear and non-nuclear issues.”

Why this matters: The lack of a formal agreement heightened expectations for military conflict in the Persian Gulf and potential logistical disruptions in the Strait of Hormuz, impacting roughly one-quarter of global oil supply.

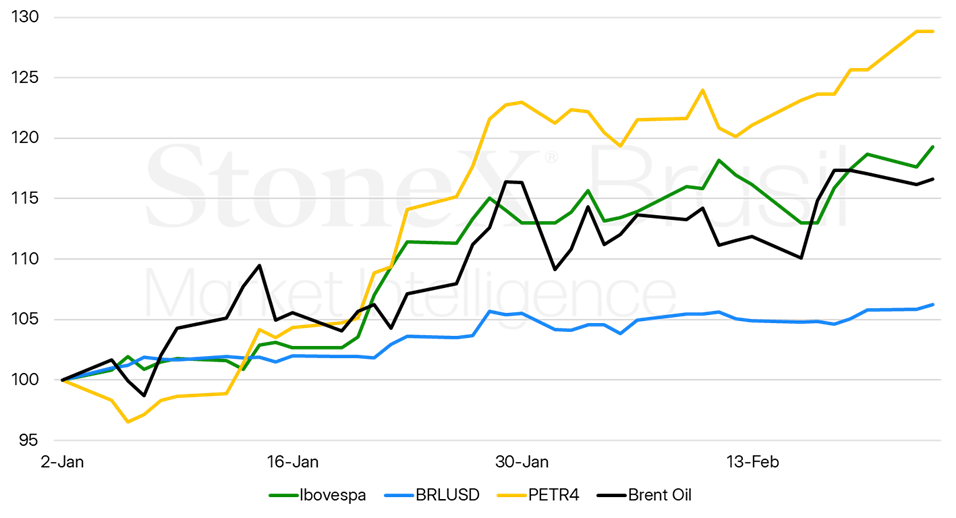

- This situation reversed much of yesterday’s oil losses and renewed commodity gains today, surpassing USD 72/bbl again.

- Geopolitical tensions tend to increase investor risk aversion, negatively impacting risky assets and emerging market currencies like the real.

- On the flip side, recent oil price hikes have benefited national oil-sector stocks, supporting the real during some sessions.

Overview: During the talks, rumors suggested reduced US flexibility on certain Iranian demands, such as forming a regional uranium enrichment consortium and stricter monitoring of Iranian activities.

- Washington continued to push for the total suspension of Iran’s nuclear program, stalling negotiation progress.

- On February 19, President Trump warned that “bad things” would happen if no nuclear deal was finalized within 10–15 days, escalating fears of military conflict in the Gulf.

- Meanwhile, the Persian Gulf has seen increased oil exports, especially from Saudi Arabia, signaling potential contingency measures amid conflict fears.

- Iran tripled oil exports between February 15–20, reaching 3 mbpd, suggesting a rush to maximize foreign sales amidst heightened uncertainty in US-Iran relations.

What to expect: In the coming weeks, the market will closely monitor US-Iran negotiations. A possible US attack on Iranian territory could introduce greater volatility in oil prices depending on the scale of the offensive.

- A smaller, localized attack might reduce risk premiums, as investors could interpret it as a signal that broader conflict is unlikely in the short term.

- Conversely, attention will turn to Iran’s potential response, with temporary disruptions in Hormuz flows potentially triggering significant price hikes.

Selected Asset Variations in 2026 (Base 100)

Source: StoneX cmdtyView. Design: StoneX.

ECB Minutes and Lagarde’s Statements

Expected Impact on USDBRL: Bearish

Next week, Christine Lagarde, President of the European Central Bank (ECB), is scheduled to make two key statements alongside the release of the minutes from the February monetary policy meeting, which maintained key interest rates at 2% for the fifth consecutive session.

- Lagarde’s remarks and the ECB minutes are expected to reaffirm the commitment to monetary policy aiming for inflation near 2% annually.

- Recent inflation data in the Eurozone has shown signs of deceleration, such as a February 27 report indicating median inflation expectations fell from 2.8% to 2.6% annually.

Why this matters: Lower inflation in the Eurozone could favor more expansionary ECB policies in the future, increasing global liquidity. This could drive capital flows to emerging markets, potentially weakening the USDBRL, although it might also strengthen the DXY.

Rumors of Lagarde’s premature resignation: Lagarde’s statements follow market concerns sparked by a Financial Times report last week suggesting her potential early resignation. Lagarde later dismissed this, affirming she would complete her term through October 2027.

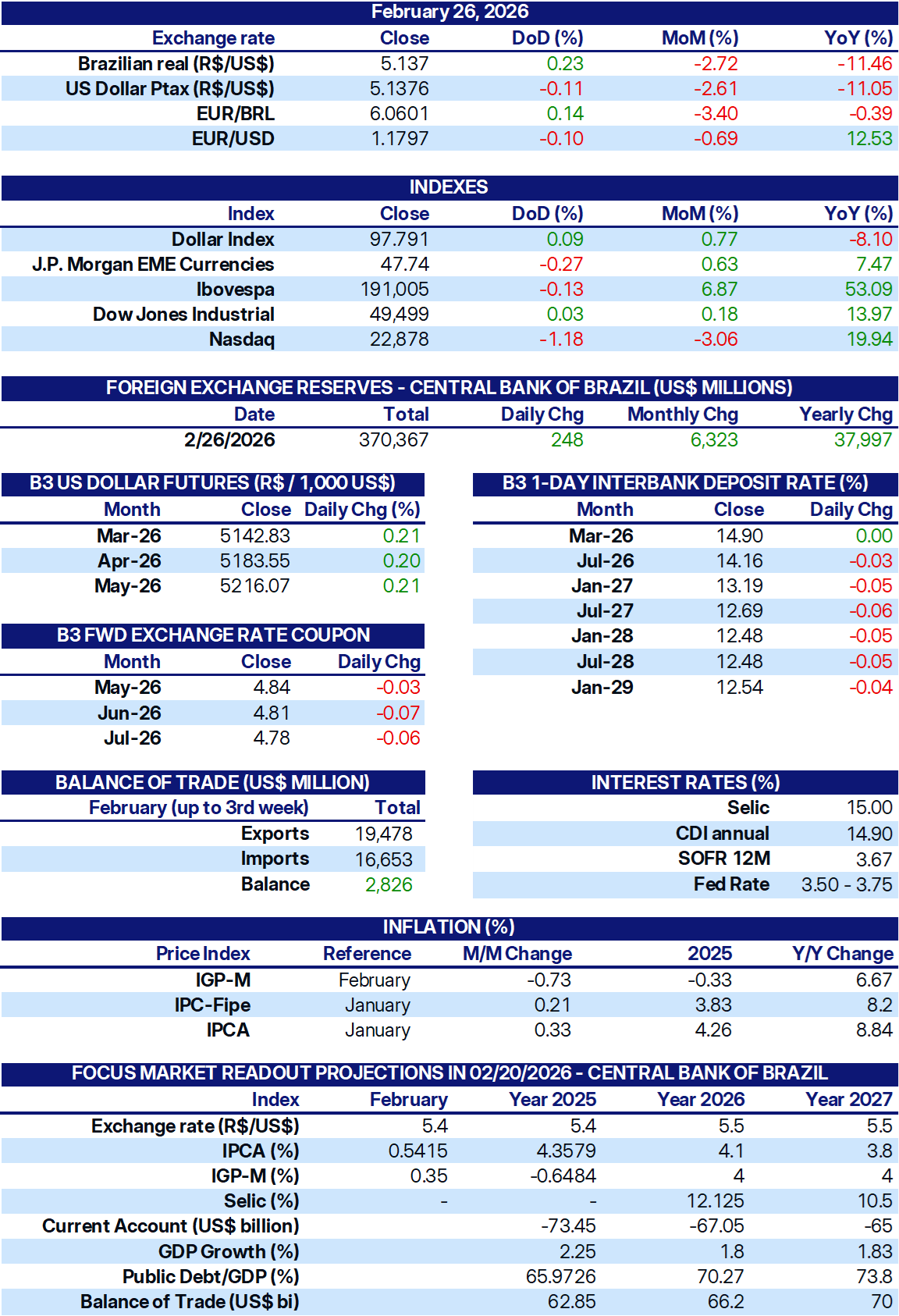

INDICATORS

Sources: Central Bank of Brazil; B3; IBGE; Fipe; FGV; MDIC; IPEA; and StoneX cmdtyView.