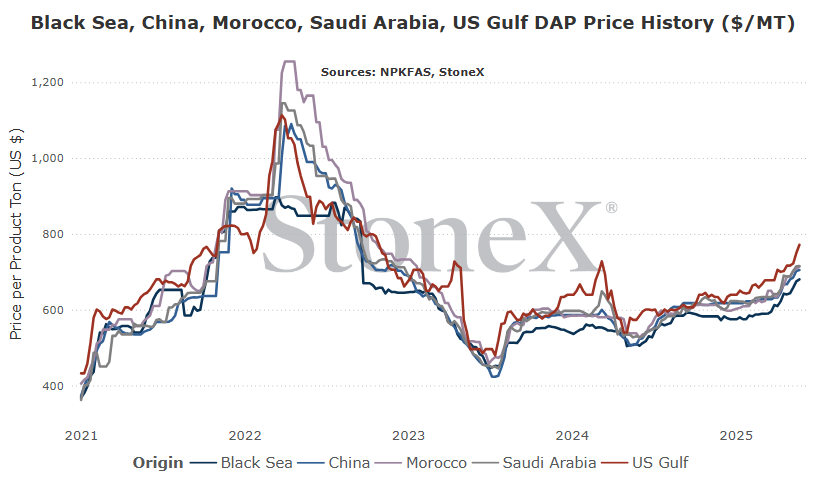

I will say this now and will say it going forward to eternity: these are the flat price graphs for each individual location. Your price where you are is going to be different. There are logistics. There is the cost of storage/interest/insurance/etc. These graphs should not be taken as "it shows the price at $700, why isn't my price $700". These graphs should be used to give an appreciation for price movements.

All values are in metric tons and USD currency.

Global

Prices are already sky high. I couldn't possibly think that they are going any higher.

Think again.

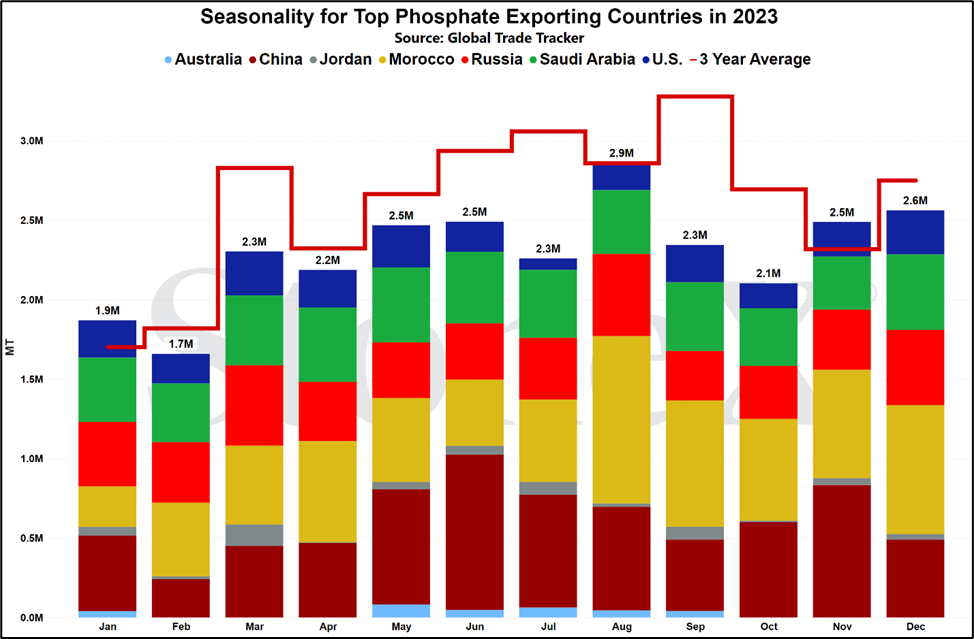

While we are still waiting for the final report from China regarding their phosphate export program, everything is pointing to a very disappointing 4M ton allowance. To put that into perspective, they are normally in the 9 - 10M tons range and hit 6.6M tons in 2024. 4M is so far below that...

Then there is demand. India just doesn't stop. They keep hoovering up tons like it is going out of style. Of course, global manufacturers are going to take advantage.

Until there is a change either from Chinese exports improving more than we currently think (4M tons) or India's buying patterns slow substantially, likely that prices continue steady to higher.

North America

Yes, I know. Demand is going to take a hit at these obscenely high prices.

I'm not here to play Dr. Feelgood. I'm here to give you the truth and the truth is the market doesn't care today if demand scales back. In fact, it is asking for the market to do exactly that.

North America is in a bad way when it comes to the top 5 manufacturing/exporting phosphate countries:

- China - U.S. tariffs

- Russia - U.S. duties

- Saudi Arabia - U.S. tariffs

- Morocco - U.S. duties

- U.S. - operating rates have been 58% for Q4 '24, Q1 '25, and Q2 isn't looking great

The market is essentially saying "I do not have enough supply to go around so I need to price some demand out of the market".

I truly do believe we are going to see demand destruction. The main corn belt region will probably proceed as normal. Moving to the outer corn acres, farmers there will react to a certain extent. Wheat country is going to hurt and will probably see demand down much more. Unfortunately, those moves will only help to balance the S&D and keep prices high.

For now, prices remain firm. N.A. values are not out of line vs the world. The supply side is simply too tight for prices to fall.

Now, if Chinese exports were to shock the market and jump substantially, the market would likely react lower but this appears to be a very low probability situation.

Unfortunately, high prices appear to be staying.

China's export program taking shape, and it isn't good for buyers

One of the things that I have been considering over the last month is "what is normal now"? In my mind, the period from 2016 thru 2020 is normal. Global fertilizer exports were sufficient. Values were at attractive levels for the farmer. Things flowed freely. There was little to no fear of product tightness or overvaluation.

This was especially true for phosphate. The world was led by Chinese export flows. When we look at the years surrounding 2019 for Chinese DAP/MAP exports:

- 2019 - 8.8M tons exported

- 2020 - 8.3M tons exported

- 2021 - 10M tons exported

Phosphate supplies were flush.

...then later 2021 happened. Russia started to make threats about its intention to invade Ukraine which is obviously followed thru with. This, along with rising grain values, caused a run on purchases that coincided with global fears that we would lose Russian exports. Inventories got snug and prices rallied hard. The result was that some countries started to scale back their exports flows.

China was very much a part of that:

- 2022 - 5.6M tons exported

- 2023 - 7.1M tons exported

- 2024 - 6.6M tons exported

2025 has not started well. January thru April cumulative exports have only reached 155K tons. That is not a typo. I checked that number multiple times. Only 155K tons for a country that was exporting 8 - 10M tons a year not long ago.

So, back to the question: what is normal today?

While Chinese exports have been down the last 3 years, the average has been around 6 - 6.5M tons. Well short of what they had been doing, but the market had been coming to terms.

Unfortunately, intel from the last months is pointing to the world needing to prepare for even less exports.

While many details from the Chinese government regarding their phosphate export program have been released (dates, destination allowances, governments ability to shut down exports at any time), the most important piece has yet to be said: tons to be exported. However, it appears that the market believes this number is going to fall far short of market hopes and only be around 4M tons.

Today, I presume the 4M ton estimate is true that is going to be bad news for buyers. The longer China stays out of the marketplace, the more supportive of prices it remains. While there are plenty of projects in the pipe, these projects will take time (think years, not months). Now, we could certainly see a situation where the Chinese surprise us and boost their export numbers...but I'm not holding my breath. The government originally lowered exports in an attempt to boost domestic supplies and lower domestic values. This program worked like a charm for urea and appears to be taking that lesson and applying it to phosphate.

Things can and will always change. If China suddenly returns, it would likely usher in a very strong bear market but for now, they are absent and values remain supported.

What does this mean for farmers?

Long and short, prices remain excessively high. Show me another market in the world where losing the leading supplier doesn't rock the price. Phosphate is unique in that only 5 countries control between 85 - 90% of global production and exports so losing the leader of those 5 is a massive hit that convinces the market prices need to be higher.

Some might be saying "well, I'll cut my demand and show them". Honestly, that is what the market wants to the tune of at least 4 - 5M tons per year. The S&D is out of whack with China's absence and the rest of the world cannot make up the difference near term. If the S&D is out of balance and supply is set, demand needs to change. Econ 101 type stuff. It is actively trying to shut down enough demand.

It sucks, I know...

India continues on its buying hot streak

I still maintain that the lack of Chinese exports is the cause of high global pricing. Losing the world's largest supplier in a market largely controlled by 5 countries has that effect. However, if no one was buying around the world, it would be hard for prices to rally. If there is no buying, there is no proof of appreciation.

This is where India comes in...

Quick backstory on why India is buying like they are. Summer of last year, the Indian government started to take an odd approach to phosphate. The way India works is that farmers do not see global price movements. Their phosphate price is set by the government and it does not change. However, as we all know, global prices do change. In order to keep imports flowing, the government sets subsidy programs that helps to bridge the gap between global pricing and domestic farmer pricing.

Over the last several years, this program has gotten EXPENSIVE.

"Why hasn't the government just went ahead and raised the farmer pricing?"

Well, India is a democracy. In fact, given their population size, you could say they are the largest democracy in the world. Of that working population, a quick google search (no, I didn't know this off the top of my head!) reveals that approximately 46% of this group is tied to agriculture in one way or another. If you are a politician, you like your position and want to continue getting reelected. Keeping fertilizer prices low is a solid way to lock up nearly half the voters...

Eventually, the subsidy cost becomes a strain on the government. That brings us to last summer. Global phosphate values were falling on the belief that Chinese exports were getting better. India made the decision to lower their subsidy rate in an effort to force global sellers to drop their price to sell India which would save them money. It started to work...until it didn't. Suddenly, Chinese exports started to get restricted again and global values started to rise.

Then India started to get behind on stockpiles.

That was nearly a year ago and to a certain extent, that is where we still are. India has been a very common and frequent buyer which has been helping show/prove to other manufacturers/sellers that phosphate values are holding/rising. Yes, the lack of Chinese exports is causing the high price, but India's buying patterns continue to prove it to the market.

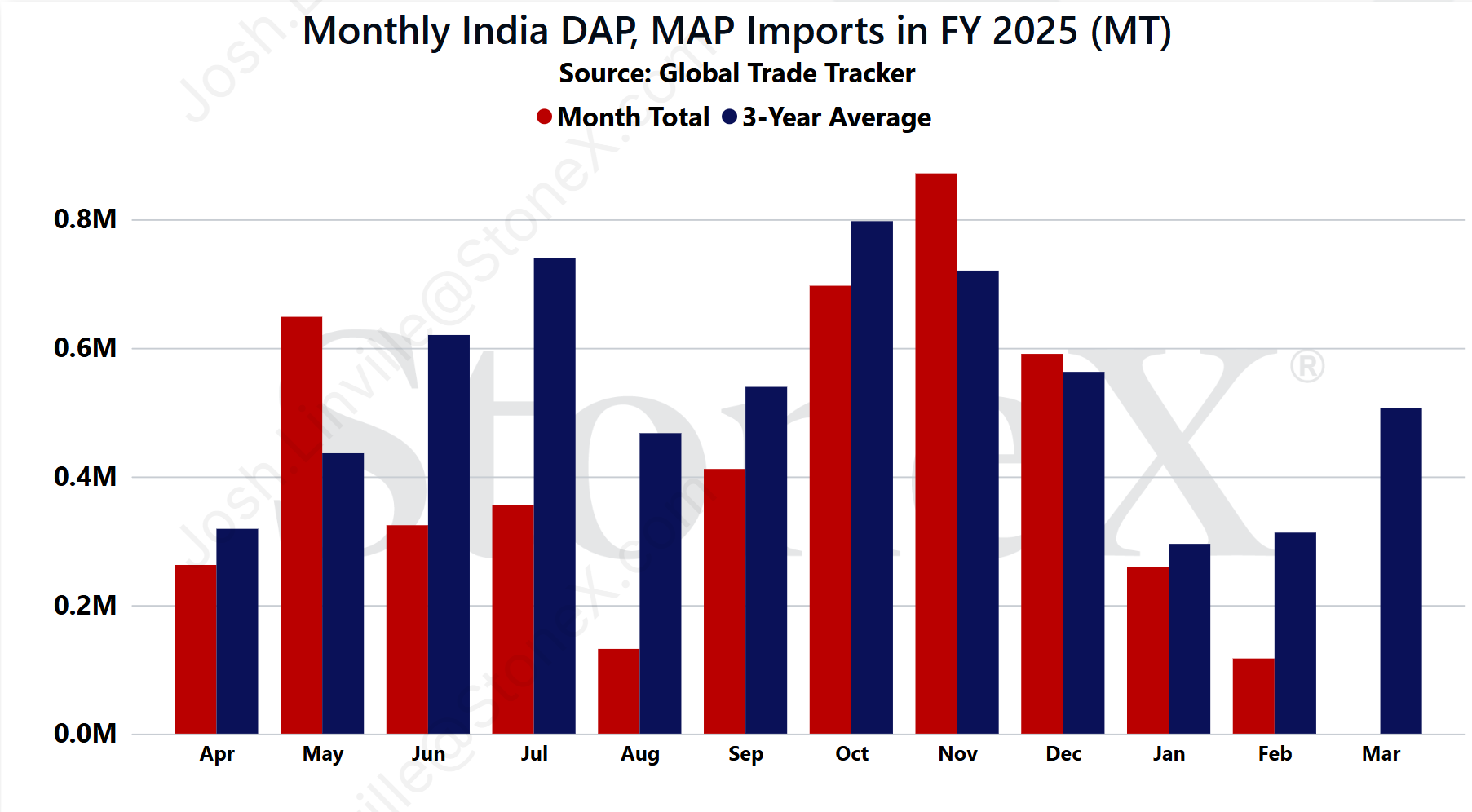

Unfortunately for those hoping that India will catch up and slow their pace, it doesn't look likely. Take a peek at the graph below. The 3-year average shows that their biggest import months are just in front of us. That does not guarantee anything but with them still appearing to rebuild stockpiles and monsoon starting early for them (good monsoon = solid fertilizer demand), hard to see their buying pace slowing.

What does this mean for farmers?

Even if Chinese exports were low as they are, if no one was buying product, that would put pressure on sellers to drop their price to find liquidity.

India's constant buying pace is keeping that from happening.

Not only are they locking up anything that might be building supplies, they are constantly proving to every seller in the world that prices are supported.

N.A. values RISING coming out of spring, hopes of summer reset low

I know, nothing about this year is normal but it is important to know what that is before diving into what is happening today.

As many of you probably already know, fertilizer prices spike during the spring season. Demand returns in a very big way and that pressures values higher as suppliers struggle to keep up. Then, once the rush of spring is complete, the market is forced to stare down a very long late spring/summer period where demand largely goes quiet. The result of the quiet demand period is that unsold supplies grow which can force sellers to drop their price to incentivize buyers to return. Once that "low" is set, values start to gain traction once again as we near fall.

This year is not going to follow any normal patterns.

As discussed in the previous two pieces, phosphate S&D is in a bad place. Supplies are very low due to the lack of Chinese exports. Demand is bigger than normal due to India, the world's largest importer, still rebuilding stockpiles. The result is that prices have been rising since the start of the year...and it doesn't look like it is done.

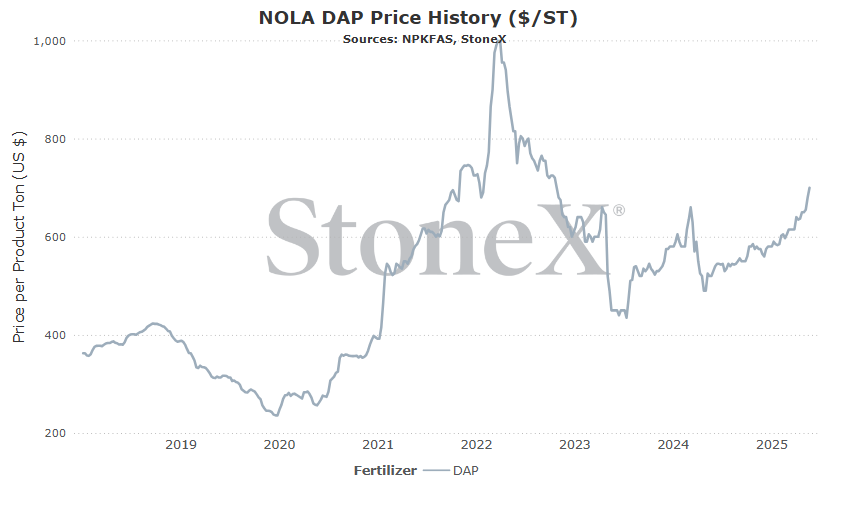

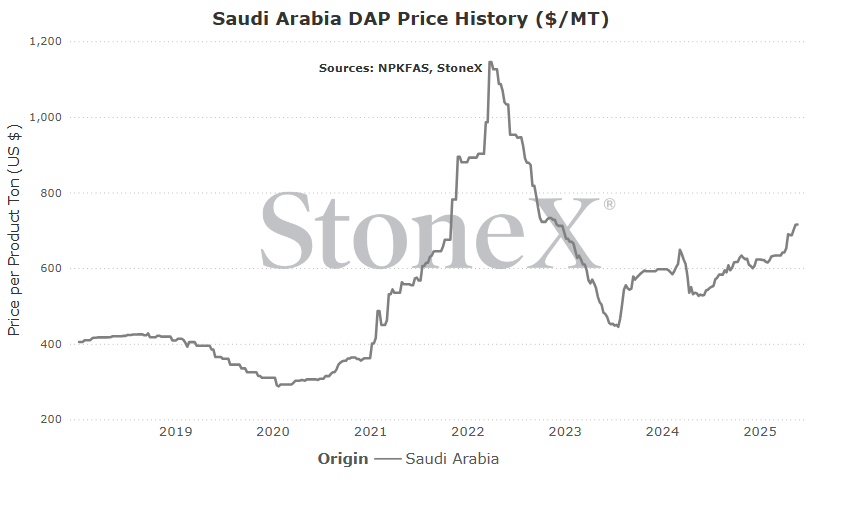

When looking at NOLA DAP values, we started the year with barges trading in the upper $500's. As expected, that price rose as we headed into spring and eclipsed $600 by February. April saw the largest part of spring phosphate demand over and that is normally when prices would start to hold and eventually start to slide.

That has not happened.

By later April, the market was starting to notice the complete lack of Chinese exports and was hearing the rumors that improvements were not coming. NOLA DAP values jumped to mid-$600's. Then, some suppliers started to get onto the story that retailers should start taking a layer of phosphate fill. Now, some of you might be irritated/pissed at that situation but honestly, it is one I agree with. I had told several of our retail customer a few weeks earlier that if I could disconnect from the high price fear, the phosphate fundamentals were pointing to the need to purchase a layer. Chinese exports, Indian buying patterns, duties, tariffs, poor U.S. production rates, expected large demand in looming fertilizer year, etc. However, I fell short of the advising to do so. The price scared me because I didn't think the farmer would pull the trigger (why would you?).

That is all a very long winded story that brings us to today. NOLA DAP values have now traded at $700...and it is hard to see values lower as we enter summer where prices normally dip.

Let's be clear, lower prices are still a possibility. There will be demand destruction at these levels. Farmers are likely to remain very cautious on buying and may wait until nearly the start of fall season. Retailers, without farmer buying, will be conservative on buying more layers. This could all combine to growing unsold positions which pressure prices. We could also see China shock the world and start exporting bigger flows. Unfortunately, both of these seem low probability from my POV. As long as China and India continue playing their game and some other things stay in place, it is very hard to see prices lower.

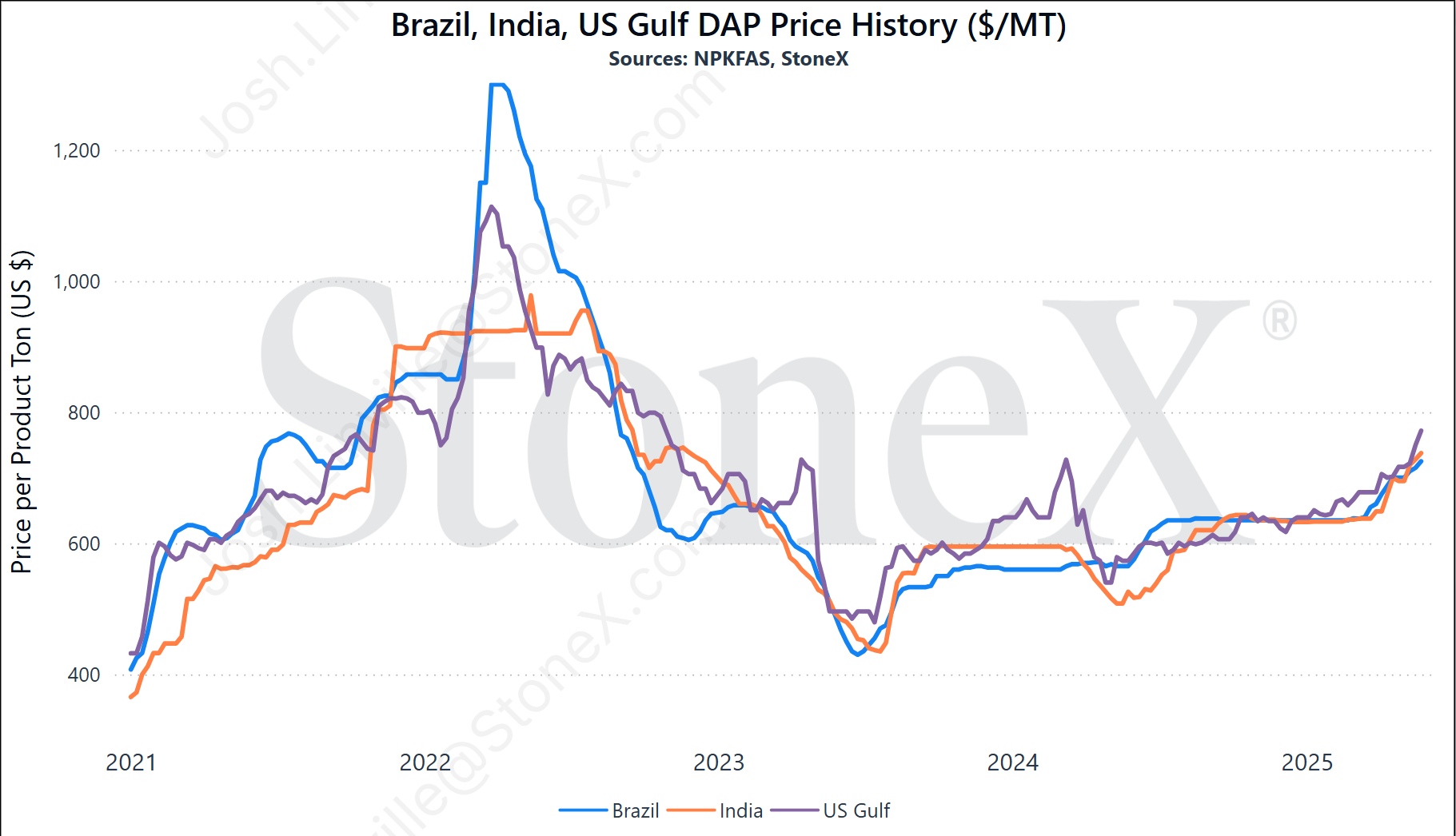

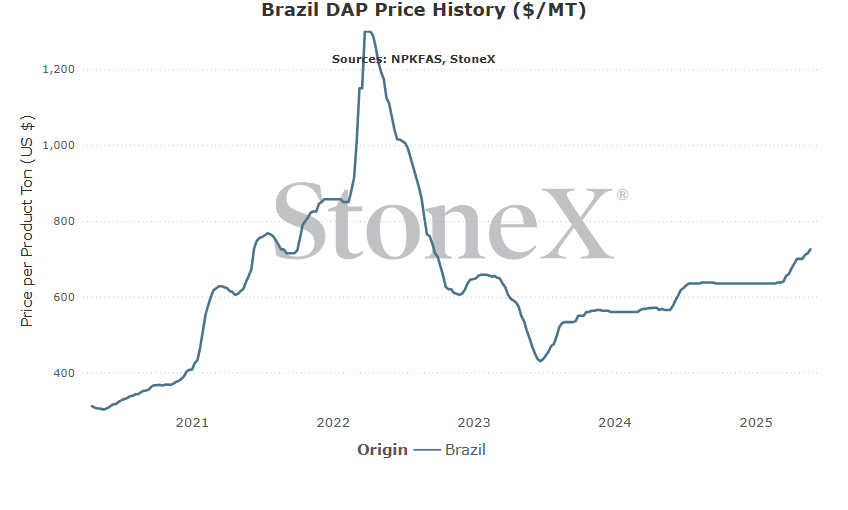

One last point. Some in North America might be saying that this is a domestic situation and that N.A. values are far above the world. Check the chart below which looks at Brazil/India/NOLA values (in MT). Yes, NOLA is a premium today, but is largely in line with the other 2 largest importers in the world. Yes, we are high priced but no, we are not a massive premium. We are trending right along with the world...

What does this mean for farmers?

Plain and simple, this means that when you start to see your first fall priced programs, they are going to be very high priced. They are going to appear even more high priced when compared against grains (more on that in the next section). This will be a hard decision. Do you pull the trigger on an outrageous price to ensure physical product is ready when you are? Do you drag your feet in hopes something happens in the coming months but supplies might be questionable under the perfect scenario (not saying supply outages, but could be snug)?

Unfortunately, the phosphate market is not doing you any favors this year...

Europe moves to further block Russian fertilizer, likely to hurt phosphate values

As the Russian invasion of Ukraine continues to drag on, tensions across Europe have been rising. The fear appears to be that Europe thinks if Russia takes Ukraine, they will not stop there. As a result, Europe is looking to put more economic pressure on Russia...in the form of blocking Russian fertilizer flows.

This will likely hurt European farmers.

As the graph below shows, there are millions of tons of urea, phosphate, and potash that flow from Russia into the EU. These are normal and efficient trade flows which helps farmers in the space find the best price possible.

Politicians view tariffs as a win for their country. By imposing a penalty on another country, they force that country to pay them money to participate in their economy. On the surface, they are right. Any tons that flow will have to see the check cut...but at least some of that check will be paid by funds received by European farmers who are forced to pay a higher price to get their supplies.

For phosphate, Russia still has plenty of sell options around the world, especially when considering how tight the marketplace currently is. Without China at normal rates, their buyers look to other sources like Russia. It shouldn't be a problem for them to find sales destinations.

So, ultimately, this move doesn't likely hurt Russia like the EU thinks that it will. If Russia was solely dependent on EU demand, it would be a different story but that is not the world we live in today. Today, this move is very likely to hurt EU farmers...

What does this mean for farmers?

If the EU goes ahead with these Russian penalties, it is very likely that EU farmers will see increases in their pricing. This would block efficient/low cost trade flows and force buyers/importers to consider secondary and more expensive shipping lanes. The importers are not going to eat that cost. The retailer is going to pass along that cost.

The farmer is going to pay the cost.

...for more uplifting messages, follow me at....!!!!

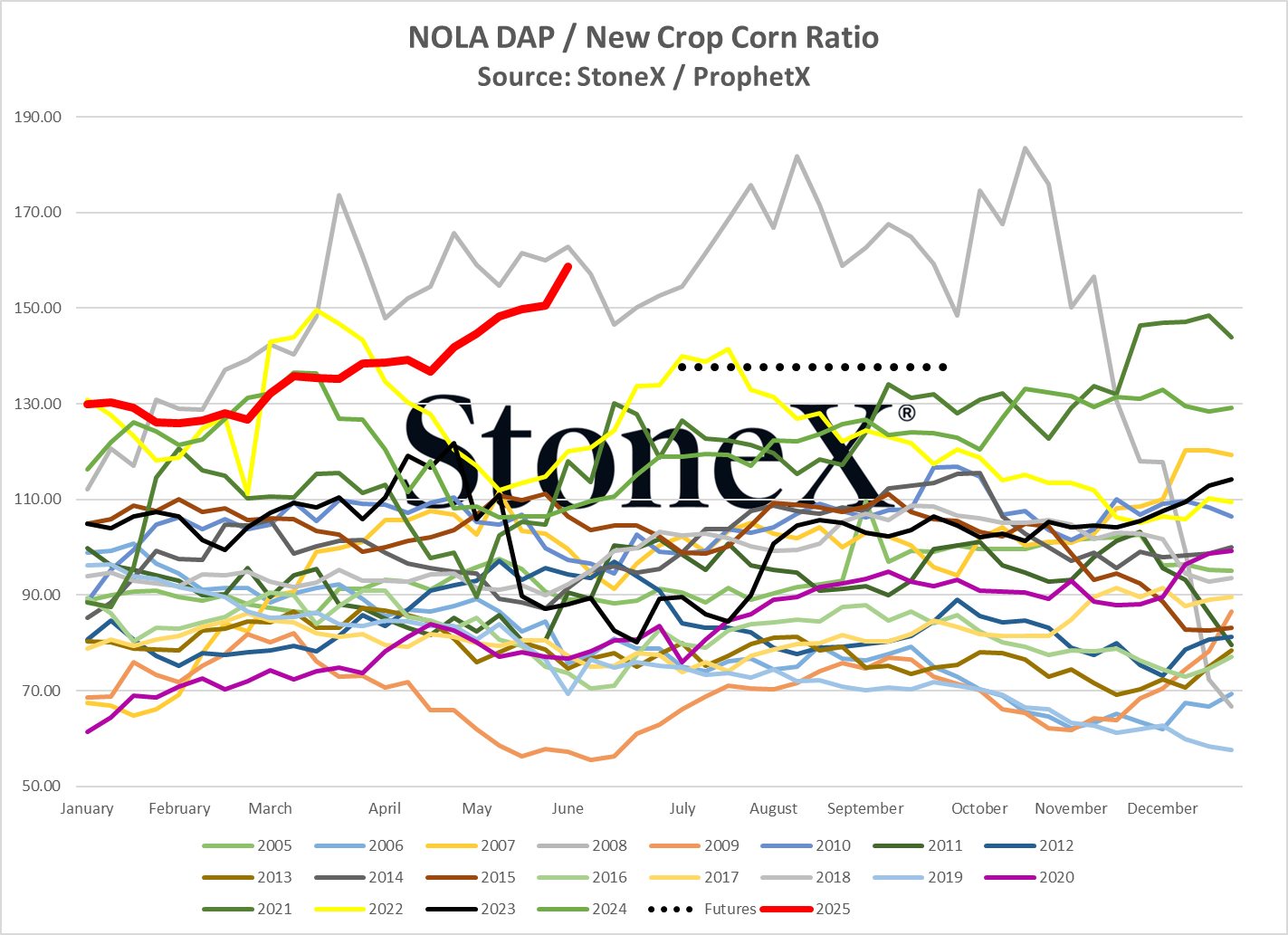

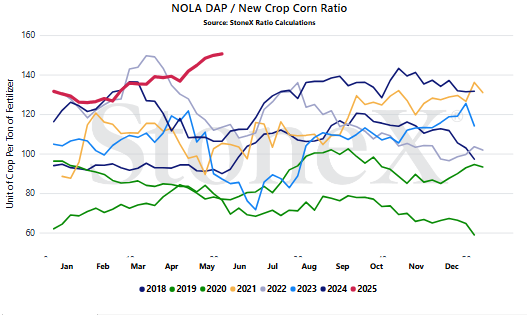

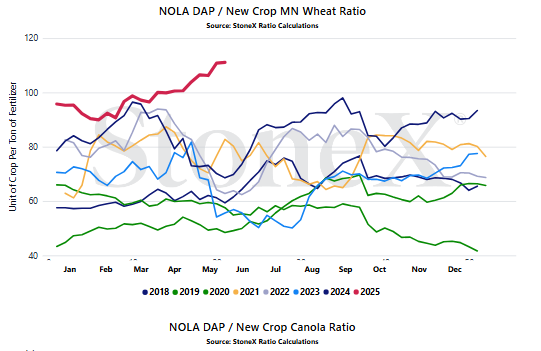

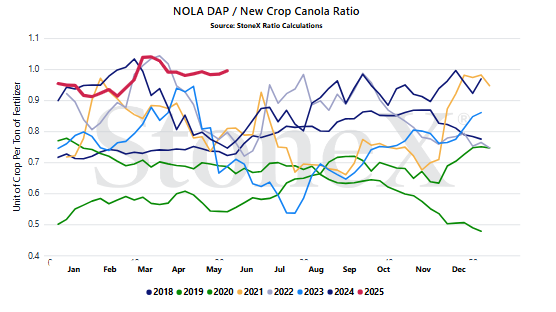

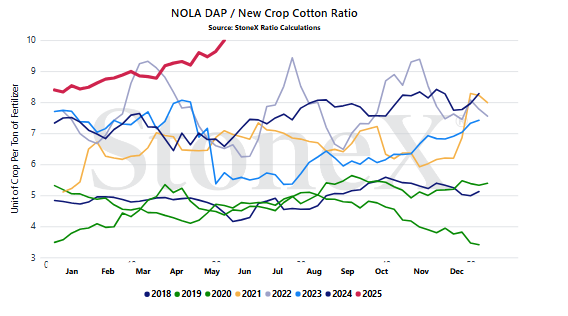

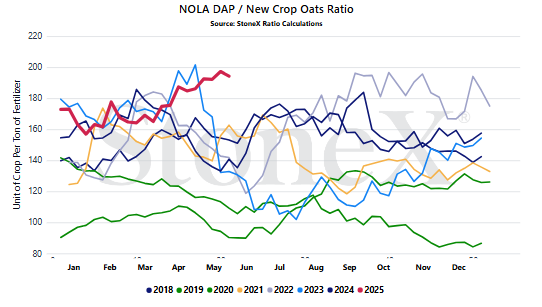

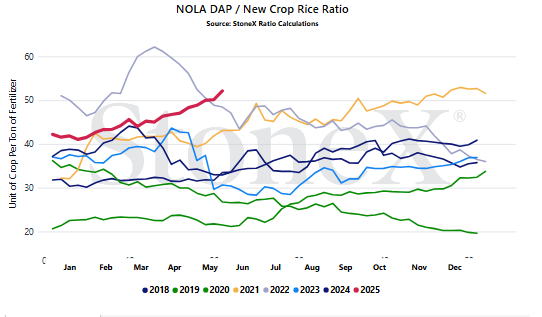

Phosphate demand questioned as phosphate rises to 2nd worst value ever vs grains

What will N.A. phosphate demand look like for the 2nd half of 2025?

That is the biggest question in my mind, and it is a question that I think will be answered differently based on where the farmer resides.

For starters, let's look at where we are.

- Most recent NOLA DAP barge traded $700

- December 2026 corn sits at $4.60 (I'm rounding up)

That puts the ratio relationship at approximately 152 bushels of corn to pay for 1 ton of DAP. As you can see below, that is the 2nd highest ratio relationship going back to 2005. It is actually the 2nd highest ratio relationship in history. But how do we shape up today to that period?

- 2008

- NOLA DAP - $992.50

- December 2008 corn - $6.09

- Ratio - 163

- 2025

- NOLA DAP - $700

- December 2025 corn - $4.39

- Ratio - 159

So today's ratio is slightly better than 2008, but with corn prices above $6, 2008 felt SIGNIFICANTLY better than today's situation. A $6 corn price brings in a lot more dollars for the farmer to help offset high input costs.

This takes us back to the question of what demand looks like. Frankly, we expect it to be lower. Some farmers will reduce their application rates. Some farmers will delay their applications in hopes of lower prices ahead. Some may have little choice and be forced to skip phosphate this year, regardless of yield destruction.

I also believe this answer will vary widely based on the territory. Those farmers in the core corn territories are much less likely to reduce their application rates. They may not like the price, but they also know they need to maximize yield potential and they raise enough bushels to justify it. As you get away from the corn regions, the yields fall off and it makes it harder to justify the costs. Rates should start to lower. As you move into tougher areas like the southern plains, it starts to get really hard. There is a reason all the country songs talk about hard living in red dirt states!!!! Here it is simply going to come down to math. Not enough income to justify it.

Don't get me started on wheat areas. You guys cannot catch a break.

All in all, these values are excessively high on their own and against grain values. The natural tendency will be to cut back, but a word of caution. Make application rate cuts based on solid math, not on emotion. The best decision may be to lower or skip this year. If the finances prove that, then that is the smart approach. My fear is some will make that decision out of anger. Farming is hard enough already...

What does this mean for farmers?

This means very hard and expensive decisions.

Phosphate prices are extremely high from a flat price perspective.

Phosphate prices are extremely high from a grain relationship perspective.

This is going to be a decision where emotion will want to weigh in.

Do not let it.

N.A. phosphate supply situation remains dire, very little hope of a "summer reset"

I've spent a lot of time in the pieces above pointing out the global phosphate situation, high prices, high ratio values, etc. Here, I want to dive a bit more into why U.S. / Canadian farmers are struggling even more.

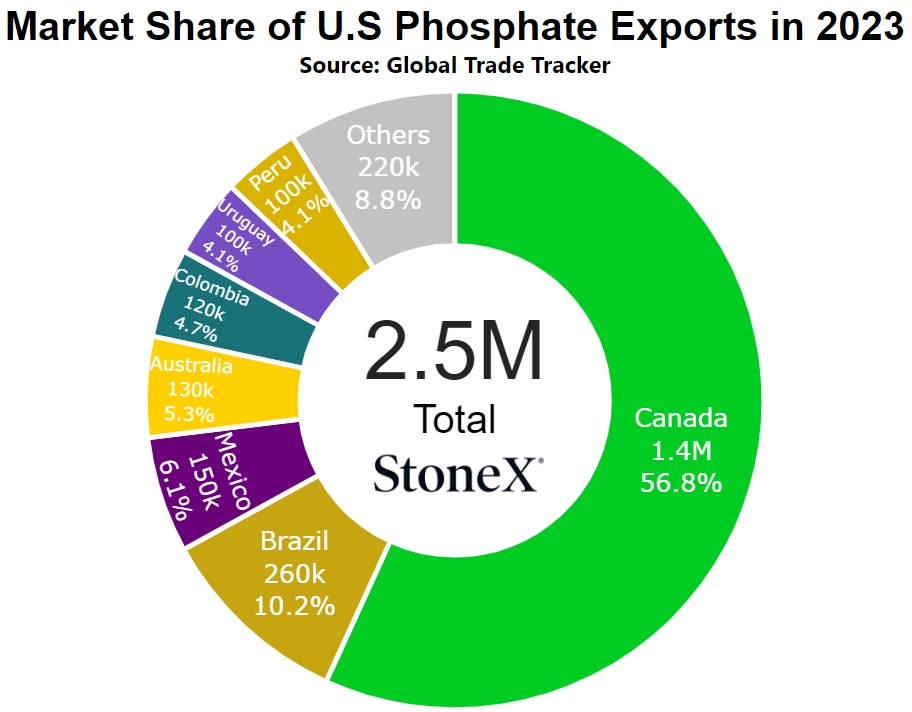

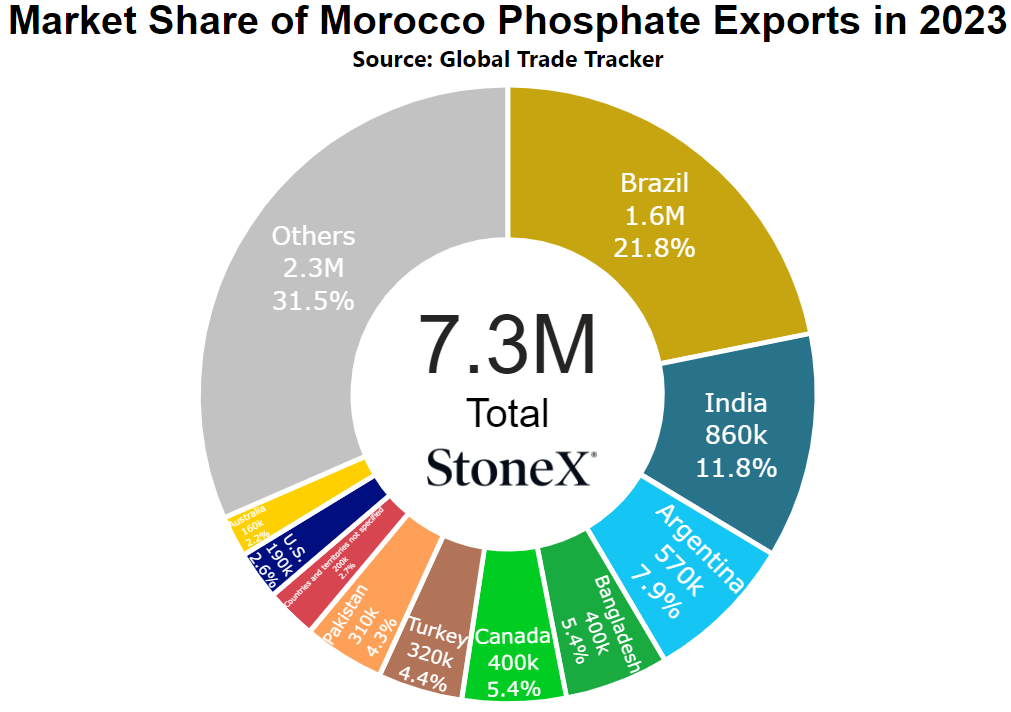

If you have heard me speak, you know I talk at great lengths about how condensed the global phosphate market is. 5 countries control approximately 85 - 90% of production and exports. That is what has made the China situation so dire.

Let's look at those 5 countries and how the U.S. is operating with them (and by proxy, it affects Canada as well):

- Morocco - U.S. imposed counter vailing duties on their phosphates in spring '21

- China - U.S. imposed tariffs on Chinese phosphates during 1st Trump administration

- Russia - U.S. imposed counter vailing duties on their phosphates in spring '21

- Saudi Arabia - U.S. imposed 10% tariffs earlier this year

- U.S. - Q4 '24 and Q1 '25 phosphate operating rates have been record low at 58%

That's it. That's the list. Not a very positive look.

Unfortunately, it does not look like this will change. The duties and tariffs appear to be remaining steady with no signs of falling off. That is going to block the majority of import options to help backfill inventories.

Fortunately, NOLA DAP values have stayed in line with other major global buyers like India and Brazil. This is a situation that can and may still see NOLA skyrocket to a big premium vs the world, but that has not happened as of late.

All of this continues to point to our belief that the current market is not likely to see a summer phosphate price reset. I would love to see it and there are still paths to that goal, but they are far and few between and are heavily outweighed by the bullish factors.

What does this mean for farmers?

Like most everything else I have talked about, this further presses the idea that phosphate values will struggle to reset lower. Massive demand destruction and/or a huge return to normal Chinese exports could send this market spiraling but both of those are not likely today.

Today, taking a step away from the anger I get when looking at these prices, the fundamentals are pointing to supportive markets.

...sorry...

NOLA/New Orleans, Louisiana DAP price comparison

Number 5 global exporter in 2022

Price comparisons

Vs 30 days ago - 8% or approximately $50 higher

Vs 90 days ago - 16% or approximately $95 higher

Vs 6 months ago - 22% or approximately $125 higher

Vs 1 year ago - 35% or approximately $180 higher

U.S. Midwest Average (using multiple points across Midwest) price comparison

Vs 30 days ago - 6% or approximately $38 higher

Vs 90 days ago - 11% or approximately $71 higher

Vs 6 months ago - 14% or approximately $85 higher

Vs 1 year ago - 19% or approximately $112 higher

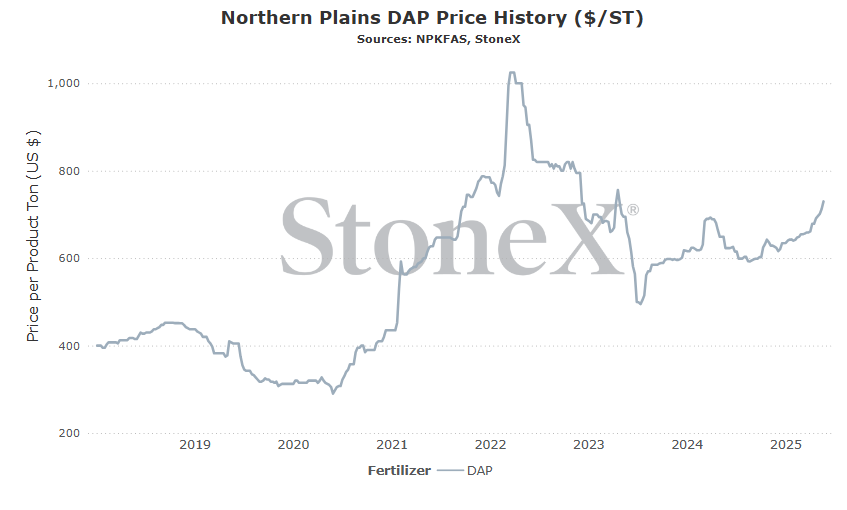

U.S. Northern Plains Average price comparison

Vs 30 days ago - 6% or approximately $39

Vs 90 days ago - 11% or approximately $75 higher

Vs 6 months ago - 17% or approximately $104 higher

Vs 1 year ago - 17% or approximately $108 higher

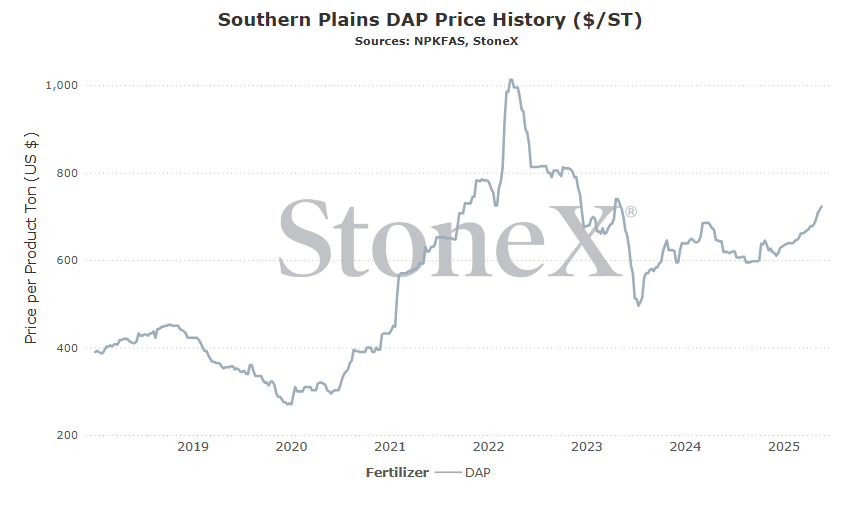

U.S. Southern Plains Average price comparison

Vs 30 days ago - 6% or approximately $40 higher

Vs 90 days ago - 11% or approximately $71 higher

Vs 6 months ago - 17% or approximately $104 higher

Vs 1 year ago - 17% or approximately $104 higher

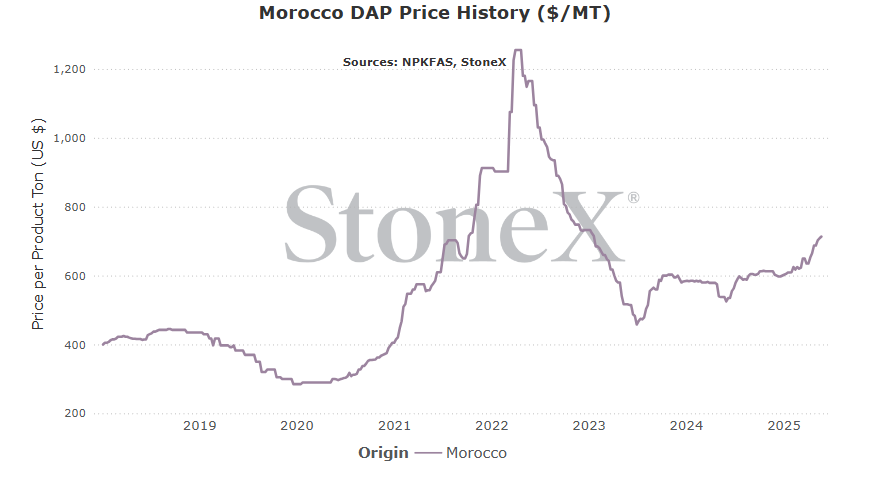

Morocco DAP price comparison

Number 1 global exporter in 2022

Price comparisons:

Vs 30 days ago - 4% or approximately $26 higher

Vs 90 days ago - 15% or approximately $94 higher

Vs 6 months ago - 16% or approximately $101 higher

Vs 1 year ago - 33% or approximately $176 higher

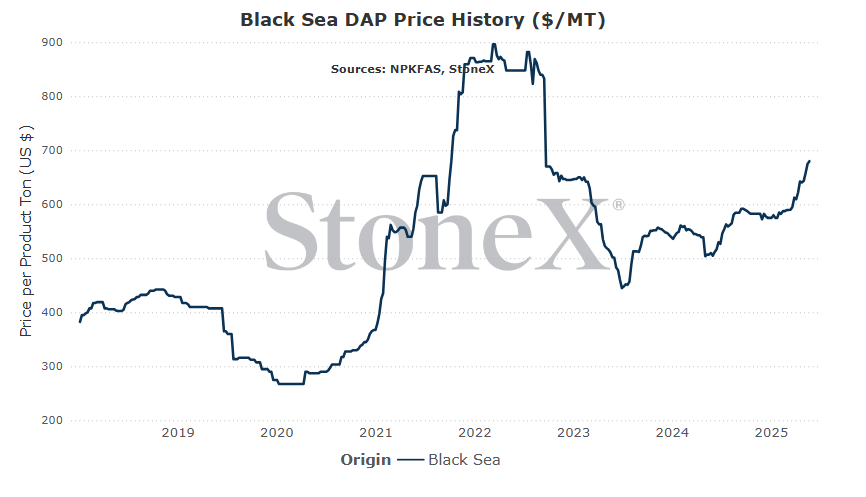

Black Sea DAP price comparison

Number 3 exporter of DAP/MAP in 2022

Price comparisons:

Vs 30 days ago - 6% or approximately $40 higher

Vs 90 days ago - 15% or approximately $91 higher

Vs 6 months ago - 17% or approximately $98 higher

Vs 1 year ago - 33% or approximately $170 higher

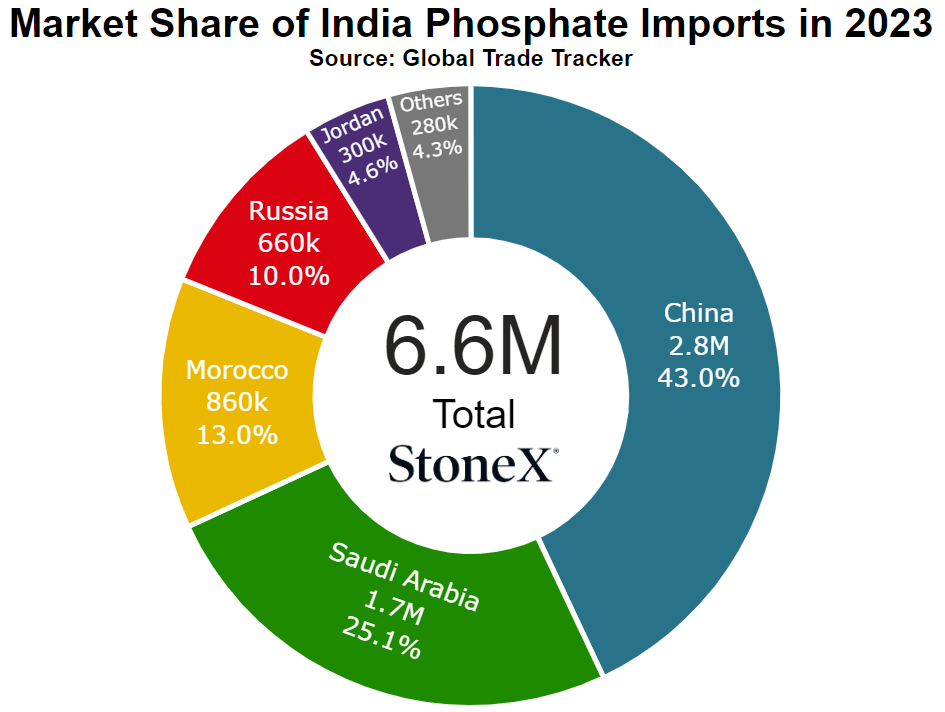

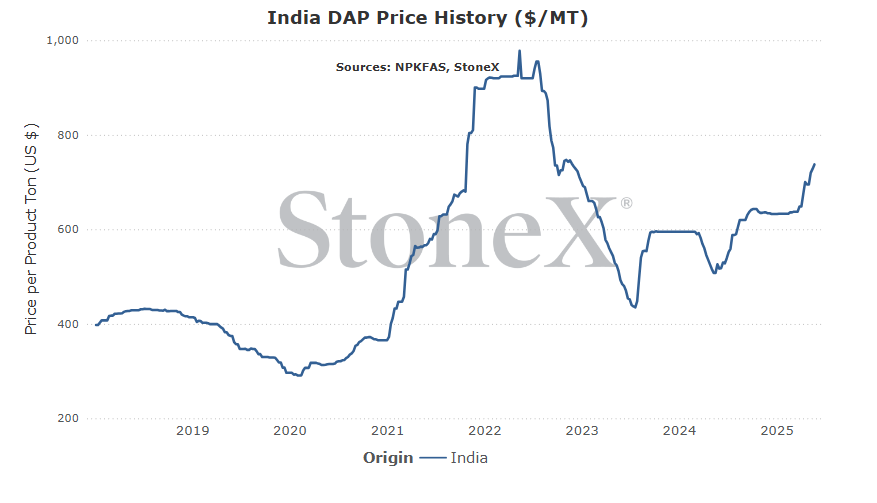

India DAP price comparison

Number 1 global importer in 2022

Price comparisons:

Vs 30 days ago - 6% or approximately $43 higher

Vs 90 days ago - 16% or approximately $102 higher

Vs 6 months ago - 16% or approximately $102 higher

Vs 1 year ago - 40% or approximately $212 higher

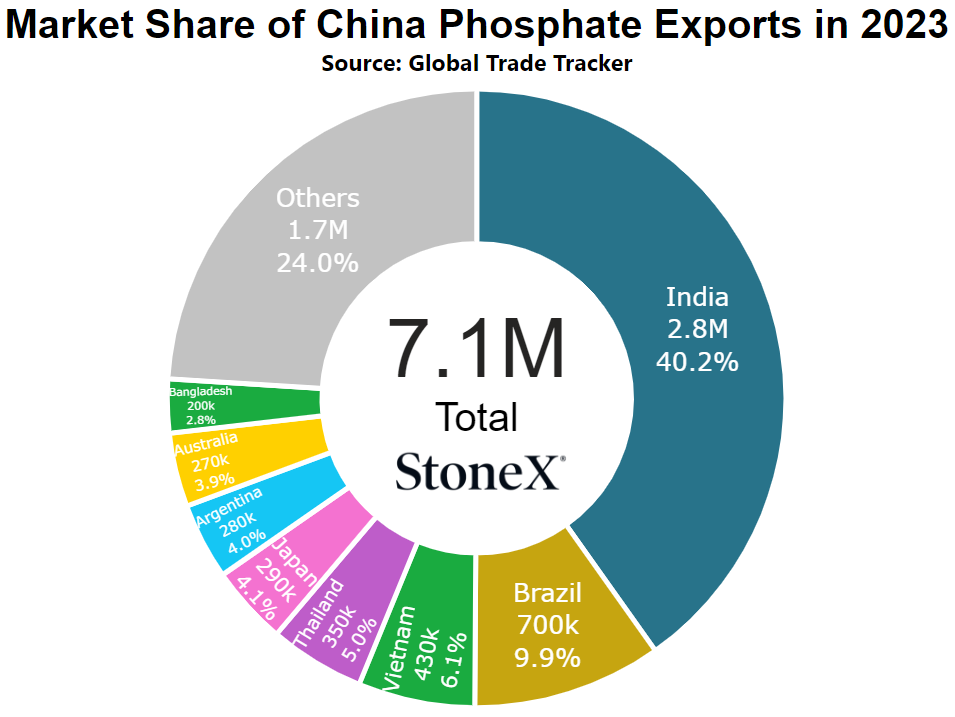

China DAP price comparison

Number 2 global exporter in 2022

Price comparisons:

Vs 30 days ago - 6% or approximately $38 higher

Vs 90 days ago - 12% or approximately $78 higher

Vs 6 months ago - 14% or approximately $88 higher

Vs 1 year ago - 39% or approximately $198 higher

Saudi Arabia DAP price comparison

Number 4 global exporter in 2022

Price comparisons:

Vs 30 days ago - 4% or approximately $28 higher

Vs 90 days ago - 13% or approximately $82 higher

Vs 6 months ago - 17% or approximately $107 higher

Vs 1 year ago - 35% or approximately $186 higher

Brazil DAP price comparison

Number 2 global importer in 2022

Price comparisons

Vs 30 days ago - 4% or approximately $25 higher

Vs 90 days ago - 14% or approximately $87 higher

Vs 6 months ago - 14% or approximately $90 higher

Vs 1 year ago - 28% or approximately $160 higher

- China starts exporting phosphate, domestic Chinese values start to rise, and the government puts a stop to exports – this is a very real fear in the marketplace today. As I write this, the expectation is that China will allow up to 4M tons of DAP/MAP exports. For reference, China normally exports 9 to 10M tons in a year and only exported 6.6M tons last year. Unfortunately, there is no guarantee that they hit the 4M ton mark. If the government sees domestic inventories getting to low or worse, start to see domestic Chinese phosphate values rise too much, they can hit the kill switch and stop exports well short of 4M tons. The world is already struggling with the hope of 4M. Less would be devastating.

- India continues to buy at this pace – while the lack of Chinese exports is causing the situation which is allowing global prices to rise, India's near constant buying pattern is proving it. India continues to work to rebuilt their stockpiles to ensure adequate supplies for their farmers who have a history of not being happy if stockpiles get too low. This has meant their being in the news buying blocks of DAP several times a week. Every time they buy, it is more proof that global values are still holding high. Each time they pay more for DAP, global suppliers point to it and effectively say "if they are buying it, you should to".

- The retail/farmer sector continues to buy into the fill/fall programs – we have already seen the first push for retailer fill programs and we are not even into June. Notice I didn't say "incorrectly". The fundamentals support the push and a lot of the factors are international, not domestic. From our vantage point, retailers took a reluctant layer. It was less a purchase out of fear that prices would rally and more a fear of buying to ensure physical product was on hand for their farmers. Now, with a layer in hand and very little chance of farmer participation based on the market today, when will the next layer be secured? If that next round happens sooner than later, do not be surprised for prices to continue higher.

- China surprises the world and lifts the cap on export flows – let me start by saying this is a very low probability but very high impact factor. I am not expecting it to happen, but the chance isn't 0%. If China exports 4M tons and sees that domestic inventory levels are still more than sufficient for domestic demand and that domestic values have not reacted, they could decide to up their allowance. If the world suddenly hears that a total of 6 or 8M tons will be exported, that changes the market and will have long positions running for cover.

- Retailers/farmers largely reject any further purchases due to high price – unfortunately, it appears that retailers went ahead and locked in the first layer of summer fill which will give suppliers/manufacturers a sales book that will keep them comfortable for a time. I do not blame the retailer one bit here. Given the global phosphate market situation and some of the events of this spring, they likely fear a scenario where they cannot find physical resupply. They would rather have high priced tons for farmers than no tons at all. However, with this layer in place and a decent chance that farmers will reject the price ideas, that next layer may take a long time to happen. Long enough and prices could start to deteriorate to find sales.

- Actual demand destruction outpaces expectations – today, the global and domestic phosphate markets are trying to destroy demand. With India rebuilding supplies and China cutting back exports, the S&D is out of balance. The market looks at supplies and realizes that it cannot do much to change it near term. That leaves demand. To balance the S&D, demand needs to be destroyed...but can that be overdone? Absolutely. If we start to find that demand has been more destroyed than expected, you could see a knee jerk reaction with prices falling to bring that demand back.

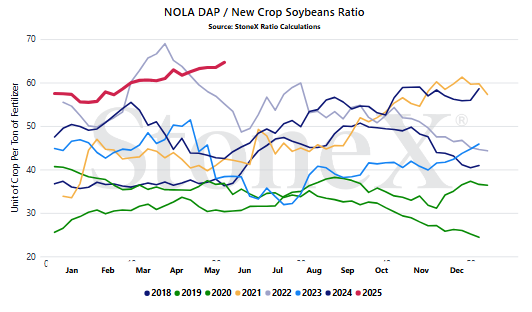

We believe that only looking at the flat price of either grains or fertilizer can be misleading:

-

Only selling grain can hurt you if fertilizer prices rise substantially

-

Only buying fertilizer can hurt you if grain prices fall

We look at the ratio "value" to get a better indication of where we are or how many bushels of X does it take to pay for 1 ton of fertilizer.

Would you rather:

-

Spend 150 bushels to pay for 1 ton of DAP

-

Spend 80 bushels to pay for 1 ton of DAP

When we compare the current ratio value against recent years, we start to see if we are high or low.

YOUR VALUES MAY LOOK DIFFERENT

This graph looks at the NOLA DAP price vs the flat grain price. There are no logistics on either product. Your location will look different due to fertilizer logistical costs, grain basis, etc.

- Easily the biggest focal point is China's export program - everyone, I cannot understate how important China's export programs are for the world. Keep in mind, their normal flows are between 9 and 10M tons per year. 2024 saw them exporting a disappointing 6.6M tons. Market continue to believe this year will only see 4M tons. That is a far cry from normal flows. That is 5 - 6M tons missing from the global S&D. 4M tons may be the number on the mark. However, if they start exporting and domestic values rise too much/quickly, that number might be reduced which would hurt the world even more. On the flip side, if they export 4M tons, do not see any reaction from domestic values, and continue to be pressured by exporters, they could increase to 6 or 8M tons which would likely set the market on its butt. All eyes need to stay on China.

- Next in line is India's purchase pace - if China is causing the global phosphate situation, India is helping to prove it constantly. Everyone knows that their stockpiles had shrunk to very low levels that had to be rebuilt or face the wrath of their farmers. That has caused the current situation where India is buying blocks of tons a few times a week. Every time they purchase a layer at the same or higher price, that emboldens the rest of the market. Other suppliers/manufacturers can point to India and basically say "if India can buy it, so can you". It gives them a very powerful negotiation tool. If India would slow/stop their purchase rate, things could quiet and we could see pressure mount.

- How will N.A. retailers and farmers approach high priced phosphates? - retailers across North America continue to be pressured to buy a layer of phosphate for the fall run. It is an impossible decisions given the high price. This is the 2nd highest/worst grain to phosphate ratio in history. Farmers are likely to shun the high price if brought the opportunity to buy. That means the onus is on the retail sector. On the one hand, they do not want to buy and support these values. On the other hand, they have to fear tight supplies. Farmers might get made about high prices, but they will never forgive a retailer who doesn't have product. Right now, it looks like the bulk of retailers took a layer which will give manufacturers several weeks to be comfortable on sales. How the next layer is approached will be interesting.

- How will the U.S. fare given a poor supply outlook? - the U.S. is in a bad place. Globally, 5 countries control approximately 85 - 90% of phosphate production and exports. The U.S. has either placed duties or tariffs on 4 of the 5. The 5th is the U.S. itself, and operating rates for Q4 '24 and Q1 '25 were record lows. Q2 '25 doesn't look much better. All to say that inventories are going to be extremely tight on top of a global situation that is extremely tight. Bad combination.

StoneX Ratio Calculation

The ratio calculation is derived from Bloomberg historical grains values as well as fertilizer values from StoneX, NPKFAS, and Argus.

The calculation is simply dividing the fertilizer price by each grain price.

All data was sourced from StoneX unless otherwise noted.