The intention of the below graphs are not to use to say "my price should be X based on this graph". These prices are derived from an FOB price point average. The intent is to show major global price movement trends. Your values will likely have significant basis difference (similar to your local grain price being different than the traded market price).

This graph is labeled as MT in USD currency.

I am watching one thing and one thing only over the next 30-days in regards to the global UAN marketplace.

Trump vs Putin

Much of the global UAN pricing is set on Russian export values...and the U.S. has become one of the few major destinations remaining for Russia. Europe is still struggling with lower production rates due to high natural gas costs, but much of that is being backfilled by N.A. manufactured tons. So the thing I am watching is how the Trump/Putin relationship plays out when Trump takes office again.

During his original 4-year term, we saw more world peace than in a very long time. However, we also know that when Trump doesn't get what he wants, he is a big proponent of using tariff's...just ask anyone in Canada right now. The hope is that Trump will be able to convince Putin to remove his forces from Ukraine, bring peace to the region which would usher in normalcy/stability back to global markets. However, Putin has been pursuing this invasion for a long time at the cost of hundreds of thousands of souls. It will be very hard for him to just say "ok, I'll leave now". If he stays, it is very feasible that the U.S. will tariff all Russian goods which would include UAN.

- If Russia refuses to leave Ukraine and Trump attacks with tariffs which blocks UAN shipments, likely we will see Black Sea UAN values drop further due to lack of options. I do not think it will signal an actual drop in global prices, more that it will mean Russian exporters must get more aggressive in the few destinations remaining to them.

- On the flip side, negotiation success could mean normalizing global relationships which could actually INCREASE Black Sea price ideas. If Russia agrees to remove forces and that is met with cordial relationships with Russia, their exporters would once again have the world available to them. That means they no longer have to desperately insert themselves into select markets. More options for sellers typically means higher prices.

All that aside, I am still more bullish on the near term outlook for UAN. Global urea markets still look tight and therefore bullish to me. If urea is bullish, UAN is most likely to follow. I also believe European production is going to continue to suffer for the foreseeable future which greatly impacts global UAN supplies.

There are simply too many factors at play that support UAN values short term.

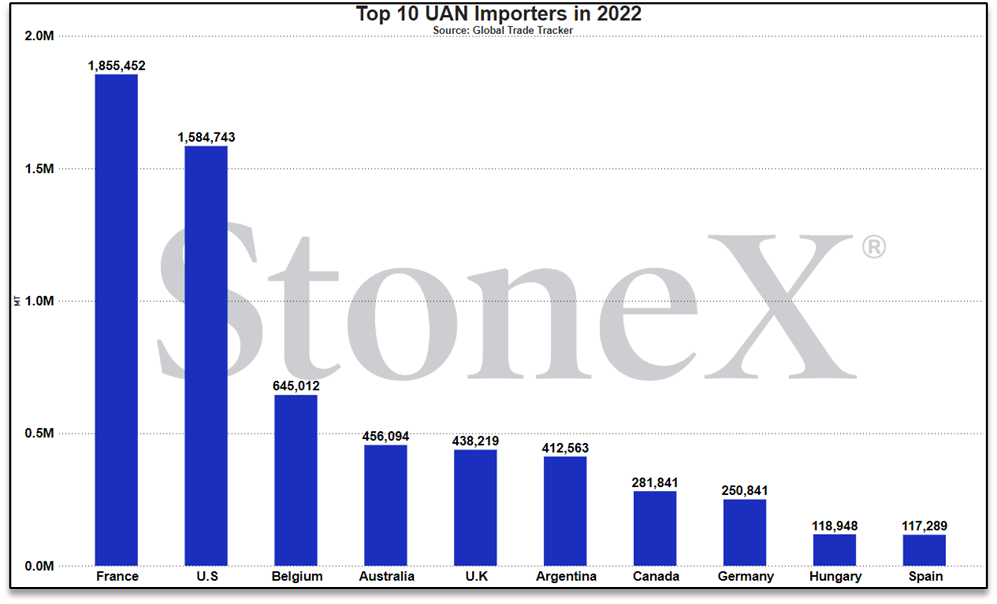

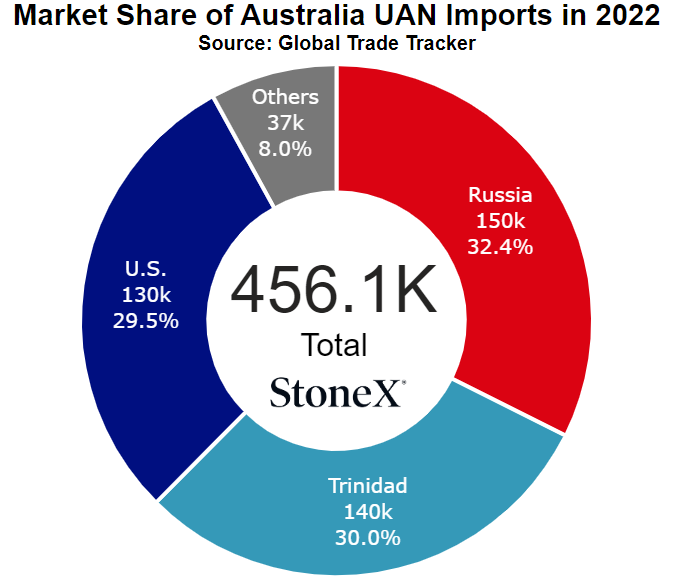

Given that Australia is almost solely reliant on the U.S. for its UAN supplies (since Russian imports are still blocked), I am copying the U.S. UAN market outlook and putting it here. What happens in the U.S. effectively happens to Australia right now.

Yep, gonna talk about Trump!

Since the start of the Russian invasion of Ukraine, U.S. farmers have actually benefitted. The U.S. led the charge of "we need to block Russian goods"...and then quietly backed away from blocking fundamental products like fertilizer (sorry Australia and Canada). Once the dust settled, the U.S. became one of the last few major UAN destinations available to Russian exporters. This meant more supply and more competition with N.A. based manufacturers.

Now with Trump taking office, we have to ponder what happens if Trump can convince Putin to leave Ukraine. If he can, Russia's departure would hopefully mean global relationships returning to normal. That would mean Russia being able to access other global UAN demand spots. Great for those countries...not so great for the U.S.

Unfortunately, the flip side could be worse. If Putin refuses to leave, we know Trump loves tariff's. We could see his reaction being a wide reaching blockade of Russian goods to the U.S. which would include UAN. In that case, the U.S./N.A. markets lose one of the biggest competitors to N.A. based nitrogen manufacturers. Less competition typically means higher prices.

If we remove all the Trump/Putin conversations, my outlook is still bullish. I tend to see urea prices higher on tight supplies and with northern hemisphere spring demand looming, that demand rush should be coming soon that will support price ideas. N.A. manufacturers are not likely to let a nitrogen bullish story go to waste. I feel confident that prices will hold/push higher for preplant needs. Sidedress is a little more iffy but even if prices corrected lower during that period, I do not think it would be by much.

Just remember that the next 30-day period is going to be important. The U.S. change of administration means a new approach to global politics. Love him or hate him, his first 4-years did see relative peace around the world. If he can recapture that lightning in a bottle, we could see global nitrogen/UAN return to normal as well...eventually.

2025 UAN market outlook

With each fertilizer, I decided I wanted to do a general market outlook for the coming year. This is not going to capture every single thing that will impact supplies/pricing. If I knew all of that, I would be writing this on a beach somewhere. However, this is meant to give insight into what we are watching the most.

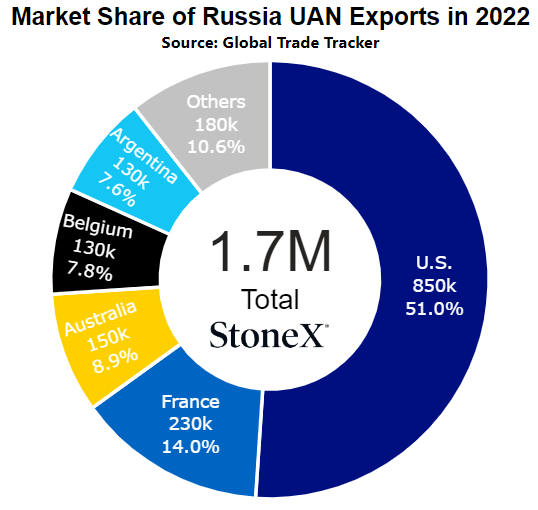

- Russian destinations - when it comes to urea/phosphate/potash, Russia has plenty of friendly countries to ship to. They can handle western countries pushing them out. All they have to do is shift their ships to countries like China/Brazil/India. These are countries that have been willing to ignore western calls to slow/stop shipments from Russia in favor of cheaper prices and guaranteed supplies. However, UAN is different. The world of UAN is much smaller than other major fertilizers...and many major destinations are western countries. UAN is simply a harder product. It is harder to use as you need more specialized equipment. It is harder to ship as you need leakproof containers. It is harder to transport from ports to farmers. We have already seen Australia and Canada block Russian fertilizer products. We have seen Europe be unwilling to take their product, and there is a chance that larger tariffs be implemented. Now, with Trump taking office, there is a chance that the U.S. may start blocking product as well (more details below). In the end, this could leave Russia with very few destinations available to them...which might mean their having to abandon production of UAN which would further tighten the global S&D.

- European production - Europe has continued to struggle with high natural gas values which started with the stoppage of shipments thru the Nordstream pipelines and was ensure to continued when someone attacked the underwater lines. As a result, European UAN production continues to be estimated at 75% of normal. To put that into perspective, that 25% that is offline represents approximately 2M tons of UAN production per year. Unfortunately, we do not see this improving near term. Even if peace could be found between Russia/Ukraine and as a result a normalization in relationships between the Europe/Russia, only then would they start repairs to the pipeline. A pipeline that was damaged as it was would take time to repair if it were on land. This wasn't. This pipe lies under the water where repairs take longer and are much more complicated. Unfortunately, it looks like European production is going to remain low for the time being.

- Tight N.A. supply outlook / timing - we are currently in the middle of rerunning our demand models as we start 2025...and it doesn't look good for UAN. First, imports have been slower than normal while exports have picked up the pace. That hurts. Second, there have been several production hiccups across North America. On their own, they do not make much of an impact to supplies, but combined they represent a few hundred thousand tons of expected production to vanish. Third, nitrogen demand for the spring is growing. Not only did fall NH3 fall slightly below normal, but we are also seeing 2025 corn acres growing. We just moved our acreage up to 92.5M. Last, winter production can be tough. We are currently staring down a very cold event moving across North America. You can read more about it below, but if this cold dips far enough south and lasts long enough, we could see UAN production slow/stop to all gas to flow to residential demand. As tight as the S&D already is, that would hurt...and hurt bad.

Fortunately, we have not seen UAN values rise recently as we had expected...but these points continue to drive our POV that bullish markets lie ahead. No doubt other things will happen that are not expected. They always do but for what we know today, these are the things that are keeping us up at night.

How will Trump administration change global UAN trade flows?

Let me clarify. What I actually mean by that title is "how will North American UAN markets change if Trump comes in and blocks Russian imports".

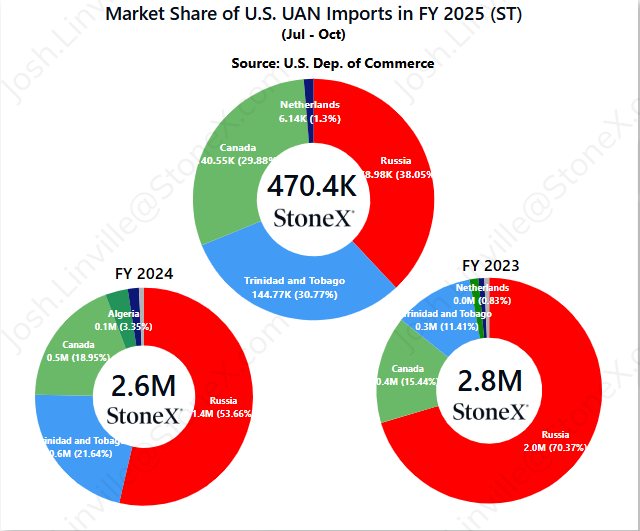

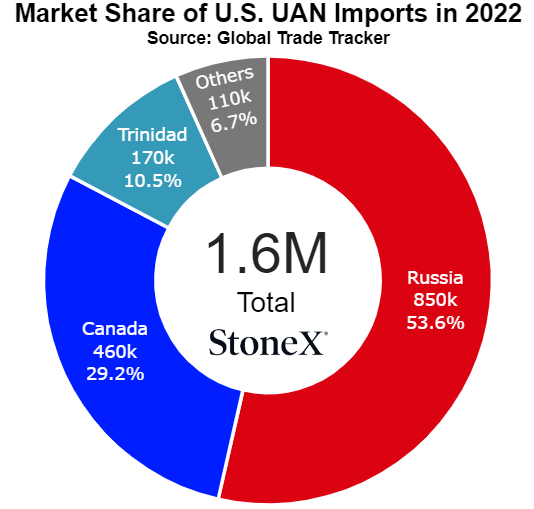

Canadian readers may be seeing this piece and wondering "why does this matter to me? Canada blocked Russia already." You would be right. Canada, along with Australia, fully blocked imports from Russia and have maintained that status. However, I always see Canada/U.S. as a single entity and the U.S. has continued to receive Russian product. In fact, over the last few years, Russian imports have accounted for the majority of tons received. For Canadian farmers, as long as the U.S. receives tons, that allows more U.S. tons to flow to Canada. The N.A. S&D remain in better shape than it could be...if those imports stopped.

Which is exactly what I am starting to fear.

In the next month, President Trump will start his 2nd term. To me, it seemed like he came into his 1st term a bit surprised by the fact he won. It took a while for him to figure out the system, his team, etc. This time that isn't a problem. He is coming into this 2nd term at a dead sprint, and he intends to make waves.

We know that Trump is a firm believer in tariffs as a tool/weapon. We also know that Presidents Trump and Putin seem to have a cordial relationship. Our hope is that this relationship can mean a swift end to the Russian invasion of Ukraine...but what if it doesn't? If Trump takes office, reaches out to Putin to put an end to the invasion, and is told to...well, let's say mind his own business! In that scenario, I could see Trump swiftly taking action and starting to put blockades on all things from Russia.

This would not help buyers of UAN.

In that scenario, the U.S. / N.A. markets suddenly loses its largest external supplier. That leads to a loss of competition. To make matters worse, where else will those tons come from? The global UAN market is nowhere near as robust as urea and NH3. There are not many major manufacturers out there so options are limited. To add fuel to the fire, Russia losing the U.S. market would mean they are running out of destination options. Rather than trying to find a home for UAN, they may just slow down UAN production which would hurt the global S&D even more than it already is.

Now, this is all predicated on "if". We do not know what will happen when the changing of the guard happens. This is all speculation. However, it is important to know what it "could" mean if it happens. Better to be prepared and ready to act rather than not prepared and having to react...

What does this mean for Aussie farmers?

If President Trump takes office and quickly starts to block Russian imports, then that leaves domestic U.S. / N.A. manufacturers with little to no competition from outside sources. They will be able to consider plenty of destination opportunities with much less fear of losing demand to imports. If N.A. farmers are not buying, they can consider Europe or Australia as a "relief valve" of sorts. However, with N.A. spring season around the corner, that need to get rid of tons is getting lower. N.A. farmers will need to start making preparations sooner than later and the supply side knows this.

Basically, if this story starts to play out, U.S. / N.A. UAN manufacturers will be in control and will have much less need to export. If N.A. values start to move higher, then Aussie price ideas will need to follow suit.

All of this is speculation, mind you. We do not know what will happen when Trump takes office. This is merely something that needs to be considered so we know how to act if it does happen.

Time before spring running out, can ill afford production hiccups

As I write this, a large portion of North America is staring down the barrel of an extremely cold pattern setting in. If this thing plays out as they expect, Northern Plains/Canadian farmers might actually put on a pair of gloves to stay warm!!!

I typically do not spend a lot of time worrying about northern temps in the winter. It gets cold...and you guys and gals are used to it. Just a part of life. That said, I spend a lot more time watching territory south of Kansas City. Once you get south of where I am, the cold is a bigger deal...and it looks like it is going to get cold.

So what happens in those scenarios? A massive cold bubble extends to the southern states who are ill equipped for it. This causes natural gas demand to surge so people can stay warm. That surge in demand causes spot gas prices to skyrocket...and present nitrogen manufacturers an opportunity.

Most nitrogen manufacturers "should" be locking up gas futures when they dip and head into the winter with a lot of inputs already secured. Well, as much as we may not like it, they may have an opportunity to shut down nitrogen production and sell those gas futures back to the spot market at a higher profit than if they made fertilizer. We have seen this the last couple winters when artic blasts made their way thru. The longer the cold lasts, the bigger the opportunity...but unfortunately the longer the production downtime.

This feels an even more important watch point this year for UAN. Our demand models are continuing to reflect a UAN market that is extremely tightly supplied. There has already been several production outages. Any single one by itself is no big deal but combined, they account for a few hundred thousand tons of production as "missing". We are also continuing to watch exports exceed average tonnages due to Europe's ongoing production issues due to their own high natural gas costs. Lastly, as detailed above, we need to be wary of what the Trump administration will do to Russian imports. Russian product has remained one of the few competitive imports for domestic production. If those tons get blocked, it could be painful.

All in all, our S&D is tight...and it isn't getting better. If we have any sort of further production hiccups, whether that be weather or plant related, it is only going to make a bad situation worse.

What does this mean for Aussie farmers?

Again, with Australia being so dependent on the U.S. for its supplies, if there is a sudden and unexpected cold event that shuts down production, then already tight supplies get tighter. Nitrogen demand is staying steady/pushing slightly higher for 2025. So lower supplies + level demand = higher price possibility.

As N.A. spring looms, demand should pick up and make it so that manufacturers have little need to export. That means much less chance of them needing to lower price ideas to ship here.

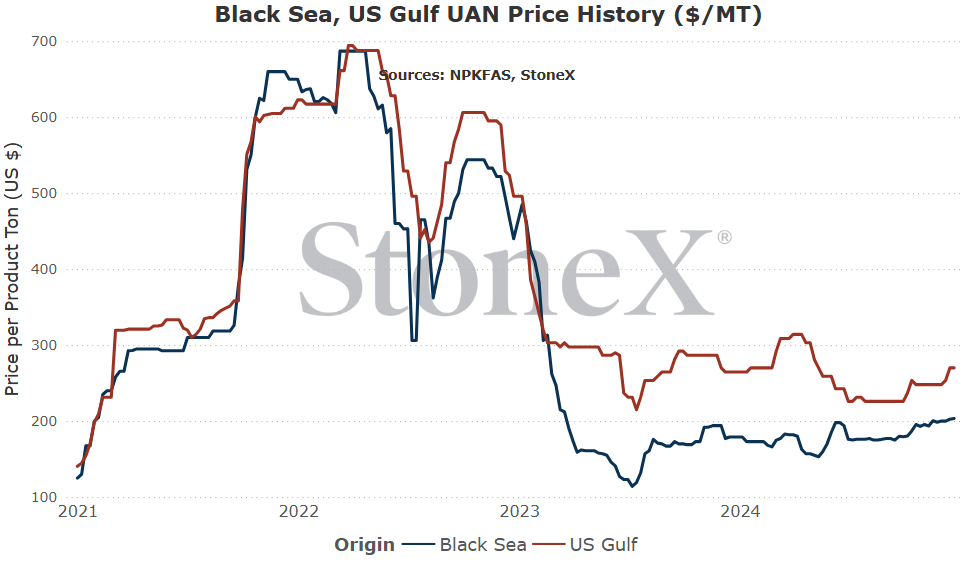

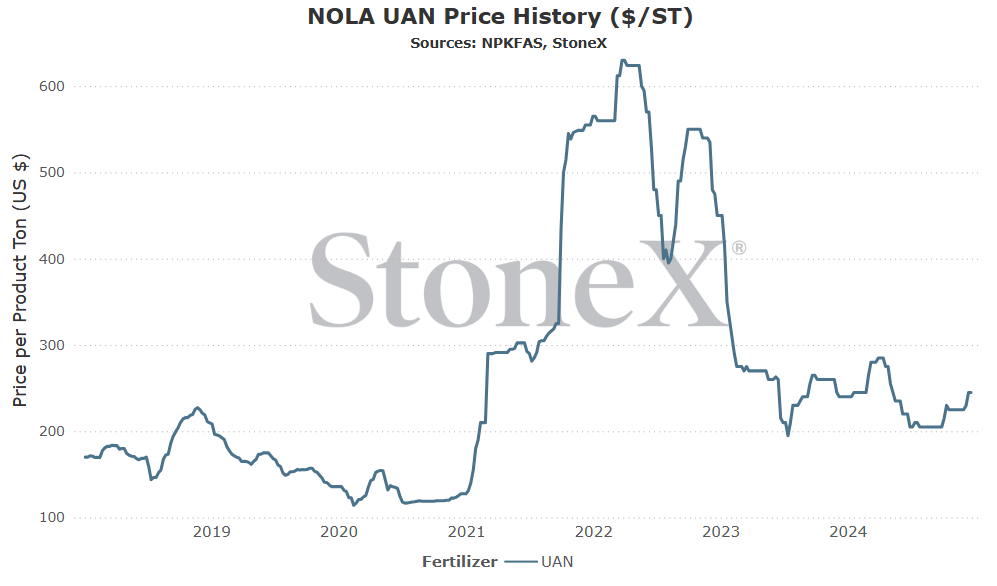

NOLA/New Orleans, Louisiana

Number 2 global importer in 2022

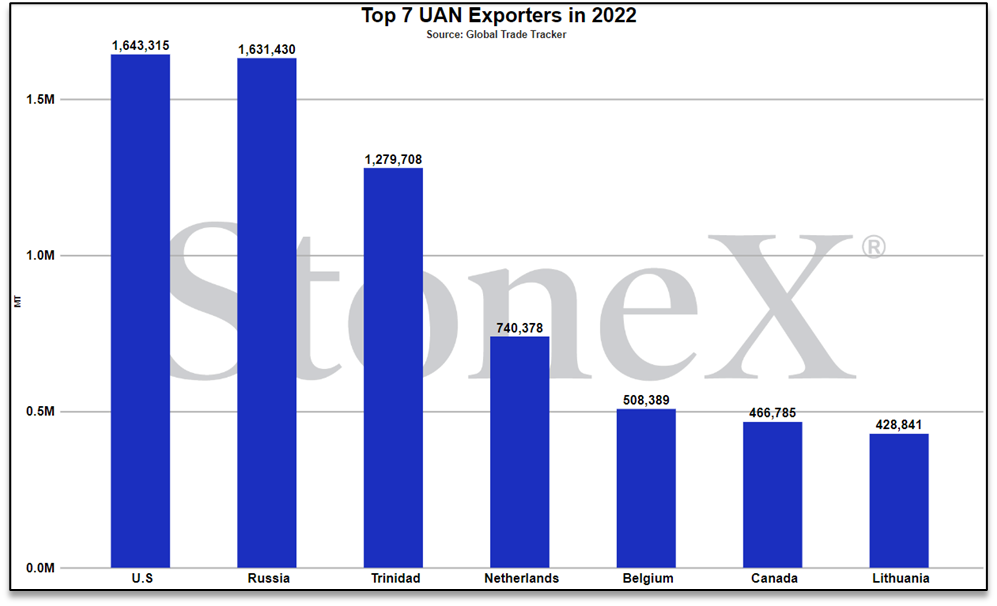

Number 1 global exporter in 2022

Price comparisons

Vs 30 days ago - 9% or approximately $20 higher

Vs 90 days ago - 20% or approximately $40 higher

Vs 6 months ago - 11% or approximately $25 higher

Vs 1 year ago - 2% or approximately $5 higher

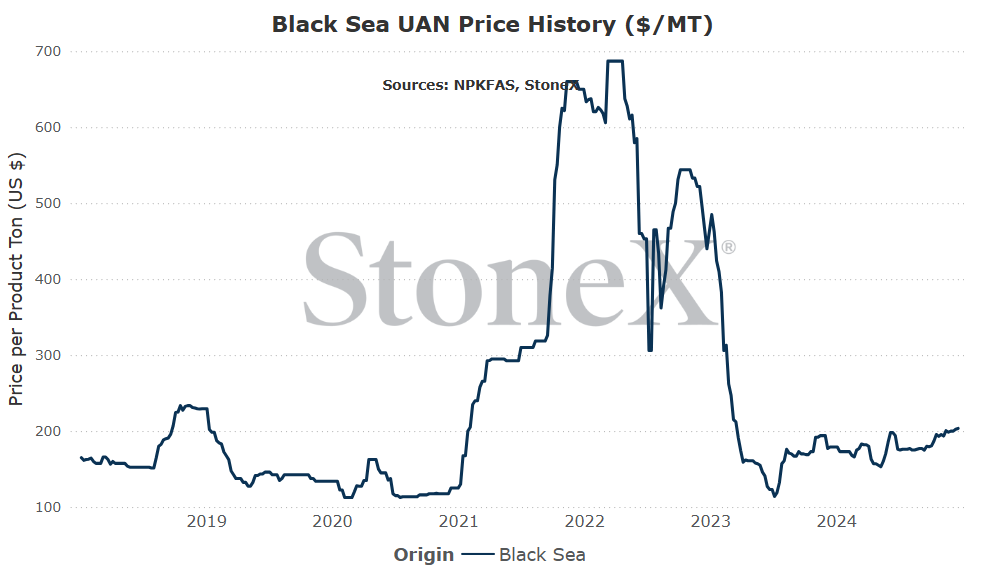

Black Sea (Russia)

Number 2 global exporter in 2022

Price comparisons:

Vs 30 days ago - 3% or approximately $5 higher

Vs 90 days ago - 13% or approximately $24 higher

Vs 6 months ago - 5% or approximately $10 higher

Vs 1 year ago - 14% or approximately $25 higher

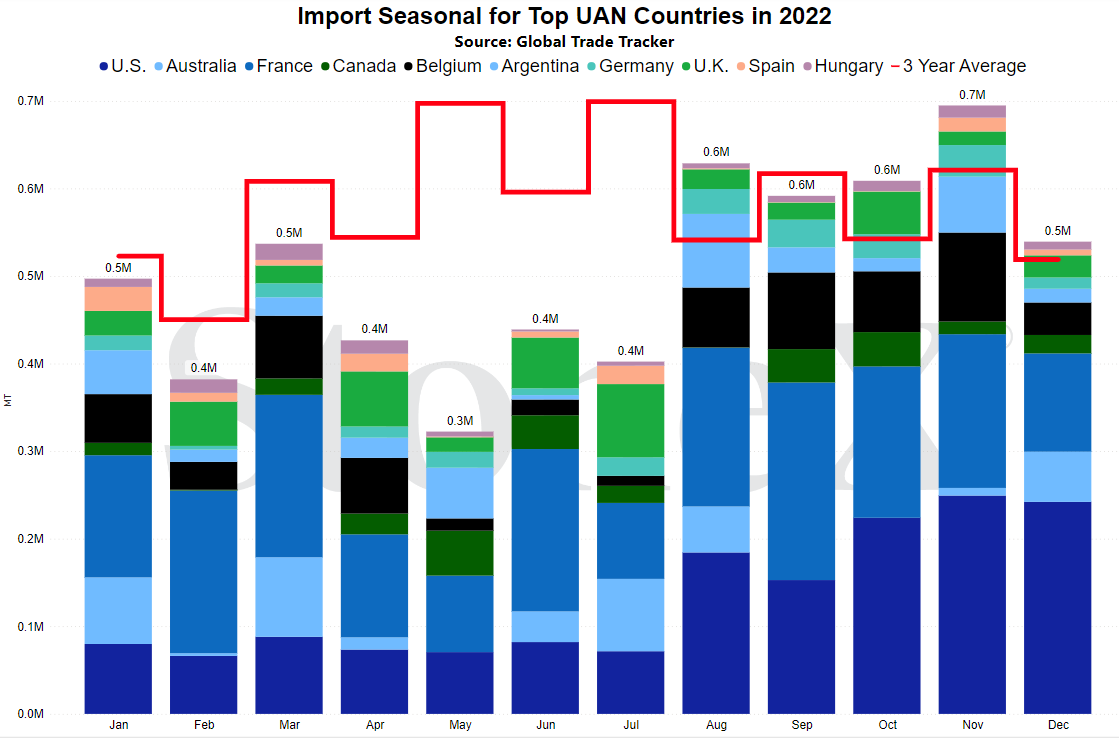

- Time is getting tight for Northern Hemisphere spring season – while it may not seem like it today, logistically speaking spring season is just around the corner. There is typically a bit of a downtime in late January/February that can cause prices to dip, but given how tight the global UAN market is today, that should not have a large effect. Global shipments need to be picking up the pace or run the risk of missing spring. Buyers getting backed into that corner is rarely a bearish situation.

- U.S. / Canada tariff threats could hurt pricing – while it remains to be seen how it will play out, President Trump has made it very well known that he plans to place tariff's on Canadian goods if his demands are not met. We are also seeing some Canadian politicians wanting to fight fire with fire. If we see tariff's imposed on both sides that include UAN, it is much more likely that both sides farmers will pay the price...

- Incoming Trump admin could block Russian imports – speaking of President Trump, how he proceeds with Russia/Putin could be hugely detrimental to the N.A. UAN marketplace. Canada currently has blocked any shipments from Russia so one might think it will have little impact. That could not be further from the truth. U.S. tons continue to flow north so if the U.S. S&D gets impacted and pushes prices higher, Canadian tons will follow. If we see tariff's put in place, it should mean imports slow significantly and U.S. manufacturers no longer need to worry about one of their largest competitors. That should be a green light to rally price ideas.

- Trump admin brings peace and with it, stability – the world has been dealing with a lot of fighting the last few years. Either consciously or subconsciously, that helps to place war premiums in the market. Some have pointed to President Trump's 1st term as a period of relative peace. If he and his administration can replicate that during his 2nd term, the fear of fighting goes away and hopefully the new stability could usher in lower price ideas for nitrogen in general.

- U.S. blocks Russian imports of UAN – so this is a bit of a double edged sword. If you are a U.S. or N.A. farmer, this would be a bad thing. Losing Russia would mean N.A. manufacturers of UAN no longer need to compete against Russian imports. That would likely mean higher prices. However, global buyers would benefit. Russia losing the U.S. as a destination would mean they get more desperate to force their way into the few remaining demand points around the world. Forcing their way in typically means lowering their price ideas. What hurts one group benefits another...

- Sizeable shift away from nitrogen needing acres – this is pretty far down the list of probable events, but it is worth watching. For the U.S., we have actually increased our corn acreage expectation for 2025 from 92 to 92.5M acres. However, there is still time before spring. Farmers can still make changes and if those changes involve switching away from nitrogen intensive crops, we could see demand fall enough to lean on price ideas. Not likely, but worth keeping in mind.

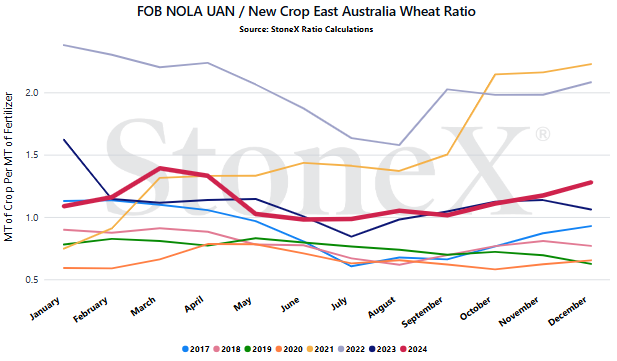

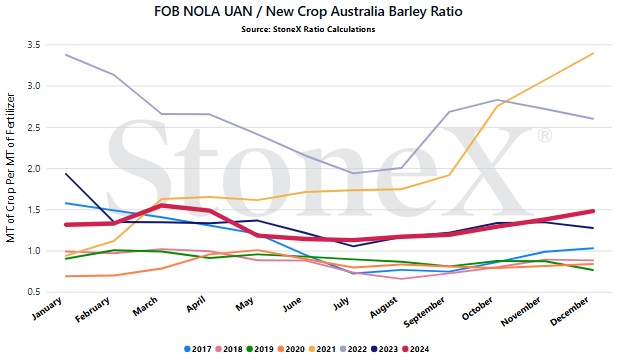

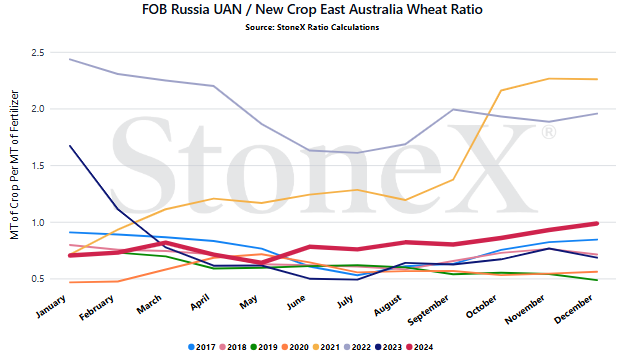

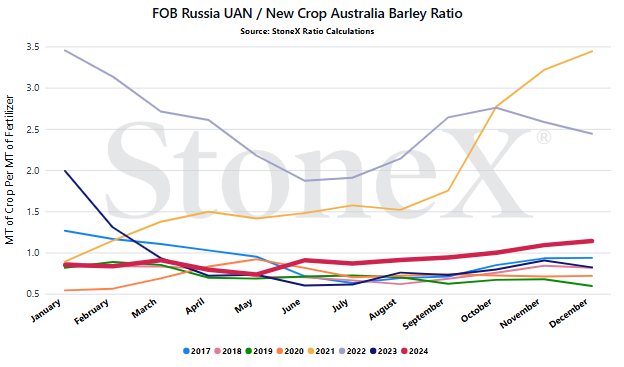

We believe that only looking at the flat price of either grains or fertilizer can be misleading:

-

Only selling grain can hurt you if fertilizer prices rise substantially

-

Only buying fertilizer can hurt you if grain prices fall

We look at the ratio "value" to get a better indication of where we are or how many bushels of X does it take to pay for 1 ton of fertilizer.

Would you rather:

-

Spend 100 bushels to pay for 1 ton of UAN

-

Spend 60 bushels to pay for 1 ton of UAN

When we compare the current ratio value against recent years, we start to see if we are high or low.

YOUR VALUES MAY LOOK DIFFERENT

This graph looks at the NOLA UAN price vs the flat grain price. There are no logistics on either product. Your location will look different due to fertilizer logistical costs, grain basis, etc.

- Russian tonnage destinations - while it may not seem like it to some parts of the world, the UAN global market is very small with few major production origins...and few major demand destinations. That is why it is so important to focus on where tons are allowed to go and why I am so focused on Russian tonnage. Today, Russia is blocked from sending product to Australia and Canada. Large parts of Europe push back against their tons with threats of raising tariffs further. The U.S. has become one of the few major destinations still wide open to their tons...but there is doubt about that future with Trump coming into office. He may convince Putin to find peace in Ukraine and world supply routes return to normal...or they may clash and we see major U.S. tariffs put into place, essentially blocking shipments which would leave domestic manufacturers to their own devices. Global politics play can play large roles in how products are shipped...or not shipped. In the end, we know who pays the price.

- Urea price movement in coming months - UAN values have done a very good job of staying relatively connected to urea price movements. N.A. manufacturers appear to have learned their lesson from a couple winters ago when they kept UAN values insanely high as urea values fell hard. The result was massive farmer switching that ended up costing UAN manufacturers in the end. It was heard from multiple places that they vowed to never allow that to happen again. So if we take them at their word, then a lot of UAN price movement will be dictated by the urea markets. Unfortunately, my current POV is that the urea market is going to be bullish thru much of Q1.

StoneX Ratio Calculation

The ratio calculation is derived from Bloomberg historical grains values as well as fertilizer values from StoneX, NPKFAS, and Argus.

The calculation is simply dividing the fertilizer price by each grain price.

All data was sourced from StoneX unless otherwise noted.