USDBRL Likely to Reflect Middle Eastern Conflict and Interest Rate Decisions in the US, Brazil, and Eurozone

- Bullish

- The ongoing conflict involving the US, Israel, and Iran has kept the Strait of Hormuz nearly closed, heightening global inflation risks and increasing risk aversion, which tends to weigh on risky assets and emerging market currencies such as the Brazilian real.

- Brazil’s Central Bank is expected to begin its interest rate cut cycle on “Super Wednesday,” reducing the relative attractiveness of domestic assets and potentially weakening the real.

- The Federal Reserve’s likely decision to maintain interest rates could favor the US dollar globally.

- Bearish

- The European Central Bank’s monetary policy decision, accompanied by signals of commitment to price stability and potential euro appreciation, may contribute to a weaker global dollar and indirectly support the real.

The week in review

- The Middle Eastern conflict remains the primary driver of movements in financial markets. Despite US President Donald Trump’s statement that the conflict is “close to resolution,” ongoing attacks and comments from the Iranian government suggest the regime’s willingness to prolong the conflict and the blockade of the Strait of Hormuz, creating uncertainty for investors.

- In an effort to ensure supply and curb rising oil prices, the International Energy Agency (IEA) announced the release of emergency reserves, while the US government granted a 30-day exemption allowing the purchase of Russian oil derivatives currently in transit. However, these measures were insufficient to bring oil prices below $100 per barrel.

- Amid global geopolitical uncertainty, key economic indicators from the US and Brazil were released, helping investors adjust their expectations for “Super Wednesday” (18).

- In Brazil, despite the Broad Consumer Price Index (IPCA) surpassing expectations, the 12-month accumulated rate nearing the central bank’s target is likely to reinforce expectations for faster interest rate cuts by the institution.

- In the US, the scenario was mixed. While inflation remained resilient at elevated levels, Gross Domestic Product (GDP) figures once again fell below expectations, generating conflicting signals.

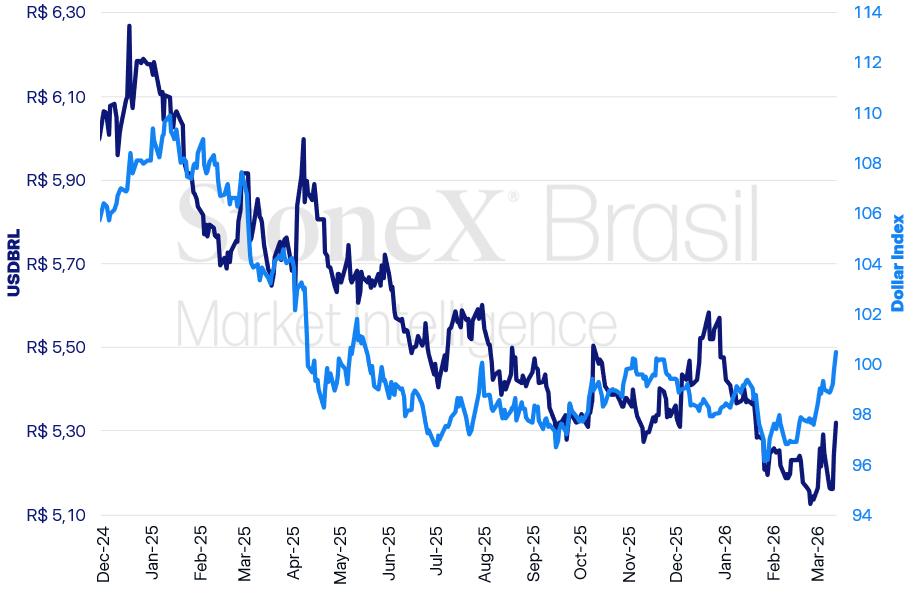

USDBRL and Dollar Index (points)

Source: StoneX cmdtyView. Design: StoneX.

USDBRL Variations

Daily: +1.47% | Weekly: +1.37% | Monthly: +3.58% | Annual: -2.84% | 12 Months: -8.23%

Dollar Index Variations

Daily: +0.74% | Weekly: +1.48% | Monthly: +2.95% | Annual: +2.18% | 12 Months: -3.26%

KEY EVENT: Middle Eastern Conflict

Expected Impact on USDBRL: Bullish

The ongoing conflict between the US, Israel, and Iran enters its third week, with the Strait of Hormuz effectively closed during this entire period, increasing uncertainty and fears of global inflation among investors.

Why This Matters: The global environment remains marked by heightened uncertainty, reflected in pronounced volatility in financial markets. Oil futures prices continue to serve as a key gauge of investor sentiment, reacting to each new development in the conflict.

- Concerns about restricted passage through the Strait of Hormuz, resulting in higher oil prices and widespread inflationary risks, could heighten risk aversion sentiment, which tends to negatively impact higher-risk assets and emerging market currencies such as the real.

- On the other hand, Brazil’s geographical and political distance from the conflict, coupled with strong performance in the domestic energy sector, positions the country as a relatively more predictable alternative compared to more traditional economies.

Conflict Duration: Currently, news suggests a mixed scenario, contributing to investor uncertainty.

- While US President Donald Trump signaled earlier in the week that the conflict was “close to resolution,” the Iranian government continues conducting attacks in the region, indicating the country’s willingness to prolong the conflict and blockade.

Oil Price Surge: On Friday (13), investors reacted to news that the US had granted a 30-day exemption allowing countries to purchase Russian oil derivatives currently in transit, despite sanctions imposed at the start of the Ukraine War.

- Although unexpected and responsible for a brief price adjustment on Friday morning, the exemption has shown limited short-term effectiveness, with Brent crude still trading above $100 per barrel.

- Analysts suggest that such emergency initiatives to alleviate supply disruptions may send a negative signal to the market, indicating that authorities see minimal chances of a swift de-escalation of the conflict.

- This measure followed the release of emergency oil reserves coordinated by the International Energy Agency (IEA) earlier in the week, which also had limited impact due to the perception that the action would not sufficiently offset the supply shock.

- Thus, recent efforts seem insufficient to mitigate the supply shock beyond the short term, likely supporting oil prices at current levels and raising inflationary concerns.

Inflationary Impacts: Amid rising oil prices, the risk of prolonged inflationary shocks remains the primary concern for investors and monetary authorities.

- Brazil’s Secretary of Economic Policy, Guilherme Mello, stated that oil surplus countries, like Brazil, may find more ways to mitigate impacts, such as by increasing trade surplus, even though they remain subject to inflationary pressures.

- The greater concern, however, lies with oil deficit countries, such as Japan and European nations.

- In this context, alongside Brazil and the US, monetary authorities from other major global economies will hold their interest rate decision meetings on Thursday (19): the European Central Bank (ECB), Bank of England (BoE), and Bank of Japan (BoJ).

Interest Rate Decision in Brazil

Expected Impact on USDBRL: Bullish

In Brazil, investor focus will turn to “Super Wednesday” (18), when both the Central Bank of Brazil and the Federal Reserve will hold their monetary policy meetings on the same day.

- The meeting gains further significance as the Copom had signaled its intention to cut the benchmark interest rate (Selic) in its last meeting, with the magnitude of the cut dependent on economic indicators.

Why This Matters: A reduction in the benchmark interest rate lowers the attractiveness of domestic assets, which tends to weaken the real globally.

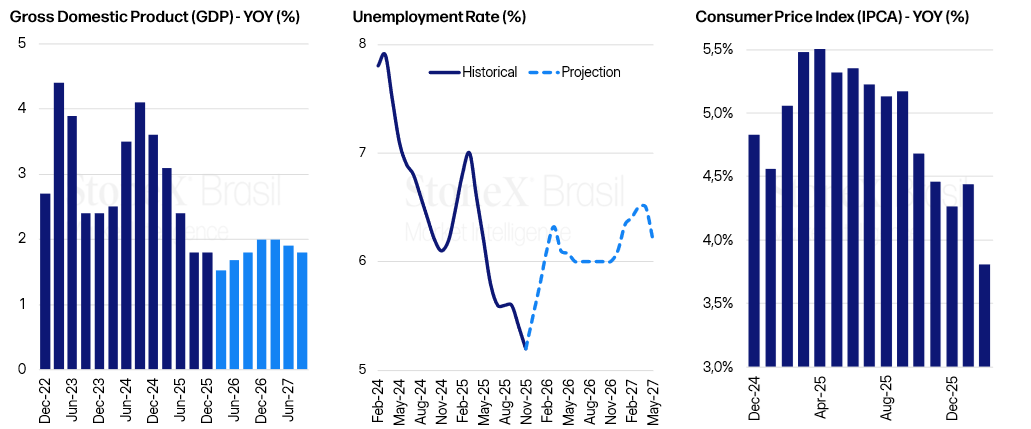

Inflation: The latest release of the Broad Consumer Price Index (IPCA) slightly exceeded expectations, surprising investors.

- The headline index accelerated and showed 0.7% inflation in February, above the expectation of 0.65%. It’s worth noting that as it pertains to February, the indicator did not account for impacts from the Middle Eastern conflict.

- Despite the monthly increase, the 12-month accumulated rate showed deceleration, dropping from 4.41% to 3.81%, closer to the 3.0% target.

- The indicator’s core, which excludes volatile components such as food and energy, accelerated from 0.41% to 0.91%, while inflation in services—more demand-sensitive—rose from 0.18% to 1.46%.

- Given this, despite inflation nearing the target, increases in the core and services—key components of Brazil’s economy—along with the Middle Eastern conflict, raise concerns about the disinflation process.

Economic Activity: GDP data for Q4 2025 aligned with expectations but indicated a slowdown in economic activity during the second half of the year.

- The reading showed quarterly growth of 0.1%, while the previous quarter’s figure was revised to 0.0%. For 2025, Brazil’s economy expanded by 2.3%, primarily driven by performance in the first half of the year.

- Despite signs of economic deceleration in late 2025, Monthly Service and Trade Surveys indicated recovery of 0.3% and 0.4% in January, respectively.

Labor Market: The latest data showed Brazil’s unemployment rate rising to 5.4%, in line with expectations.

- In December, the rate hit 5.1%, the lowest level in the historical series starting in 2012.

Interest Rate Outlook: In late February, the majority of bets were on a 0.5 percentage point cut. However, the Middle Eastern conflict and the surprise IPCA data have led to more dispersed expectations.

- Last week, Central Bank Monetary Policy Director Nilton David stated that the expected Selic “calibration” this month should not be interpreted as the beginning of a monetary policy easing cycle.

- This statement helped reduce bets on a prolonged or intense cycle of cuts and slightly diminished expectations of a 0.50 percentage point move at the next meeting.

- As of Wednesday (11), most bets leaned toward a 0.25 percentage point cut (51%).

Brazil Economic Indicator Overview

Source: IBGE

US Interest Rate Decision

Expected Impact on USDBRL: Bullish

In the US, unlike Brazil, the expectation is for the benchmark interest rate to remain unchanged. Investors’ focus will be on statements from Federal Open Market Committee (FOMC) authorities, particularly regarding the impacts of the Middle Eastern conflict and future monetary policy direction.

Why This Matters: The expectation of prolonged maintenance of the benchmark interest rate could increase the attractiveness of domestic assets, strengthening the dollar globally.

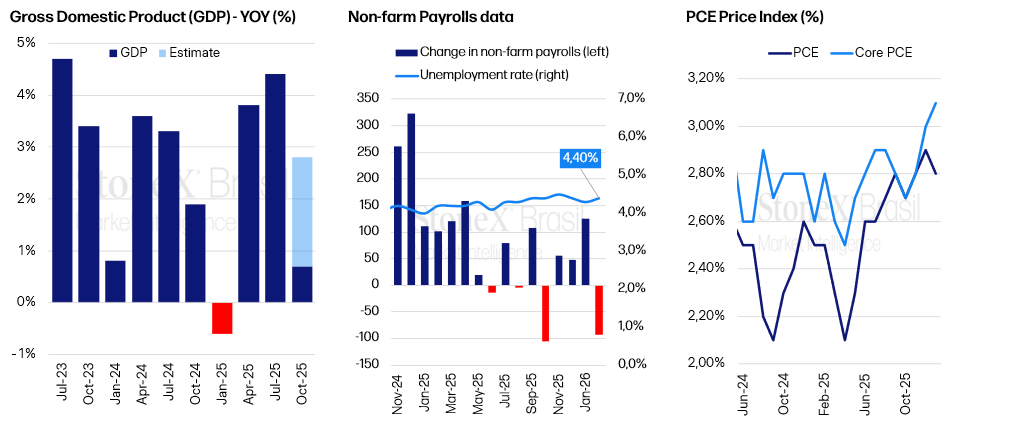

Inflation Concerns: This week, the Personal Consumption Expenditures (PCE) Price Index—the inflation indicator most closely watched by the Federal Reserve—showed signs of deceleration. However, its core component remains concerning.

- The headline index slowed, rising 0.3% in January compared to 0.4% in December, meeting expectations. Over the past 12 months, the index exceeded forecasts by decelerating to 2.8%.

- Conversely, the core index, excluding volatile components, indicated renewed acceleration, fueling fears of inflationary resurgence.

- It’s important to note that as it pertains to January, the index does not account for impacts from the Middle Eastern conflict.

- In the FOMC minutes from its last meeting, the monetary authority signaled a cautious stance regarding further rate cuts, even mentioning the possibility of future increases if inflation moves further away from the 2% target.

Economic Activity and Labor Market Indicators: While inflation remains resilient, typical of a heated economy, other indicators suggest the opposite.

- The second reading of Q4 GDP showed annualized growth of 0.7%, below forecasts of 1.4%. Additionally, the first reading had been expected at 2.8% but came in at 1.4%.

- In Q3, the economy grew 4.4% on an annualized basis, highlighting a slowdown in late 2025.

- In the labor market, negative surprises persisted. Unemployment rose to 4.4%, contrary to expectations of stability at 4.3%, while payroll data indicated a net loss of 92,000 jobs compared to expectations of a 58,000 gain.

Interest Rate Outlook: Recent indicators present a mixed picture of the US economy. While inflation remains elevated, economic activity and labor market data show signs of weakness.

- This creates a dilemma for investors and monetary authorities regarding controlling prices versus maintaining economic activity and employment.

- Alongside the Middle Eastern conflict and potential inflationary impacts, fears of stagflation—a stagnant economy coupled with high inflation—are growing, likely increasing caution among monetary authorities.

- As such, expectations for continued monetary tightening could gain traction, with the Fed likely adopting a “wait-and-see” approach.

US Economic Indicator Overview

Sources: BLS and FRED. Design: StoneX.

BCE Interest Rate Decision

Expected Impact on USDBRL: Bullish

Next week, markets will also monitor the European Central Bank’s (ECB) interest rate decision.

- Market bets point to maintaining rates at the 2% level.

- With Germany’s annual inflation, released this week, at 1.9%—below the 2% target—expectations of a precisely neutral stance have been reinforced.

Why This Matters: Maintaining interest rates in the European Union tends to favor euro appreciation against the dollar. This movement could indirectly benefit the real, as a stronger euro is often associated with a weaker global dollar.

Committee Member Projections: Alongside the interest rate decision, the ECB will release official forecasts from committee members. Markets will closely watch these updates amid growing fears of an inflationary escalation due to rising energy costs following last week’s Strait of Hormuz closure.

- Last Wednesday (11), ECB President Christine Lagarde stated that European monetary policy would do whatever is necessary to ensure the Middle Eastern conflict does not lead to an inflationary shock similar to the one observed after Russia’s invasion of Ukraine in 2022.

- The Eurozone, as a net importer of oil and natural gas, is likely to feel the inflationary impacts of the war more acutely.

- Nonetheless, Lagarde’s comments underscore monetary policy’s role in combating inflation and suggest a more hawkish stance from the ECB should prices accelerate in the economy.

Analysis: In a scenario where purchasing power increasingly dominates global public discourse, a renewed inflation spike could heighten popular dissatisfaction with incumbent governments.

- In Europe, this risk intensifies given the electoral calendar: Germany faces a series of regional elections between March and September, while France approaches a presidential decision early next year.

- In this context, the rise of candidates with more extreme profiles increases uncertainty about the selection of Christine Lagarde’s successor as ECB president.

- Thus, a firm stance by the bloc in combating inflation could have a politically stabilizing effect, reducing the appeal of more radical proposals and favoring the continuation of a market-aligned leadership at the central bank next year.

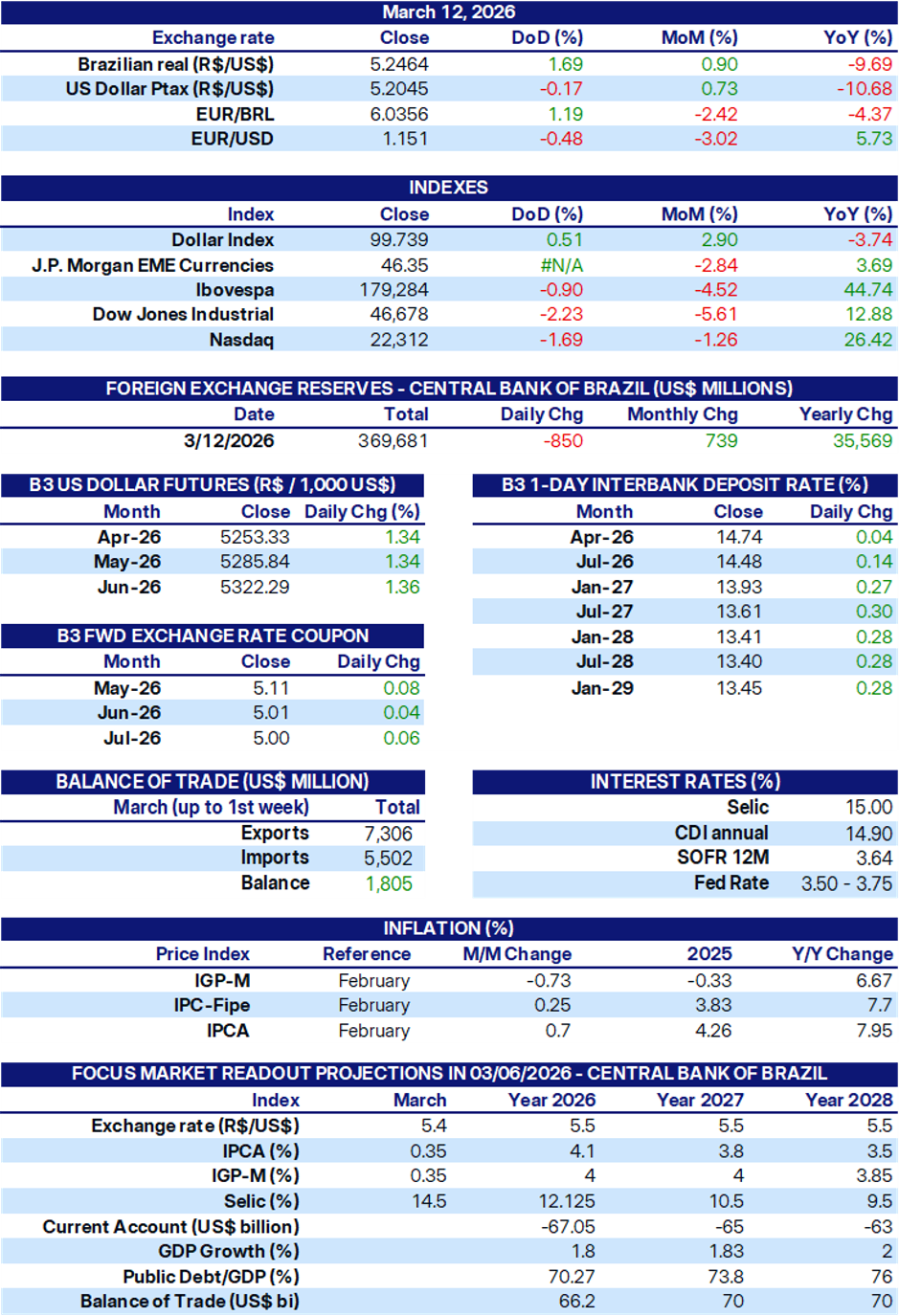

INDICATORS

Sources: Central Bank of Brazil; B3; IBGE; Fipe; FGV; MDIC; IPEA; and StoneX cmdtyView.