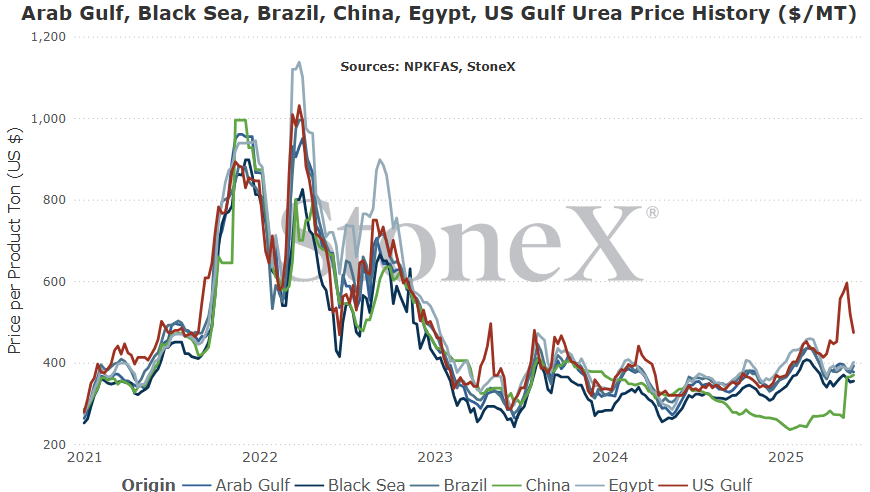

The intention of the below graphs are not to use to say "my price should be X based on this graph". These prices are derived from an FOB price point average. The intent is to show major global price movement trends. Your values will likely have significant basis difference (similar to your local grain price being different than the traded market price).

This graph is labeled as MT in USD currency.

- Tonnage goal of 1.5M tons

- Offers are to focus on west coast ports

- Shipment period thru July 31

The fact that the world had anticipated this exact event for the last couple months should mean that values do not react. It was already baked into the marketplace.

LOL! This is fertilizer. OF COURSE there was a reaction!

Global urea values have been firming slightly since India's announcement. Nothing huge, but certainly on the upward slope.

Now, the waiting game begins with the biggest question being how manufacturers/traders will approach this. On the one hand, it feels like industry parties are fighting to keep prices high. This is especially true when a country like India steps in for 1.5M tons. However, this shipment period stretches to the end of July. There should be plenty of tons available with offers having to consider their next sales options if they miss out on this opportunity.

No doubt this will be an interesting one.

What does this mean for farmers?

This can set the stage for global prices going higher or lower which will eventually make its way to the farm gate.

If India fails to hit 1.5M tons but it is because they decided they didn't need them, solid chance values start to fall.

If India fails to hit 1.5M tons but it is because offers refused to move their price, there is a solid chance that values climb.

If India buys their 1.5M tons but offers were massive, prices could slide on the belief that all the unsold tons now need to find a home.

India has that power to set the tone. Time will tell.

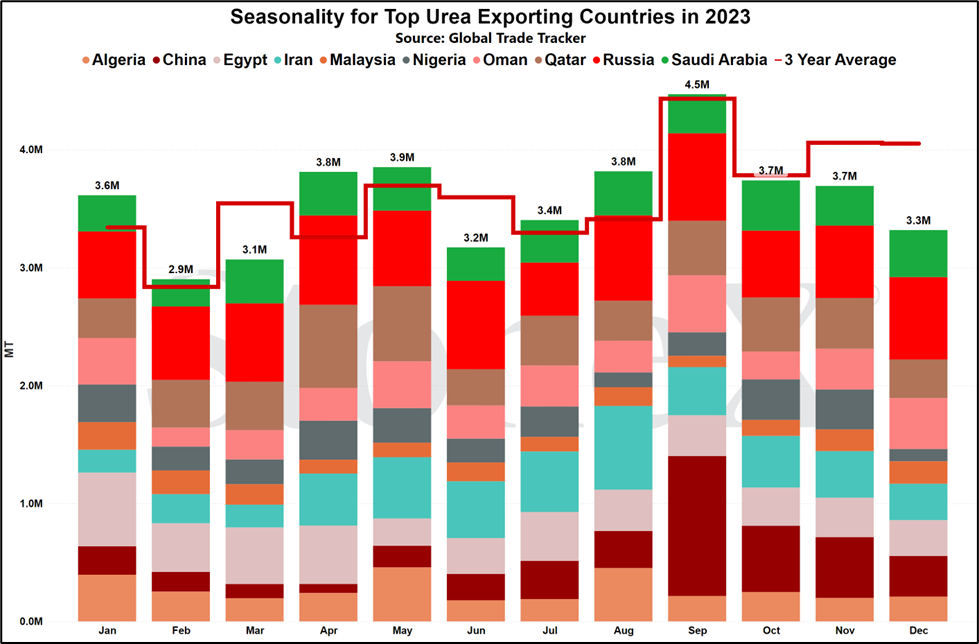

- Russia - 7.8M

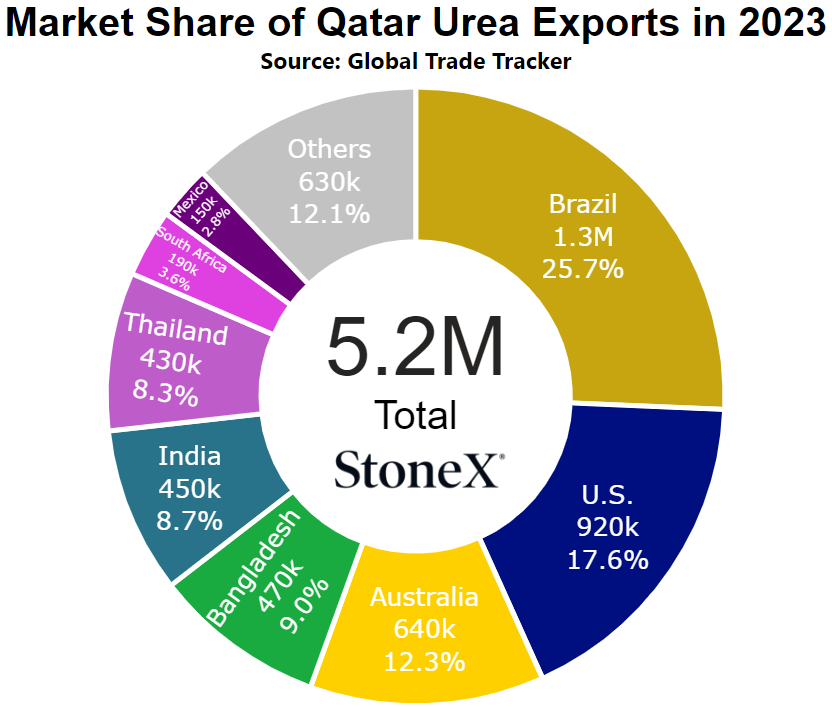

- Qatar - 5.2M

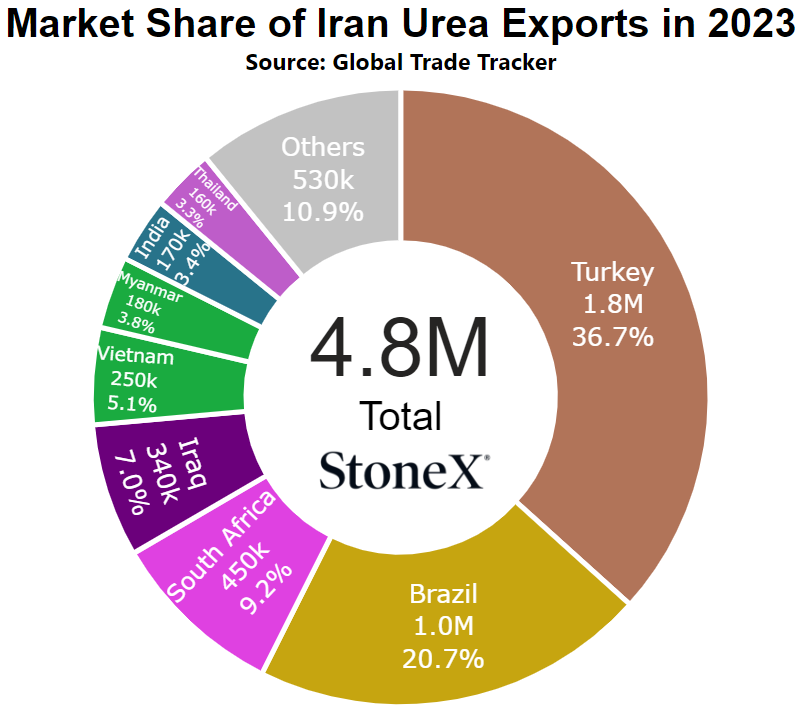

- Iran - 4.8M

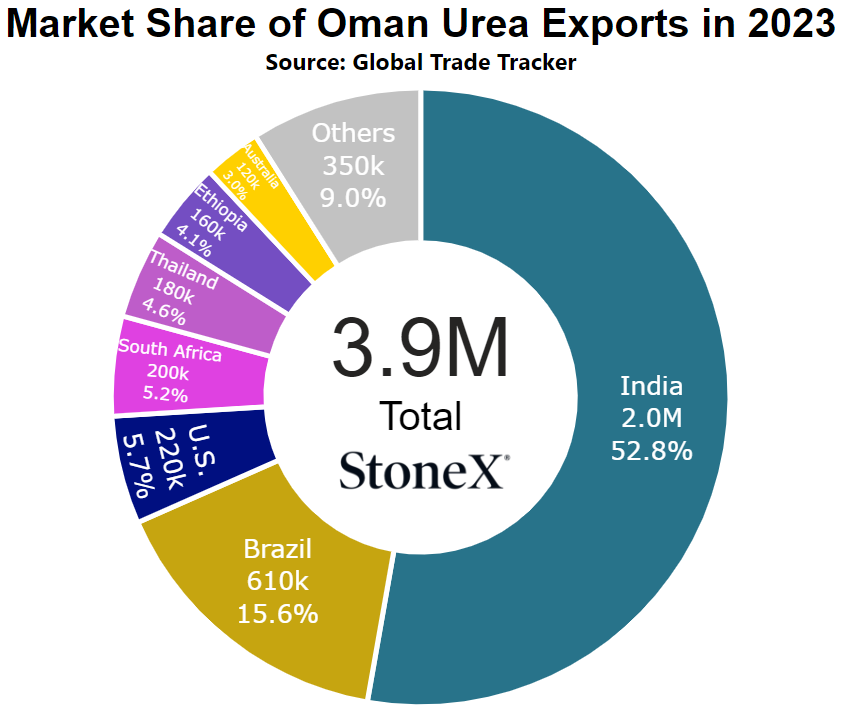

- Egypt - 4.6M

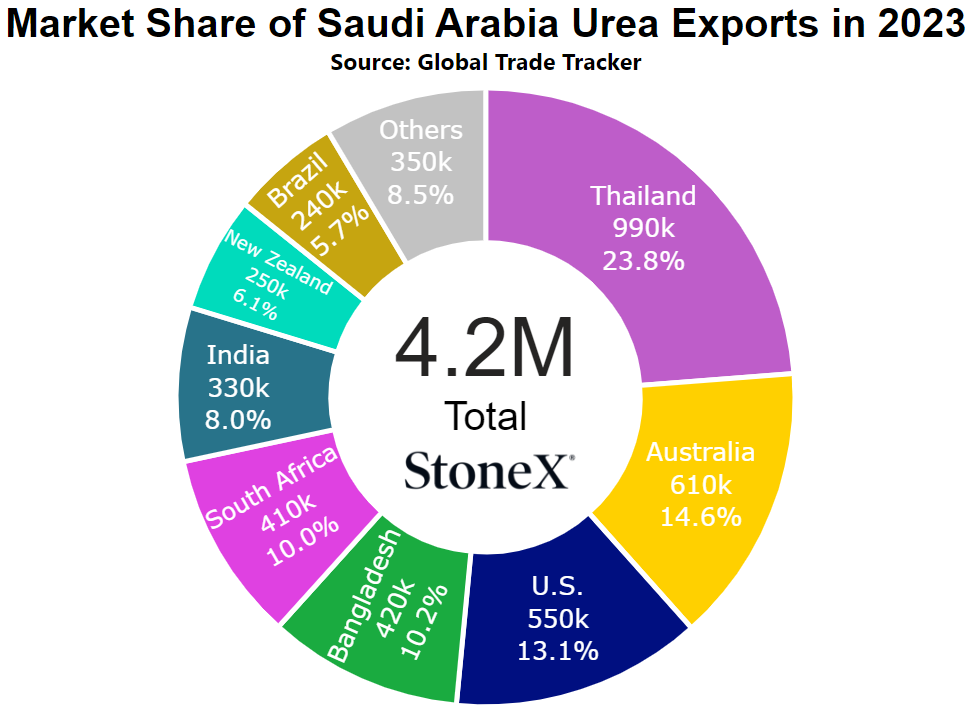

- China - 4.2M

While far from the top spot tonnage wise, they are still a major exporter and a major part of the global urea complex. Production reductions still have effects on the world. Having this happen as India was preparing to announce their 1.5M ton purchase tender certainly doesn't help lower price ideas.

We are hopeful that this remains a very short term situation with limited impact on available supplies.

What does this mean for farmers?

Having a top 5 global urea exporter lower their production rates also lowers global supplies which is a very price supportive situation.

Hopefully this remains a short term situation and production can resume full rates much sooner than later. That would help to alleviate much of the impact on global pricing.

Still, this is a bullish event as India begins their purchase tender which can set the tone of the world going ahead.

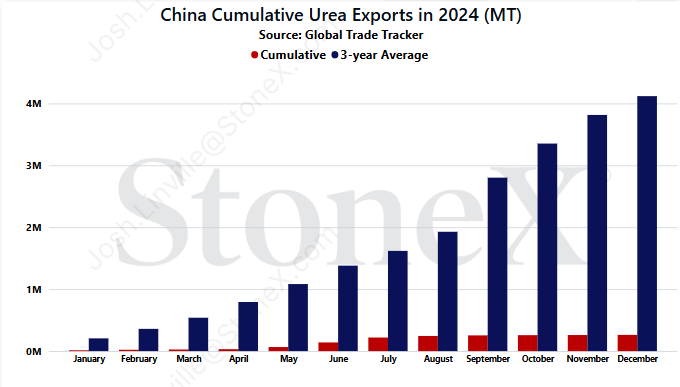

- 2021 - 5.3M tons

- 2022 - 2.8M tons

- 2023 - 4.2M tons

- 2024 - 262K tons

So when viewed on years 2023 and earlier, the "2M tons is nowhere near enough" crowd is absolutely right in their POV. However, look at 2024. They exported almost nothing, yet global values were lower than they were today. From my vantage point, 2M tons is a vast improvement from last year which helps to boost global supplies. More global supplies should theoretically mean lower prices. It doesn't always mean that, but it certainly helps.

For now, we are going to have to continue to wait and see what the final announcement is. I'm still a believer that they will allow 2M tons to be exported but we will have to watch close. If those domestic values do start to climb, the program can be cancelled and suddenly 2M tons disappear.

That wouldn't be good for buyers...

What does this mean for farmers?

I still want to believe that if they allow 2M tons to export and they are not allowed to target India as a destination, that will create a lot of competition in the coming months. Whenever China is a participant, they act like the boogey man of the industry. The market runs scared. That should mean lower prices. However, if they cancel the program, hit their tonnage mark, etc., they disappear and suddenly the price ceiling disappears.

Hopefully they come through and at last provide some short term bearishness for buyers.

- We started the year growing corn acre expectations - at the start of 2025, our forecast had corn acres at approximately 92M tons. We quickly jumped to 92.5M...then 93.4M...then 95+M. Now, many estimates are pointing to a possible 96M acres when the dust clears. The average nitrogen application rate for the U.S. corn crop is around 155 lbs of actual N per acre. That was a lot of last minute nitrogen demand. The market simply didn't have enough time to react.

- Spring seasons was nearly perfect for farmers/retailers - weather has been PERFECT this year. It warmed up, it stayed dry, and farmers/retailers were able to apply/plant/etc. with no stoppages. Importers have to plan ahead since it takes weeks for vessels to arrive. They make these purchase/shipping decisions with the anticipation of a "normal" spring. If spring is late, they have to eat the cost of that ship sitting around. If spring is early, their vessels do not arrive soon enough. This year, spring was early and it never stopped. Nearby inventories simply were not ready.

- UAN supplies became non-existent for much of April/May which switched demand to urea - this was the big one and something we spoke a lot of this year. UAN became near impossible to find. That does not mean that farmers will stop planting. Rather, they decided to switch to urea for their nitrogen needs. Heck, some switched from UAN that they had in hand to urea for the cost savings. I cannot wait for the season to be done so we can get the final data and see how it all happened.

In the end, supplies simply were not ready for the demand to come the way that it did. I know folks are upset and looking to blame someone. Don't. OK, maybe that is a bit harsh. Do what you want, but it isn't anyone's fault. Importers brought product as they should for a normal spring season. It would have been irresponsible to plan for this type of spring. Retailers did all they could to keep product available. Farmers did what they did best. They planted and applied and when necessary, they stayed nimble.

Yes, seeing N.A. jumping to such a massive premium to the world is shocking, but I think a testament to our industry. Given all the issues that were out there, the market did a hell of a job of getting this spring done.

- We are expecting another big corn crop next year - it is far too early to make definitive calls for next years crop mix, but we have to start today. The fertilizer year starts July 1 and demand models and outlooks do not work without a POV on crop mixes. Right now, 2026 could see very similar nitrogen demand with corn acres expected to be high again. That will likely change many times between now and next year, but that is where we are today.

- Global trade flows are still questioned based on multiple issues (Russia/tariffs/etc) - Russia is showing less signs of peace with Ukraine. The world may begin to stand up and start refusing business with them that would cut the largest urea exporter from the market (low probability). U.S. tariffs continue to confound traders/importers and have folks less willing to lock up tons (higher probability). Chinese exports are expected to hit 2M tons, but could be cut at any time. All in all, there are still plenty of issues around the world.

- Nitrogen supply issues this spring will have buyers more "jumpy" - after UAN supply issues and massive urea price increases across N.A. this fall, I think buyers are going to be a bit more nervous. That could cause folks to buy sooner/higher than they want to but the fear of losing out might drive that.

- Chinese exports hitting 2M tons will help, but are not guaranteed - again, as mentioned above, we are expecting 2M tons of urea to be exported from China. That is far from guaranteed.

- This price does get somewhat in line with grain values - if we reset slightly higher than last year, the urea/corn ratio does get back in line with what we would consider normal. It would not be a no brainer, but justifiable.

Again, I am on an island with this point of view. For reference, Q3 '25 NOLA urea futures traded at $365 earlier today. That is $40 higher than my reset POV. There is a LOT of work for the industry to do to get to my number. Still, the factors that I look at support the $325 reset for NOLA barges today. Time will eventually tell.

NOLA/New Orleans, Louisiana

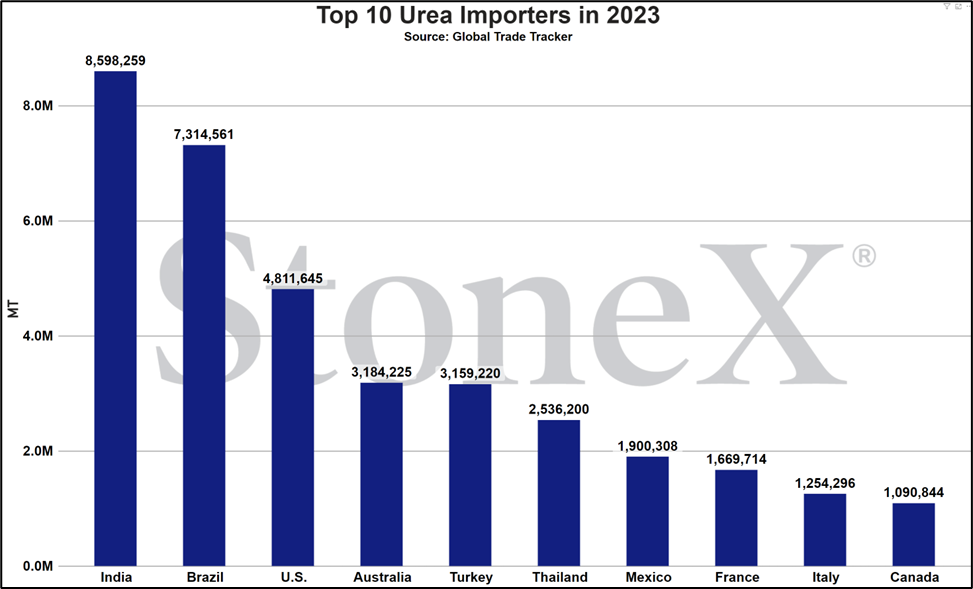

Number 3 global importer in 2022

Price comparisons

Vs 30 days ago - -15% or approximately $75 lower

Vs 90 days ago - 9% or approximately $35 higher

Vs 6 months ago - 39% or approximately $121 higher

Vs 1 year ago - 48% or approximately $140 higher

U.S. Midwest Average

Vs 30 days ago - 4% or approximately $21 higher

Vs 90 days ago - 16% or approximately $79 higher

Vs 6 months ago - 50% or approximately $188 higher

Vs 1 year ago - 54% or approximately $199 higher

U.S. Southern Plains Average

Vs 30 days ago - 11% or approximately $60 higher

Vs 90 days ago - 26% or approximately $120 higher

Vs 6 months ago - 55% or approximately $208 higher

Vs 1 year ago - 61% or approximately $223 higher

U.S. Northern Plains Average

Vs 30 days ago - 10% or approximately $57 higher

Vs 90 days ago - 24% or approximately $114 higher

Vs 6 months ago - 62% or approximately $228 higher

Vs 1 year ago - 55% or approximately $212 higher

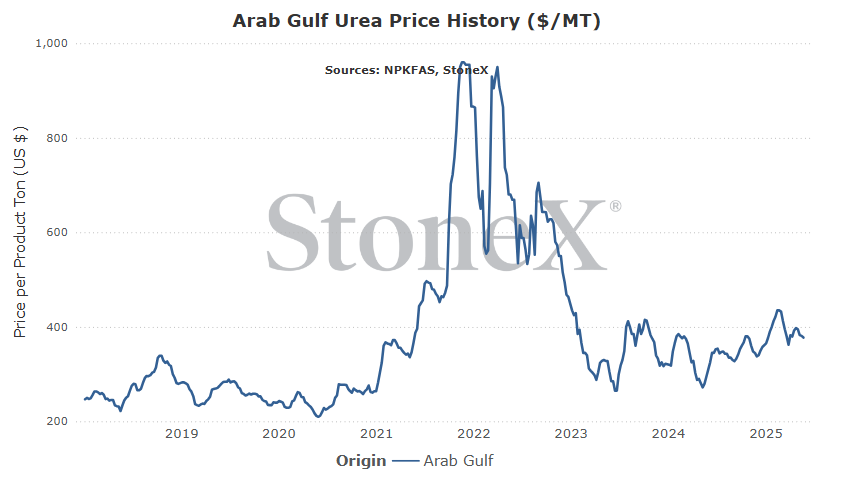

Middle East

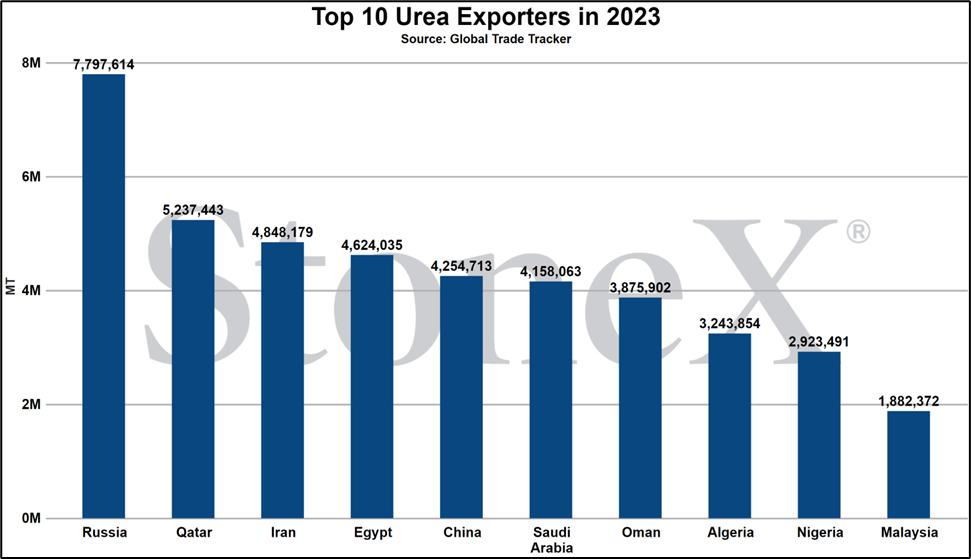

Number 1 exporter (as a region, not as individual nations)

Vs 30 days ago - -5% or approximately $20 lower

Vs 90 days ago - -13% or approximately $55 lower

Vs 6 months ago - 9% or approximately $33 higher

Vs 1 year ago - 28% or approximately $83 higher

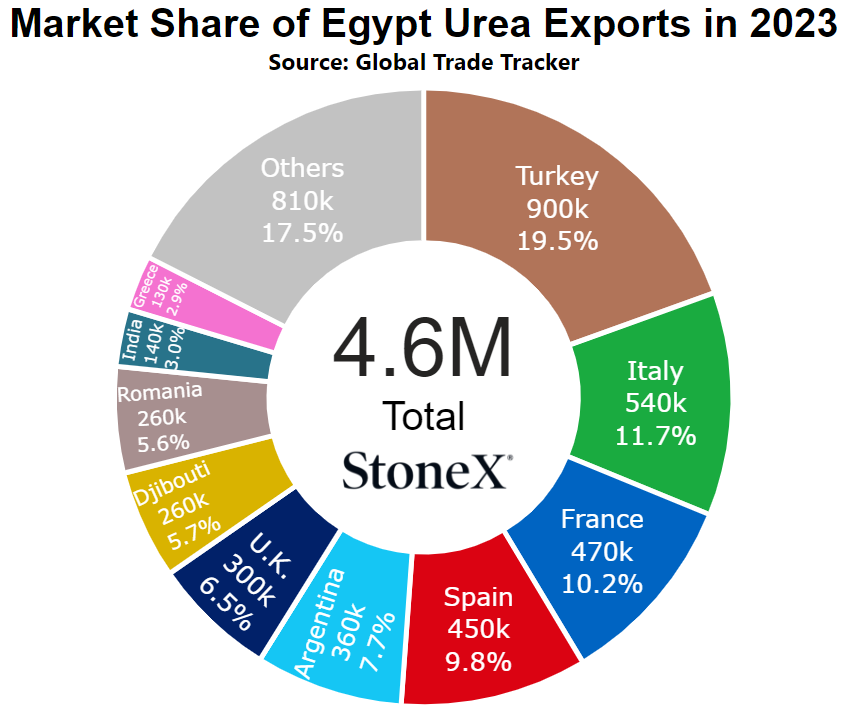

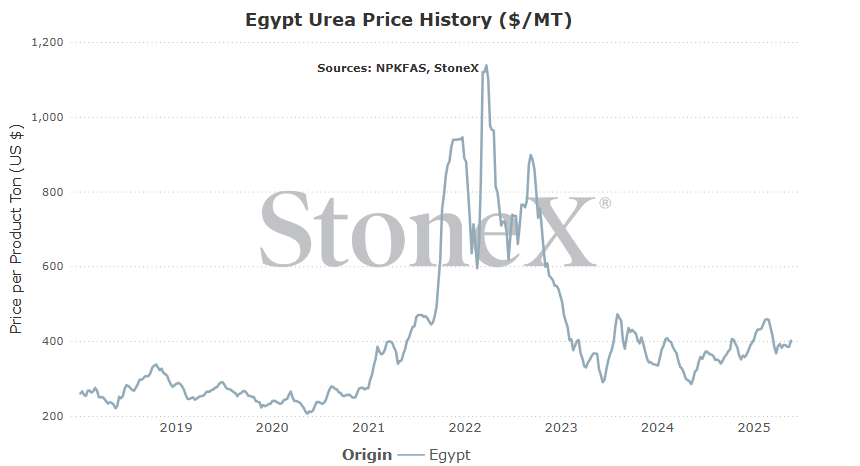

Egypt

Number 4 global exporter in 2022

Price comparisons

Vs 30 days ago - 3% or approximately $12 higher

Vs 90 days ago - -12% or approximately $56 lower

Vs 6 months ago - 11% or approximately $40 higher

Vs 1 year ago - 26% or approximately $82 higher

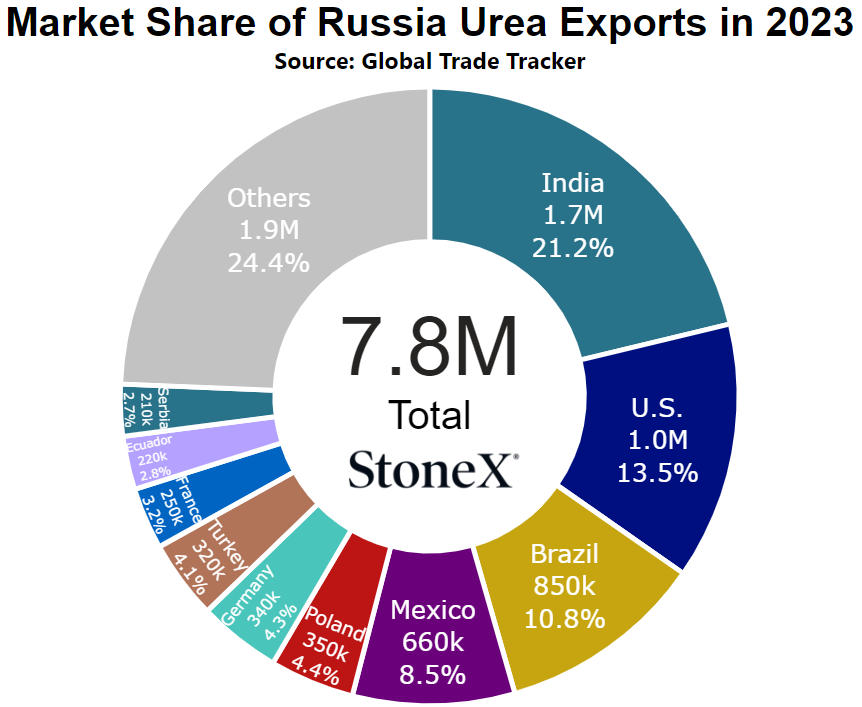

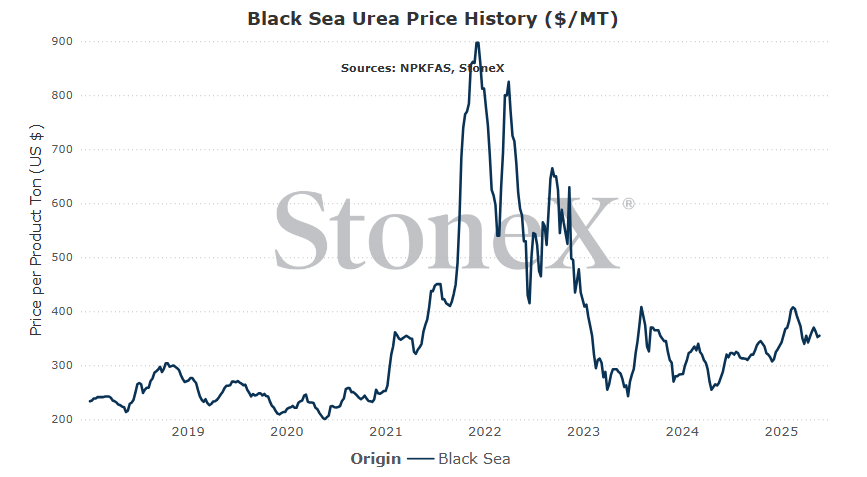

Black Sea

Number 1 global exporter in 2022

Price comparisons

Vs 30 days ago - -2% or approximately $8 lower

Vs 90 days ago - -10% or approximately $38 lower

Vs 6 months ago - 13% or approximately $40 higher

Vs 1 year ago - 28% or approximately $78 higher

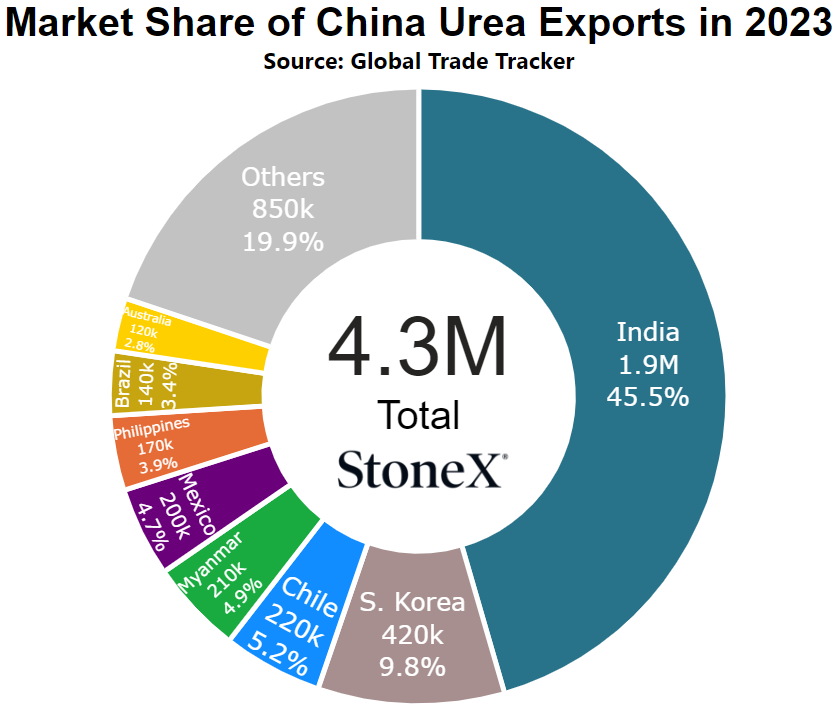

China

Number 9 global exporter in 2022

Price comparisons

Vs 30 days ago - 36% or approximately $98 higher

Vs 90 days ago - 38% or approximately $101 higher

Vs 6 months ago - 40% or approximately $106 higher

Vs 1 year ago - 10% or approximately $35 higher

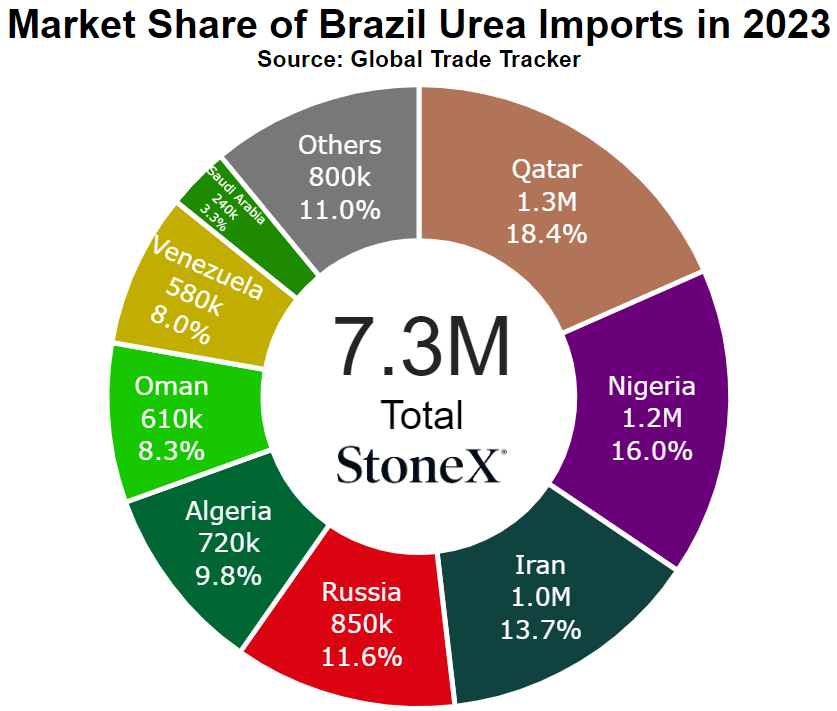

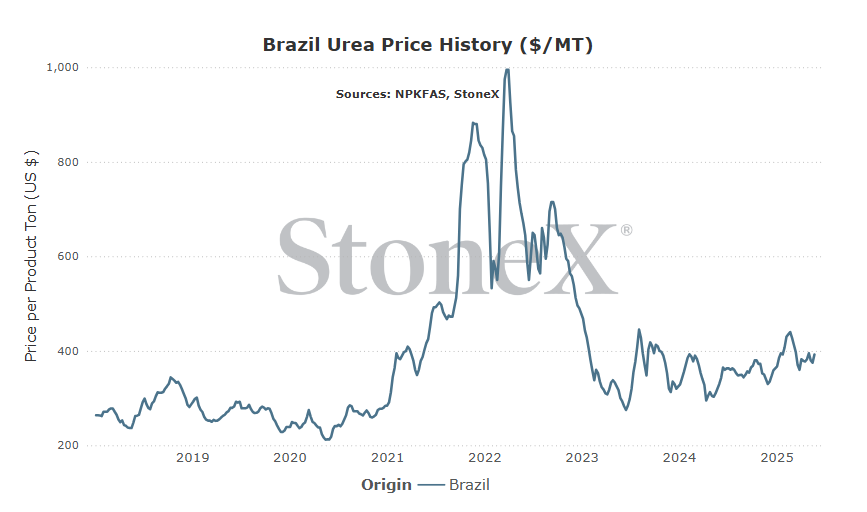

Brazil

Number 2 global importer in 2022

Price comparisons

Vs 30 days ago - 3% or approximately $10 higher

Vs 90 days ago - -8% or approximately $35 lower

Vs 6 months ago - 15% or approximately $53 higher

Vs 1 year ago - 23% or approximately $73 higher

- The typical "India purchase bull" event happens - there is absolutely nothing about the India urea purchase tender that was surprising. At the conclusion of the last tender, the market largely circled the wagons around a late May/early June return and estimations of tons to be secured were 1.5 - 2M tons. It was the most well known secret in the fertilizer market...yet prices still react. The market tends to bull up on urea prices when India tenders and we are watching for that once again...though we need to see for how long it lasts.

- China slashes export quotas - right now, the expectation is that the Chinese government will allow upwards of 2M tons of urea exports. However, we all know that they will hold the kill switch if they see exports happening too fast or worse, they see domestic values rising. If the world wakes up one morning to the news that China has said no more, we could see prices supported.

- Unexpected production downtime/higher turnaround events due to bearish fears - right now, we are still expecting a value reset as we look to the Northern Hemisphere summer months as they typically do. However, manufacturers also know it is coming. There is still the possibility that manufacturers either have unplanned production outages. We could also see manufacturers try to pull forward plant turnarounds/repairs if they do not like the outlook. Either scenario reduces available supply and supports price ideas.

- India elation gives way to summer demand lull - I think any Indian elation will quickly give way to summer demand lull's which could/should weigh on price ideas. There are always reasons why a price will not fall as far as some (myself included) might think. However, the July/August is generally slow for demand, unsold positions get bigger, and manufacturers get aggressive on price to find liquidity. Things can change but no reason to believe normal cannot be expected.

- China exports 2M tons...or more - many folks have pointed to the 2M ton Chinese urea export number and said "that is significantly less than their normal 5 - 5.5M ton export". That is absolutely true, but they haven't been normal for a lot of years. If we look to 2024, their exports were only around 265K tons. If China proceeds and follows through on their 2M ton benchmark, that is a vast improvement over last year. Fuel to the fire would be if China exported 2M tons, domestic values didn't budge, and supplies were still more than plentiful. At that point, the government could surprise the world and say "go ahead and export another 1 - 2M tons". I would expect that would send values spiraling.

- Farmers and retailers reject high prices - eventually, the end user has to approve of the value and in this value chain, the farmer has last say. Overall, demand for fertilizer year 2026 is already looking big based on too early acreage mix forecasts. However, that does not mean folks will want to rush to buy high priced product. Grain prices are low. Most inputs are high. Farmers are getting squeezed on the input and output part of the equation. That is not going to make them want to spend money very quickly. If fill programs come out and farmers/retailers largely say no, it could rock the supply chain and pressure prices.

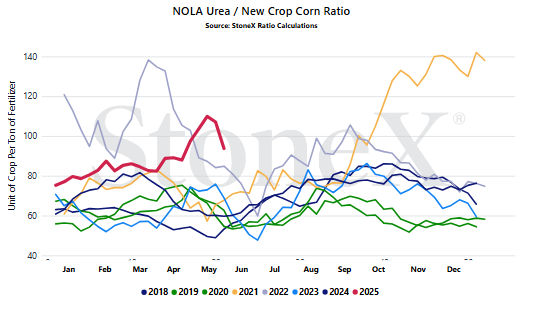

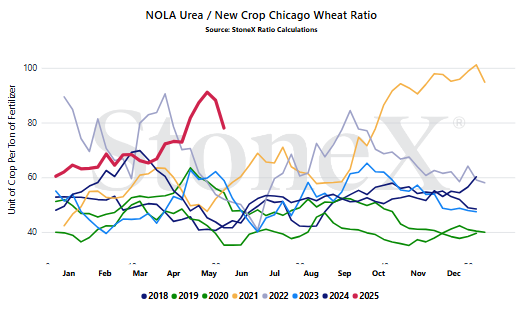

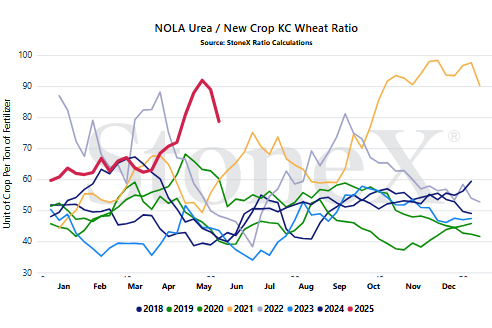

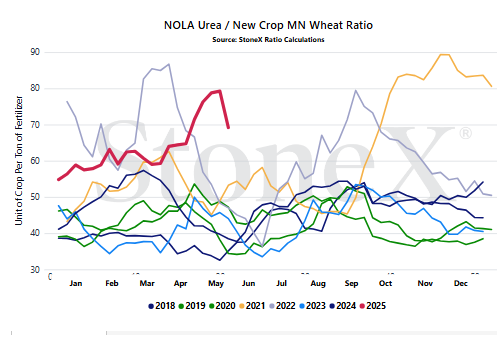

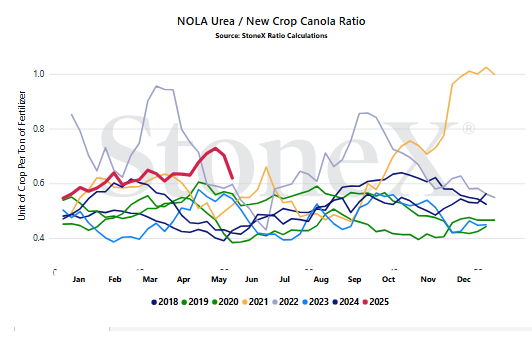

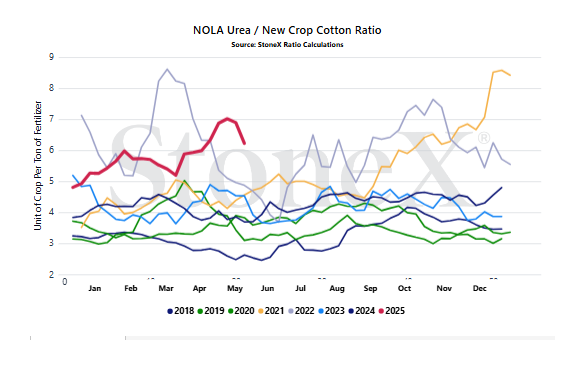

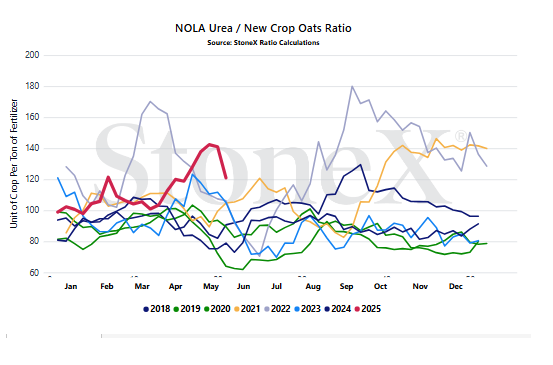

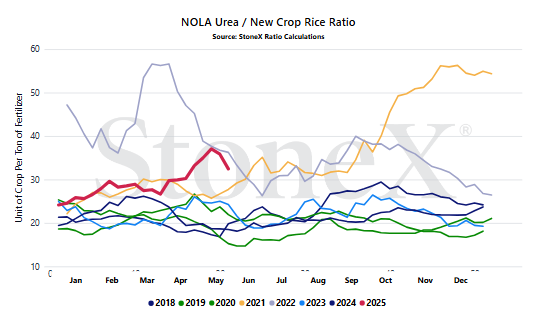

We believe that only looking at the flat price of either grains or fertilizer can be misleading:

- Only selling grain can hurt you if fertilizer prices rise substantially

- Only buying fertilizer can hurt you if grain prices fall

We look at the ratio "value" to get a better indication of where we are or how many bushels of X does it take to pay for 1 ton of fertilizer.

Would you rather:

- Spend 135 bushels to pay for 1 ton of urea

- Spend 55 bushels to pay for 1 ton of urea

When we compare the current ratio value against recent years, we start to see if we are high or low.

YOUR VALUES WILL LOOK DIFFERENT

This graph looks at the NOLA urea price vs the flat grain price. There are no logistics on either product. Your location will look different due to fertilizer logistical costs, grain basis, etc.

- Biggest focal point remain Chinese export programs - China still keeps the number one watch point in my mind. It sounds like 2M tons will be their export goal for 2025. That is significantly higher than the 2024 total of 266K tons. However, it is significantly less than their normal export rate of 5+M tons. Will China adhere to the 2M ton goal? Will they reduce the number of tons allowed if domestic Chinese values start to rally? Is there a path where they allow 2M tons and then decide that more can be released? All of these scenarios change the scope of the market...and the price points.

- Second biggest focal point are other global production rates - Europe as a whole is the low hanging fruit here. Everything is relatively unchanged vs the same time last year. We still see their production at around 75% of normal. It hasn't improved...but it hasn't gotten worse. However, production hiccups in places like Egypt and Trinidad are reducing available supplies and helping keep a bit of strength in the nearby market for now. However, if production normalizes and demand starts to step back, this can change the outlook quickly.

- India purchase tender strength/fallout - India shouldn't matter. We have been expecting this announcement since their last tender fell short of their tonnage goal. There shouldn't be a urea player in the world that didn't know India was going to announce...but somehow it will still matter. How many tons will be offered? What will the price points be? Will India lock up 1.5M? If they fall short, will it be because the market refused a lower price or because India decided it didn't need it. All of these things will help shape the market as it stares into the demand abyss of July/August.

- Looming summer months and the markets demand reactions - speaking at the typical summer demand abyss. Right now, the market is a bit worked up between Chinese export programs, India purchase tender, and some production issues. However, eventually the temps will rise and the demand will fall. If/when that time comes, how will prices respond and how will buyers respond to those price changes?

StoneX Ratio Calculation

The ratio calculation is derived from Bloomberg historical grains values as well as fertilizer values from StoneX, NPKFAS, and Argus.

The calculation is simply dividing the fertilizer price by each grain price.

All data was sourced from StoneX unless otherwise noted.