USDBRL Likely to React to U.S. Payroll Amid Middle East Conflict Uncertainty

-

Notice: The Economic Indicators Agenda is now available as an interactive report.

-

In this new format, you can dynamically track both past release dates and scheduled announcements through the end of the year.

-

To access it, click here.

- Bullish

- The ongoing Middle East conflict, with sustained risks of disruptions in the Strait of Hormuz and upward pressure on energy prices, is keeping global risk aversion elevated. This scenario bolsters demand for safety and liquidity, strengthening the U.S. dollar while pressuring the Brazilian real.

- Bearish

- The release of the "payroll" and JOLTS reports may confirm a weakening U.S. labor market, increasing expectations for faster rate cuts by the Federal Reserve.

- PMI data from the U.S. might signal a slowdown in activity, particularly in services, reinforcing the outlook for economic deceleration and contributing to lower Treasury yields.

The week in review

- Developments in the Middle East conflict continue to be the primary driver of financial market volatility. On Thursday (26), U.S. President Donald Trump extended the deadline for Iran to accept American conditions—originally set to expire today (27)—to avoid strikes on the country's energy infrastructure.

- Despite the extended deadline, conflicting signals have sparked concern among investors, who remain pessimistic about a ceasefire agreement in the coming days.

- Brazil's Central Bank, in its Monetary Policy Report (MPR), maintained its 2026 economic growth projection at 1.6%, while raising its inflation forecasts for the year. Inflation is expected to move further away from the target center but remain within tolerance bands amid inflationary risks from the Middle East conflict.

- On the economic indicator agenda, the IPCA-15 consumer price index showed higher-than-expected price increases in March, sparking concerns about inflationary acceleration. However, despite the reading exceeding expectations, the cumulative index declined.

- Additionally, the National Household Sample Survey (PNAD) reinforced the perception of a gradual cooling in Brazil's labor market, with unemployment rising to 5.8% in the quarter ending in February, distancing itself from historical lows reached in December.

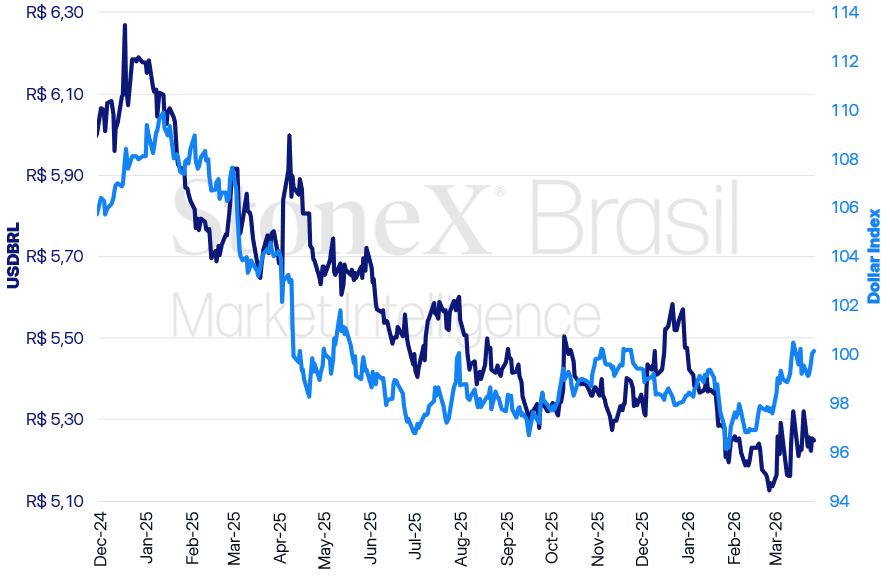

USDBRL and Dollar Index (Points)

Source: StoneX cmdtyView. Design: StoneX.

USDBRL Variations

Daily: -0.13% | Weekly: -1.37% | Monthly: +2.14% | Annual: -4.19% | Last 12 months: -8.87%

Dollar Index Variations

Daily: +0.14% | Weekly: +0.58% | Monthly: +2.62% | Annual: +1.85% | Last 12 months: -3.97%

KEY EVENT: Middle East Conflict Hits 1-Month Mark

Expected Impact on USD/BRL: Bullish

Despite mixed reports in recent days, a swift resolution to the conflict involving Iran, the U.S., and Israel appears increasingly unlikely in the short term, maintaining a high degree of global economic uncertainty.

- The surge in energy commodity prices continues to heighten inflationary risk perceptions, prompting defensive portfolio adjustments, selling pressure on risk assets, and broad dollar strengthening.

- On Thursday (26), U.S. President Donald Trump extended the deadline for Iran—originally set to expire Friday—to accept Washington's proposed terms and avoid strikes on its energy infrastructure.

- The lack of diplomatic progress and growing investor skepticism have pushed the dollar index (DXY), which measures the dollar's performance against a basket of liquid, safe currencies, to a monthly increase of over 2.4%.

Why This Matters: A reduced likelihood of a ceasefire tends to fuel global risk aversion, given the perception that the conflict's prolongation could disrupt shipping flows through the Strait of Hormuz—one of the key logistical bottlenecks for oil and derivatives from the Persian Gulf—leading to sustained inflationary pressures and faster global economic deceleration.

Ceasefire Terms: On Wednesday (25), reports emerged that the U.S. had sent Iran a 15-point structured ceasefire proposal.

- According to sources, the terms included removing enriched uranium stockpiles, curtailing Iran's ballistic missile program, and halting funding for regional allies.

- Iranian officials labeled the proposal as “unilateral and unfair.” To consider an agreement, sources close to the government indicated Tehran would demand guarantees against future military actions, compensation for losses incurred, and some formal control over the Strait of Hormuz.

- Faced with the impasse, President Trump stated he was unsure whether the U.S. would be willing to advance negotiations, keeping the possibility of intensified military actions on the table if terms are not accepted.

The Dollar's Strength Reflects Demand for Safety and Liquidity: Amid the escalating conflict, the dollar's role as the primary safe-haven asset in the global financial system has reemerged.

- Since early 2025, this characteristic had been waning as a significant portion of investors began questioning U.S. institutional predictability and the dollar's stability as a reserve currency.

- The geopolitical shock, however, shifted this dynamic. In an environment of high uncertainty, market participants are favoring not only traditionally safe assets but also highly liquid instruments capable of facilitating swift portfolio adjustments.

- This explains the weaker performance of other defensive assets like gold, which, despite its safe-haven status, has lower relative liquidity when rapid reallocation becomes critical.

Potential Deployment of Additional U.S. Troops: Meanwhile, American media outlets reported that the Pentagon is considering expanding its military presence in the Middle East, potentially sending around 10,000 additional troops for ground operations.

- The move comes amid reports that President Donald Trump is contemplating a ground offensive against Iran.

- Key strategic targets mentioned include Kharg Island, a central hub for Iran's oil exports, and coastal areas along the country.

- While the exact destination of the troops remains unconfirmed, reports suggest positioning that would allow for rapid military response, including operations targeting the island.

Marco Rubio's European Visit: In this context, U.S. Secretary of State Marco Rubio traveled to France on Friday (27) for meetings with G7 representatives.

- According to the State Department, the agenda aims to promote American strategic interests, discuss shared security concerns, and explore cooperation opportunities.

- Sources indicate Rubio has not requested immediate military support for freeing the Strait of Hormuz, which remains severely restricted since the conflict began, but rather assistance in the post-war scenario.

- Details regarding the type of support expected have not yet been disclosed. However, Rubio suggested to interlocutors that, in the U.S. government's view, the conflict could be resolved “within weeks.”

U.S. Labor Market Data

Expected Impact on USD/BRL: Bearish

The two most critical U.S. labor market indicators are set to be released next week, offering investors key insights into the country's economic outlook.

- The most important labor market report, the Employment Situation Report ("payroll"), will be published on Friday (03).

- The second key labor data point, the Job Openings and Labor Turnover Survey (JOLTS), will be released on Tuesday (31).

- Recent data from these indicators has painted a mixed picture but is expected to have less influence on monetary policy decisions given inflation concerns, especially amid rising energy commodity prices due to the Middle East conflict.

Why This Matters: If the reports continue to signal deceleration in the U.S. labor market, expectations for faster interest rate cuts are likely to rise, potentially lowering Treasury yields and weakening the dollar globally.

Latest Data: February's payroll report was significantly below expectations, with a negative balance of 92,000 new jobs versus an expected 58,000 gain. Meanwhile, the U.S. unemployment rate rose to 4.4%.

- Conversely, January's JOLTS report showed an improvement in the ratio of job openings to unemployed persons, rising from 0.87 to 0.94.

- This improvement was driven by an increase in job openings and a reduction in unemployment during that period, pointing to a tighter labor market.

Focus on Monetary Policy: Despite mixed signals, U.S. monetary authorities remain focused on controlling inflation. The Personal Consumption Expenditures (PCE) index—considered the Federal Reserve's preferred inflation gauge—has shown resilience at levels above target.

- The latest Summary of Economic Projections (SEP), released after the most recent Federal Open Market Committee (FOMC) meeting, indicated that policymakers anticipate only one rate cut during 2026, underscoring their commitment to price stability, particularly amid the Middle East conflict and rising energy commodity prices.

PMI and Initial Impacts of the Middle East Conflict

Expected Impact on USD/BRL: Bearish

What to Watch in the Data: Beyond the overall PMI levels, investors should focus on the "prices paid" subcomponent of the manufacturing PMI.

- This indicator is likely to capture, in real-time, potential cost pass-throughs from rising energy and input prices, particularly in the context of geopolitical tensions driving up oil and derivative costs.

- Higher readings in this subindex could amplify inflation concerns and shift perceptions about the trajectory of U.S. monetary policy.

Why This Matters: Signs of deteriorating U.S. economic conditions, especially if accompanied by moderating activity without further price acceleration, tend to bolster expectations for rate cuts in the near term. This scenario could lower U.S. Treasury yields and weaken the dollar globally, creating a more favorable environment for emerging market currencies, such as the Brazilian real.

Recent Indicator Trends: The PMI is a diffusion index ranging from 0 to 100, with readings above 50 indicating economic expansion and values below suggesting contraction.

- In the U.S., preliminary March PMI readings from S&P Global surprised to the upside, showing expansion in the manufacturing sector. The index rose from 51.6 in February to 52.4, signaling accelerated activity. The result was notable given the sector's sensitivity to fluctuations in energy commodity prices like oil and diesel.

- The services sector, which accounts for roughly 70% of U.S. GDP, showed slight deceleration, with the index dipping from 51.7 to 51.1. Despite the slowdown, the sector remained in expansion territory, indicating resilience in domestic demand.

INDICATORS

Sources: Central Bank of Brazil; B3; IBGE; Fipe; FGV; MDIC; IPEA; StoneX cmdtyView.