Global

We have been in a cycle for a little while where there has been a lot of demand but potash prices have stayed steady to lower. As we continue to look forward, we see more supplies becoming available as well as a chance that some large global buyers could start to scale back or stop purchases for a bit (and rely on ample domestic inventories).

Barring a hardcore, long-term Canadian rail strike/work stoppage (very low likelihood, in my opinion), it is hard to see much bullishness out there.

North America

We continue to believe that we will start the new fertilizer year (July 1) fairly low on inventories. The fall/spring seasons were really good and should have emptied most warehouses. That means plenty of work that needs done to prepare for the fall run...but nothing "feels" tight. Inventories seem more than adequate. Logistics seem to be doing well. Everything is running like a well oiled machine for potash.

Barring some unforeseen situation or a possible Canada rail strike, hard to see the potash market as anything other than flat to bearish. Maybe if summer fill programs are significantly better received than expected we could see a bump...but it should be very limited.

Potential Canadian rain strike could hurt potash

Strike threats continue as we move into July for Canadian rail workers.

This saga has been going on for a while now. An official strike vote was successful and was supposed to go into effect later May, but hopes of finding common ground caused workers to delay that move.

A 2nd strike vote shows how much relations have deteriorated.

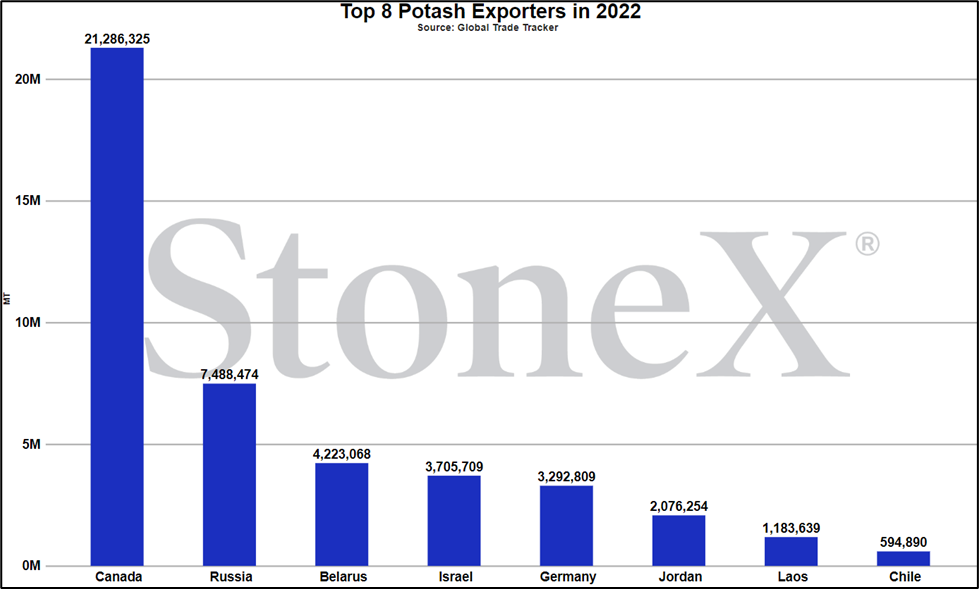

It goes without saying that rail is EXTREMELY important to the N.A. and the global potash market. Canada is the largest global exporter, and if you look at the above exporter graph, you will see that it isn't a close second. I could be wrong but I struggle to see how trucks could make up the difference of losing rail shipments.

Ultimately, I continue to believe that common ground will be found. Workers rarely want to stop working. Rail companies/executives do not want to lose days as it means losing income. Both sides understand the importance of rail to Canada as a whole.

However, the chance of a work stoppage is not zero so we need to continue to watch. Fortunately for the potash market, especially for North America, this is the perfect time for this to happen with there being plenty of time before fall season ramps up. The market could ill afford this happening close to or during fall. It would be hugely detrimental during the short winter. Spring...don't get me started. This is the one period of the year where the market can bear it...to a point. Hopefully, this passes with no issues.

I thought this article did a pretty good job of explaining the current situation:

https://getfea.com/transportation/teamsters-canada-to-hold-second-strik…

Also, I had originally thought that even in the event of a strike, some services would continue as it would be deemed "necessary". After reading this article, I'm no longer so sure...

https://theloadstar.com/rail-strike-in-canada-likely-as-essential-servi…

Global demand remains solid but values keep falling

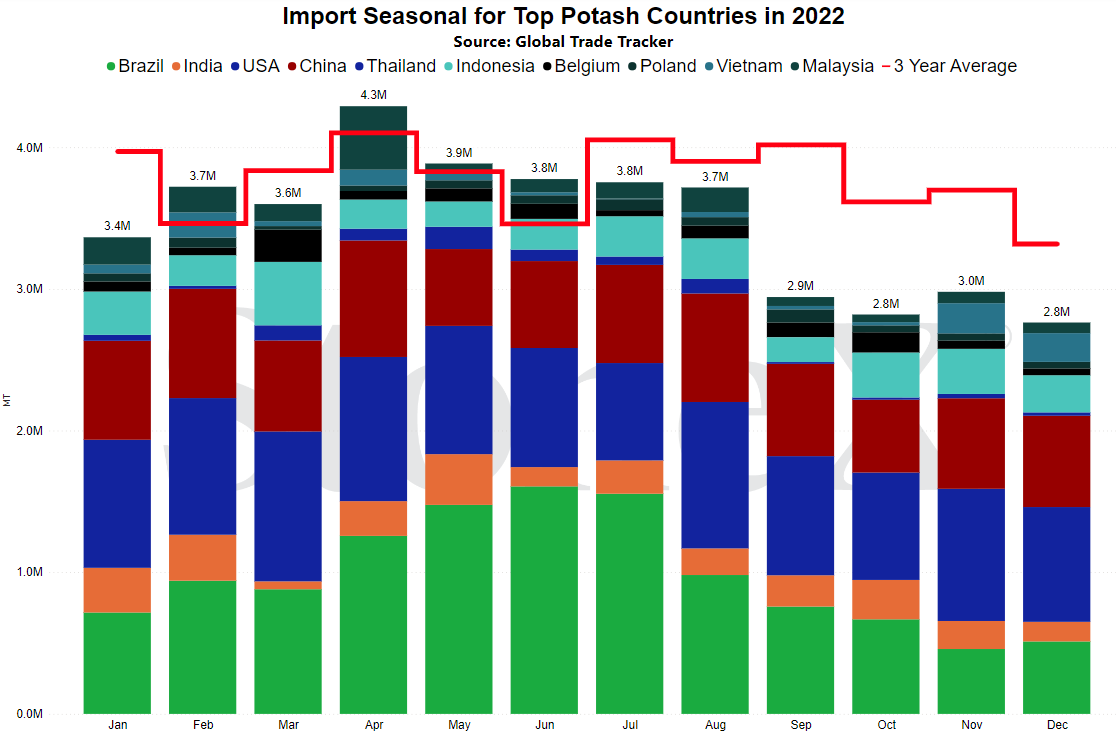

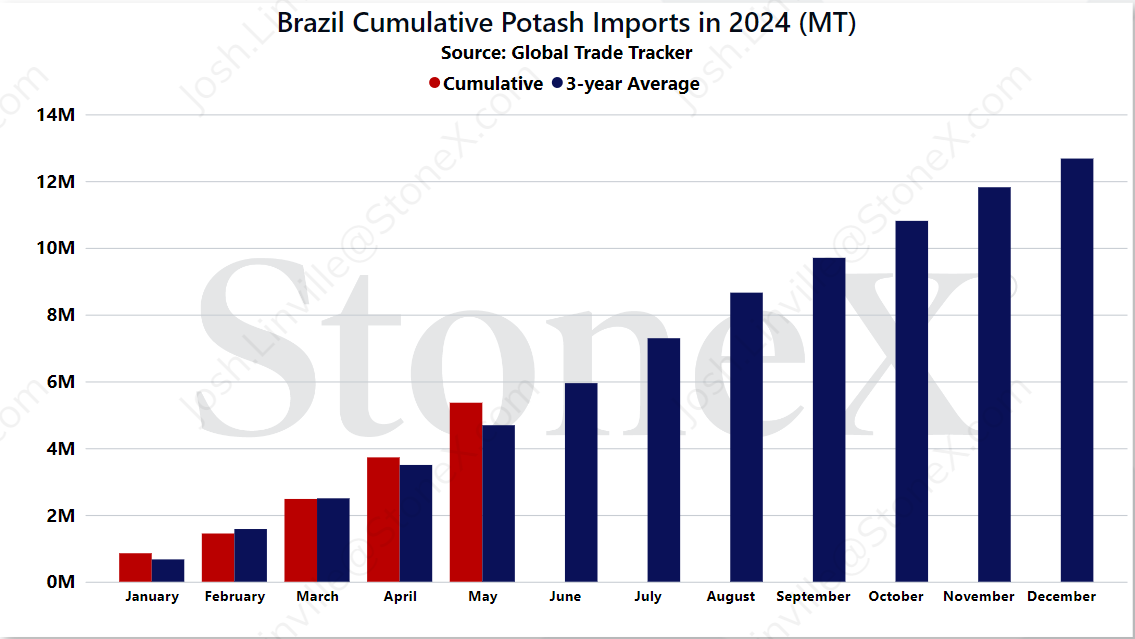

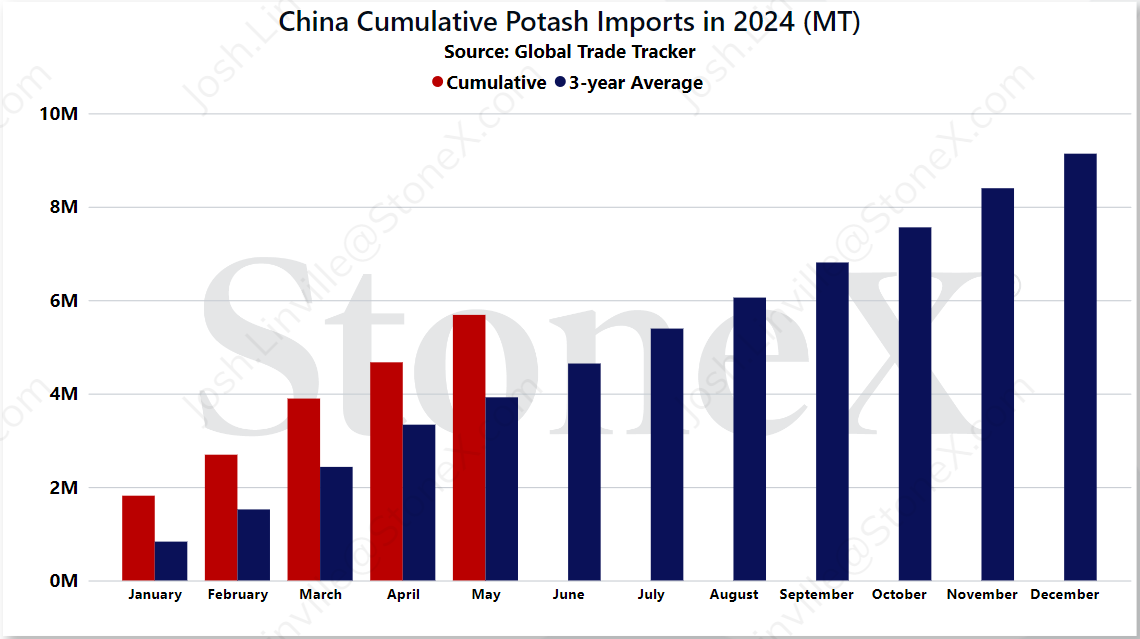

Some of the world's largest buyers have either been in line or well above recent year averages in terms of potash imports. However, at the same time, global potash values have continued to fall. What does that tell us?

Well, short story in case you are pressed for time - potash supplies continue to appear more than adequate vs global demand.

With global demand being so substantial, one would think that we would be seeing prices rise but that just has not been the case. Fortunately, it looks like supplies will continue to grow. China continues to invest in Laos which when finalized on production upgrades should mean that they are much less reliant on Canadian produced tons. Some Russia upgrades are still anticipated. New production in Canada is still being watched for.

Overall, our longer term view of the potash marketplace is one that is well supplied and bordering on over supplied. That is good news for buyers/farmers.

Still no word on India/China annual contracts

The market continues to wait and watch for announcements regarding India's and then China's annual potash contract with Canada...so why no word?

One theory is that both countries see what is happening around the world. As stated above, global values have been bearish in the face of higher than normal demand. They could be using that information/POV to really beat up price ideas on these contracts which is delaying a final verdict.

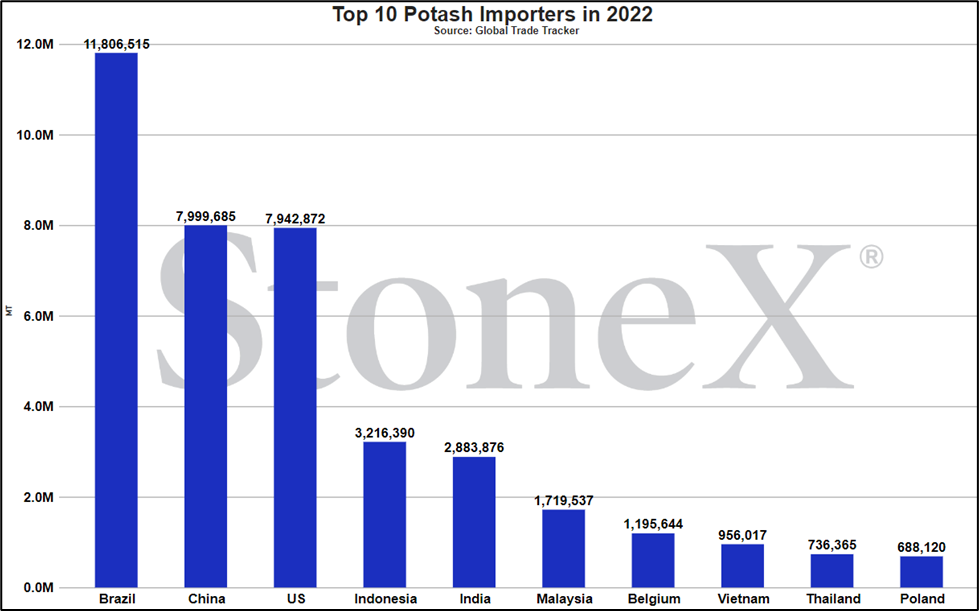

Another theory is that both countries might be deciding that an annual contract is not something they want any longer. Take a look at China's import levels. They are well ahead of normal and have been for a while. Stockpiles should be very good. They have obviously had no issue in getting their hands on product...and supplies continue to look to grow. So why lock into an annual price in a market with no real supply fears and a steady to weak price trend.

We are continuing to watch and do anticipate that something will be announced but the delay/market structure right now shows how much the world has shifted since early 2022.

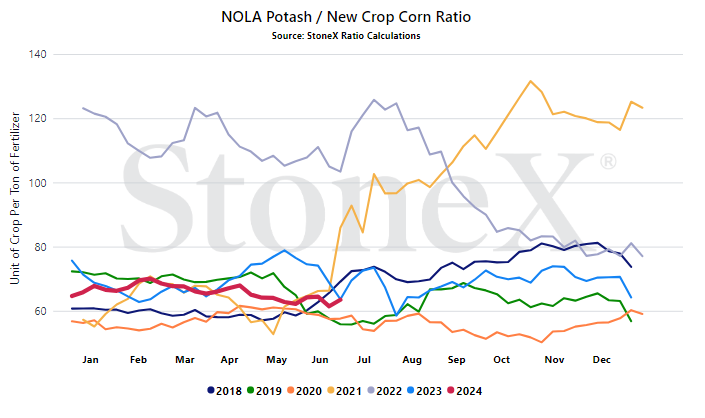

Potash remains attractive vs grain values

With current potash values having fallen significantly from their 2022 high's and never having recovered like other fertilizer products, potash has remained decently priced vs grains...even with grains falling. Could it be better? Sure. Has it been better in recent years? Absolutely.

Does potash still stand out as the best priced input that I can see. 100%.

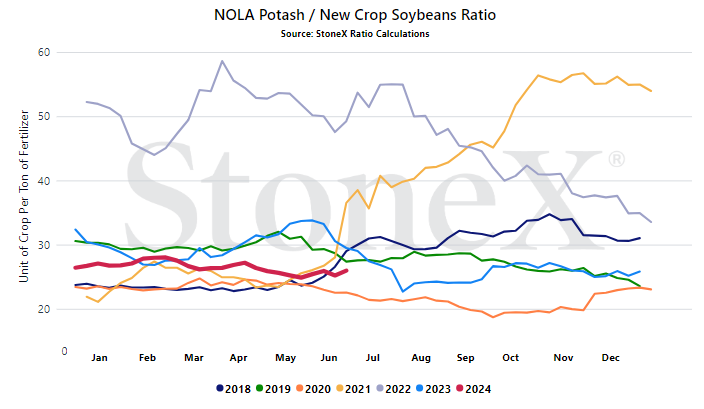

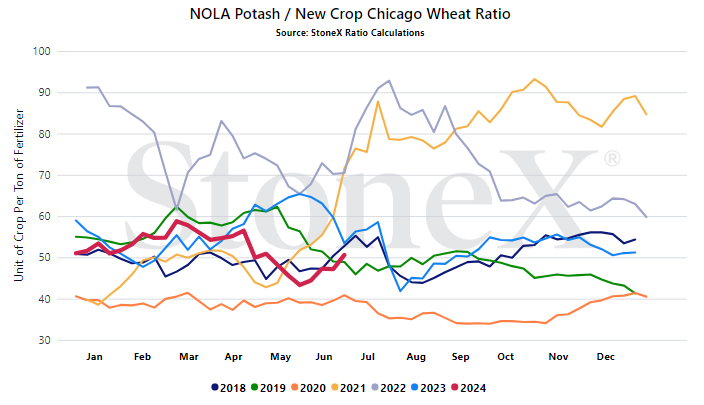

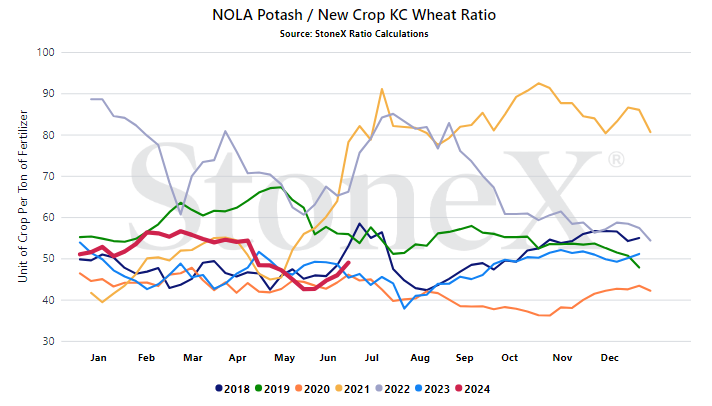

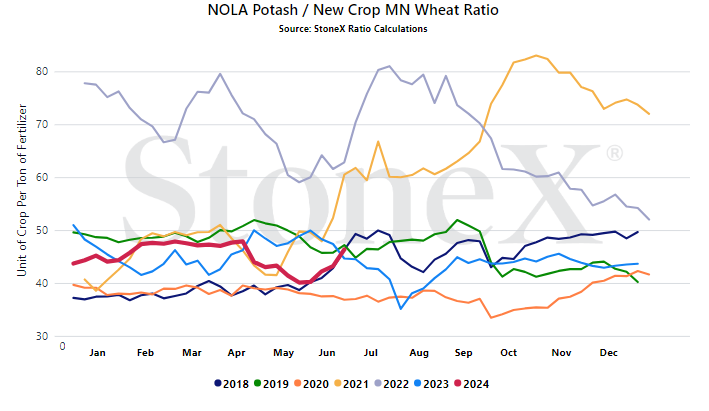

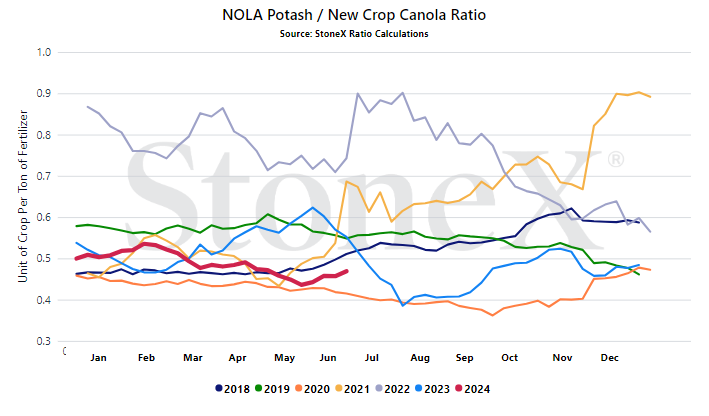

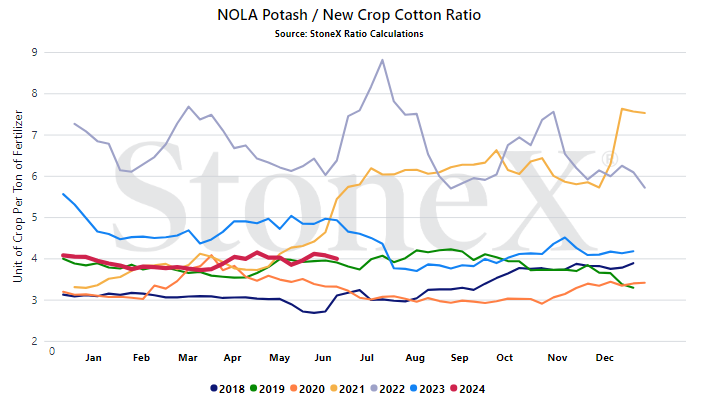

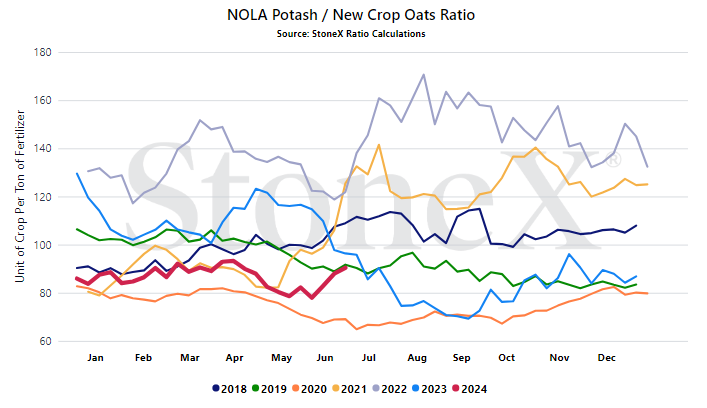

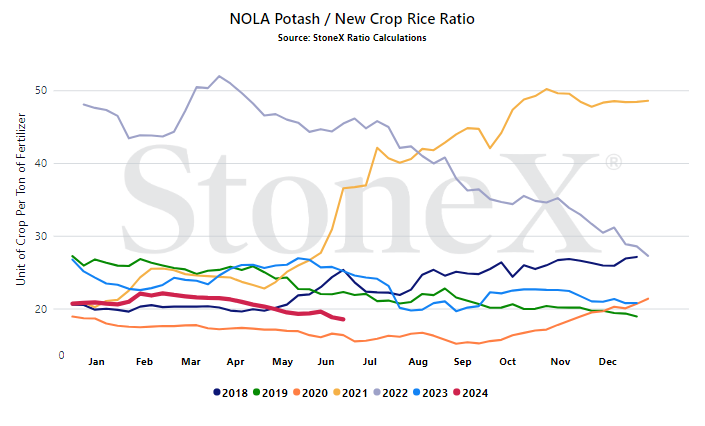

As always, these values are much more important to run where you live. Basis plays a huge role in setting inland values and knowing where your local history is now vs has been is more important. I run these graphs on NOLA (New Orleans) and straight Chicago corn pricing (no basis) because I have no idea where everyone is located. Look at it as a 50,000 foot view, if you will.

Today:

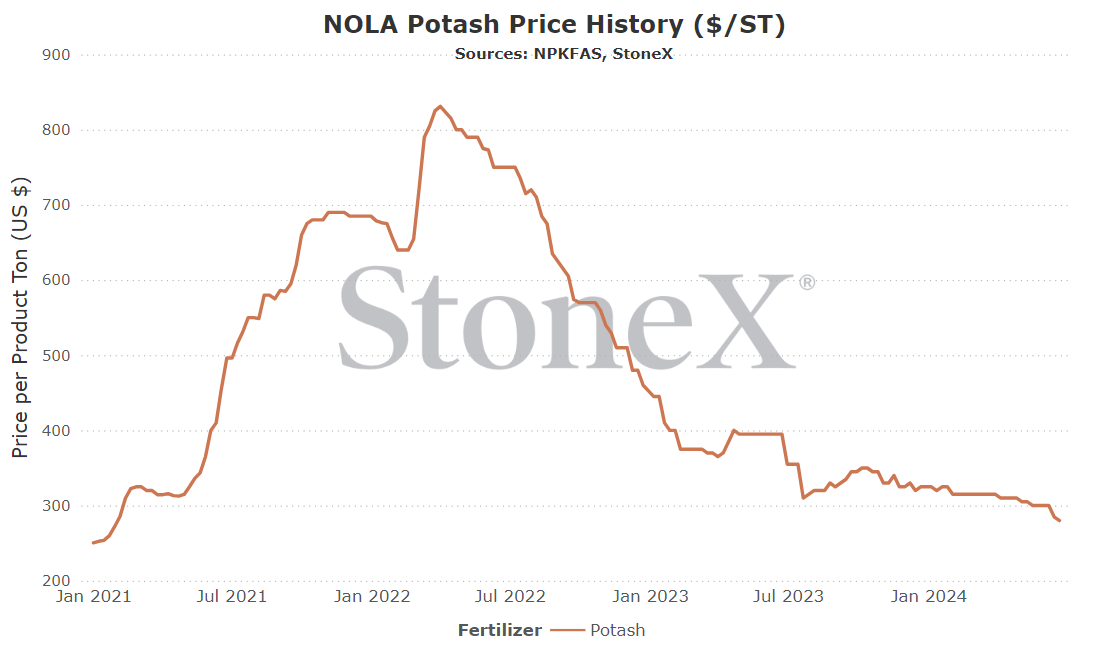

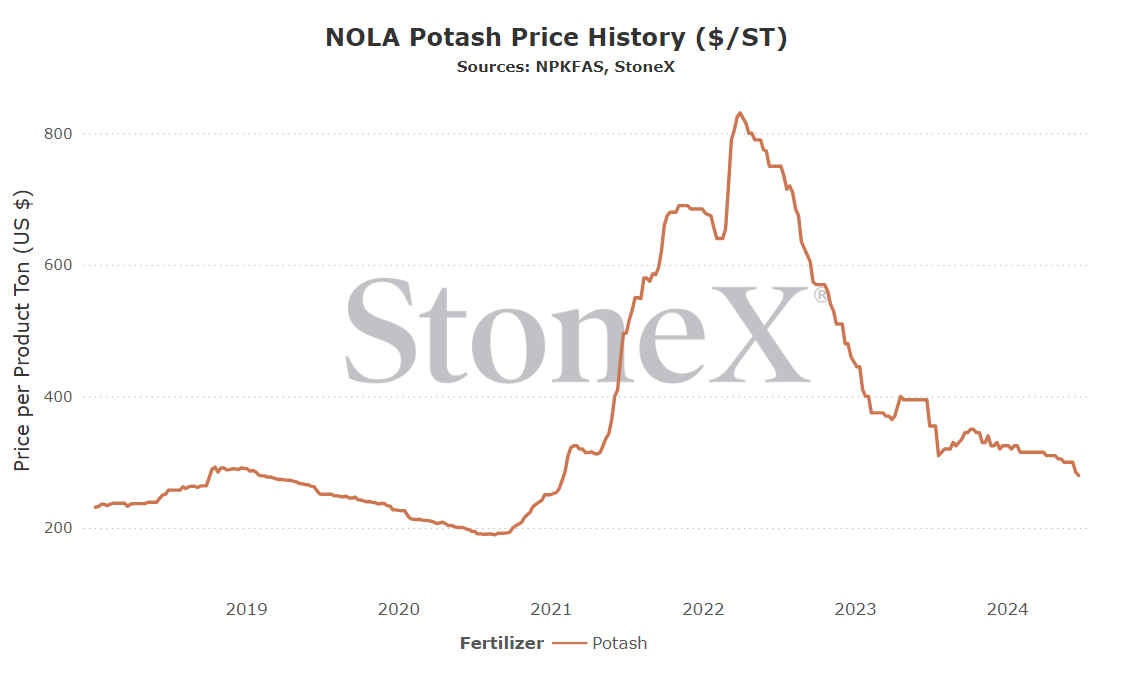

- Potash NOLA barge values - $280

- December '25 corn values - $4.56 (as I write this...puke)

That puts the current ratio at 61.

Glancing at the graph below, we have seen better values going back to 2018...but 61 is toward the lower end of the spectrum. As you go thru the other products, I think you will struggle to find something this aggressive.

Again, run these numbers with your local supplier/retailer. Those matter WAY more. In case you need the formula, it is simple:

Price of fertilizer / price of grain = number of bushels it takes to pay for that fertilizer

You can run that formula based on fertilizer tonnage. You can run that formula based on fertilizer poundage. It doesn't matter so long as you are consistent. Ultimately, all we want to do is spend less grain to pay for fertilizer.

![]()

NOLA/New Orleans Louisiana

Vs 30 days ago - -7% or approximately $20 lower

Vs 90 days ago - -11% or approximately $35 lower

Vs 6 months ago - -14% or approximately $45 lower

Vs 1 year ago - -29% or approximately $115 lower

U.S. Midwest Average (average of several points across the Midwest)

Vs 30 days ago - -1% or approximately $4 lower

Vs 90 days ago - -5% or approximately $20 lower

Vs 6 months ago - -8% or approximately $30 lower

Vs 1 year ago - -14% or approximately $58 lower

- Canadian rail strike – while the chance of an actual work strike is still low, it is not zero. If that happens, it could quickly have decent impacts on supply/logistic capability. Sure, fall applications is still months away, but the calendar moves fast (faster the older I get, as I have learned!!). The market can ill afford losing time.

- More producers scale back production in face of low values - so far we have not seen any other producers follow in Mosaics footsteps from when they curtailed production...but that doesn't mean they will not in the future. "IF" they were to start doing that and it impacted supplies enough, that could drive the potash into a bullish wave.

- All other fertilizers have popped higher, will potash follow? – how long can potash go it alone? All fertilizers fell from their early 2022 high's. However, potash was the only one that didn't bounce off the bottom. Can potash continue to keep values low as others go higher?

- Grain prices keep falling – the farmer outlook seems like it gets worse by the day/week with grain prices falling. We are currently looking at corn prices not seen in a while? Are you feeling like you are in a spending mood right now? Guessing that answer is no. The further grain prices fall, the more demand slows/stops. The more demand slows/stops, the more unsold inventories build. The more inventories build, the more price pressure that builds.

- Global inventories/supplies look very flush - as stated in the last month review section, some large global buyers have been well ahead on their import flows...yet values have not budged as a result. Just how well supplied is the global potash market...or has it toed into the oversupplied territory? As long as inventories are/feel more than adequate, prices will have an anchor around its neck.

- Some of the largest global buyers have been ahead...will they stop buying? – countries like China have been well ahead of average on their potash imports. How long can that last? Is their demand truly that much bigger in a short amount of time...or are we about to be surprised/shocked by their stopping purchases? If they suddenly slowed or bowed out for a time, I would assume it would weigh on price ideas even further.

Where are the current potash/grain ratio values today

We believe that only looking at the flat price of either grains or fertilizer can be misleading:

-

Only selling grain can hurt you if fertilizer prices rise substantially

-

Only buying fertilizer can hurt you if grain prices fall

We look at the ratio "value" to get a better indication of where we are or how many bushels of X does it take to pay for 1 ton of fertilizer.

Would you rather:

-

Spend 120 bushels to pay for 1 ton of potash

-

Spend 60 bushels to pay for 1 ton of potash

When we compare the current ratio value against recent years, we start to see if we are high or low.

YOUR VALUES MAY LOOK DIFFERENT

This graph looks at the NOLA potash price vs the flat grain price. There are no logistics on either product. Your location will look different due to fertilizer logistical costs, grain basis, etc.

- Canadian rail strike threats - first on this list is easily the Canadian rail strike situation. Only because Canada is the world's largest exporter by far and if rail shuts down, so to do potash shipments. If we were to lose Canadian rail for several weeks or worse, it could have implications that have the market playing catch up for a while and that never bodes well for price ideas.

- Demand patterns of biggest global buyers - second is how world buyers continue to go forward. Does China continue its hot path on purchases? Do India/China actually get an annual contract in place or have they learned they can purchase spot from around the world? Sure feels like things are shifting globally...

- Grain values - third but by no means less important are grain values. I continue to hear from folks that farm economics...well, they suck. They are not good. They are causing folks to look at where they can cut on inputs to make next year more manageable. Typically, that means buyers take longer to step forward, it takes lower prices to create activity, it has folks considering delaying their fall applications until spring (with its own issues), etc. If high tides float all boats, then low tides ground them all out as well...

StoneX Ratio Calculation

The ratio calculation is derived from Bloomberg historical grains values as well as fertilizer values from StoneX, NPKFAS, and Argus.

The calculation is simply dividing the fertilizer price by each grain price.

All data was sourced from StoneX unless otherwise noted.