GLOBAL

Where do we go from here?

We finally saw the bullishness we had been looking for. Tight supplies finally met demand that stepped forward and the markets got hot. Well, since that happened, things have slowed down. India has been dragging their feet on their anticipated purchase tender and other global buyers have gone silent. Values have dipped a bit, though they are still higher than last edition.

My fear is that buyers are now backed into a corner. We are nearly certain (I would say I am certain, but compliance does not like that talk!!!) that India needs to step in. They fell significantly short of their tonnage goal in their December tender. They fell significantly short of their tonnage goal in their January tender. Demand I heard to be solid. They can drag their feet a week or two, but that should be about it.

Other global buyers must make last preparations for their spring season. North America is no different.

On the supply side:

- Iranian production is still offline

- Chinese exports still do not exist

- European production is still 75% of normal

That is a HUGE hole in the global S&D.

With all of these, I still think higher prices are on the horizon. I just do not think there are enough pages left in the calendar for buyers to slip their way around it. When the buying starts, I’m afraid the outcome will be higher prices.

One last point, when I look at today’s S&D, I think it is in worse shape than in late 2021/early 2022 when prices were significantly higher. This is not to say I think prices are going back to those levels, but I do believe the actual S&D is tighter.

Iranian production stays offline longer than expected

Our story surrounding global urea markets has been that of tight supplies. Europe continues to produce at approximately 75% of normal which is removing 3+ million tons of production from the global S&D. The Chinese government continues to largely ban urea exports to raise domestic urea stockpiles as well as lowering domestic urea values. Fortunately for Chinese farmers, this strategy has worked well. Unfortunately for global famers, this strategy has worked well. Chinese exports are historically normal around 5 to 5.5M tons per year. 2024 saw them at a grand total of 266K.

Now, the world is having to contend with Iran having issues.

The global urea market puts a lot of weight on Chinese participation. Their 5 – 5.5M tons typically equates to roughly 10% of the global export marketplace. When they are participating, it creates a sense of dread and nervousness that helps to drive price ideas lower. When they are not participating, it allows the market to rally higher.

Rarely discussed are Iranian tons. They have been the subject of strict tariffs that have seen many major global buyers refusing to do business. When an Iranian price goes up or down, the market generally shrugs it off as “it’s just Iran. It doesn’t matter.” From a direct POV, they are correct. However, what is missing from that approach is the fact that Iranian tons STILL affect the global S&D.

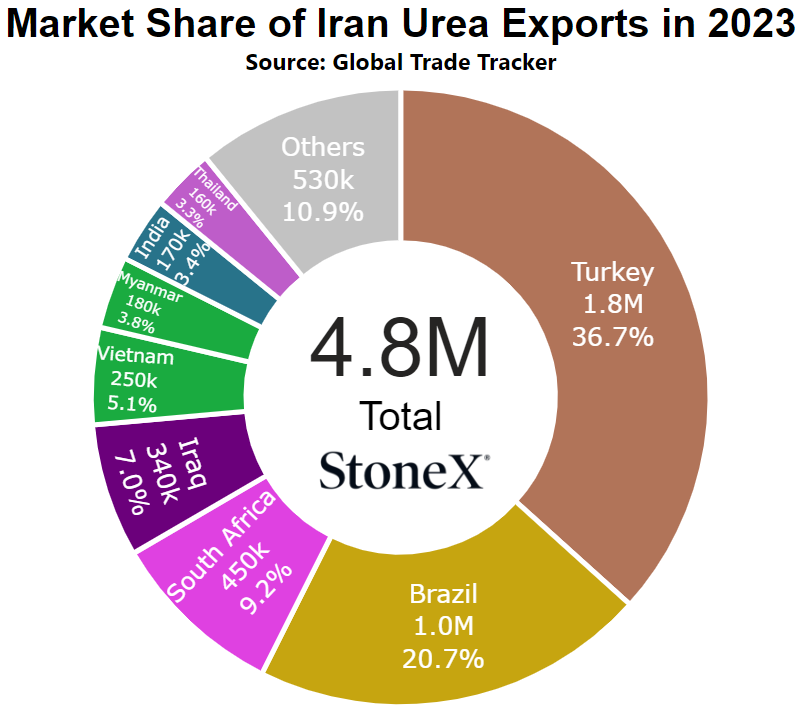

In 2024, Iran accounted for roughly 4.8M tons of urea exports. That is VERY near the same total that China would export on a normal basis.

We started 2025 with Iranian production suffering due to gas supply issues. These were seen as relatively short term and we, as well as many in the market, believed it would be short lived. However, as I write this, their production STILL has not been heard returning. As a result, approximately 400K tons are lost ever 30 days on top of losses from European and Chinese sources.

I still do not believe this will be a long-term issue…but damage is being done that will not be made up before many spring seasons. When combined with European and Chinese shortfalls, over 1M tons of supply are being lost. The world does not have excessive production as it has in the past so when these issues pop up, prices increase rapidly as has been seen in the last month. Now, I do not believe we will see supply shortfalls/outages. That is a story that has been talked out too many times in the past. Rather, this puts the market more on edge and with higher prices.

With spring fast approaching, this makes a hard situation much harder.

Update: Between starting this and sending it out, it appears things are finally changing for Iran. There have been a couple vessels of urea sold with manufacturers expecting to be back online at the start of March. This is very welcome news for the global urea market, but damage has already been done. With production already going as hard as it can under current circumstances, their production losses will remain as a hole in the global S&D. It helps to place a bit of a cap on the market, fundamentally should not do more than stop the rise based on it, but emotionally could see prices slide a bit as the market breathes a sigh of relief.

What does this mean for Aussie farmers?

My POV on global urea has been one of much tighter supplies for several months now. Normally, Aussie importers can drag their feet and wait for Northern Hemisphere buying to wrap up and then take advantage of more aggressive sellers in its wake. That is usually because supplies become MUCH more sufficient after that run.

But what if things stay tighter than normal?

If that is the case, then prices do not dip as quickly as they normally do. This is the issue facing importers today. Do they get caught up in the bullishness of today to help lower overall values to the farmers and take the price risk? Do they drag their feet in hopes of buying lower prices later, knowing there is a chance they might be wrong?

All of these decisions change how the pricing structures within Australia react. Unfortunately, losing Iran for as long as we have likely means losing an additional 500 - 750K tons that was expected. Those tons do not get made up. They are gone for this fertilizer year.

That hurts.

India holds off on expected purchase tender in hopes of lower prices

In December, India tendered for urea with a tonnage goal of 1.5M. They would only end up securing 187K.

In January, India again tendered for urea with a tonnage goal of 1.5M. They would only end up securing 559K. The east coast was very near their 500K ton goal, but the west coast suffered.

That brings us to today. Given that these past tenders had failed and domestic demand had been heard as very good, it lead many (myself included) to believe that the would need to tender once again in mid-February. In fact, at one point, it looked like it was happening. There were conversations starting that usually begins their process.

Then, crickets.

Nothing has been announced. All discussions have gone away and that has left the market wondering WTF.

That brings us to today. Global values are certainly higher than last month's edition of this, but they have dipped from their high's. The market was expecting a purchase battle between India and many other global buyers as everyone prepared for spring. India played a big part in that battle, given that their purchase was more based on government subsidies than farmer profitability. However, as much as India stepping in was going to be a driver, their dragging of feet plays just as big a part.

Now, if you ask most parties in the industry if they think India is still coming, they will give you a resounding yes. It isn't a matter of IF they tender, it is a matter of WHEN they tender. Now, from a fundamental POV, that means prices shouldn't dip. Everyone knows they are going to buy eventually. However, fertilizer can be an emotional market and that is how I see it today. Buyers have stepped away and a deafening quiet left in its place. As a result, prices have slide but it begs the question "what happens when demand returns".

Spring is just around the corner. Demand is coming.

What does this mean for Aussie farmers?

This has been a GREAT situation for Australian farmers!

India dragging its feet has had a huge effect on global prices. The lack of an India tender has helped prices fall around the world...for now.

However, my word of caution is that they are coming. I still think they are coming sooner than later. When they do, I am worried what the reaction will be.

Might be worth having a conversation or two today just to see what opportunities are available.

Peace hopes rise for Russia/Ukraine, not likely to help fertilizer short term

Trump has hit the ground sprinting since taking office. Unlike in his first term that seems like it started with confusion on how he actually won, this term seems to be starting as though he has been planning for four years.

One of the centerpieces of his early days have been finding peace between Russia and Ukraine. Not all parties are thrilled with the approach or the heavy handed "assistance", but he is pushing forward and it appears peace is closer now than at anytime before.

So this begs the question: what happens to urea markets if peace is found?

There are a couple pieces to this from my POV.

The first is the immediate response which shouldn't affect urea fundamentals. During the early days of the invasion, there was a serious fear that Russian fertilizer would not be allowed to ship. That is a large part of why prices spiked in late '21/early '22. However, they ultimately did not slow down. In fact, they picked up the pace as Russian manufacturers took advantage of high global prices. If peace is found, I think it will calm some nerves in the market which could help lower price ideas.

The second would be a step toward normal relations between Russia and Canada/Australia. Both Canada and Australia placed heavy tariff's on Russian produced fertilizers and effectively blocked them from arriving directly. If peace can be found, a next logical step should be to normal relations which includes dropping these tariff's...eventually.

The third and longer term one would be gas flows to Europe. Now, this is a longer term situation that could result in Europe returning to normal production flows. Russian supplies traveled thru the Nordstream pipeline. When tensions rose, Russian shut off the pipeline. While less than ideal for European buyers, it at least meant that if relations improved, the pipeline could open and shipments resume. Then, someone attacked it. Not sure which country did it but the ending result doesn't care. The pipeline was ruptured, rendering it useless until repairs are made. So, even if European countries and Russia were to return to normal diplomacy tomorrow, that would only mark the day that repairs can begin. This pipeline sits under a large amount of water and the inside has been exposed to sea water which means a long stretch will need repaired. Short term markets could slide with the excitement of normalcy returning, but it would take time before real effects took place that would bring European production back online.

What I am trying to say is that there is hope building. I do not want to take away from a somewhat feel good story. I just want to make sure we do not overjudge how quickly things can change.

What does this mean for Aussie farmers?

This helps Aussie farmers across a couple different points of view.

First, it could lead to open trade routes with Russia once again. Remember that the Australian government took the steps to block Russia goods as a retaliation of Russia's invasion of Ukraine. Removing these lanes means less opportunities for importers to find product to meet demand. Less supply options = less competition = higher prices.

Second, it could eventually lead to European production returning. If that were to happen, it would be a major win for the global S&D and as a result, a massive win for Australian farmers. If Europe could get back to producing their own nitrogen, they would no longer need to buy it from the world. Those global suppliers would then be forced to find other buyers. Basically, the domino effect that cause nitrogen to rise on Europe's issues would have the opposite effect on their return.

These are not going to be overnight situations but are positive for buyers.

Rumors grow of Chinese exports returning, unfounded

I normally do not write about rumors in the marketplace. I would rather sit back and wait for actual stories to pop up, but China is too big a deal. It also gave us a glimpse of what would happen.

Since late 2023/early 2024, the Chinese government has been restricting urea exports with two goals in mind:

1. provide more than adequate supplies for Chinese farmers

2. provide significantly lower urea prices to Chinese famers vs the world

This program really showed itself in 2024. China normally exports around 5 to 5.5M tons of urea per year. 2024 saw their export total at only 262K.

That is not a typo...

The result was exactly what the government had hoped for. Chinese supplies grew significantly while domestic values fell. By losing export competition, manufacturers were forced to fight in the domestic market and with supplies huge, it forced prices lower. From a Chinese perspective, it was brilliant. Unfortunately, the rest of the world paid the price.

In the last month, rumors started to circulate that this export restriction was going to be softened due to record stockpile levels. Something had to give. Either production rates had to drop or exports allowed to flow. Some rumors tagged March as the return date. Others tagged July. The ultimate result? Domestic Chinese urea values started to rise...exactly what the Chinese government did NOT want to have happen. Especially just before their spring season.

Because of the rumors and the resulting price change, I think the government got a peek of what not to do. If they allow exports, prices rise. That doesn't mean they will not eventually soften their stance, just probably not right before the spring season. If I were them, I would wait until spring was over, and then do a limited export program. Only 1 or 2M tons allowed to export. It alleviates some of the massive supplies while capping domestic values.

For now and for the rest of the world, it doesn't look like change is coming soon enough to influence the spring, but it does give home for summer resets.

What does this mean for Aussie farmers?

Short term, it means very little because it doesn't look like anything is changing. The rumors ended up being false. Exports do not look like they are increasing.

However, it is positive longer term as it shows the struggle China currently has. Stockpiles are believed to be a record high's. Domestic Chinese demand is good, but not enough to offset what they produce. Eventually, something has to give and the path of least resistance appears to be allowing at least some exports.

If/when Chinese exports resume, it should have a net negative affect on global prices. If this were to happen sooner than Aussie imports are required to be secured, this could be a massive win for Australian prices/supplies. If China returns in time and becomes a competitor for Australian demand, the rest of the world could "freak out" to make sure they stay competitive.

More suppliers is a good thing for buyers.

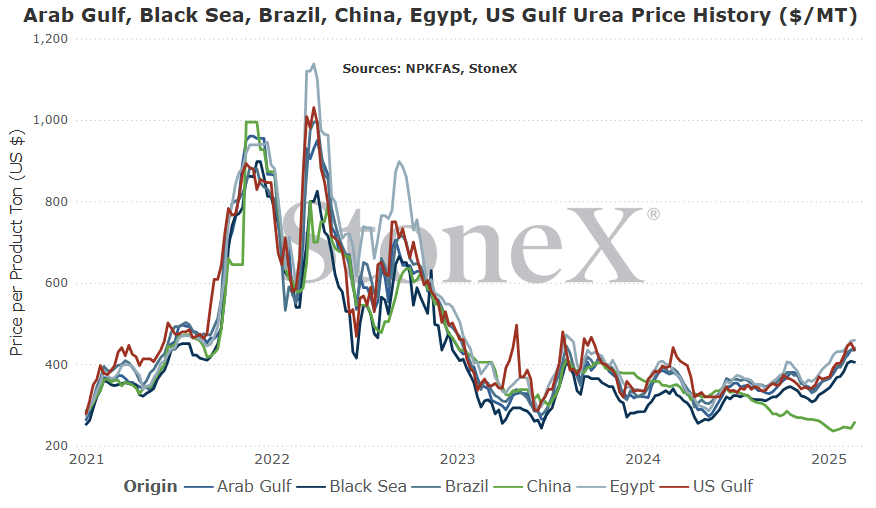

Number 1 exporter (as a region, not as individual nations)

Vs 30 days ago - 9% or approximately $35 higher

Vs 90 days ago - 25% or approximately $87 higher

Vs 6 months ago - 30% or approximately $100 higher

Vs 1 year ago - 16% or approximately $59 higher

Egypt

Number 4 global exporter in 2022

Price comparisons

Vs 30 days ago - 6% or approximately $28 higher

Vs 90 days ago - 31% or approximately $108 higher

Vs 6 months ago - 31% or approximately $108 higher

Vs 1 year ago - 15% or approximately $61 higher

Black Sea

Number 1 global exporter in 2022

Price comparisons

Vs 30 days ago - 9% or approximately $35 higher

Vs 90 days ago - 27% or approximately $85 higher

Vs 6 months ago - 30% or approximately $93 higher

Vs 1 year ago - 24% or approximately $78 higher

China

Number 9 global exporter in 2022

Price comparisons

Vs 30 days ago - 6% or approximately $16 higher

Vs 90 days ago - -4% or approximately $10 lower

Vs 6 months ago - -16% or approximately $48 lower

Vs 1 year ago - -26% or approximately $88 lower

- Iranian production remains offline - 1st, we didn't expect Iranian nitrogen production to go offline. 2nd, after coming to terms with their going offline, we didn't expect them to be offline for as long as they have been. This is the supply loss that was not expected. Every 30 days that their production is down, the world loses a further 400K tons that the world will struggle to make up. The global S&D is already tight. Iran is making that worse.

- India finally steps in to purchase - India has done a fantastic job of getting the market excited with rumors of their purchase tender, and then ripping the carpet out from under the markets feet by delaying. That has caused a lot of angst amongst "players". However, they cannot do this forever. Their December tender fell very short of tonnage goals. Their follow up January tender once again fell very short of tonnage goals. India needs to buy...just a matter of when.

- Chinese exports continue thin - the rumors that the Chinese government was going to allow exports to begin caused domestic values to spike. No doubt government officials saw that and will use that information in their decision making process. To start allowing exports to occur right before their spring season would fly in the face of the strategy they have used for over a year. It makes sense to believe that if they allow exports, it will not be until late Q2/Q3. That would mean nearby exports remain very thin, leading to a much tighter global S&D.

- India continues to drag their feet, causing an uncomfortable quiet - right now, it seems more of a "when" India announces their tender rather than "if". However, we could be wrong. Maybe India is doing much better on stockpiles than we believe. Maybe demand has slowed significantly, allowing imports to wait. I do not think so, but I do not work in a world of certainty. The longer India drags their feet, the more pressure it puts on the market.

- Iran/China exports return - Chinese exports returning seems a very low probability situation to me short term (thru spring), but it is possible. More possible is Iranian production returning, causing companies there to start selling product once again. Iran returning is likely more a "taking the worst case scenario off the table" situation, meaning prices shouldn't fall (should slow the rise). China returning would likely be seen as a very bearish event. Again, doesn't look likely, but it would be a major disrupter.

- Importers decide to wait for lower prices before purchasing - importers are in rough shape today in terms of what to do. Global prices have rallied hard to start the year, but have been bearish the last couple weeks. Do they step in huge at this dip? Do they drag their feet hoping it goes lower? There is plenty of risk either way but if they can wait and global prices continue to fall, Aussie based values should follow.

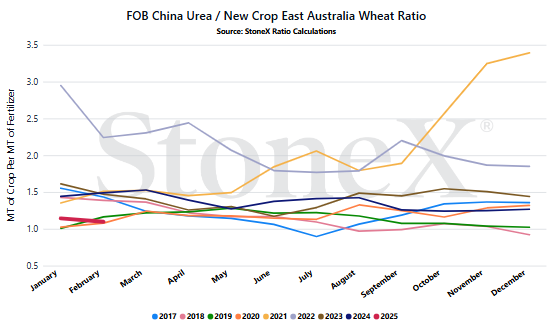

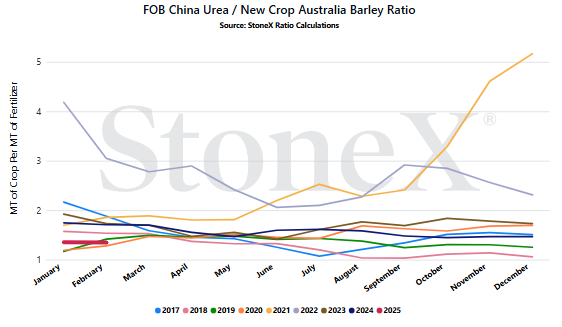

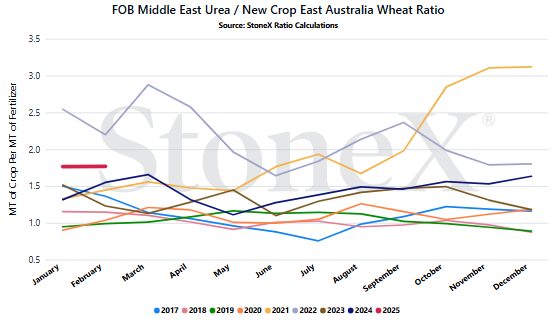

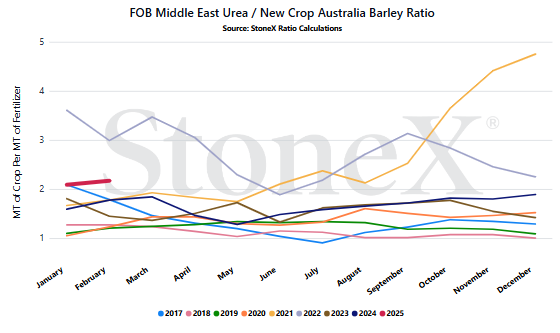

We believe that only looking at the flat price of either grains or fertilizer can be misleading:

-

Only selling grain can hurt you if fertilizer prices rise substantially

-

Only buying fertilizer can hurt you if grain prices fall

We look at the ratio "value" to get a better indication of where we are or how many bushels of X does it take to pay for 1 ton of fertilizer.

Would you rather:

-

Spend 135 bushels to pay for 1 ton of urea

-

Spend 55 bushels to pay for 1 ton of urea

When we compare the current ratio value against recent years, we start to see if we are high or low.

YOUR VALUES MAY LOOK DIFFERENT

This is a work in progress section! We plan on looking at the relationship between Aussie grains and global price points (and hopefully Aussie specific locations, though that data is hard to secure, very protected). Big reason why we are still in the "trial" stage of this newsletter!!!!

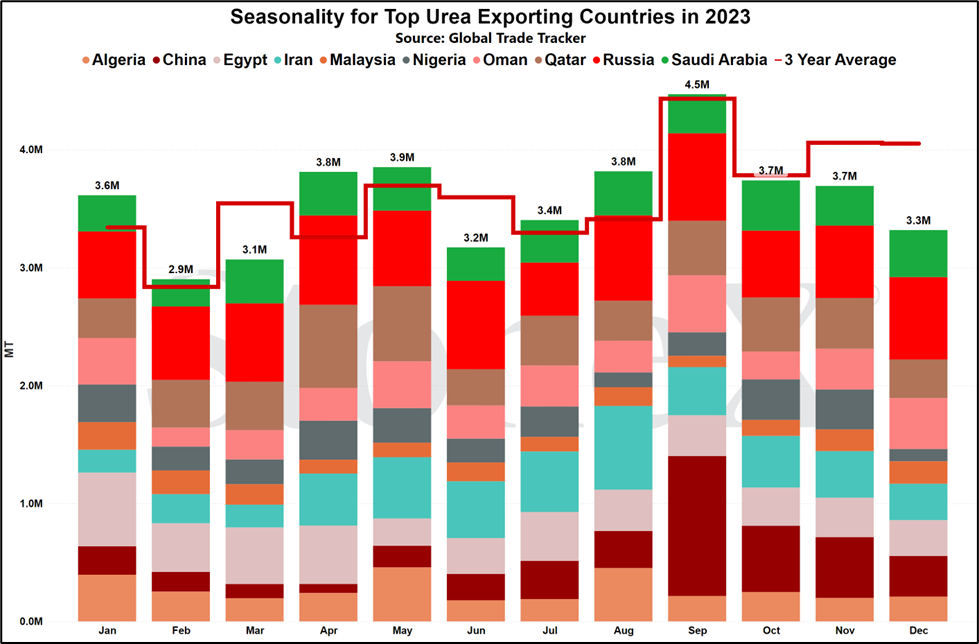

- Iran (since they should be first to come back) - Iran is the piece that we didn't expect. While it isn't crazy that Iranian production stopped, the fact that it has gone this long is. An even that we thought would be a couple week ordeal has now been going a month plus. Iran exported almost 5M tons in 2023, making it very near the same size as China who we talk a lot about. While many around the world will not do business with Iran, their exported ton counts just as much as everyone else's for the global S&D. The longer their production is down, the tighter supplies get.

- China (largest missing piece, rising questions of export programs) - it seems China is getting to a decision point. On the one hand, their stockpiles are heard to be at record levels. Production cannot continue at their current paces without exports being allowed. However, even the rumor that Chinese exports would be allowed caused domestic Chinese values to rise which is completely against the governments strategy. I do not believe exports will be allowed before their spring season, but it is China. We never truly know. Given how the world reacts to their exports (or lack of), what the Chinese government allows or disallows will matter significantly to the world.

- Europe (likely lower production rate for a while, gas costs worry me) - unfortunately, I do not list Europe as a "possible ramp up in production rates". Rather, we started to fear that we would lose MORE production. Gas values spiked and we heard that nitrate values were rising on the fear that if they didn't, further production stoppages would occur. Since that time, gas prices have calmed...but winter is not over. If prices start to spike again, we need to keep watch...

- India (market knows it is coming...but when) - talk about a head fake! It looked all but guaranteed that we would have heard India's much anticipated urea purchase tender by now. However, they have drug their feet and surprised the world. Unfortunately for them, they still need to buy and the world knows it. I am concerned for what values do when they finally do step in to purchase. Their purchase will be in direct conflict with a lot of other buyers.

StoneX Ratio Calculation

The ratio calculation is derived from Bloomberg historical grains values as well as fertilizer values from StoneX, NPKFAS, and Argus.

The calculation is simply dividing the fertilizer price by each grain price.

All data was sourced from StoneX unless otherwise noted.