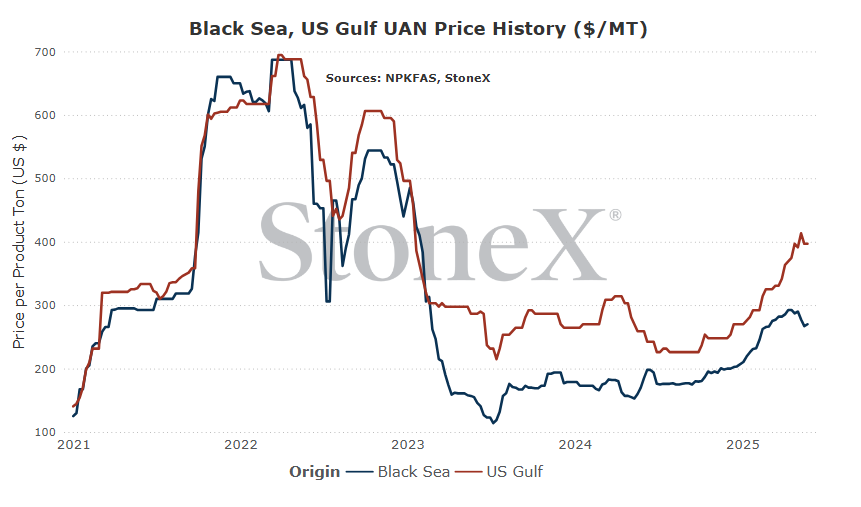

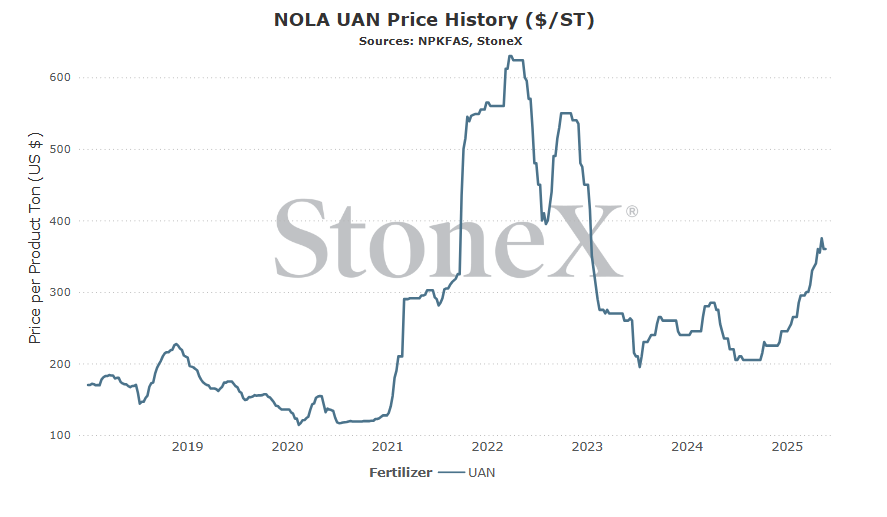

The intention of the below graphs are not to use to say "my price should be X based on this graph". These prices are derived from an FOB price point average. The intent is to show major global price movement trends. Your values will likely have significant basis difference (similar to your local grain price being different than the traded market price).

This graph is labeled as MT in USD currency.

Trinidad production suffers due to low natural gas supplies...again

Trinidad's natural gas flow struggles continue to upend global nitrogen markets.

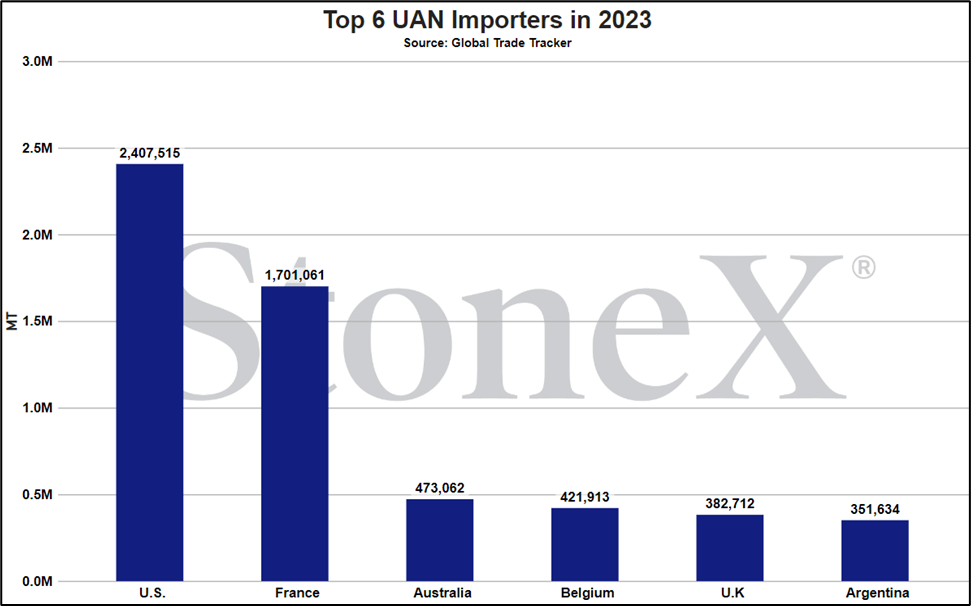

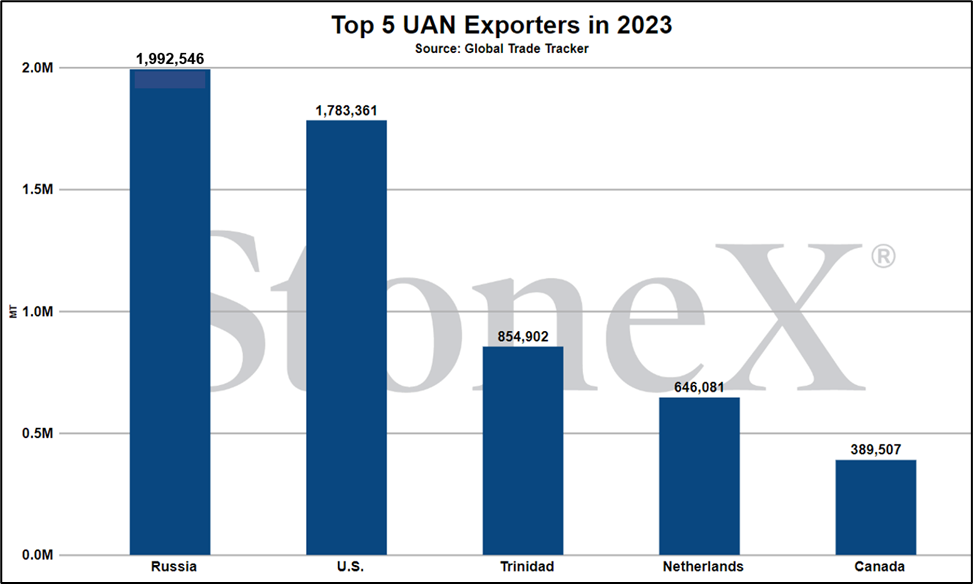

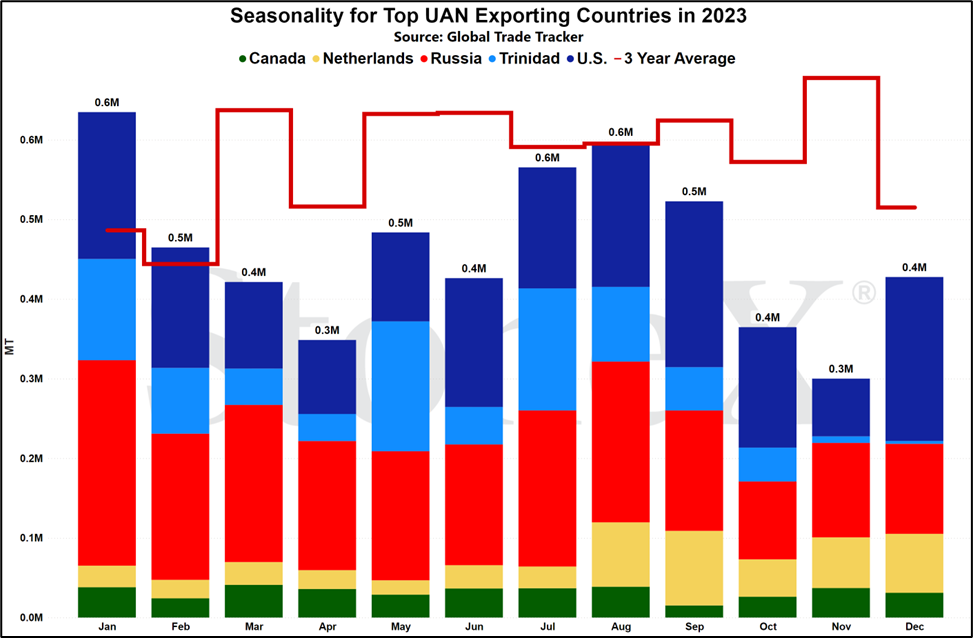

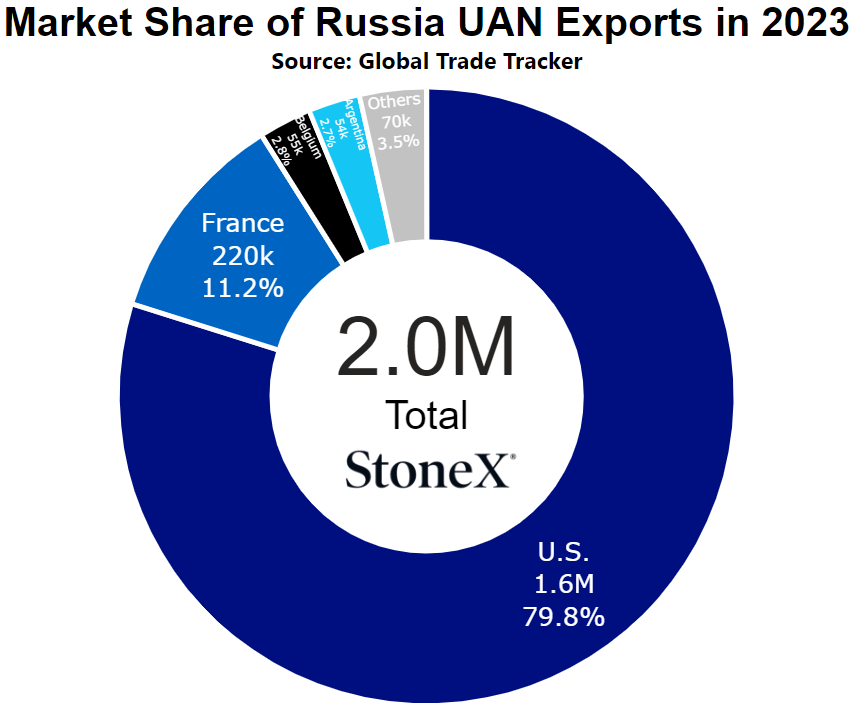

For years, Trinidad's natural gas supplies have ebbed and flowed. The result has been that nitrogen manufacturers have had to match this flow with production increases and decreases of their own. As the 3rd largest UAN exporter in the world in 2023 (just about ready to release the 2024 numbers, but not quite there), their production issues are felt around the world:

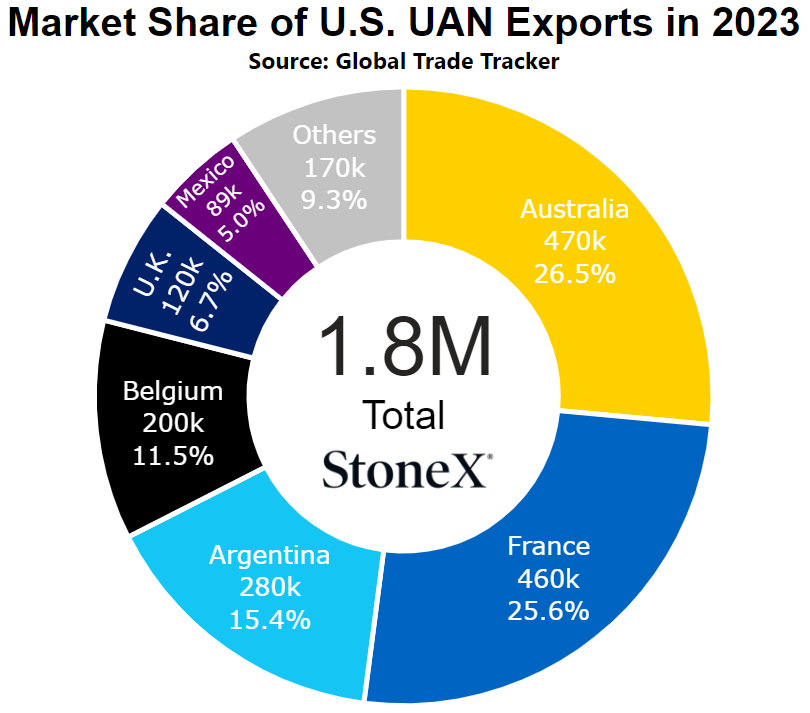

- Russia - 2M tons exported 2023

- U.S. - 1.8M tons exported 2023

- Trinidad - 855K tons exported 2023

Fortunately, the long range outlook for Trinidad appears a lot more stable. The country has been pushing to increase natural gas production by opening previously untouched ocean territories and has been willing to partner with other countries to make these developments happen.

Unfortunately, it takes time to develop these systems...lots of time.

For now, natural gas continues to see inventories and flows somewhat unreliable as the last month has proven. Nitrogen producers have once again had to lower their production rates and that has weighed heavily on available UAN supplies.

Our outlook remains that their production will largely normalize in the coming months which could help stabilize UAN values, but there are no guarantees.

What does this mean for farmers?

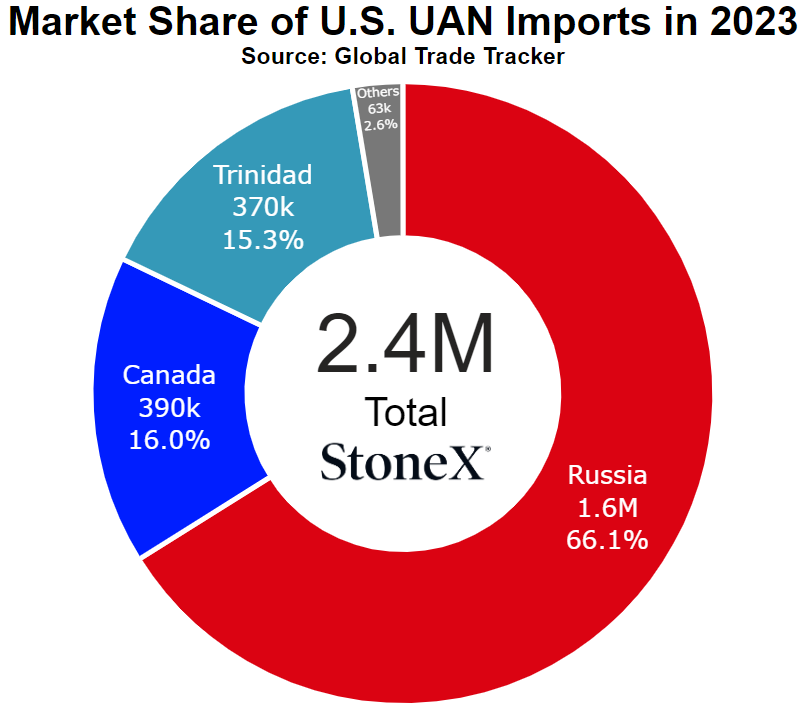

For European farmers, this mean losing access to one of the larger providers of UAN that has helped to backfill the loss of domestic production. This puts you more in direct competition with farmers in North America (since you are trying to grab tons from there), as well as western Australian farmers (who rely almost solely on U.S. produced UAN.

For North American farmers, this means a reduction in one of the larger U.S. UAN importers. N.A. inventories are already extremely tight as April and May have proven. It is very likely that fertilizer year 2026 (starts July 1) will begin with extremely low inventory levels. That is already supportive. Losing access to some of one of the larger importers only makes it worse.

For Australian farmers, if Trinidad continues to struggle, that could make N.A. values push higher. If N.A. values push higher, so too will Australian values as nearly all UAN that gets imported comes from there right now.

N.A. UAN supplies loosening in approach to June, still VERY tight

That was not the most fun couple months that the N.A. UAN market has ever had.

The story that the industry had been crying wolf about for years finally happened. A perfect storm of issues finally came together to make it nearly impossible to find product:

- Low starting inventories for the fertilizer year

- Production hiccups in the fall reduced supplies

- Production hiccups in late winter due to extreme cold reduced supplies

- Imports were lower than expected

- Exporters were much bigger than expected

- Demand grew as corn acres rose

- Spring came and never really slowed down

The result is that retailers and farmers alike struggled to find additional supplies during the months of April and May.

Fortunately, as we get set to start the month of June, supplies are loosening up lightly. I still doubt you would find anyone will to say that supplies are plentiful, but instead of only finding a truckload or two, folks are now saying they can find 500 - 1,000 ton blocks. Yes, they are very expensive...but they are available.

My POV is that this will continues through the month of June and into summer. Hopefully, as it improves, so too will values but I wouldn't count on it. The sell side of the industry still realizes how tight things are and how much demand is still in front of them. No doubt they will try to capture as much margin as possible.

Still, conversations with your retailers will hopefully improve in the coming days/weeks.

What does this mean for farmers?

N.A. inventories becoming more available have seen some pockets showing a slightly better price...but not substantial. Values are still very high and inventories are still very tight and will likely remain that way through a chunk of June.

While far from the saving situation we would all like to see, this is still good news for retailers and farmers.

First stab at summer price reset expectations

Whenever I take my stabs at what to expect for summer UAN price resets, I normally start with urea. Urea is a much larger produced product globally and is produced by FAR more companies/countries than UAN. As a result, urea is a much better indicator of the market as it acts much more like a commodity. While I wouldn't say UAN is a specialty product, it has a much tighter grip on it by manufacturers.

The reason I bring this up is that my urea outlook/forecast is a bit more bold than many in the market. For reference, the price difference between a strip of Q3 '25 NOLA urea and my summer urea physical price reset is that mine is around $40 lower. There have been a couple chuckles at my bold and cheap claims. I am VERY much on the other side of the ship!!!!

Still, when I look at the fundamentals of the current urea market, it points to lower values. That is what I'm going to stand behind until the market tells me differently.

All that said, my current UAN summer reset is that we see values only getting within $50/ton of 32% from last years lows...

Yeah, it is going to be expensive.

So why the big jump over last year?

- Starting fertilizer year 2026 (July 1) inventories will be very low - after this spring for N.A., I believe we will either have near record low starting inventories or extremely low starting inventories. The difference lies on just how much demand switched away from UAN. Regardless, the market is going to be empty...and that is a lot of space for manufacturers to fill.

- Trinidad production issues will keep inventories snug - Trinidad continuing to struggle tightens global supplies and supports global values. North America will not be immune.

- Fears of losing Russian produced tons should keep prices elevated - Canada blocked Russian fertilizer flows long ago, but has been fortunate that the U.S. never took that step. While it would be more efficient to have Russia shipping directly to Canada, the U.S. can push some of its tons north while receiving Russia. That has helped to boost available supplies and creates a competitor for domestic manufacturers. Word of caution. If President Trump gets tired of Putin's games around peace with Ukraine, we could see revenge tariffs be put into place very quickly. If the U.S. loses these tons, UAN goes to a much worse place.

- Fears of U.S. tariffs keep another layer of uncertainty in the market - in the last few days of this week, we have seen the U.S. tariffs be negated by a high judges ruling and then returned not long after by an appeals court. Now, we wait to see what happens at the highest levels. All to say that we have no clue what will happen. If tariffs stay in place, it acts as a barrier to imports, and UAN does not need that.

- Current expectation is for 2026 to see big acres again (big demand) - it is FAR too early to make solid judgement calls on the 2026 crop mix. Heck, some of you are still planting THIS years crop. However, the fertilizer year starts on July 1 and to build demand models, we need an idea of the crop mix. To that, our early estimations, even if we get solid yields, is that 2026 will be another big crop acreage year which means big nitrogen demand.

- After this spring fiasco, buyers will be more "jumpy" - while this is largely an emotional bullet point, it is important all the same. This spring did things that we have never seen. Ever. The inability of finding product when it was needed and the outlook that 2026 will share a lot of the same factors will likely have buyers jumpy and more willing to pull the trigger early on purchases...even if that price is perceived as high..

Again, this is my educated (ok, educated might be a stretch!!!) POV today. There are a lot of things that can and most likely will change. As/if they do, I will keep everyone up to date. For now...we wait.

NOLA/New Orleans, Louisiana

Number 2 global importer in 2022

Number 1 global exporter in 2022

Price Comparisons

Vs 30 days ago - 0% or approximately $0

Vs 90 days ago - 22% or approximately $65 higher

Vs 6 months ago - 60% or approximately $135 higher

Vs 1 year ago - 53% or approximately $125 higher

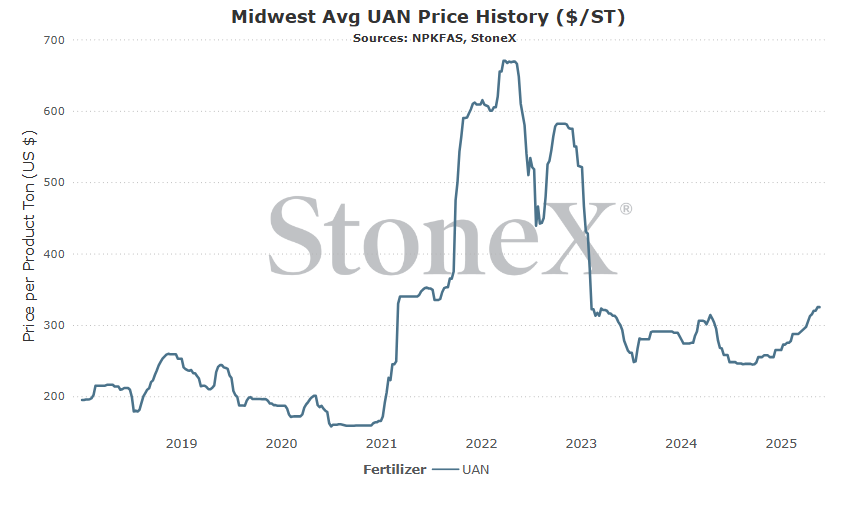

U.S. Midwest Average

Vs 30 days ago - 3% or approximately $10 higher

Vs 90 days ago - 13% or approximately $38 higher

Vs 6 months ago - 27% or approximately $70 higher

Vs 1 year ago - 21% or approximately $58 higher

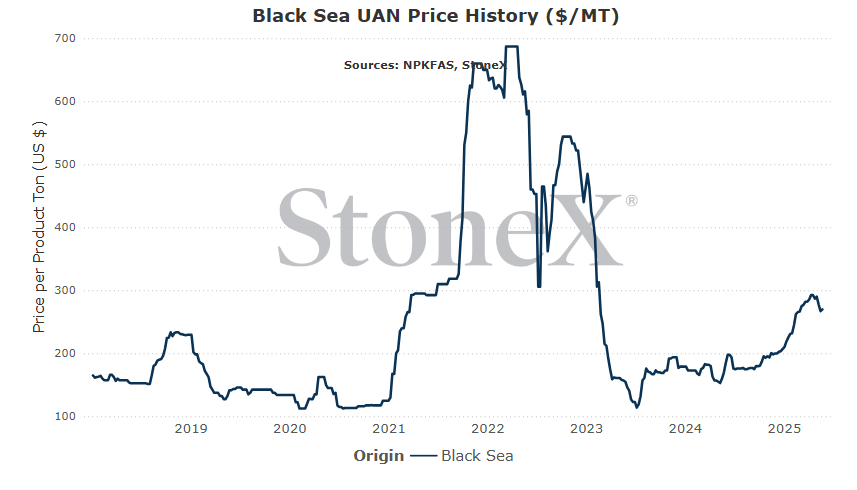

Black Sea (Russia)

Number 2 global exporter in 2022

Price comparisons

Vs 30 days ago - -6% is approximately $17 lower

Vs 90 days ago - 1% or approximately $4 higher

Vs 6 months ago - 36% or approximately $72 higher

Vs 1 year ago - 59% is approximately $100 higher

- Europe proceeds to further block Russian UAN supplies – this looks to be a very real possibility. The EU is taking steps to put more blockades into place to stop Russian fertilizer flows. This will be impactful across the board, but especially so for UAN. This would force European retailers/farmers to look harder to the rest of the world to make up the price difference. That means more competition and higher logistical costs. Guess where those costs eventually end up...

- Trinidad production issues continue – Trinidad has been struggling to normalize their natural gas flows. As a result, nitrogen producers have had to scale back production to meet that input supply. This not only reduces global UAN supplies, it also creates uncertainty of how much the market can depend on Trinidad for supplies. Uncertainty may be an emotional factor, but it still counts and can affect price ideas higher.

- U.S. moves to block Russian goods thru tariffs – this scares me the most. For a time, it looked as though President Trump was going to be able to broker peace between Russia and Ukraine and put this ugly chapter in world history behind us. That no longer seems to be the case. Appears Russia is amassing another huge group (50K) of soldiers on the border for another push. We all know the Trump will react. If this continues, it is not out of the realm of possibilities that he places barriers to entry for Russian goods. If the U.S. loses Russian UAN supply lines, that will remove one of the few competitors of domestic manufacturers which is very price supportive.

- Trinidad natural gas supplies normalize, allow for normal UAN production – this is the hope. While it may seem a bit far fetched today, this is the end goal. We could still see Trinidad natural gas flows return to normal and allow nitrogen manufacturers to return to full production rates. If that happens, it helps to boost global supplies and give the global UAN market confidence going forward.

- Farmer/retailer rejection of summer fill programs – today, I am expecting that summer fill UAN values will be approximately $40 - $50 higher than they were last summer. That is going to be a big pill to swallow for not only farmers but also retailers. On the one hand, after what happened this April and May with the inability to find fresh product, buyers are going to be scared of missing out. However, times are tough and cash reserves are running out. The market might see a high priced summer fill program and decide it doesn't work. Even with what happened, it just doesn't work. If that scenario plays out, it will place pressure on the seller/manufacturer side.

- Spring demand destruction overshot goals – much of April and May saw retailers/farmers finding it near impossible to find UAN that wasn't already purchased. As a result, the few tons found were very expensive and a lot of demand switched to either urea or NH3. To a certain extent, that is exactly what UAN wanted. It's S&D was out of balance and it couldn't fix it with supply. The only other option was to destroy demand to bring balance...but that can be overdone. If as we go through the next month the UAN market starts to find out that too much demand was lost, that can start weighing on price ideas.

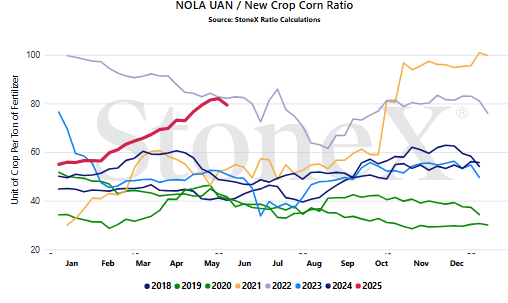

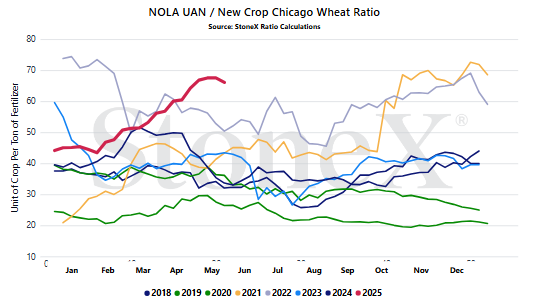

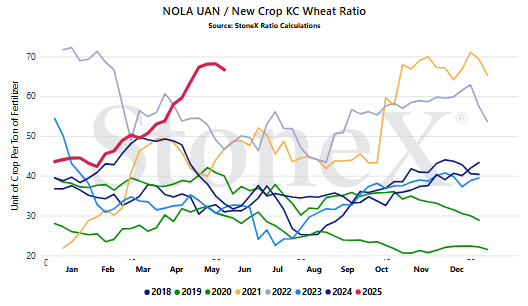

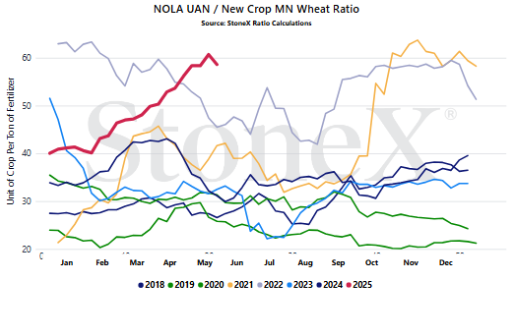

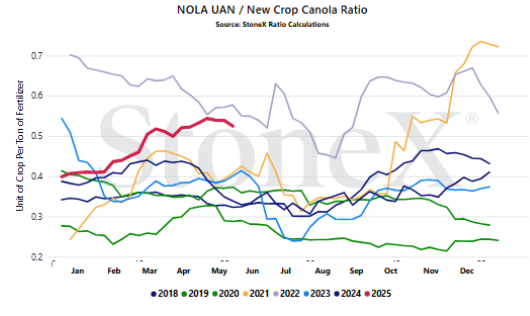

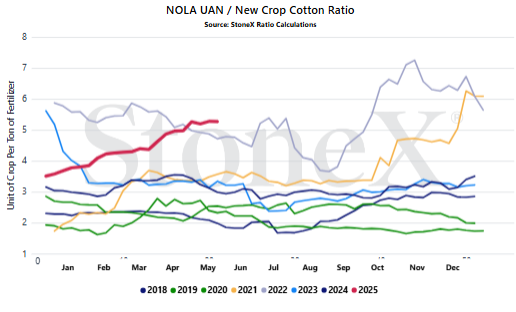

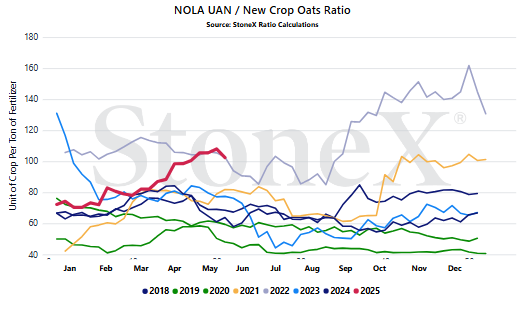

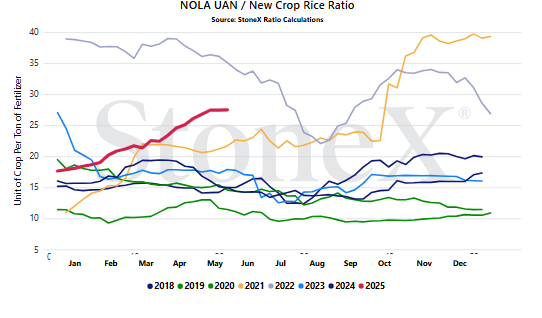

We believe that only looking at the flat price of either grains or fertilizer can be misleading:

-

Only selling grain can hurt you if fertilizer prices rise substantially

-

Only buying fertilizer can hurt you if grain prices fall

We look at the ratio "value" to get a better indication of where we are or how many bushels of X does it take to pay for 1 ton of fertilizer.

Would you rather:

-

Spend 100 bushels to pay for 1 ton of UAN

-

Spend 60 bushels to pay for 1 ton of UAN

When we compare the current ratio value against recent years, we start to see if we are high or low.

YOUR VALUES MAY LOOK DIFFERENT

This graph looks at the NOLA UAN price vs the flat grain price. There are no logistics on either product. Your location will look different due to fertilizer logistical costs, grain basis, etc.

- Europe's approach to Russia - I really believe that Russia's production decisions and this current European spat increase with Russia are about even in importance. However, because the Europe situation will likely change global trade flows, I'm listing it first. If European countries move to further bar Russia and are successful, that will leave Russia with another destination removed. Now, in a perfect world for N.A. buyers, those tons would flow to the U.S. and build supplies which would weigh on values. However, I thought we would see imports higher this last year and we didn't. Is that due to a lack of capacity? Lack of bank backing? Lack of willingness by importers/Russia? If the U.S. cannot increase imports from Russia, that will be a problem because Europe is going to be looking for more. As they block Russia, their import needs rise. This last year saw huge U.S. UAN exports. This coming year could be bigger. This hurts Europe/N.A./Russia.

- Russian production decisions - so, if Europe moves to block Russian UAN and struggles to find more homes in the U.S./world, will they continue to produce UAN? Globally, UAN is a relatively small product with few major destinations. Most of those destinations are western countries who are not seeing eye to eye with Russia. If Russia can change production from UAN to urea, that has a lot more friendly destinations. That would be good for Russian manufacturers, but bad for UAN buyers. Losing that supply would further tighten the S&D which will support price ideas.

- How the U.S. manufactures will approach exports this coming fertilizer year - I believe a big talking point when we review fertilizer year 2025 (July 1, 2024 thru June 30, 2025) will be how massive U.S. exports were to outside North America. I fully expect the market to start asking questions of "how did UAN get so tight in April and May" and I fully expect a lot of answers to come back as "exports". Was it the only reason? Absolutely not. However, it will be the easiest to point to and blame on someone. Will domestic manufacturers reduce exports to "protect their butts" or proceed with little fear of ramifications. What they do or do not do with exports will vastly affect our price ideas.

- Price relationship between urea and UAN - a few short winters ago, the UAN market made the mistake of trying to keep UAN price ideas high while urea tumbled. Part was hubris. Part was hope that urea would return. The end game was that UAN was forced to slash prices in the spring to find demand. Since then, it has been commonly heard that "we will not allow UAN to be a premium to urea again". They feared repeating that story...but times change fast. Now, the UAN market is fundamentally different due large part to the factors listed just above. My guess is we will go back to seeing UAN a premium to urea. It will still need to follow urea price leads, just not in lockstep.

StoneX Ratio Calculation

The ratio calculation is derived from Bloomberg historical grains values as well as fertilizer values from StoneX, NPKFAS, and Argus.

The calculation is simply dividing the fertilizer price by each grain price.

All data was sourced from StoneX unless otherwise noted.