The USDA's November supply and demand report brought some surprises, impacting some markets. Below are the main highlights for soybean, corn, wheat, cotton and vegetable oils in this report.

Soybean

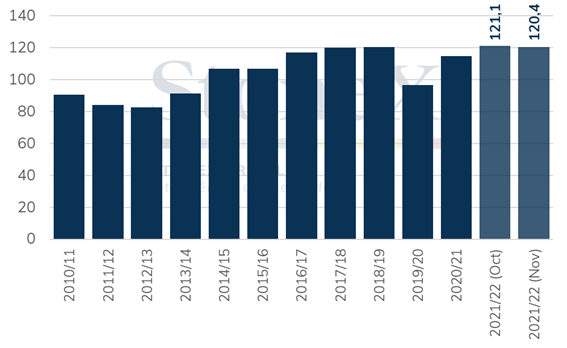

For soybean, the USDA went in the opposite direction of market expectations and slightly reduced the expectation of the US production in 2021/22 to 120.4 million tonnes, as a result of the drop in the average yield, to 51.2 bushels/acre (3.44 tonnes/hectare). It is noteworthy that, unlike the October estimate, at 121 million tonnes, and the latest StoneX number, at 122.2 million tonnes, this production level brought by the Department does not configure a record, occupying the second position as the largest crop ever achieved by the US, slightly behind that recorded in 2018/19.

US soybean production (million tonnes)

Source: USDA. Design: StoneX.

Despite the lower production, there was also a downward revision of the expected volume of US exports until August 2022 and a revision of domestic consumption, which raised the expectation of ending stocks of the oilseed to 9.25 million tonnes. Therefore, there were no changes in the country's 2020/21 soybean balance sheet.

This surprise cut in US production led to a price rally after the report, even though the balance sheet was more comfortable.

In general, other revisions also increased the soybean supply expected for 2021/22, such as the increase in production expected in India and the cut of 1 million tonnes in Chinese imports, which would remain at 100 million.

Even so, in the world balance, consumption grew, and production fell, leading to a small reduction in ending stocks, of less than 1 million tonnes, to 103.8 million. However, it is important to point out that significant changes can still occur until the end of the crop. For example, it is considered that the cut in US exports was not enough given the delay in sales and shipments.

Anyway, on the supply side, new production adjustments in the US should only occur again in the January report, leaving demand at the center of attention, in addition to the prospects for the next crop, 2022/23, at a time when possible area switching are being discussed, in a scenario of high costs, especially for fertilizers.

Corn

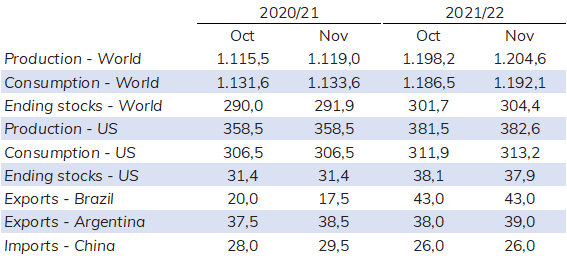

For corn, the USDA raised its number for the US 2021/22 crop yield to 177 bu/acre (11 tonnes/ha), nearly equal to the average market expectation of 176.9 bu/acre (11.10 tonnes/ha), and up from 176.5 bu/acre (11.08 tonnes/ha) in the previous report.

Thus, production increased to 382.6 million tonnes, versus average market estimates of 382.3 million tonnes and 381.5 million tonnes in the last publication. StoneX estimates that US production will total 384 million tonnes in the 2021/22 season, showing an average yield of 177.7 bu/acre (11.15 tonnes/ha).

The USDA also increased its estimate of domestic consumption compared to the last report by 1.3 million tonnes to 313.2 million. This revision reflected the expectation of greater use of corn for ethanol production, now estimated at 133.4 million tonnes, in the face of very favorable margins at US plants.

With these revisions in the supply and demand estimates, ending stocks remained almost stable compared to the figure released last month, at 37.9 million tonnes, slightly above the average market expectation of 37.6 million tonnes.

Turning to the world balance sheet, the estimate of global production for the 2021/22 crop year increased by 6.4 million tonnes, reflecting upward revisions in production in Argentina and the European Union – in addition to the already mentioned increase in the US. The South American country's production was revised up by 1.5 million tonnes to 54.5 million, motivated by the expectation of a larger late corn planting.

On the consumption side, the total demand for the grain was increased by 5.6 million tonnes, driven mainly by the use for human food, seed production and industrial purposes, since the use for animal feed increased by only 1.1 million tonnes.

In addition, it is also worth noting some revisions for the 2020/21 crop. The Department raised Chinese imports by 1.5 million tonnes to 29.5 million, increased Argentine exports by 1 million tonnes to 28.5 million, and reduced Brazilian shipments by 2.5 million tonnes to 17.5 million, a number above StoneX's estimate (16 million tonnes).

As a result of all these changes, global ending stocks for the 2021/22 crop year increased by 2.7 million tonnes to 304.4 million tonnes, above the upper limit of market estimates, which ranged between 294 million and 303.9 million tonnes.

Selected variables - Corn (million tonnes)

Source: USDA. Design: StoneX.

Wheat

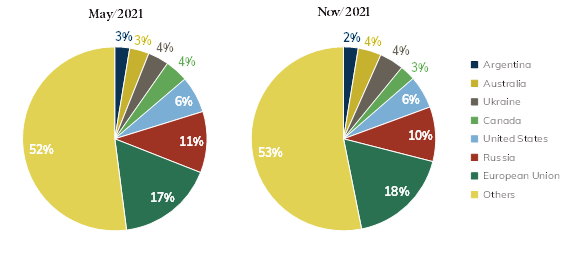

As for wheat, the WASDE update (Nov/21) reinforced the scenario that had already been observed of a more adjusted global supply and demand ratio. The perspective is that in 2021/22, a lower level of global wheat supply will be confirmed due to the revision of beginning stocks (287.95 million tonnes) and the decrease in production (775.28 million tonnes). It is worth remembering that the current crop year was marked by strong corrections in the estimates of major producing and exporting countries. In its most recent update, the USDA brought lower production levels for the EU (-1.0 million tonnes) and the UK (-0.7 million tonnes), which partially offset the increased estimates for Russia (+2.0 million tonnes).

In Europe, despite the increased expectation for Romanian production, the drop in the production estimate results from revisions to the national figures for France and Germany. While in Russia, the production increase is supported by higher than expected yields, even with a smaller harvested area.

This scenario of lower supply faces a slight increase in consumption, driven by higher animal consumption in Russia, Iran, and Turkey, which compensate for the reductions seen in the EU, UK, Ukraine, and Uzbekistan. The USDA still projects an increase in world exports to a record 203.2 million tonnes, mainly due to increased shipments from the EU, India, Russia, and Ukraine. Ending stocks in the 2021/22 crop were reduced from 277.2 million to 275.8 million tonnes due to declines in Australia (-0.5 mmt), EU (-0.98 mmt) and India (-1.0 mmt).

For the US, the USDA brought a lower supply level of winter wheat, mainly due to a lower expected volume of imports. On the other hand, the Department projected a small increase in domestic consumption compared to the Oct/21 balance, from 31.6 million to 31.65 million tonnes, an increase supported by higher anticipated use of seeds for 2022/23. According to the USDA, exports were also revised down due to higher domestic prices for the HRS and White sub-classes and lower-than-expected sales for this time of year. Overall, US ending stocks were revised positively but would still be the lowest level seen since 2007/08.

Production share - Wheat

Source: USDA. Design: StoneX.

For cotton, the report brought few changes. Agents were betting on decreases in global production and consumption due to problems in some crops in the northern hemisphere, especially in India, and the various bottlenecks on the demand side, such as the slowdown in China and the global maritime logistics crisis. However, the data ended up having a more neutral impact.

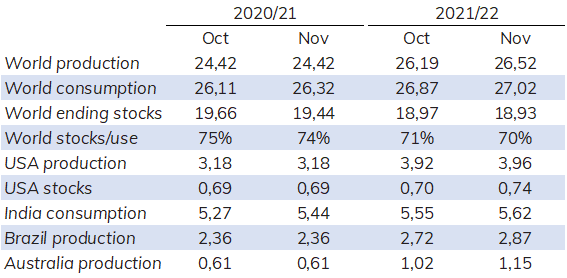

On the supply side, the USDA revised world production to 26.52 million tonnes in the 21/22 crop year, an increase of 330,000 tonnes compared to the October projection and 8.6% higher than in 2020/21. The crop condition in the United States, where more than 60% of cotton is classified as "good or excellent" for several consecutive weeks, continue to be reflected in the projection of yields in the country, which rose from 871 pounds/acre to 880 pounds/acre, with the country's production rising to 3.96 million tonnes.

Other important revisions came in the Australian and Brazilian crops, which had increases of 150 thousand and 130 thousand tonnes, respectively, in their production expectations for the 2021/22 season, helping this global increase.

There was an increase in the projection of world consumption for demand by 150,000 tonnes to 27.02 million tonnes in the 2021/22 season. This movement was driven by Pakistan, Bangladesh, and India, where domestic consumption rose from 5.55 million tonnes in October to 5.62 million tonnes, reflecting the strong recovery of the Indian economy and its textile industry. However, even with production growing more than consumption, global stocks had a slight decrease, reflecting the previous crop, keeping the more neutral tone of the publication for cotton.

It is important to highlight some data regarding China and India. First, Indian stocks, although revised in October and in November, may still be overestimated, an assessment mainly reinforced by recent crop losses in the Muntajat region, which has suffered from outbreaks of pink bollworm. Finally, Chinese demand was revised in October, but there were no changes in this report. China has been facing domestic issues such as the energy crisis, which involves coal shortages and a slowdown, albeit timid, in its economy. Another critical variable, which may affect the demand for cotton in the coming months is the global logistics crisis, evidenced by the lack of ships and containers due to the sudden resumption of trade, especially in the commodities market. In this scenario, the USDA maintained its projection for US exports when the market was betting on an upward change.

Selected variables - Cotton (million tonnes)

Source: USDA. Design: StoneX.

As far as the vegetable oil complex is concerned, the November WASDE did not bring any major changes to the global S&D dynamics of the main oils, generating few reflections on the pricing of futures throughout the week.

The main movements in the report were the upward revisions to US soybean oil stocks for the 2020/21 and 2021/22 crops. The 5.4% hike in the revised US soybean oil inventories was passed to the next crop, with the final stockpile volume up 6% from the October estimate. Despite the upward revision of 2021/22 stocks, the USDA still expects an available volume of soybeans 12% lower than the end of the 2020/21 season but slightly higher than the 2019/20 season. The higher US domestic consumption expected for 2021/22 (totaling 11.3 million tonnes, 7% higher than the previous season) overlaps the expected drop in US soybean oil exports and contributes to pressure on ending stocks.

Regarding the higher expected consumption of soybean oil in the US 21/22 season, the main driver of demand is the fuel sector, mainly the biodiesel one, whose destination of oil is expected to grow 24% from 2020/21 to 4.99 million tonnes, a scenario mainly influenced by the resumption of fuel consumption after the pandemic shutdowns.

In a global outlook, there were no other major revisions in estimates for soybean oil. However, global soybean oil ending stocks for 2021/22 were revised upwards by 1.1% to 4.1 million tonnes, mainly pulled by the revision in the US.

Selected variables - Soybean oil (million tonnes)

Source: USDA. Design: StoneX.

For palm oil, the main revision in November was the 2.7% increase in import expectations from India in 2021/22, favored by the tax reductions provided by the Indian government in recent months for vegetable oils imports.