USDBRL to reflect Middle East conflict and economic data from the US and Brazil

-

Notice: Starting Sunday (08), daylight saving time begins in the US, reducing the time difference between Washington D.C. (EST) and Brazil from two hours to one hour. As a result, US economic indicators will be published earlier in Brazil's local time.

- Bullish

- Military escalation in the Middle East leads to global risk aversion, which tends to negatively impact riskier assets like emerging market currencies.

- Expectations of milder inflation data may reinforce the outlook for faster interest rate cuts in Brazil, which could weigh on the Brazilian real.

- Bearish

- Potentially weaker US economic activity and inflation data could negatively impact the dollar globally.

The week in review

- The week’s key event was the outbreak of armed conflict in the Middle East following US and Israeli attacks on Iran on Saturday (28). US and Israeli leaders stated the conflict could last several weeks, but there have been no signs of diplomatic progress thus far.

- Due to the conflict, oil and LNG production in the region has been reduced, and shipments through the Strait of Hormuz are nearly halted, driving up energy commodity prices and raising concerns about global inflationary pressures.

- The US “Payroll” report, the country’s main labor market indicator, fell significantly short of expectations, showing a negative balance of 92,000 new jobs while the unemployment rate rose to 4.3%.

- In Brazil, quarterly GDP data showed a 1.8% increase in the fourth quarter, while the unemployment rate rose to 5.4% in January, both in line with estimates, signaling a slowdown in economic activity and the labor market.

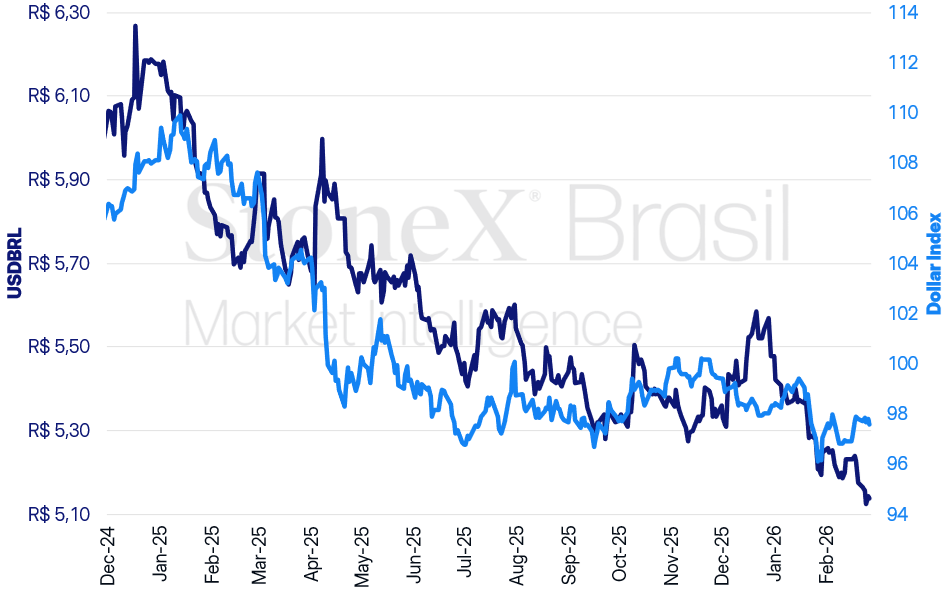

USDBRL and Dollar Index (points)

Source: StoneX cmdtyView. Prepared by: StoneX.

USDBRL dollar variations

Daily: -0.81% | Weekly: +2.18% | Monthly: +2.18% | Annual: -4.16% | 12-month: -8.87%

Dollar Index variations

Daily: -0.32% | Weekly: +1.45% | Monthly: +1.45% | Annual: +0.69% | 12-month: -4.82%

KEY EVENT: Middle East conflict reignites inflationary fears

Expected impact on USDBRL: Bullish

The military escalation in the Middle East, which began on Saturday (28) following US and Israeli attacks on Iran, affected financial and commodity markets throughout the week.

- Key developments so far include the death of Iran’s Supreme Leader Ali Khamenei and the near-total shutdown of the Strait of Hormuz, a route that handles about one-fifth of global oil trade by sea and 20% of global LNG trade.

- Iran has retaliated against Middle Eastern countries hosting US military bases, such as the UAE, Qatar, Bahrain, Kuwait, Jordan, and Iraq, spreading the conflict across the region.

- For further insights on the energy sector’s impacts, read our special report.

Conflict duration: During the initial days of the conflict, US President Donald Trump said he expected the conflict to last 4-5 weeks, although he assured the country has the military capacity to sustain operations for a longer period.

- Israeli Prime Minister Benjamin Netanyahu stated he does not expect the war to last for years, reinforcing signals that countries anticipate a brief conflict.

- However, Trump emphasized that the only acceptable agreement is Iran’s “unconditional surrender” and the selection of an “acceptable leader,” countering reports that Mojtaba Khamenei, son of the Supreme Leader Ali Khamenei, is a contender for the role.

- Despite initial statements aiming for a short conflict, there are no signs yet of any imminent agreement.

Conflict reignites inflationary fears: Currently, key economic concerns center around the risk of global inflation re-acceleration driven by rising energy prices.

- This trend would emerge at a time when inflation has been slowing in major economies, allowing for a relatively lower interest rate environment globally.

- In this context, Neel Kashkari, President of the Minneapolis Federal Reserve, stated on Tuesday that the Iran conflict has significantly increased uncertainty regarding the US economic outlook, making it harder to anticipate monetary policy directions.

- Kashkari noted that just days ago, there was “strong confidence” that slowing inflation would pave the way for a single interest rate cut. Now, however, it’s necessary to evaluate “how this new shock unfolds, its duration, and its magnitude.”

- In Brazil, while the Central Bank has not officially commented on the conflict's potential impacts, Finance Minister Fernando Haddad stated on Tuesday (3) that it’s premature to discuss reversing the Selic rate cut cycle due to Middle Eastern tensions.

- In his words: “At this moment, and everything depends on timing, I don’t see reasons to reverse what’s more or less established—that is, a rate-cutting cycle. We still don’t know how this conflict will develop.”

US GDP, inflation data, and JOLTS

Expected impact on USDBRL: Bearish

Next week’s agenda highlights the release of key US economic indicators, which should help investors fine-tune their expectations regarding the country's monetary policy direction.

- Focus will be on inflation data, the second reading of Q4 2025 US GDP, and new labor market figures.

Why this matters: Changes in economic activity, labor market conditions, and inflation remain decisive factors influencing Federal Reserve monetary policy decisions.

- If the indicators point to economic deceleration and slowing inflation, expectations for faster interest rate cuts in the US are likely to rise, potentially reducing Treasury yields and weakening the dollar globally.

Inflation data: Key releases include the Consumer Price Index (CPI) on Wednesday (11) and the Personal Consumption Expenditures Price Index (PCE) on Friday (13), which will help investors adjust their outlook, especially given the persistent inflation backdrop.

- The headline CPI dropped to 2.4% YoY in January, while the core indicator slowed to 2.5%, both expected to remain stable in February.

- More critically, the PCE is considered the Federal Reserve’s preferred metric. Unlike the CPI, the PCE stayed close to 3.0% in the last release.

- After rising to 2.9% in December, the headline PCE is estimated at 2.8% for January. Median forecasts for the core PCE suggest stability at 3.0%.

- Despite the PCE’s lag compared to the CPI, any upside surprise amid elevated inflation risks could decrease bets on rate cuts, supporting short-term dollar strength.

- Investors will also monitor other PCE report components, particularly personal income and consumption data.

Fourth-quarter GDP: On Friday, investors will also focus on the second reading of Q4 2025 US GDP.

- Current estimates suggest maintaining the annualized growth rate at 1.4% from the previous reading.

- Forecasts for the first reading anticipated slower economic activity with a 2.8% annualized growth rate. However, the actual figure pointed to just 1.4% growth, disappointing investors.

- If the figure holds steady in the second reading, signals of US economic deceleration will likely be reinforced.

Labor market: Investors will also track the US Job Openings and Labor Turnover Survey (JOLTS) for January, considered the second most important labor market release.

- The latest report for December indicated a drop to 6.5 million open job positions, the lowest level since 2020.

- The ratio of job openings to unemployed individuals reached 0.87, marking the second consecutive month with fewer job openings than unemployed people.

Focus on interest rates: In the minutes from the latest Federal Open Market Committee (FOMC) meeting, the Fed signaled a cautious stance on further rate cuts, even mentioning the possibility of additional hikes if inflation remains above the 2% target.

- Next week’s indicators, especially the PCE, will be crucial for refining expectations around monetary policy direction.

- Additionally, tensions in the Middle East driving up oil prices are another area of concern.

Inflation and activity data in Brazil

Expected impact on USDBRL: Bullish

Brazil’s agenda for the week includes key economic indicators that could help investors refine their expectations for the magnitude of the interest rate cut at the next Copom meeting on March 18.

- The highlight is the Broad Consumer Price Index (IPCA) for February, set for release on Thursday (12).

- Additionally, monthly surveys on the services (PMS) and commerce (PMC) sectors will be published, shedding light on economic activity.

Why this matters: At its last monetary policy meeting, the Copom signaled plans to reduce the Selic rate in March, with the size of the cut depending on economic indicators.

- Clearer signs of slowing inflation could increase bets for a larger cut, which may weaken domestic asset yields and the Brazilian real.

IPCA: According to the latest Central Bank Focus Report, median expectations indicate a 0.47% increase in February’s headline index, above the 1.31% increase seen last February, which should reduce accumulated variation.

- However, the most recent inflation data, the Broad Consumer Price Index 15 (IPCA-15), surprised with a 0.84% rise versus expectations of 0.60%, raising concerns about price stability.

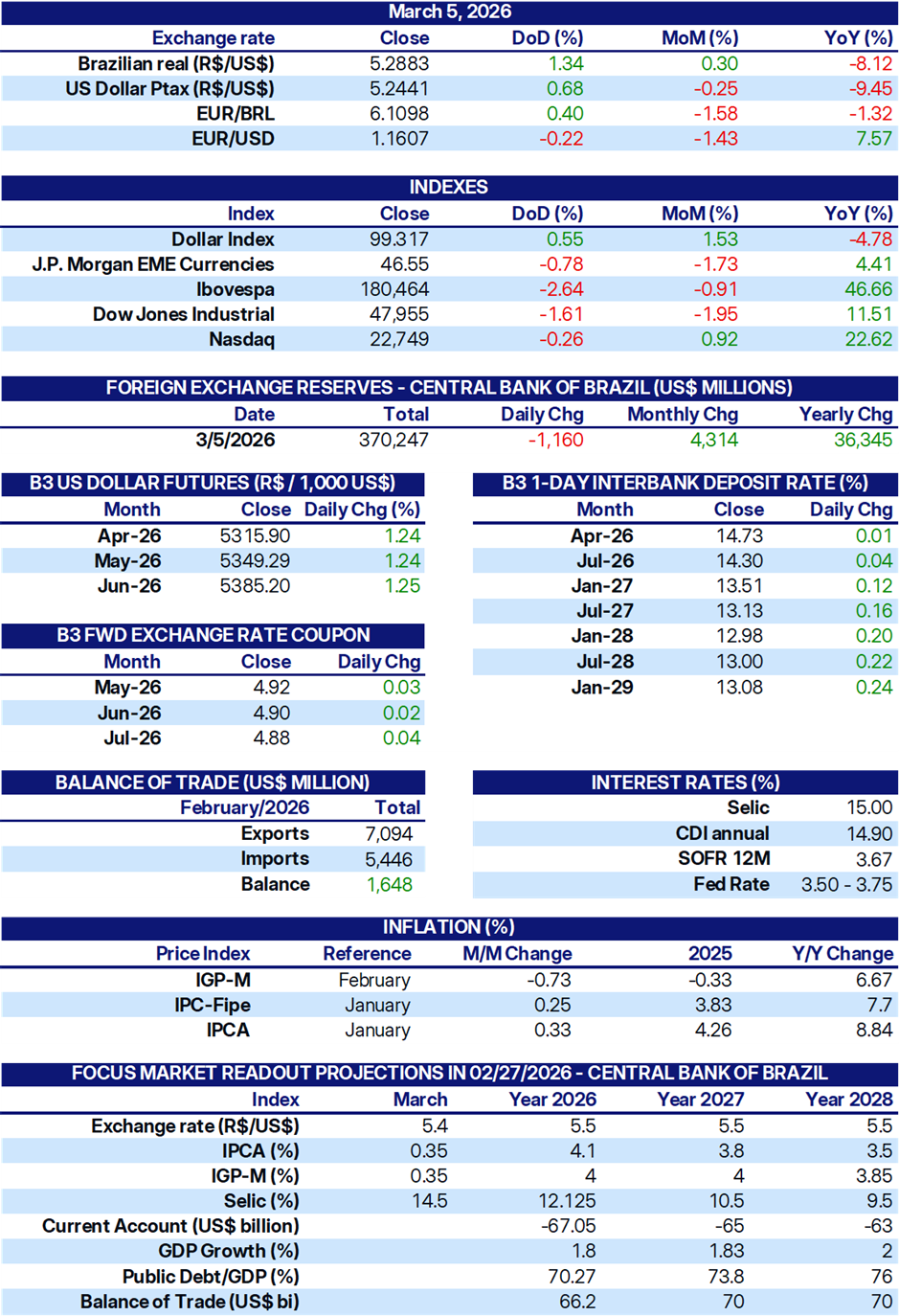

INDICATORS

Sources: Central Bank of Brazil; B3; IBGE; Fipe; FGV; MDIC; IPEA; and StoneX cmdtyView.